Axon: 2Q25 Business Update

Growing over 30%... What's Priced In?

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members click here for an extended version of this post or here for a PDF)

2Q25 Earnings.

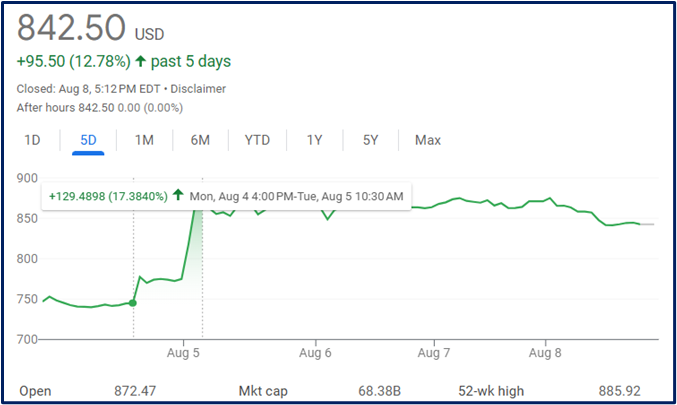

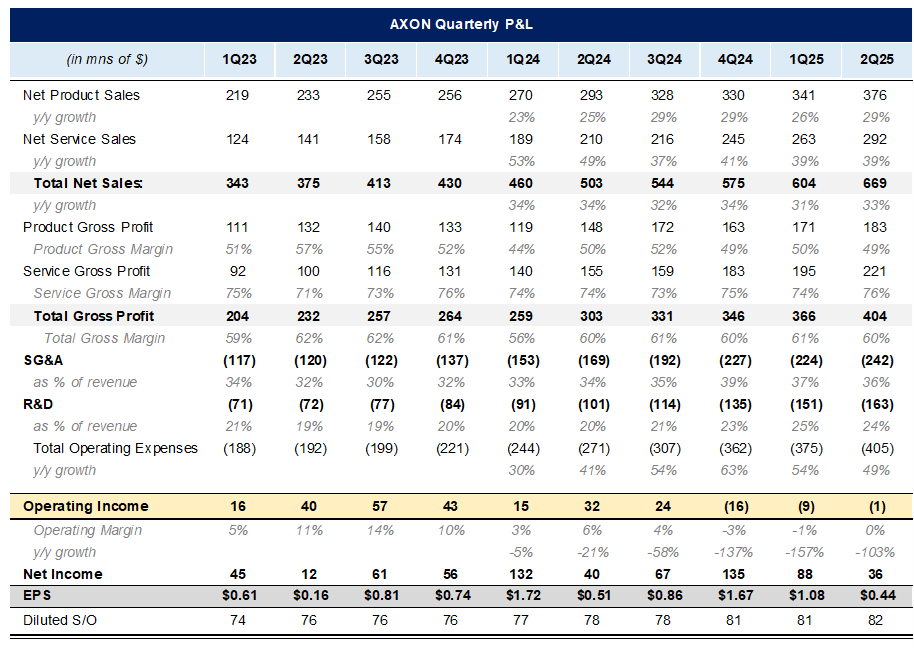

Axon reported 2Q25 earnings and the stock was up +17% the next day. Axon’s results marked the 14th consecutive quarter of 25%+ growth and 6th quarter of 30%+ growth. Total revenue growth improved sequentially to +33% y/y from +31% last quarter. Both product and service segments saw continued momentum and adoption.

Net revenue retention increased slightly to 124%, up 100bps, which is the 20th consecutive quarter over 120%, underscoring customer stickiness and their ability to consistently upsell and renew contracts.

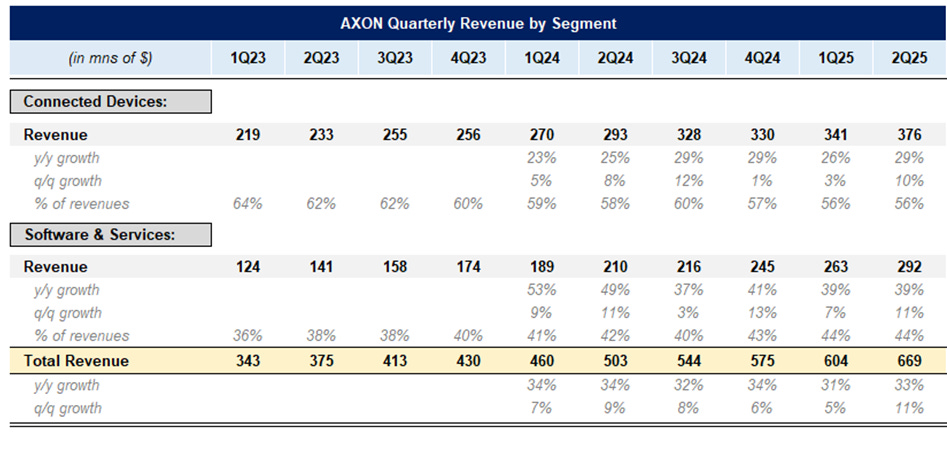

It is important to note that in the beginning of the year, Axon updated their operating segment reporting to Connected Devices (which includes TASER, cartridges, body cams, sensors, counter drone, and VR) and Software & Services (Evidence.com, Draft One, and other AI workflow tools).

Their Software & Service Segment continues to be a bright spot for them. Total revenues grew +39% y/y, a 4 point acceleration q/q, but down 10 points from 2Q24 growth rate of +49%. Still, this is phenomenal revenue growth.

Underpinning this growth is new users and the ability to drive Axon’s newest products. CFO Brittany Bagley mentioned that “approximately 70% of our domestic user base is still on our basic plans.” This means Axon has ample opportunity to upgrade them to higher premium plans, which could be a long-term tailwind.

Their Connected Devices Segment saw revenues increase +29% y/y, a 4 point acceleration y/y from +25% the year prior and 7 point increase q/q. Within the segment, TASER revenues grew +19%, driven by TASER 10—their newest version that gives officers more range and 10 shots. Personal Sensors grew +24%, driven by the Axon Body 4. Platform Solutions grew +86% y/y, led by counter-drone and virtual reality. Drones are going to be a be growth avenue for them.

Axon’s ability to garner higher adoption rates for their solutions is a testament to their long-lasting build of trust, obsession over the consumer, and focus on product innovation.

On the call, CEO Rick Smith noted the quick adoption Axon’s solutions are seeing.

With all the positive momentum Axon is seeing across their ecosystem, they raised their 2025 revenue guidance to $2.65bn-$2.73bn, from $2.6bn-$2.7bn, representing an annual revenue growth rate of ~29%.

Product gross margins slipped slightly –1 point to 49% due to lower device margins from strong growth in new hardware products and new markets. However, offsetting this was Software & Services gross margin expanding slightly by 2 points to 76% (the highest since 3Q23). Total gross margin remained steady at 60%.

In the quarter, Axon increased their R&D spend +38% y/y. R&D is now run-rating at 24% of revenues, almost 6 points higher than 2020. Over the same period revenue growth accelerated, despite them now generating as much revenue in a quarter as they used to in a year. With the success of the TASER 10, Axon plans to increase manufacturing capacity. This prompted them to update their capex guide to $170-185mn, up from their previous guidance of $160-180mn

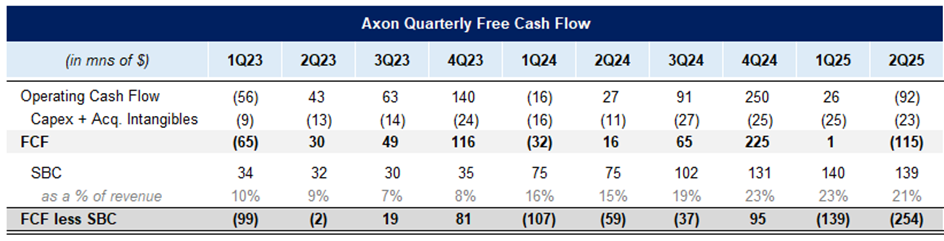

However, revenues have not been translating into cash flows. The nature of recording most revenues from a contract upfront and receiving cash for it over the term, plus ample stock comp has meant tepid free cash flow. After backing out SBC, they burned $250mn this quarter. Investors aren’t complaining though given the growth figures they are putting up.

Business Commentary.

Despite very high penetration (>90%) with the law enforcement departments in the US, they have ample room to expand their relationship with existing customers and grow internationally. On the call, President Joshua Isner called out that the largest deal in Axon’s history occurred in the quarter, “This team took back the record for the largest deal in Axon company history by a wide margin. This contract with a major city department also marked the largest contract we’ve seen in terms of new product bookings, encompassing everything from drones to our AI products.”

Key to growth...

The rest of this update is only accessible to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

Click below to access the rest of this post, as well as our in-depth 75 page report on Axon, PLUS a large and growing library of other deep dives and business updates.

For further reading, check out our Axon Extensive Research Report.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Coupang (Apple, Spotify).

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Coupang report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered APi Global, Airbnb, AppFolio, Axon, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in Axon. Furthermore, accounts one or more contributors advise on may also have a position in Axon. This may change without notice.