Casey's Exploratory Report

Casey's Company Exploratory Research Report

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

We will also record a podcast episode on Casey’s soon, follow our podcast here to get it when it’s released: (Apple, Spotify).

This is an exploratory research report, which means it is about a third of the depth of our typical reports. These pieces exist so we can write about a business without having to do our normal multi-hundred hour process or because in researching a company we decided for one reason or another that we should shift our attention elsewhere. This can be because we found key risks that we think most investors won’t be comfortable with and incremental research won’t increase clarity around that, or simply because we felt there are more interesting names to move on to. In this case we felt that most readers or investors would understand the business well enough after just an explortatory report and more in-depth research probably wouldn’t change their minds one way or another. Nevertheless, we think you will learn a lot about the business and industry from this report!

Business History.

In 1959, Don Lamberti, an Iowa native, worked at his parent’s country store with a gas station in Des Moines. The person who Don bought gas from was a man named Kurvin C. Fish, and one day he suggested the two of them buy a few local gas stations, which were being sold together. There were four gas stations in the deal, and they only needed to put $40k down. Fearing that people might discriminate against Lamberti’s Italian last name, they wanted to call the store something generic. Casey’s was picked after Kurvin’s initials of “K.C.”. One of the four properties they ran had a convenience store added to it, marking the creation of the first Casey’s in 1968. It was an instant success, generating in the first year what they thought it would take three years to make.

The duo opened a second Casey’s in Creston, Iowa, which had a population of just 7,000. This showed that the model was replicable and, critically, that it could work in very small towns. They continued to open stores and, by the late 70s, had over 100 of them, all stationed in Iowa. They stocked a lot of non-perishable food items, which helped lower costs from spoilage, and other non-food merchandise like tobacco products, ammo, and other small consumer package goods. While larger convenience store chains focused on larger towns, Casey’s would focus on adding more units in the smallest of towns.

Their other “secret” was cleanliness. Lamberti commonly quoted a survey to employees that showed that customers leave dirtier stores quicker than clean ones, and he wanted them to linger around and browse to encourage impulsive purchases. While this may sound like a simple sales tactic, it was also somewhat rare back then—especially in these small towns.

To continue to fund their expansion of convenience stores and gas stations, they went public in 1983. They offered about a quarter of the company at $15 a share for an estimated market cap of $42mn at the time. Helping differentiate their convenience store offering early on was launching “made from scratch” pizza’s in their stores in 1985. They expanded through a mix of greenfield store openings and acquiring independent convenience stores to convert to Casey’s. They continued to steadily add units, reaching 1,000 locations by 1996.

By 2000, they had expanded into nine states across the mid-west, with a particularly strong presence in Iowa, Illinois, Missouri, and Kansas.

In 2005, they would conduct one of their largest acquisitions of a chain store operator, adding 58 units from the Nebraska-based “Gas N’ Shop Inc.” Since then, they have been regular acquirers of larger convenience chain stores.

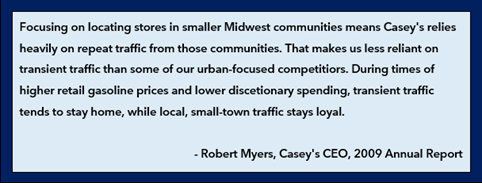

In 2009, while most American businesses were suffering due to the Great Financial Crisis, Casey’s was showing its resiliency. Its core philosophy of “Small Community Focus” and “Emphasize Food Service” was holding up well in small towns. Rather than being dependent on transient traffic, as many gas station/ convenience store combos are, Casey’s focuses on catering to the locals within an individual town. This means a higher rate of repeat purchases from the same customers and less dependence on road travel for sales. (Road travel tends to drop in tough economic times as people take fewer road trips). The fact that local consumers had few other alternatives and Casey’s offerings (including food) were already low-priced, meant that there was nothing to trade down to. Same-store sales increased +6.7% and margins improved.

Their performance through the GFC attracted interest from other convenience store operators. In 2010, Casey’s was almost acquired by the much larger Canada-based convenience store chain Alimentation Couche-Tard. After Casey’s rebuffed the hostile $2bn offer from Alimentation Couche-Tard, Japan’s Seven & I Holdings, which owns 7-Eleven, stepped in. Seven & I Holding’s offer was also rejected. and Casey’s management raised a bond with a change of control provision that allowed the bondholders to redeem at a premium should there be a takeover to dissuade any further acquisition attempts. With their independence secured, Casey’s continued to acquire more units in the mid-west and lean into their prepared food offering.

By 2014, revenue approached $8bn as their prepared food and fountain drink offering was proving to be a key differentiator. In order to compete with established pizza chains, and increase the utilization of their on-site kitchens, they created a pizza delivery program to serve over 400 locations.

Having a prepared food offering where items are cooked on-site adds a lot of logistics complexity. Whereas most convenience store items have long shelf lives, allowing for just occasional drop offs, fresh food expires quickly, requiring constant deliveries of fresh ingredients. Compounding the problem is the fact that most of their stores are out in the middle of nowhere, so there wasn’t a strong established 3rd party logistics supplier they could leverage. While Casey’s had started to build up their own logistics network many decades ago to improve margins, their fresh food offering demanded they expand it even more. This is because fresh ingredients spoil quickly and thus only a few days’ worth of ingredients can be shipped at once, requiring more frequent deliveries.

In addition to building their own logistics network, they built distribution centers. This allowed them to cut out wholesalers, which not only improves margins, but helps keep quality control more consistent. Casey’s stores are established within a 500 mile radius of its distribution centers, enabling them to have lower logistics costs, better inventory control, and consistent product availability across stores. In 2016, after three decades of just operating from their original distribution center in their hometown in Iowa, they built their second distribution center in Terre Haute, Indiana to better serve their expanding footprint as they entered new markets in Tennessee, Ohio, and Michigan.

In 2019, Darren Rebelez joined the company as President and CEO, succeeding Terry Handley. Under Rebelez’s leadership, the company crossed the 2,000 store threshold and began accelerating its digital capabilities, including mobile ordering, delivery partnerships, and building out its loyalty program called “Casey’s Rewards”. When the pandemic hit in 2020, these investments proved critical. Despite volatile fuel sales, Casey’s operating profits improved to ~$450mn in 2021, up from ~$400mn the year prior (although that was admittedly helped by the $580mn acquisition of Bucky’s, not to be confused with Texas-based chain Buc-ees).

As a way to further improve profitability and compete with local grocery stores, Casey’s expanded their grocery selection and introduced their own private label in 2021. While they started out with only a handful of SKUs, it quickly grew to over 300, encompassing everything from bakery items and nuts to meat snacks and drinks.

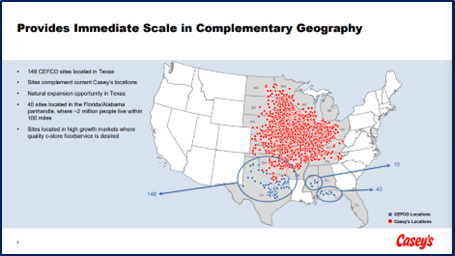

After their Bucky’s acquisition, which gave them a foothold in Nebraska and Illinois, they started looking to expand their presence in the South. Casey’s acquired 101 locations across Kentucky and Tennessee, along with entering the Texas market with its acquisition of 22 Lone Star Food Stores in late 2023. The Lone Star acquisition would later set the stage for Casey’s larger expansion into Texas the following year.

In 2024, Casey’s made its largest acquisition in company history with its ~$1.15bn purchase of Fikes Wholesale, which added 198 CEFCO convenience stores (or roughly 7%) to its store count. This enabled Casey’s to enter Florida, Mississippi, and Alabama, along with further expanding their footprint into Texas.

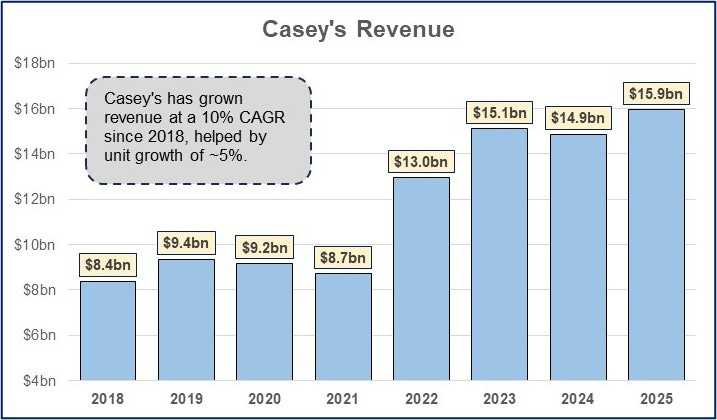

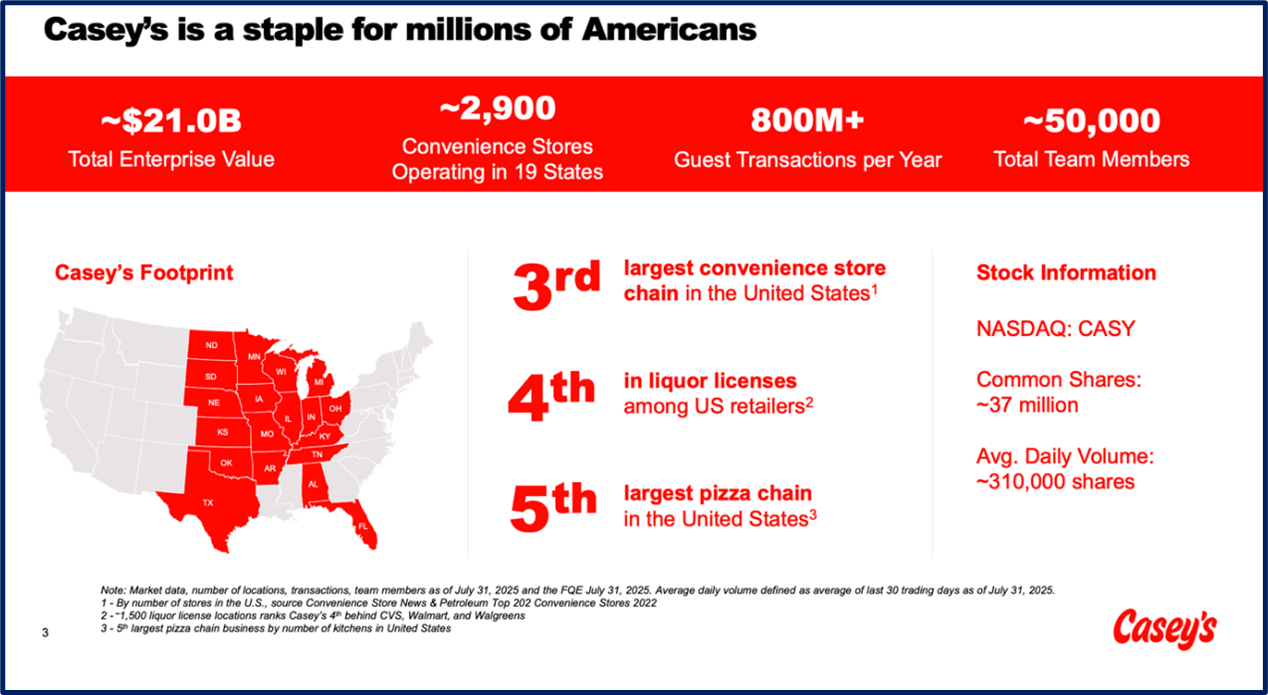

Today, Casey’s manages nearly ~2,900 stores across 20 states, serves over 9 million members in their loyalty program, is the 3rd largest convenience retailer, the 5th largest pizza retailer nationally, and generates over $16bn in revenues at a 5% operating margin.

Business.

Casey’s General Stores operates convenience stores with gas stations throughout the mid-west with a presence in 20 states. Half of their ~2,900 store footprint is concentrated in Iowa, Missouri, and Illinois. Almost all their stores operate under the Casey’s brand except for some acquired stores. They operate 63 stores under the “GoodStop” name, 12 under “Lone Star Food Store”, and 198 under CEFCO (from the recent Fikes acquisition). Casey’s is the 3rd largest convenience store chain, the 4th largest liquor license holder, and the 5th largest Pizza chain in the United States.

The typical Casey’s store is in a small town (71% of stores are in cities with a population under 20k and about 50% have a population under 5k). Most stores open at least 16 hours a day, seven days a week. While the size of their stores varies depending on how much traffic the location gets, almost all of them have on-premise kitchens and gas pumps (only 6 Casey’s do not have an attached gas station).

Each convenience store carries about 3,000 SKUs and sells a broad selection of snacks, beverages, tobacco and nicotine products, groceries, health & beauty aids, automotive products, and other non-food items.

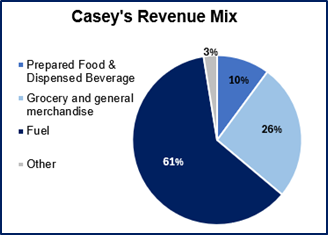

The prepared food offering includes breakfast pizza, donuts, hot breakfast items, and hot and cold sandwiches. Food, beverage, grocery, and general merchandise is 34% of revenues, but 63% of gross profit (before accounting for D&A). As a result of acquisitions, they also operate 260 car washes. They also have a small fuel wholesale network where they sell fuel to 3rd party locations (2% of revenue).

They have 3 distribution centers that supply most of their stores. Their distribution centers are in Iowa, Indiana, and Missouri. They self-distribute the vast majority of their products as well as the majority of their fuel. They currently have about ~500 tractors, which allows 60% of their fuel to be delivered from their own fleet. Sales are strongest in the 1st and 2nd fiscal quarters (May to October) where the warmer weather encourages more driving and thus the purchase of more fuel, as well as beverages.

Currently they conduct over 800mn transactions a year and have >50k employees. Their rewards program has over 9 million members, which allows users to redeem points in their mobile app for discounts. Users can also get curbside pickup and delivery for store items and their food offering.

Casey’s breaks out revenues by 1) Prepared Food and beverage, 2) Grocery and General merchandise, 3) Fuel, and 4) Other. The other category includes car wash revenues and their wholesale fuel business (where they sell fuel to other gas stations).

They also provide a contribution profit by segment metric which they calculate as gross profits before D&A. While of course D&A is a real cost for these segments, it is actually a helpful metric to gauge the profitability before accounting for fixed costs.

On this “revenue less cost of goods excluding D&A” metric for 2025, their Prepared food and beverage segment generates 58% margins, Grocery and general merchandise generates 35% margins, Fuel generates 13% margins, and “Other” is at 30%. We will refer to this margin as a “contribution margin” from here on. From these margin profiles it is easy to see why Casey’s is focused on increasing their Prepared food offering and why that category sets them apart from more basic convenience stores.

They currently generate $16.4bn in LTM revenues. Their average location generates about $5.5mn in revenues, but a large portion of that is fuel, which carries a contribution margin that is about 1/5th of their prepared food and beverage and 1/3rd of their grocery and general merchandise sales. Fuel sales per location average ~$3.5mn, with average contribution profits of $446k for 2025. This has grown from $223k in 2019 with a contribution margin of 8%. (Later in the report we will talk about what has driven this fuel margin expansion).

“Retail Inside sales”, which includes Prepared Foods and Beverages, and Grocery and General Merchandise, is ~$2.1mn with contribution profits of $842k per location for 2025. In 2020 this figure was $651k, for an Inside Sales growth CAGR of 4.3%.

In total, the average location generates $1.3mn in contribution profits with 65% coming from Inside Store Sales. Average operating income per store (which they calculate and disclose) is $496k. This comes out to average store level operating margins of 8.9%.

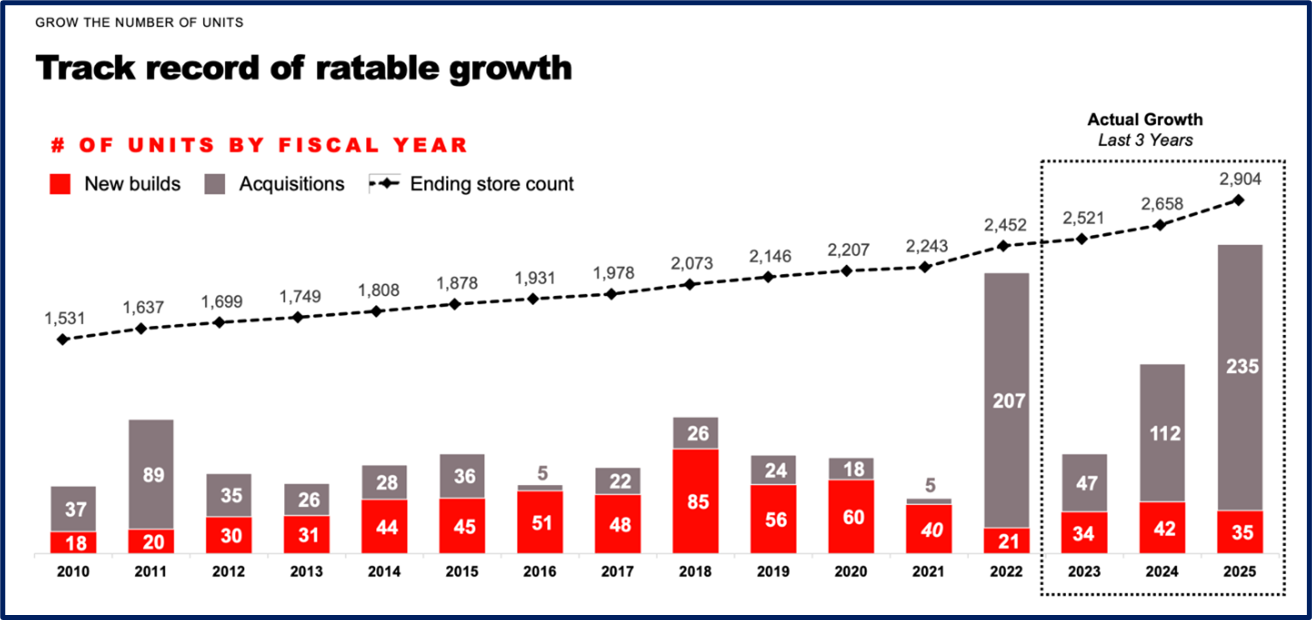

Since 2010, they have grown revenues at a ~12% CAGR and a ~11.5% CAGR since 2020. For 2025, revenues grew +7.3%, with same store sales from Food and Beverage growing Speedwellresearch.com 15 +3.5% and Grocery and General Merchandise growing +2.3%. Fuel sales were roughly flat. he rest of their growth has come from unit count, which was up +9% in 2025 (the full year of sales of acquired units isn’t included in 2025 figures though).

Operating profits have grown from ~$650mn, with a 7% margin, in 2020 to $1.2bn, with a slightly improved margin of 7.5%. This represents a 13% CAGR. Their current goal is to continue to grow EBITDA ~8% a year, with half of that coming from existing store growth and the other half from new units - whether those are acquired or built.

To better understand their opportunity to continue to improve same store sales and acquire units, we are now going to turn to the industry overview and competitor set.

Industry.

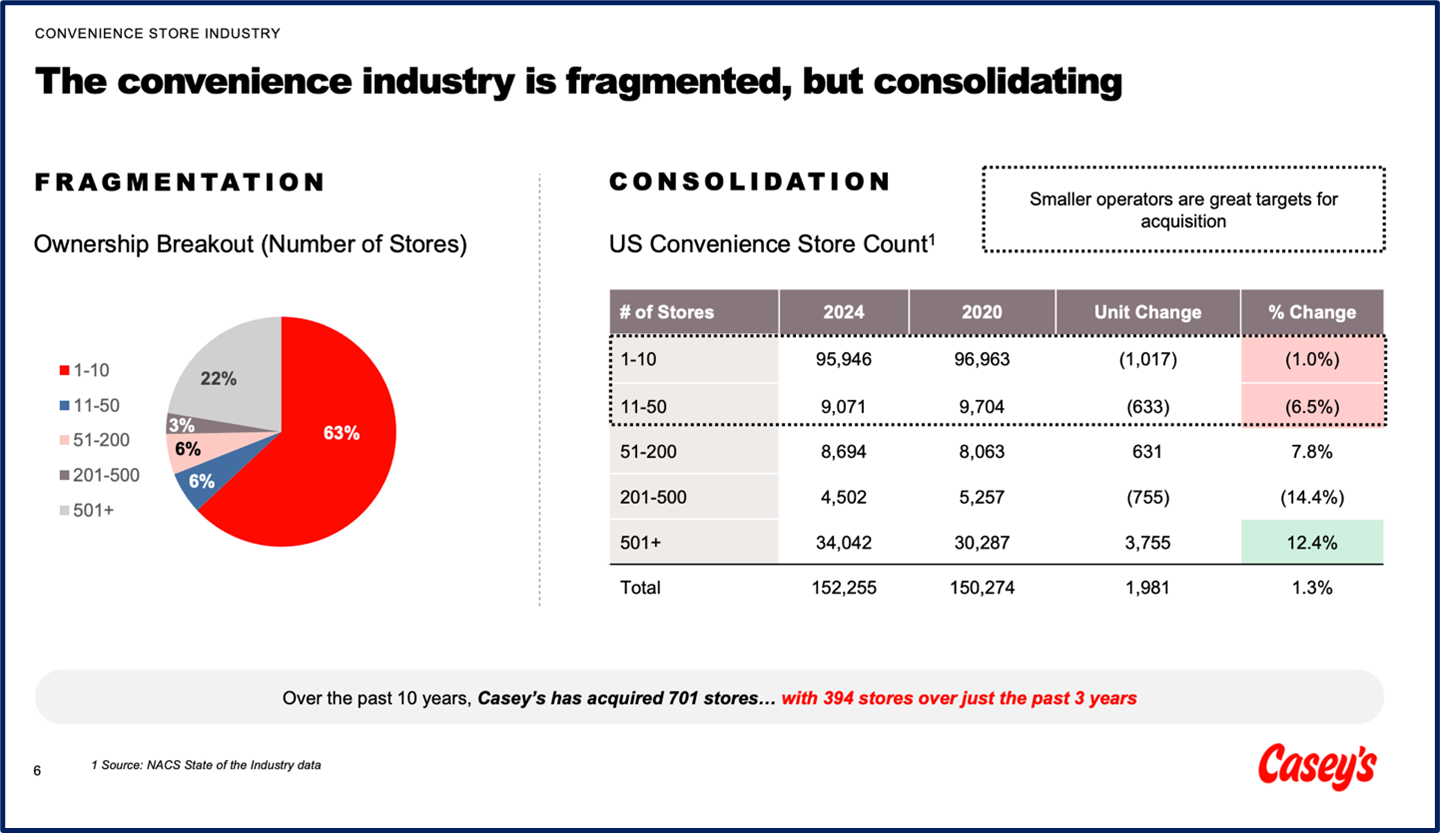

The convenience store industry is very fragmented, with 63% of stores owned by operators who run 10 or fewer stores. This suggest both an opportunity to acquire these small operators, but also that the majority of the competition set doesn’t benefit from scale or professional management.

While there are several other large convenience store chains, most stick to a particular region with the exception of 7-Eleven who has a nation-wide presence. Other large chains include Circle K, which is owned by Aliment Couche Tard, and Speedway (which was acquired by 7-Eleven). For a sense of scale there are 13,000 7-Elevens, 9,200 Aliment Couche Tard-owned stores, and 3,000 Speedways in North American. Casey’s store count tallies to 2,900.

Speedway is a regional player that is biggest in the Midwest and the East Coast. Other regional chains include Murphy’s USA which operates in the Southeast, Southwest, and Midwest. Murphy’s is known for opening units directly next to Wal-Mart, leveraging the traffic that the retail store brings. They have about 1,500 locations.

QuikTrip also has about 1,000 locations and has their own kitchens that offer fast food, including pizzas and sandwiches. They have a presence in the South, Midwest, and Southwest, but are the most popular in Oklahoma, Georgia, Missouri, and Kansas.

While there are many other regional and sub-regional chains, Wawa’s and Sheetz are most similar to Casey’s as they both have strong fresh food offerings and loyal customer bases, partially due to their high penetration in a concentrated region.

Wawa’s home state is Pennsylvania, but they expanded across the east coast with a notable presence in New Jersey, Delaware, Maryland, and Virginia. Wawa’s is known for their hoagies (sub sandwiches), which have become a bit of a cultural icon for the locals. They have in total around 1,100 locations.

Sheetz’s was also born in Pennsylvania, which created a bit of a rivalry between the two. Sheetz has a larger menu, serving tacos, burgers, sub sandwiches, and fried foods, and allows for extensive customization through their touch screen ordering kiosks. Besides their home state, they have a presence in Ohio, West Virginia, Maryland, Virginia, North Carolina, and Michigan, but do not have as high penetration outside of Pennsylvania.

While consumers may have their favorite convenience stores, as the name suggests, “convenience” is going to be the primary factor that sways a customer to visit one store vs the other. Putting the fresh food offering aside for a moment, most stores are essentially substitutable relative to each other. If you are just going to pick up a bag of chips and a drink, any store can do just about as good of a job as the next.

That is why it is very common to group a convenience store with a gas station—once a customer is already on the location, they are much more likely to make that purchase at that store. Thus, getting a good location that has natural street traffic is very important; unless you are desperate for gas or a bathroom, you are unlikely to go much out of your way for a gas station/convenience store. That is why you can see convenience stores on opposite sides of the streets. Simply having to cross the street is so much of an inconvenience to customers that stations will lose their business.

The gas station business is challenging, with many gas station operations barely maintaining profitability on a stand-alone basis. This is because consumers are very price sensitive and gas is almost the definition of a commodity product. Any decent margin a gas station can garner is mostly a byproduct of procuring in large enough quantity and owning their own distribution chain to cut down on costs.

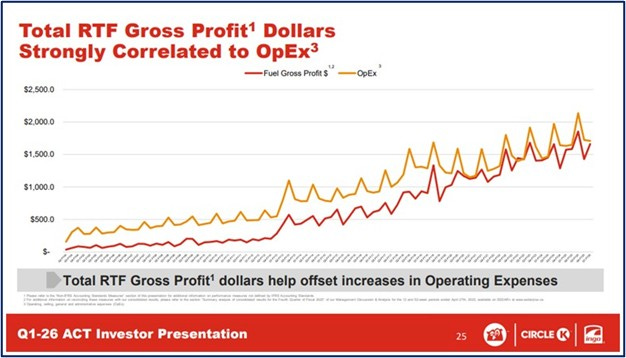

Fuel gross margins have improved over the past couple years for a few reasons. The first is that there was labor inflation and smaller mom and pop gas stations had to raise fuel prices to expand their fuel gross profits to offset an increase in labor costs. The slide below from Aliment Couch-Tard seems to corroborate that as they note the correlation between operating expense growth and fuel gross profit growth

The second, and lesser mentioned reason, is lasting impacts from the Russian oil embargo. In contrast to what you might think, crude oil (unrefined oil from the ground) is not a homogenous commodity, but varies a lot based on where in the ground it comes from. Crude oil can be “heavier” or “lighter” which refers to how tight the hydrocarbon molecules are packed together. Another common difference is how “sour” or “sweet” it is, which refers to sulfur content. Russian oil (their main blend is called Urals) tends to be heavier and more sulfur-rich (sour) compared to U.S. shale crude.

Many European refineries had been configured to run on Russia’s heavier crude, and when that supply was cut off, the refineries struggled to adapt quickly to new supply. This created a distortion whereby the existing refinery capacity was not fully optimized. Even if Europe had access to plenty of crude oil from other sources, much of it could not be processed into diesel and gasoline as efficiently. This boosted demand for U.S. refined products and many European refiners are still less efficient on alternative crude oil, leaving overall output yields lower than before (and thus more reliant on U.S. refined products).

Lastly, several European refineries shut down during Covid and never re-opened, reducing capacity. Together, the lingering inefficiencies, tighter heavy crude supply, and higher refined product demand introduced lasting volatility and helped drive U.S. fuel retailer margins higher.

This is all to say though that an investor should not mistakenly believe the improved fuel margins had much to do with decisions an operator made, but rather are by and large the by product of events outside of their control. Beyond some procurement and distribution advantage from scale, this is a business where everyone is going to earn the same margin.

Many operators, especially mom & pops, are hardly profitable on the gas stations, but rather use them as a customer acquisition tool for the convenience stores. Once a customer is stationary while filling up their car, they will often come up with a reason to buy a snack or something from the convenience store.

Now, the fresh food offering is a more differentiated product. If someone wants a Wawa’s hoagie or a Casey’s pizza, they would be willing to not just cross the street for it but drive a bit out of their way to get it. This is only to an extent of course, as there are many foods options, and a convenience store is hardly going to be top of mind for most consumers. That is why there still is usually this element of convenience when a customer does purchase hot food from a Casey’s or Wawa.

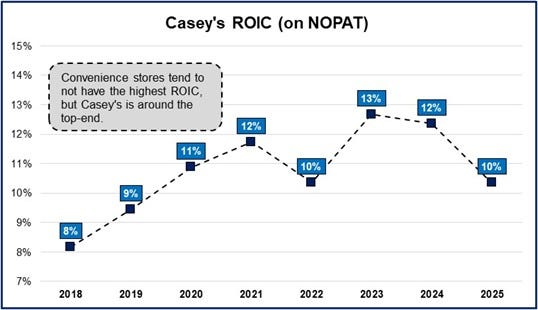

This makes most convenience stores fairly average businesses. The competition and lack of strong differentiation makes it hard to have an outsized ROIC, as competitors can (and do) literally pop up across the street to steal business. Alimentation Couche-Tard has a ROIC of about 11%, and Seven & i Holdings, owner of 7-Eleven, is closer to 5%. While this is a meaningful range, 11% is right around the edge of mediocre and 5% is dreadful. Casey’s is at the higher end, averaging 11% since 2020.

Casey’s Model.

While it is a very competitive industry, Casey’s does stand out in some respects. They…

Become a Speedwell Member to get the rest of this report.

If you are a Speedwell Member, click here to read the rest of this post.

If you are not currently a Speedwell Member, join below!

Members will receive access to the rest of this report PLUS our library of other research reports AND on-going updates on our covered business. See our full coverage here.

(Please reach out to info@speedwellresearch.com if you have any issues or need to speak to us to become an approved research vendor in order to expense the membership).

The Synopsis Podcast.

We will be releasing a company episode just on Casey’s in the future. Follow our Podcast below to make sure you get it when it is released!

Become a member today for access to our Casey’s as well as many others! See our full list of coverage here.