AppFolio: 4Q25 Business Update

Revenue Reaccelerate with new AI-Features

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

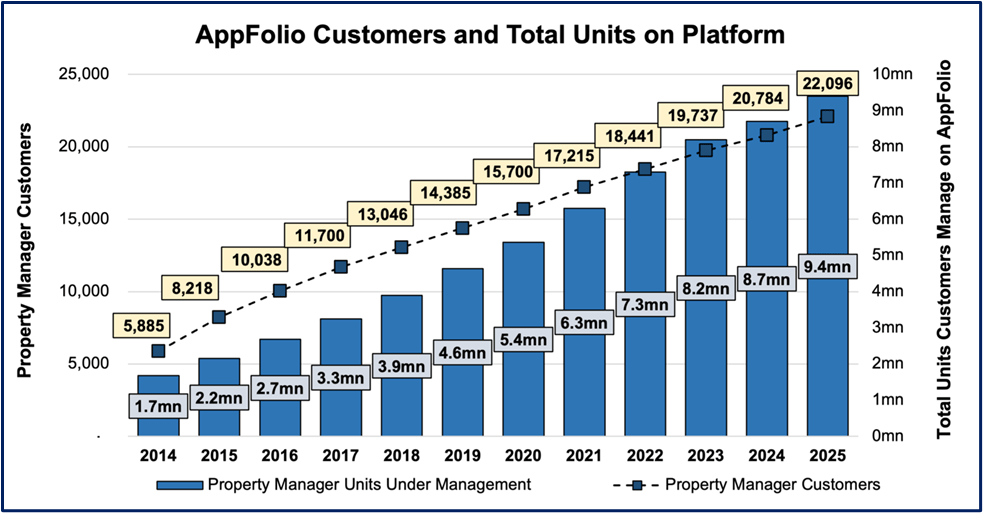

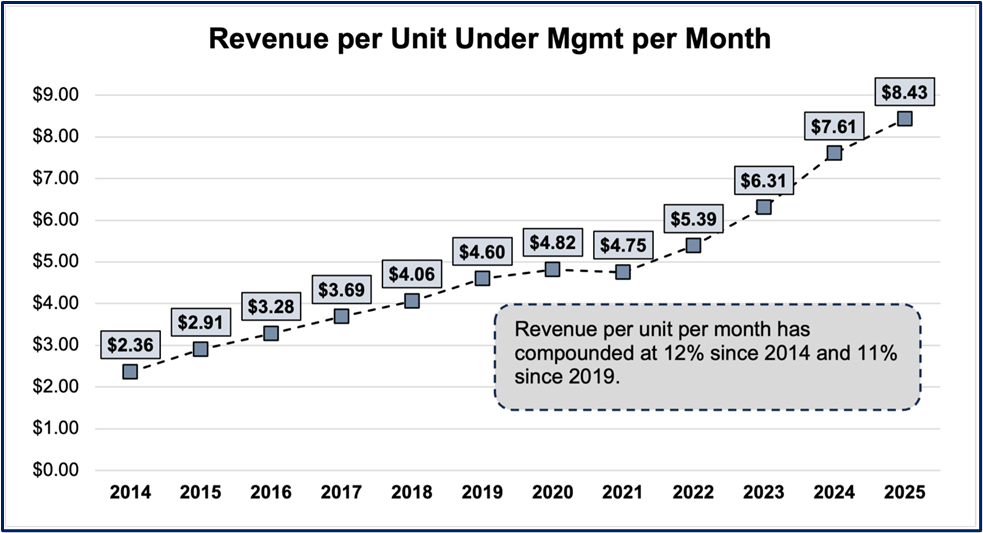

AppFolio is a leading vertical market software provider for property managers with a focus on the small to middle market, however they been pushing up market recently. Their software product is very sticky and they are constantly adding more functionality to it, which has allowed them to upsell customers. They charge property managers on a per unit basis and currently have 9.4 million units on their platform. On average, they generate >$8 in revenue per unit per month. For more background, see our report here.

(Members can find a fuller version of this post here and a PDF here)

4Q25 Update.

AppFolio reported decent 4Q25 results and the stock was down -8% in next day trading.

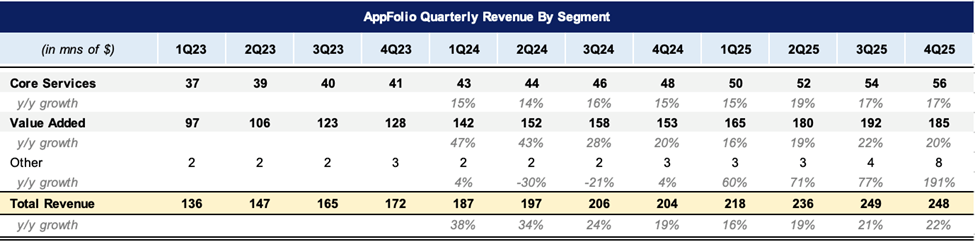

Revenues accelerated 100 bps to 22% y/y. This marked the 3rd consecutive quarter of acceleration after a soft 1Q. However, full-year 2025 revenue growth is still lower than last year at 20% vs 28% in 2024.

Core Services revenues grew 17% y/y to $56mn in the quarter, driven by 1) winning new customers, 2) growth in total units under management, and 3) more customers choosing their plus and max premium tiers. They mentioned that adoption for plus and max premium tiers exceeded 25%, which suggested some more success with penetrating the largest property managers. As a reminder, they have traditionally focused on SMB property managers and only recently gone up market. The initial foray into the end of the market was met with significant investor skepticism as incumbents like Yardi have long dominated that area. It is encouraging to see them already get some wins despite a product that is generally lacking in the complete feature set (particularly accounting) that complex property managers want. (See our 2Q25 update here for a more full competitive analysis).

For full-year 2025, Core Services revenues accelerated 180bps to +17% y/y from 15% in 2024. (On the call, they noted that they are renaming this segment to “Subscription Service Revenues” going forward.) At the end of the year, AppFolio ended with 9.4mn units from 22,096 customers, which is up 8% y/y and 6%y/y, which is a reacceleration of 200bps from last year.

Meanwhile, Value Added Service revenues grew 20% y/y in 4Q to $185mn, down -200bps from 22% last Q. For the full-year 2025, total revenues grew 19% to $722mn, which was a deceleration of 14 points from 33% last year.

Keep in mind that as they roll out more premium packages, they may include some value added services and so that revenue get’s booked in the Core Services line, but it is not indicative of the features being less demanded. On the call they mentioned that they continued to see great use and adoption in FolioGuard risk mitigation services, Folio Screen offerings, and online payments, with newer offerings such as Resident Onboarding Lift and LiveEasy beginning to contribute incrementally.

While the company exited the year with strong low 20% growth, their 2026 guidance calls for a slight moderation of growth. Management is guiding for a deceleration of revenue growth at 17% to $1.1-1.12bn, with cost of revenues being flat y/y/ for 2026.

Turning to profitability, gross margins improved slightly to 64% q/q, and GAAP operating margins expanded 400bps to 18%. Driving this increase in operating margin for the quarter was a 320bps decrease in R&D expenses as a % of revenue, and -180bps decrease in G&A as a % of revenue, showing some operating leverage. S&M spend however, did increase 180bps to 16% of revenues.

For 2025, GAAP operating margins fell -100bps to 16% due to higher S&M spend. In addition, operating margins declined due to performance levels attained under their 2025 corporate incentive plan, which resulted in an additional expense of $15mn.

On the call, AppFolio CEO Shane Trigg noted a benchmark report that stated 77% of property managers expect to increase unit counts in 2026. This number was 65% a year ago, which signals that property manager expectations are increasingly positive for 2026. In addition, Shane Trigg mentioned that 98% of AppFolio’s customers are using one or more AI capabilities on their platform. And 45% of say they plan to consolidate their software solutions, which is key to AppFolio’s value prop as their unified platform simplifies a property managers operations. It is also worth mentioned that their platform is built to quickly iterate off of, which has allowed them to be first to market with many AI-enabled featured.

CEO Shane Trigg reiterated three strategic pillars guiding the company: differentiating through AI-driven product innovation, delivering value efficiently through premium tier adoption and workflow automation, and sustaining a strong internal culture. Initiatives such as Realm-X agentic AI capabilities, new integration partners like Genesis for rent recovery, and bundled services such as Group Rate Internet are intended to deepen platform engagement and increase wallet share among existing customers.

Overall, AppFolio continues to execute well by expanding their offerings and increasing their revenue per user. While competitors have lagged in rolling out AI-enabled tools, AppFolio’s streamlined and comprehensive platform positioned them well to not only grow revenues, but to acquire customers as well. Their success here is showing up in the numbers with revenue growth reaccelerating after the launch of these features. There is still much more for them to build though.

Valuation.

At a $185 stock price...

The rest of this update is only accessible to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post! You will also get our 66-page AppFolio Research Report and a large library of our other reports and updates!

For further reading, check out our 66-page AppFolio Research Report.

The Synopsis Podcast.

Follow our Podcast below.

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our AppFolio report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered Appfolio, APi Global, Airbnb, Axon, Casey’s, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, LVMH, Meta, Perimeter Solutions, Porsche, Shift4, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in APPF. Furthermore, accounts one or more contributors advise on may also have a position in APPF. This may change without notice.