Axon: 3Q25 Business Update

Can they outexecute their valuation?

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members click here for an extended version of this post or here for a PDF)

3Q25 Earnings.

Axon reported 3Q25 earnings Tuesday and the stock closed -9% after initially dropping -20%. It faced continued pressure though and is now down -18% at $590 from its pre-earnings price of $720.

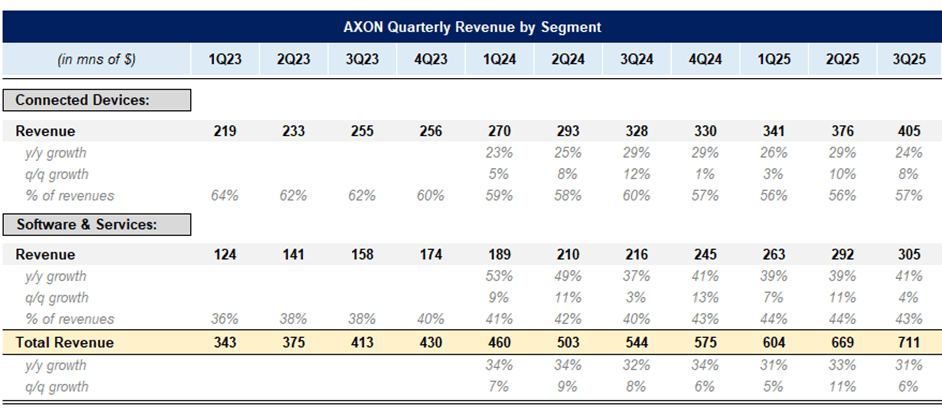

This quarter marked the 15th consecutive quarter of 25%+ growth and the 7th quarter of 30%+ growth. Total revenue rose +31% y/y to $711mn, a slight deceleration from +33% y/y in the prior quarter. Net revenue retention remained robust at 124%, consistent with last quarter and marking the company’s 21st consecutive quarter over 120%.

Breaking down their $711mn total revenue by segment, Software & Service Segment accelerated again to +41% y/y, a 200 bps increase from last quarter’s growth rate of +39%, driven by adoption of premium software features and an expanding user base. However, the Connected Devices segment slowed, growing +24% y/y to $405mn, a -500bps contraction from the prior quarter. Within the segment, TASER revenues grew +17%, Personal Sensors rose +20%, and Platform Solutions increased +71%. Each category saw a slight contraction in growth from the prior quarter, but growth remained steady.

With continued success they are seeing across their ecosystem, they’re raising their revenue guidance for the remaining of the year. They expect 4Q revenue between $750-$755mn, and full year revenue of $2.74bn up from $2.65-2.73bn, representing an annual revenue growth rate of ~31%.

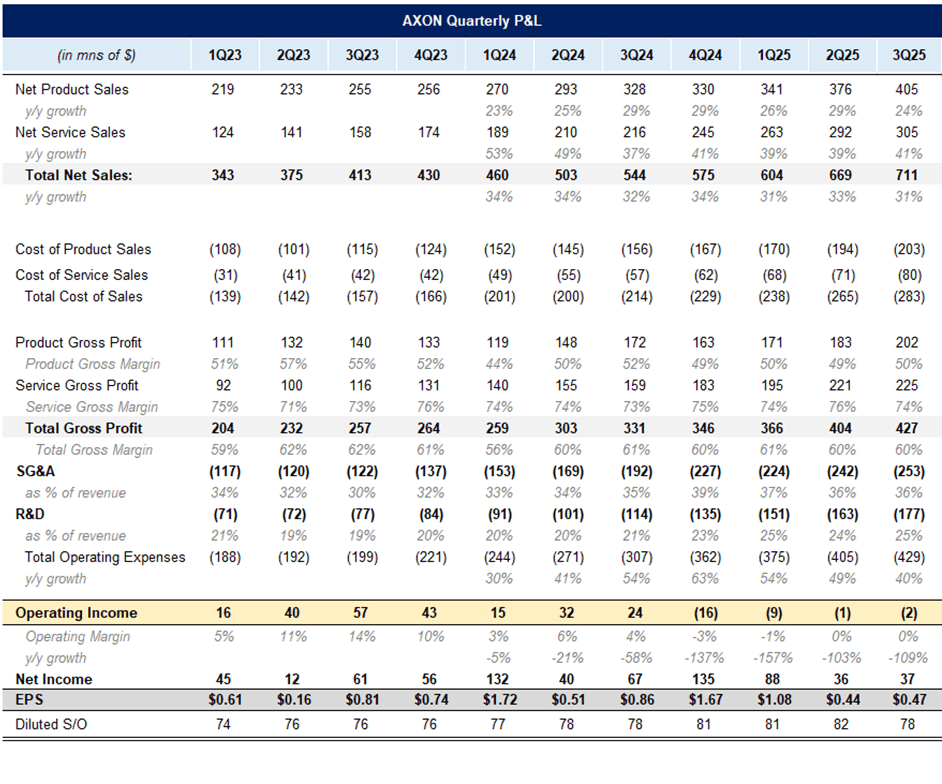

Turning to profitability, total gross margins held steady at 60%. Product gross margins improved +100 basis points to 50%, however offsetting this was Software & Services margins contracting -200bps to 74% from 76%. CFO Brittany Bagley noted that this was the first full quarter to feel the effect of tariffs, primarily in the Connected Devices segment, though production shifts to India and Vietnam helped offset some of the pressure.

Axon continues to increase their R&D spend as they build out the TASER 10 and innovate new product offerings. In the quarter, R&D rose +54% y/y, but despite this increase, R&D is still running at 24% of revenues.

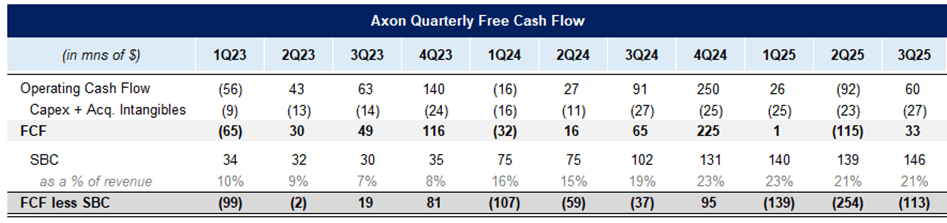

Despite strong revenue growth, their elevated operating expenses, high SBC, and slow cash conversion cycle means that revenues haven’t been converting to cash. After backing out SBC, they burned $113mn in 3Q.

Business Commentary.

A major focus of the quarter was Axon’s expansion into...

The rest of this update is only accessible to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

Click below to access the rest of this post, as well as our in-depth 75 page report on Axon, PLUS a large and growing library of other deep dives and business updates.

For further reading, check out our Axon Extensive Research Report.

The Synopsis Podcast.

Follow our Podcast below where we cover Axon more!

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Coupang report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered APi Global, Airbnb, AppFolio, Axon, Casey’s, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in Axon. Furthermore, accounts one or more contributors advise on may also have a position in Axon. This may change without notice.