Airbnb: 4Q24 Business Update

Growth Inflection Brings Confidence, but are Ambitions Stretching Too Far?

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

4Q24 Update.

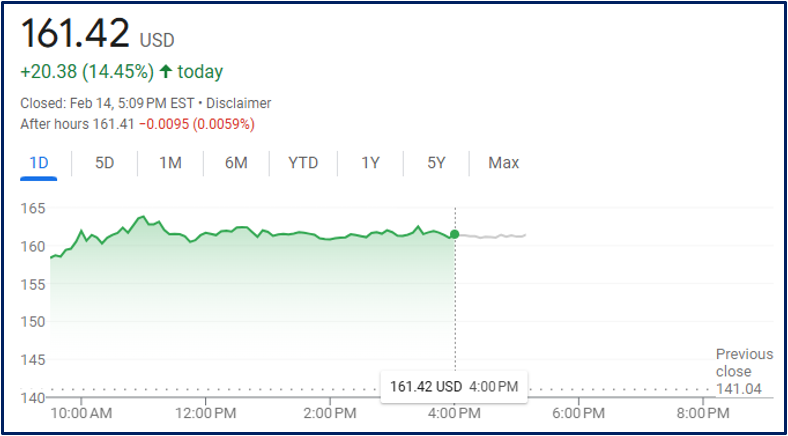

Airbnb reported 4Q24 and the stock was up +15%.

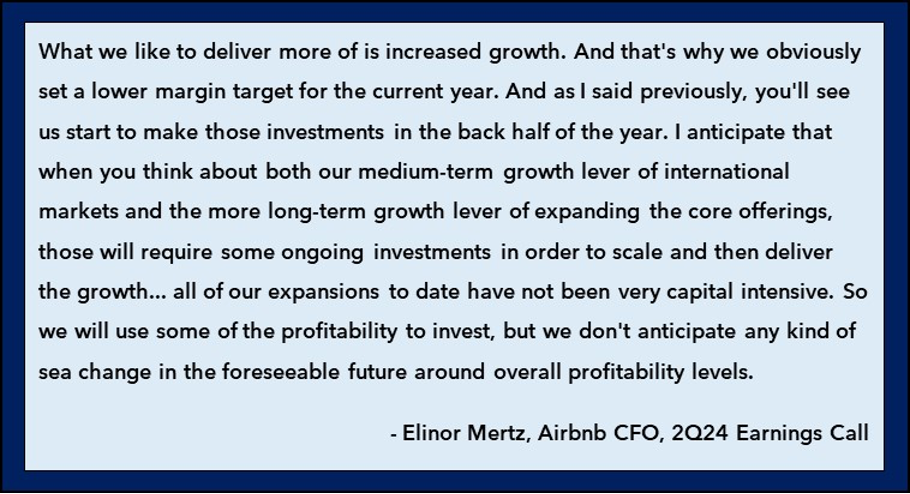

If you recall, over the past couple of quarters Brian Chesky and CFO Elinor Mertz, have called for an acceleration of growth. In 2Q24 Elinor Mertz said:

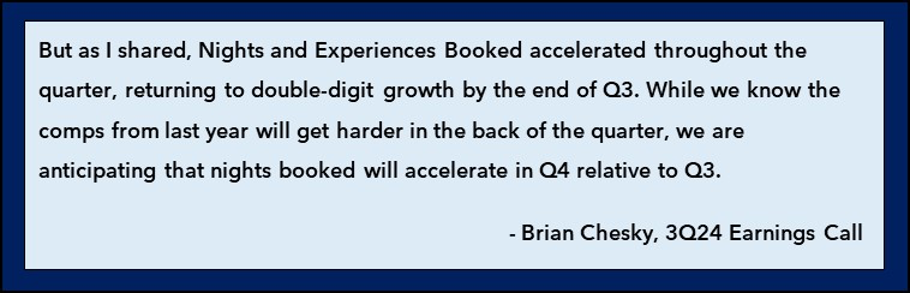

Last quarter Brian Chesky noted that:

The stock’s reaction suggests that the market was skeptical on Airbnb's ability to stoke growth, but this quarter seems to have put that question to rest.

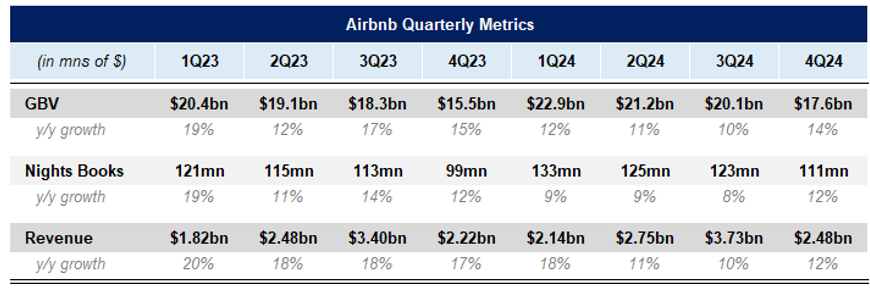

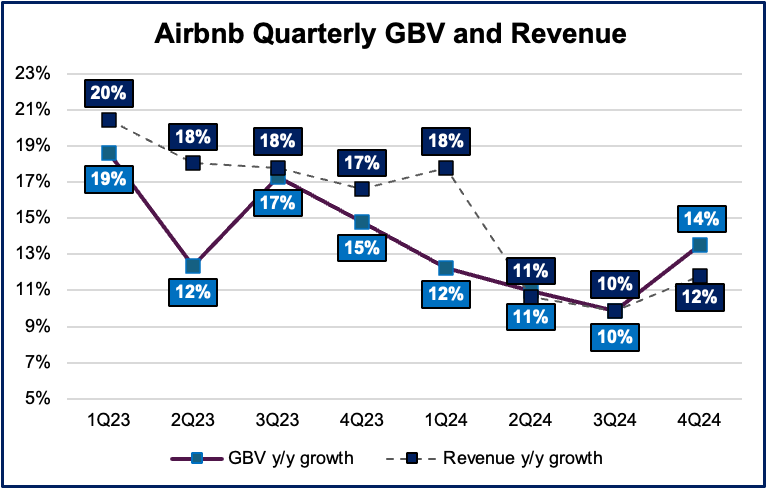

Revenue growth was +12% y/y, a 200bps sequential improvement from last quarter.

GBV accelerated even more to +15% y/y (FXN) compared to +10% y/y growth last quarter.

Nights booked also accelerated from +8% y/y growth in 3Q to +12% y/y in 4Q.

In terms of profitability, operating margins were 17.3% for the quarter, down from 19.6% in the same period last year. This margin contraction is largely driven by their increase in product development expenses.

If you recall, in 2020 Airbnb was deeply in the red, losing $3bn for the year. By 2022, operating margins were over 20%. They have since started to invest back into the business for more growth, which has weighed on margins, but they will continue to generate meaningful cash.

In 2024, after treating based stock based comp as a cash expense, they generated $3bn in free cash flow. Although, investors should be aware that about $800mn of this is from interest income from their massive cash pile of almost $11bn—and they also generate interest on $6bn of funds held on behalf of hosts.

While the float generated from the timing of when guest pay for a property and when it is disbursed for hosts is certainly an attractive aspect of the business model, no investor should put the same multiple on this “bank-like” stream of earnings. (We will touch on valuation later on).

We can still think of the core Airbnb platform as having generated over $2.2bn in free cash flow, which is incredible considering just 4 years ago that figure was a negative $4bn. They have started to flex their cash generating abilities, showing the strong economics that an internet marketplace platform can garner.

Business Commentary.

The inflection in GBV and nights booked is encouraging as it gives credence that many of Airbnb’s product roll outs were indeed geared towards growth and not just maintaining their current share. While many of their features seemed like things customers would like, it was unclear whether it would actually result in more bookings. The real fear was that as they continued to grow, they would be weighed down by the law of large numbers.

It’s worth pointing out too though that revenue growth of +12% y/y trailed GBV growth of +15% (FXN) as a lot of growth stemmed from lower ADR (average daily rate) international markets. Growth in new geographies vs their core markets wil likely weigh on revenue growth as their take-rates tend to be lower there. But nevertheless, there are many levers left for Airbnb to pull to increase revenue monetization (the most obvious of which is sponsored ads). The more important take-away is that the growth deterioration has been reversed.

Competitors like Booking and Expedia’s VRBO have continued to grow as well (BKNG hasn’t reported 4Q, but VRBO noted a sequential acceleration of growth). Ellie Mertz pointed out on the call that VRBO had a soft comp to explain VRBO's strength, but more to the point, she noted that Airbnb is still #1 in terms of supply coming online and new listings, the majority of which are exclusive to Airbnb. This portends well for Airbnb’s continued dominance in the alternative accommodation segment (see our research report for a fuller discussion on competition).

The big call option is on the Experience business relaunch and all of the other new business lines they will launch. Brian Chesky is positioning Airbnb to be more than just a travel company and it started with the tech re-platforming that would allow them to more rapidly launch new products. While he notes this has started several years back with 535 new products launched since they started their biannual product releases (with the majority in the past 2 years), these are relatively trivial compared to the multiple billion dollar business lines they are contemplating releasing each year (which admittedly almost sounds farcical).

While an investor likely doesn’t need to assume any success with these initiatives in order to rationalize a market-like return (see our Reverse DCF below), it could be a significant source of upside. Before moving into a discussion on that, it is worth pointing out the Brian Chesky continues to address all of the customer pain points with the core service successfully. When customers complained about high prices, they rolled out pricing tools to make hosts more competitive in setting rates, a new Rooms offering that supports the lowest end of the market, the ability to filter by total price including cleaning fees, and reduced fees on longer-term stays. When customers complained of lack of consistency (still an issue but improving), they rolled out guest favorites which have a much higher and more consistent guest experience.

Like the best operators, Chesky doesn’t talk much about take-rates or margins, but rather how to make the customer experience better. That is what tends to build the most consumer surplus overtime and allows for the most long-term value creation for investors.

It is with this lens in mind, we like to zoom out and speculate a bit on what the future could portend for an Airbnb that is about much more than travel.

BlueSky Option: SuperApp.

Before you dismiss a SuperApp as fanciful, you should know that Wang Xing, Founder of Meituan built a very large hotel booking business in China by coupling it with a food delivery business. 80% of Meituan’s users who booked a hotel used another one of their services first. With success in the food delivery and hotel booking business, Meituan continued to add a slew of different services like beauty, home renovation, bike-share, pharmacy, and many other local services. While not everything was successful, they definitely proved that once you have a user on your app, it is much easier to acquire them for another service.

This also isn’t a tactic exclusive to a handful of “SuperApps”. As we wrote in this memo on SuperApps:

Ben Thompson’s Aggregation Theory points out that in a zero-distribution cost, internet-enabled world competitive dynamics shift as physical barriers that previously contained competition are removed. This results in an increased focus on customer acquisition and retention since distribution is no longer a differentiator.

A classic means of increasing retention is to get a user to use your product more often. This is commonly done by growing offerings. Convenience stores are commonly paired with gas stations to increase frequency of visits. Markets traditionally may have sold primarily just groceries, but “Supermarkets” have not just a butcher and bakery too, but also may have a flower shop, pharmacy, bank, and coffee shop, in addition to selling a ton of household items. This is all to drive more traffic and build consumer habit, but there is also the ancillary benefit that the more offerings you carry, the greater your ability to monetize.

A supermarket groups together various offerings in hopes that each offering help feeds traffic into other offerings, while simultaneously allowing them to monetize better. The more offerings an individual consumer utilizes, the less likely they are to go elsewhere and the more valuable they become.

A SuperApp is no different.

A “SuperApp” is just an app that has an essential, high-frequency service that allows them to use that point of customer contact as a low-cost funnel for future customer acquisition of new products. The trouble most have with a SuperApp is building a strong enough foundation where it is a service that isn’t replaced and is used in high enough frequency that the app can cross-sell. It makes sense that Tencent’s WeChat—initially a messaging service—holds the title as the best SuperApp. In this context, it is also clear why Airbnb has been trying to improve in-app usage and not just in-app bookings (which increased from 55 to 60% most recently).

In-app usage is important because it grows the users relationship with the app and keeps them top of mind, which is important to cross-sell services. This is why Chesky was alluding to helping users do more in-app once the trip was booked. Brian Chesky basically realized that once you build a marketplace for something, you can sell anything. However, Airbnb needs to increase the user reliance on the app for more opportunities to cross-sell so new service don’t just stay dormant and unused.

He's laid out his vision clearer than ever before in this excerpt from the earnings call:

I think we're now ready for this next platform, next chapter to expand beyond our core where Airbnb is just a place to stay. And to do that, here's a couple of philosophies, couple of principles we have with our philosophy I'll share, and I'll also tell you a little bit about the friction.

Number one, I think, we can do this quite efficiently, because we are not going to launch separate apps or separate brands. We're going to have one app, one brand, the Airbnb app. And we want the Airbnb app kind of similar to Amazon to be one place to go for all of your traveling and living needs. A place to stay is just really, frankly, a very small part of the overall equation. Every new business we launch, we'd like to be strong, and I think it's standalone, but it makes the core business stronger. I think that each business could take three to five years to scale. A great business could get to $1 billion of revenue. It doesn't mean all of them will. And you should be able to expect like one or a couple of businesses to launch every single year for the next five years.

We're going to start initially with things very closely adjacent to travel. So when people book an Airbnb, there's a lot of like experiences and services and other things that would make their stay more special, and it would even include things they wouldn't think to search for. And from there, we're just going to keep expanding, and we're going to expand out to more host services to enable them to become better host, and then eventually, we'll move further and further away from our core. I think like, maybe the analogy of Amazon is a really good one, which is to say, they started with books. The nearest adjacency to books was DVDs and CDs back when people bought physical media. And then they went to like, I don't know, maybe toys and other things and eventually, they end up with fashion and pretty soon, they were doing things pretty far adjacent from media and books

So we're going to probably follow that path. So we're going to really, really start adjacent to travel. And part of the reason why is, a traveler booking a home, what else would they want to book. And the other great thing is that, we offer these other experience and services that could potentially bring in new guests that then book more homes in Airbnb. And I think one of the ultimate goals is, Airbnb is used by, like, I think, 1.6 billion devices a year. So it's got pretty big volume of users, but we're not a very frequently used app. People typically use us once or twice a year. And I would love Airbnb one day for people to use us once or twice a week. And so that's kind of one of the goals over the long term.

As we mentioned in our research report, it is likely they start with tangential services like a cleaning/ housekeeping marketplace so Airbnb hosts can offer housekeeping services and compete more against hotels. Co-hosting–where a host who doesn’t own a property and is connected to someone who has a property, but doesn’t want to host–is sort of small step in this direction. Over time though, really any service can be added to the app. It is more a matter of user receptivity to using Airbnb for all of these services and their ability to build network density for new offerings.

The big thing is creating verified users with preloaded payment information to reduce friction, which they already have for many users. (And is also why they have pushed people to upload photos and fill out more info–it could be useful for other services down the line). The push into Experiences, which is a unique offerings, could further help bolster the number of user profiles, while also getting people more used to using the app for a variety of different things. At the extreme, Experiences could be used by people to book services while they are in the city they live in—not just for tourist. This would greatly expand usage and eventually could bleed into Yelp territory (which has been an incredibly under monetized asset and missed business opportunity).

While this all may be fun to think about, it is all very, very hard to execute on. Some of the more tangential opportunities like cleaners seem to be very reasonable, but as they get farther out of their core, getting a successful 2-sided network for each of these business is much harder.

Earnings Call and Shareholder Letter Notes.

Product Development

Rolled out more than 535 features and upgrades

Rebuilt platform

“optimizing key parts of our product, like search, merchandising and payments, we're seeing strong near-term results, and we're building a foundation to support the introduction of new offerings”“what it's going to lead to is, fewer engineers being able to basically ship features faster. And so there's a pretty, pretty huge gain here”“new listing management tools for host, and these tools make it easier for hosts to list and manage their homes while giving them the ability to eventually offer more services”

The ease of listing is one of the primary reasons that independent hosts only use Airbnb and not competitor platforms.

“With this new tech platform, we are able to innovate faster and expand beyond short-term rentals into becoming an extensible platform with a range of new offerings”

Growth

“Our strategy is designed to drive long-term growth and deliver market share gains through three levers: one, perfecting our core service; two, accelerating growth in global markets; and three, launching and scaling new offerings. We're focused on strengthening the economics of our core business and generating strong free cash flow, while also investing in growth opportunities”

“our business is concentrated in our top five core markets. So that's US, UK, Canada, France, and Australia. Those five markets comprise about 70% of our gross booking value. And so, as a growth lever that we've been investing in, we've been targeting markets outside of that top five, where we think there's a sizable opportunity for us to invest and both gain penetration in the markets and also provide a tailwind to our global growth rates.”

Advertising

“I think it's like almost every marketplace that successful has done this. We've looked at this. We definitely think this is easily $1 billion revenue opportunity. It's not a matter of if, it's a matter of when.”

“It's not the most perishable opportunity. So it's not something we'll be doing this year, but it's definitely something on the horizon”

This is the first time Brian hasn’t wavered on saying whether they would do ads. Noted it won’t happen this year.

VRBO

“ I think one of the underlying questions I'm sure people have is vis-à-vis Vrbo and their strong performance in Q4. What I would say there is that, Vrbo, obviously, had a very soft comp in terms of their business contracting in the US or globally in Q4 of 2023. And in the last quarter, what we see is that, the markets that we tend to compete against them in, in particular, non-urban US markets, it was actually one of our fastest-growing segments in the US. So even in that comparison point, we feel like we're doing quite well”

“The other point I would make on the competitive front is that, we continue to see that on the supply side, we are, number one, leading in terms of total supply growth, and number two, in terms of the new listings coming online, the majority come to Airbnb and the majority are exclusive. So further extending our differentiation with regard to both the breadth, but also the differentiation of the supply that is key to the brand and key to the guest value proposition for Airbnb”

App Frequency

“So that is part of our criteria in terms of selecting new offerings is, what if added to the platform would actually likely cause people to, one, book more frequently in terms of accommodations, but also come back to the app or the service on a more frequent basis than they do today, because we have a variety of offerings that may work not just on their trip, but also when they are in their home markets”

“We also saw a notable acceleration in the number of first-time bookers on our platform”

Mobile app bookings increased from 55% to 60% of nights booked

Capital Allocation

Repurchased $838mn shares in 4Q, $3.4bn total for the year, representing a 2.7% share count reduction for the year

$3.3bn remaining under prior authorized stock repurchase plan

Geography

North America saw mid-single digits Nights and Experiences Booked growth y/y, an acceleration relative to 3Q24

EMEA saw low-double digits Nights and Experiences Booked growth in y/y. ADR increased 6%

Latin America saw low-20s Nights and Experiences Booked growth y/y. We continue to see the highest level of growth for domestic travel with these nights increasing 30% compared to the same prior-year period.

4Q24 saw growth in the number of first-time bookers in Latin America accelerate nearly 15 percentage points compared to Q3.

Brazil continues to outpace other countries. Launched local payment method, Pix, in Brazil.

Asia Pacific saw low-20s Nights and Experiences Booked y/y. Saw strong growth domestically, cross-border continues to drive the majority of nights booked in APAC. In fact, in 4Q24, cross-border nights booked increased 27% year-over-year

Network

Ended Q4 2024 with more than 5 million hosts and over 8 million active listings around the world

Removed 400k listing since quality system review introduced in 2023

Observed reduction in customer service issues and fewer credit card charge backs with higher guest NPS

Co-hosting network grown to 100k listings and these listings earn 2x comparable listings

Guidance

Revenue growth of 7-9% excluding fx impacts. However 1Q24 is an unfavorable comp with Easter and a Leap day, absent of which revenue growth guidance would be 10-12%.

Nights books relatively stable

Plan to invest $200 million to $250 million towards launching and scaling new businesses to be introduced later this year

Inclusive of these investments, we expect to deliver a full-year Adjusted EBITDA Margin of at least 34.5%

Valuation.

The rest of the valuation section is paywalled.

If you are a Speedwell Member, please click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post, our 108-page Airbnb Research Report, and a large library of other reports!

As a reminder, we named our research firm Speedwell Research after the ship that helped ferry passengers to the Mayflower. The idea is that we want to help you take your journey, but ultimately you are on your own in the decisions you make. An investor must judge for themselves whether they believe these returns are worth the potential risks that could materialize with Airbnb.

The Synopsis Podcast.

Follow our Podcast below. Evolution’s Todd Haushalter will be featured next week!

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Airbnb report and all of our other in-depth research reports, shorter exploratory reports, updates, and Plus members also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in ABNB. Furthermore, accounts one or more contributors advise on may also have a position in ABNB. This may change without notice.