AXON, CSU, and DFH: 3Q24 Business Update

+28% stock jump, building homes through high interest rates, and Constellation Software grew revenues +20% y/y

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

We will provide an update on CSU and DFH through our podcast too. Follow our feed here (Apple, Spotify)

Paying Speedwell Members please click here for the full update. To become a full Speedwell Member click here.

DFH Commentary.

DFH Reported 3Q24 earnings last week. As a reminder, they do not have an earnings call and their press release is fairly short. Overall, we do not think this was a particularly eventful quarter.

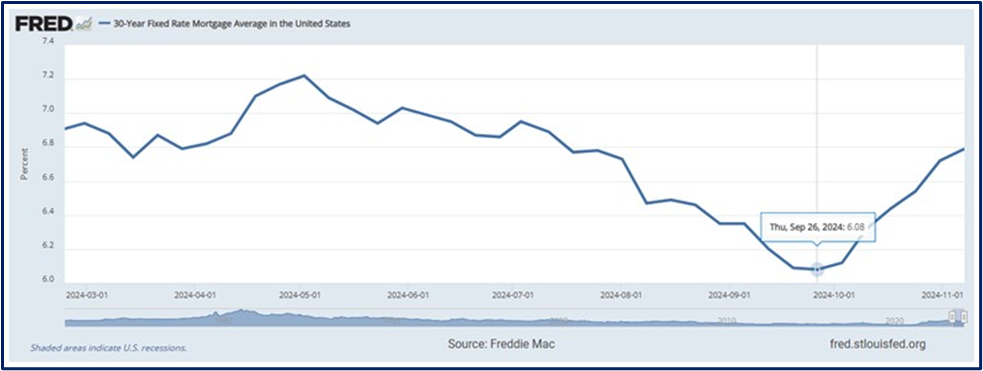

They are on track for their annual home closing target of 8,250 homes, despite some end market headwinds. Freddie Mac reported that home sales declined 2.9% in August. Existing home sales fell to the lowest since October 2010. This was despite rates reaching their lowest point in two years in September. Additionally, existing home supply reached 4.2 months in October, the highest since July 2019. While this could be a potential headwind for DFH in 4Q, this figure is still at the low end of the historical average of 4-5 months.

The impact of mortgage rates is multifactorial. While higher rates can be a headwind as they increase monthly home payments, the more expensive financing costs also make existing home owners (who locked in much lower rates) more reluctant to sell their homes. This is why new home sales as a portion of total home sales has greatly increased. Furthermore, when rates start to decline, some potential home buyers may defer their purchases, thinking they could drop further. Lastly, there is a lag between lower rates and an increase in purchase activity.

Big picture though home demand remains strong ,“bolster by the demographic tailwind from Millennials and Gen-Z, who are at prime home-buying age” per Freddie Mac.

From our DFH report:

While higher interest rates do make homes more unaffordable, people are not willing to push off a home purchase indefinitely. A 4% versus 8% mortgage is about $1,300 a month more, which is no doubt a considerable amount of money for most Americans. But many who desire a home are likely to cut other expenses or take on second jobs to realize their home ownership dreams.

Ultimately the homes sales will come, it is just a matter of timing, which is why DFH’s capital-light strategy is so important to being able to withstand deteriorating economic environments. Having said all of that, they continue to perform well despite high rates. At $32 a share, they trade around 11x earnings based off of their diluted market cap.

DFH 3Q24 Update.

Home revenues increased +10% y/y to $986mn for the quarter, down 200bps sequentially.

Noted revenues were partially offset by an increase in sales incentives during 3Q24.

Home closing increased +5%, but net new orders increased +9%.

ASPs increased slightly +3% y/y to $518k, up 100bps sequentially.

The Crescent Homes acquisition in Feb. 2024 boosted ASPs since those 223 home closings carried an ASP of $554k.

Home gross margins compressed -140bps y/y to 19.2%, but were +20bps sequentially.

Mostly due to higher land and financing costs, offset by some direct cost savings and an improvement in cycle times.

Backlog slightly shrunk to 3,996 homes valued at $2bn from 4,205 or $2.1bn last quarter.

Cancelation rates improved was 13.8%, a 110bps improvement y/y..

Controlled lot pipeline has increased to 45k from 31k last year.

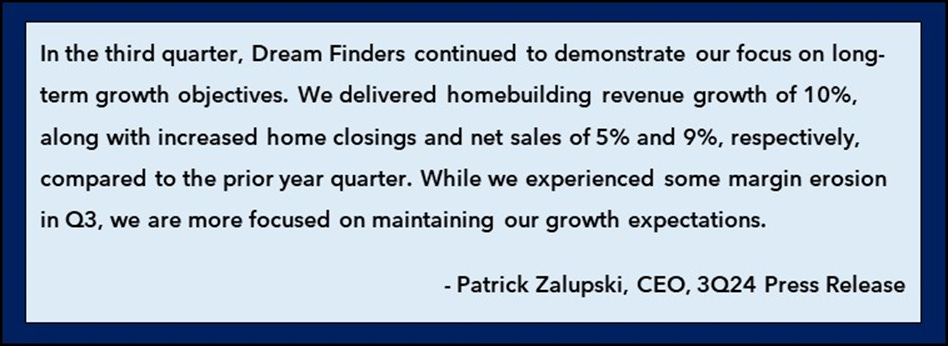

CEO Patrick Zalupski commented on their performance the following:

Other DFH Comments.

Repurchased $5mn in shares

“In addition to investing in the growth and scale of our business, we remain committed to our capital allocation strategy, which includes buying back shares when we believe there is an attractive disconnect between the market price and the intrinsic value of the shares”

“We will remain opportunistic in all facets of growing the per share returns of DFH.”

Guidance

Reiterate guidance of 8,250 closings for the full year 2024.

Acquired remaining 40% interest in Jet Home Loans

“Deal was immediately accretive, contributing revenues of $16 million and pre-tax profitability of $7 million in the third quarter”.

Axon 3Q24 Earnings.

Results were strong marking the 11th consecutive quarter of 25%+ growth and 3rd quarter of 30%+ growth. Total revenue growth of +32% y/y was a 3 point decel sequentially, but is up 8% q/q. For context, this growth rate is still elevated from their high 20s growth rate a couple years ago.

In their Software & Sensors Segment, Axon Cloud & Services revenue was +36% y/y (y/y growth down 10 points sequentially) and net revenue retention was 123%. Sensors & Other grew +18% y/y (y/y growth rate also down 10 points sequentially). Despite the slowdown in growth, these are still very strong numbers and more than they were doing a few years ago.

The TASER Segment grew +36% y/y, representing a 9 point deceleration from last q, but up 13% q/q. The TASER business is strong with their latest device, the TASER 10, garnering double the interest of their last model at the same point in the upgrade cycle. This was the 6th consecutive quarter that the TASER segment hit record revenues.

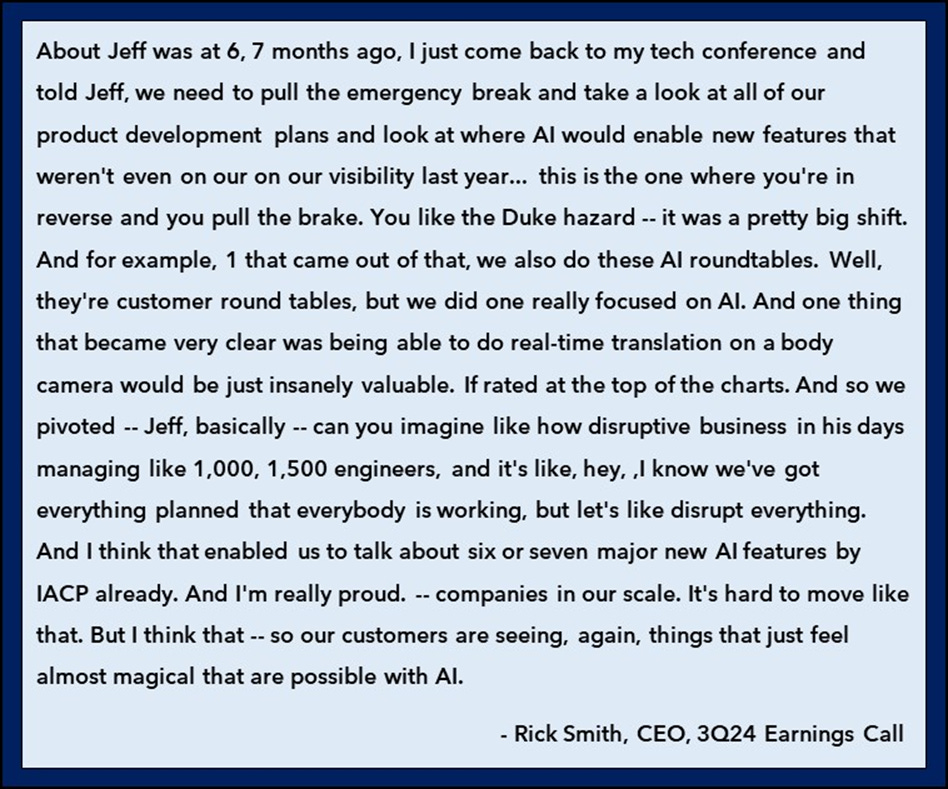

Commentary on new products, particularly AI, is optimistic. They wil launch an AI bundle next year with DraftOne as a marquee feature. Axon President Josh Isner noted he was “very, very bullish on Draft One”. The AI bundle, called “AI Aero”, will be $199/mo, giving them another important growth lever to push ARPU higher.

Drones is another future growth vector. Currently local law enforcement cannot intercept drones, but that could change soon. This is especially important as the availability of drones has led to some incidents, like someone attaching a pipe bomb to a drone in Pennsylvania. Axon’s Dedrone can locate drones and in the future give law enforcement the ability to intercept them.

Overall, the call was brimming with optimism and as President Josh noted, “Part of what's informing that confidence is just tremendous execution across all four segments of the business. state & local, enterprise, federal, and international.” They are gaining adoption with all of their end markets and across both their product segments.

Such optimism was quickly mirrored by the market though, which sent Axon shares up +28% the day, seeming to reflect much of the optimism conveyed on the call. At a $46bn market cap today, Axon trades at 22x sales or, assuming a 40% mature margin, 71x earnings.

CSU 3Q24 Update.

3Q24 revenues grew +20% y/y to $2.54bn for the quarter. This is a slight drop from last Q’s growth of +21%.

Organic growth was +1% y/y, down from +3% y/y last quarter.

As a reminder the “Maintenance & Other Recurring” revenue

The rest of this update is accessible only to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

If you are not a Speedwell Member, click here to become one.

Members will receive not just updates from our covered companies, but all of our Extensive Research Reports and our Shorter Exploratory Reports. See the full list of our covered companies here.

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in AXON, CSU, DFH. Furthermore, accounts one or more contributors advise on may also have a positions in AXON, CSU, DFH. This may change without notice.

The AXON stock-based compensation is getting a bit steep now. Thoughts?