Constellation Software: 1Q26 Business Recap

AI Strategy Revealed

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(This is a Business Recap, which is shorter than our Business Updates. We usually only publish Recaps to our Website to avoid spamming the Substack, but we thought Constellation had large enough interest to warrant sharing more broadly. Members can find a PDF of this post here.)

1Q26 Update.

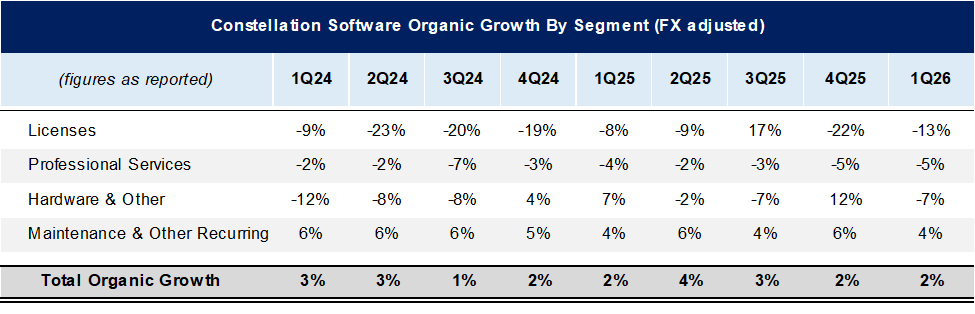

Constellation Software reported 1Q26 and had their first earnings call in 8 years.

Revenues grew +20%, but organic growth was only 2%. However, their maintenance & other recurring revenues (which is the best barometer of the health of their core software businesses) grew 4%. While an acceleration of growth would have been nice to see and could have put to rest the fears that AI is disrupting their business, their organic growth rate has stubbornly been bobbing around ~2% for years.

On the call and AGM, they talked a lot about how AI has helped them improve product cycles.

“If you think of a cycle time from concept through to production software, typically for us, that was measured in months. When we came back in May, we already started measuring that in weeks. And as we went through last year, we turned that from weeks into days. And today, our cycle time is measured in hours. We can cycle from concept through to production in hours. And that means a road map that might have taken, say, a whole year, we plan out a whole year road map. That can be literally a week now.”

– 2026 AGM

Something that is worth emphasizing is that speed of development, in and off itself, isn’t beneficial to the customer. This is part of the reason why software companies are somewhat insulated from the growing ease of creating software. AI does mean creating software is easier, which is a benefit to the software company creator, and they may be able to reduce their costs as a result. However, passing off a portion of this cost savings to customers with a price decrease is not that value additive to customers.

To better understand this, just listen to what Mark Miller said:

“The way we lose customers is, a, they get essentially go out of business, which happens, you can’t do much about that. They’re acquired by other customers, particularly larger customers. That’s another way of losing. You can’t do much about that. Other than you hope you -- the other customer that buys them is your customer. Pricing is the third and pricing, rarely, we lose customers on pricing because the switching is painful for customers and it’s working and they’re using it and retraining all their users and adapting the interfaces to make it work and make it harder. Where you lose customers is when the competitor can provide something much different than you can provide that the customer really needs. And that’s where I always worry the most, just generically forgetting about AI. So that’s kind of how I sort of look at it.”

This means not only that it is hard to win new business just based off of price, but also that it is not that simple creating new products with AI to upsell customers—there needs to be a real value add. While this might seem obvious, a lot of investors are seemingly forgetting the distinction between a benefit to the business and a benefit to the customer.

“So I think, there’s no question, you can enhance your technology stack faster, thanks to AI. But really, again, it’s going to come down to, do you understand what the customer is trying to solve? What’s the pain point they’re trying to solve?”

– 2026 AGM

We are optimistic that Constellation Software will figure out how to deploy AI in a way that will drive real customer benefit, but a conservative investor would not want to assume that in the base case.

FCFA2S is the best indicator of owner earnings. FCFA2S (after backing out the IRGA liability) is $2.18bn, which is +26% y/y. This is on the back of having deployed $1.6bn YTD (includes 1Q and commitments to date, which takes us to about half way through 2Q). This is a clear step-up in deployment and doesn’t include their PEMS, or Permanent Engaged Minority Shareholdings (although it doesn’t look their PEMS were meaningfully increased this quarter—we see just a $28mn increase in investments in associates).

This shows that Constellation is having little trouble deploying capital lately, taking off the table one of the bear cases of them not being able to deploy enough capital beyond their small VMS acquisitions—at least for the interim.

“It just comes and goes up and down as the market evolves. We don’t see more transactions than usual. We don’t see less transactions than usual. It’s just the same amount across the market as we’ve always seen. So nothing’s changed. There’s a real disconnect between the SaaSpocalypse publicly traded stuff and private markets. But yes, it’s just ebbs and flow of the market. “

- Bernard Anzarouth, 1Q26 Earnings Call

While it may have seemed like a consequential quarter because of all of the AI fears and their large stock drawdown, it really isn’t. If AI does ultimately weigh on Constellation’s ability to grow (which we don’t think it will), there was little reason to think it would have had a notable impact already. If new start-ups with AI-created software start going after Constellation’s vertical markets, it will still take them years to build up distribution and fight for clients. Again, we don’t think this represents a significant source of new competition because of the moats Constellation has, but we are just emphasizing that in bear’s minds the risk will continue to linger.

Listening to the AGM it seems that Constellation is doing everything you would want them to do with AI. They are experimenting, creating more products, working closely with customers to utilize AI as they would see fit, and in some limited cases, disrupting their own businesses.

“So I think it’s easily said, I’m going to disrupt my own business and what you have with people working in the business in the existing business, I think that requires some change as well. So you might organize it outside of it. But there are, of course, businesses where you already had for a longer period of time, the idea that we should step up our game and we should do more. And those kind of businesses might be an ideal situation to really try to disrupt yourself. And so we try to analyze in our portfolio, our strong businesses and also our weaker businesses. We try to win with our excellent businesses, but there are also business where we think, hey, we could disrupt ourselves and really try to make a quantum leap into the future. That’s what we try to do. But again, that’s not all over the place. It’s easier said than done, but we try selectively to do that.”

– Robin Poelje, Topicus CEO

At a current stock price of $2,050, Constellation has a market cap of $43.4bn. This puts them at a 20x LTM FCF multiple for a company that has grown cash flows at a 14% CAGR since 2020.

For further reading, check out our Constellation Software Extensive Research Report.

The Synopsis Podcast.

Follow our Podcast below.

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Airbnb report and all of our other research reports, business updates, and Plus Members also receive Excels.

We have covered APi Global, Appfollio, Airbnb, Axon, Casey’s, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in CSU. Furthermore, accounts one or more contributors advise on may also have a position in CSU. This may change without notice.