APi Group: 2Q25 Business Update

Revenues Reaccelerate, Strong Organic Growth, 2028 Long-Term Targets

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(If you are a Speedwell Member click here for the member's version of this post or here for the PDF).

Business Summary.

Since APG is one of the newer companies added to our coverage, we wanted to give readers a quick summary of their business as a reminder. If you are familiar with them, you can skip to the update.

APi Group is a global leader in fire and life safety services with over 500 locations worldwide. They focus primarily on statutorily mandated and other contracted services to a diverse collection of industries. They are structured on a regional operating model so each operating group can quickly respond to customer needs and have more ownership over operations. This makes APi Group a sort of “platform” with support for purchasing, back office, and various other support functions, while giving each franchise autonomy to respond to their clients' needs.

They operate through two segments: 1) Safety Services and 2) Specialty Services. Safety Services comprises about 75% of revenues with Specialty Services accounting for the rest. Safety Services offers mission-critical services for life safety systems such as fire sprinklers, alarm systems, backflow prevention, remote monitoring, access control, and security. Since acquiring Elevated in 2024, they also do elevator maintenance.

Their specialty services offer construction, installation, and servicing for infrastructure & utilities. They also provide specialty contracting, fabrication, and HVAC services. For more info on what all of these services are, please see the Business section in our report.

APi Group’s model is to lead with inspections first. What that means is that they will inspect a customer’s services and then try to win a service contract thereafter. Inspections are very often mandated by law and customers want someone who is well known and competent to avoid any potential issues with their facilities. The inspections are not particularly expensive, but they use them to build a customer connection. After an inspection, APi Group can then help them fix any potential issues with their systems or put them on a schedule for regular service (which is also often required by law).

This differentiates them from their competitors who try to win customer’s service business by doing their construction first and then cross selling a service contract. APi Group’s model is better though because it allows them to avoid having to do lower margin contracts just to win service business. For each $1 in inspection service they earn, they generate $3-4 in service revenue. They also do projects though, so their customers do not have to go to a competitor, which could otherwise potentially open the door for them to lose their service contract. However, they are selective with the projects they take on and avoid “bid-based” work.

The markets they operate in are fairly fragmented with no large player having more than ~10% market share. They can be quite acquisitive but are very disciplined with their purchase prices. Right now they intend to deploy about $250mn a year in bolt-on M&A at mid-single digit EBITDA multiples.

For a more thorough background on APi Group, check out our in-depth research report. Now on to the update.

2Q25 Update.

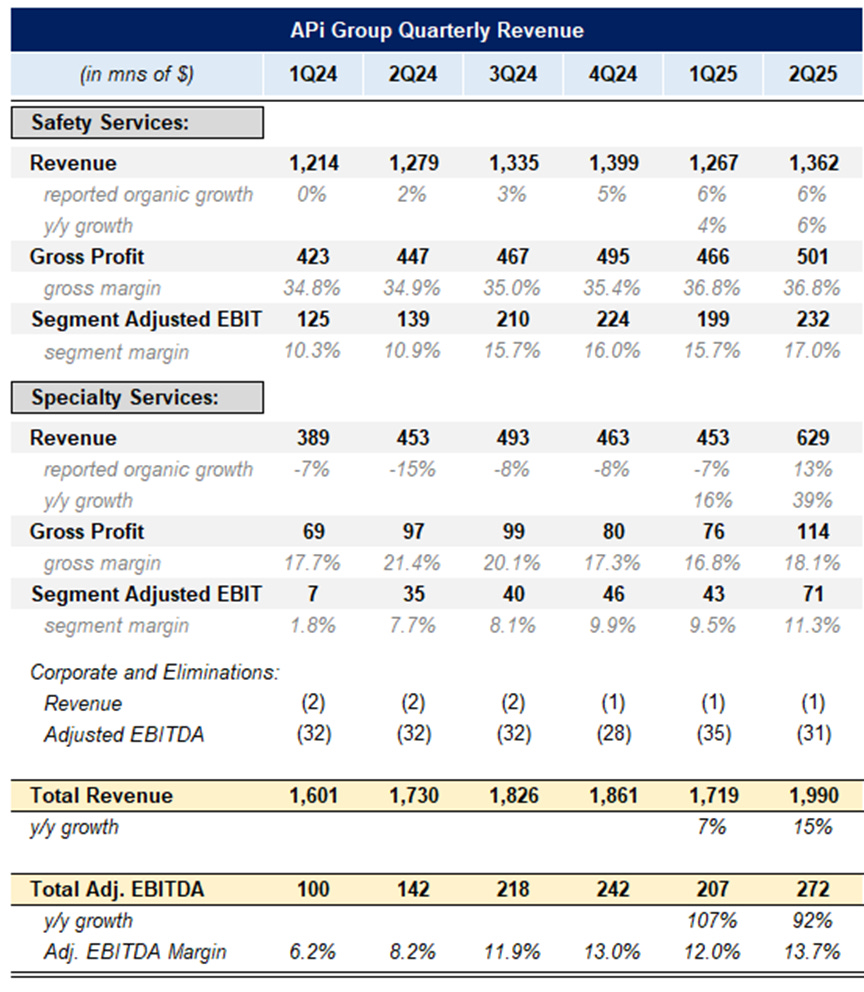

APG reported a strong 2Q25 with revenue growth accelerating +15% y/y, up from +7% last quarter. Organic growth was strong at +8% y/y versus +2% last Q. Within that, the more important safety services segment grew +5.6% y/y, which is in line with last quarter.

They noted that their inspection revenues (which are housed in the safety services segment) grew double digits for the 20th straight quarter. This is an important source of revenue because it tends to be a leading indicator for other service revenue down the line. As a reminder, they try to acquire new customers by doing their inspections first and if they have something that needs service, APi Group is well positioned to provide it. They tend to generate $3-4 in service revenue per dollar of inspections.

The specialty service segment saw +13% organic growth. If you recall, they have been rationalizing revenue from this segment as many of the projects they were previously doing were low-margin and occasionally loss-generating. That is why CEO Russell Baker clarified that their backlog (which reached a record $4bn+ this quarter), “focuses on our target end markets and is healthy from a disciplined customer and project selection perspective.” APi Group has been very focused on profitability over volume.

In terms of M&A, they completed 6 acquisitions this quarter, including their second acquisition for their elevator business. They entered into the elevator business just a year ago with a platform acquisition of Elevated and have used that as a base to start to roll-up more elevator operators. They believe there is a $10bn opportunity here despite a couple larger player having a much earlier start (namely Otis, but there are others).

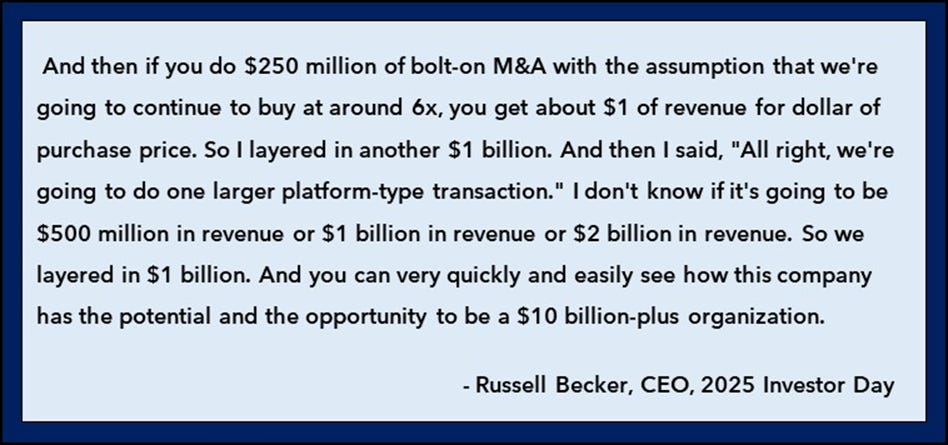

They are on track to deploy $250mn into acquisitions this year, which is up slightly from the ~$220mn they did the last 3 years. APi Group increased their credit facility to $750mn from $500mn and with their leverage ratio at just 2.2x (below their prior target of 2.5x), they are in a good position to continue to be acquisitive. CEO Russell Becker gave some more color on acquisitions and the potential for a larger platform acquisition at the investor day.

They bumped up guidance to $7.65-7.85bn in revenue, increasing the range by $250mn. Adjusted EBITDA was also increased to $1-$1.045, representing a margin of 15% at the midpoint. CFO Glenn Jackola commented “you can think of our EBITDA raise as 1/3 of it driven by our Q2 over delivery, maybe 1/3 of it due to M&A in the quarter and maybe 1/3 of it due to an increase or an improvement in our second half business outlook.”

Business Commentary.

Overall this was a very strong quarter of execution; APi Group continues to deliver on what they set out to.

As a reminder, APG had prior targets they called “13/60/80”, which represented 1) 13% adjusted EBITDA margins, 2) 60% of revenues from inspections, services, & monitoring, and 3) 80% free cash flow conversion. While they hit their 13% adjusted margin target last quarter, this quarter they again cleanly exceeded it with an adjusted EBITDA of 13.7%. This was despite some gross margin pressure driven by rising material costs, increased projects starts, which was offset by some pricing and project discipline. GAAP gross margins contracted 50bps y/y to 31.4%.

At the beginning of May they had an investor day and announced update long-term targets. Their 2028 targets are now called 10/16/60+. Their 2028 targets are 1) over $10bn in revenues, 2) 16%+ adjusted EBITDA margin, 3) 60%+ of revenues from inspections, services, & monitoring, and 4) over$3bn in cumulative adjusted free cash flow through 2028. They also added revenue growth would be supported by mid-single digit organic growth (so can’t be purely from acquisitions).

The slide below showcases their 2028 targets. Their new 16% adjusted EBITDA target likely translates to about a 14.5% EBIT margin given historical D&A as a % of revenue is 1.5%. In our reverse DCF below we will talk more about margin assumptions.

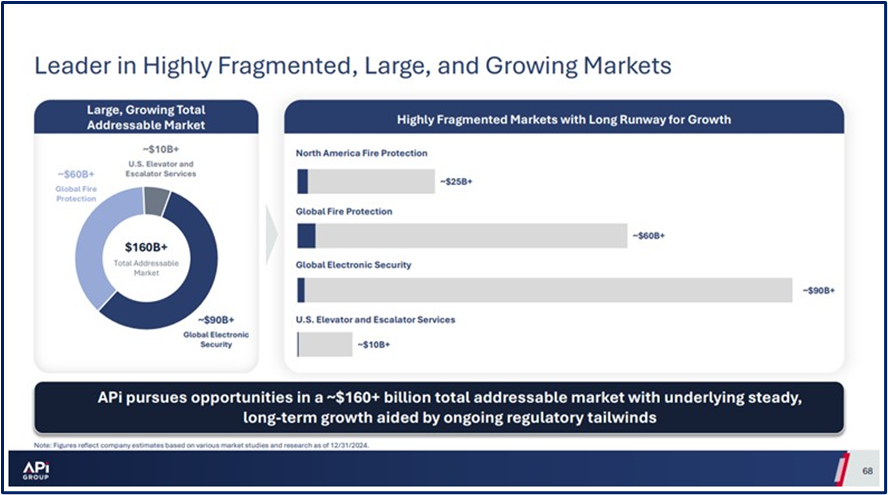

We can see below how there is plenty of runway left for M&A growth in all of their markets. On the call they noted that the big spend in data centers is also creating a lot of new opportunities for both of their segments. This is likely one of the larger factors that drove the specialty segment’s organic growth this quarter. Still though, they are broadly diversified across end markets. Although it is an open question if they are willing to increase exposure to data center given it is a fast growing market with a lot of service needs and high quality customers.

CEO Russell Becker summarized the quarter well below. We will next move on to valuation.

Valuation.

With APG stock up 51% YTD, we wanted to refresh our Reverse DCF valuation....

The rest of this update is only accessible to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post! You will also get our 61 page APG Research Report and a large library of our other reports and updates!

For further reading, check out our APG Extensive Research Report.

The Synopsis Podcast.

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Meta report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered Appfolio, APi Global, Airbnb, Axon, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in APG. Furthermore, accounts one or more contributors advise on may also have a position in APG. This may change without notice.