Constellation Software: 3Q25 Update

AI Narrowing the Moat?

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(This is a Business Recap, which is shorter than our Business Updates. We usually only publish Recaps to our Website to avoid spamming the Substack, but we thought Constellation had large enough interest to warrant sharing more broadly. Members can find a PDF of this post here.)

3Q25 Update.

Constellation Software has had its largest draw down in their history, dropping over 37% from peak. While it is always hard to attribute reasons to a stock’s movement, many investors lately are talking about how AI’s ability to create software will ultimately weigh on Constellation’s business. We will address this after a quick quarterly update.

Constellation Software reported 3Q25 and revenues grew +16% y/y. This is a slight acceleration from last quarter’s +15% y/y growth. Of course, the timing of acquisitions is one of the largest factors driving revenue growth.

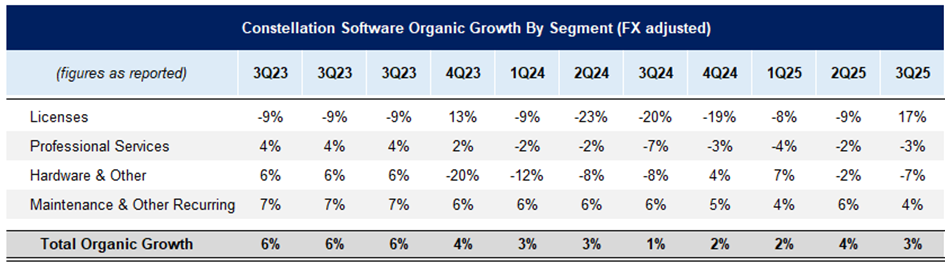

Organic revenue growth was +3% y/y. Slightly less than last quarter’s +4%, but still higher than our base rate assumption of 0 to 2% long-term. Within organic growth, their Maintenance & Other Recurring revenue segment is the best indicator for the underlying health of VMS (vertical market software) businesses.

As a reminder, Constellation Software commonly gets the criticism that they are just buying “cigar butts”, or businesses on the cheap that are slowly melting with dismal growth prospects. While most of their businesses do have low growth prospects owing to the inherently limited TAMs of VMS, they still are net growing despite churn. (One of the most common reasons for churn is a VMS’s client goes out of business). This helps allay concerns that the business’s are in “run-down”, which would suggest a long-term cash flow headwind with an increasing difficulty to grow as it would require replacing existing VMS business’s plus finding new ones. The positive organic growth, particularly with Maintenance & Other Recurring revenues being positive, helps allay these concerns.

Professional Services is about 18% of revenues and as a reminder, this segment constitutes “fees charged for implementation and integration of their services, customization programs, product training and consulting.” Remember this when we address the AI software risk momentarily.

For the past nine months, capital deployed into acquisitions was $955mn. However, if you include the Asseco equity stake, offset by acquired cash, total cash invested was $1,351mn. This compares to 9M25 free cash flow available to shareholders (FCFA2S) of $1,495mn. This figure backs out the minority interest, whereas there is no equivalent way to do that on the cash flow statement for investments. While adding back the minority interest increases the free cash flow amount, which may seem like a positive, in terms of capital deployment it would lower the total % of capital deployed. If you add back the minority interest and then look at total capital deployed, it is about 80%. This is quite strong given they haven’t had a large acquisition this year and last time they did have one it put them well over 100%. In our original DCF, most of our scenarios assumed lower than 100% free cash flow deployment and the real surprise is that they were able to do well over that the past couple of years. Of course, the nature of acquisitions are lumpy and so we don’t believe you can extrapolate too much from 3 quarters that have dipped below 100%. However, as they continue to grow free cash flows, it will get tougher to deploy the full amount every year unless they are able to continue to find large opportunities.

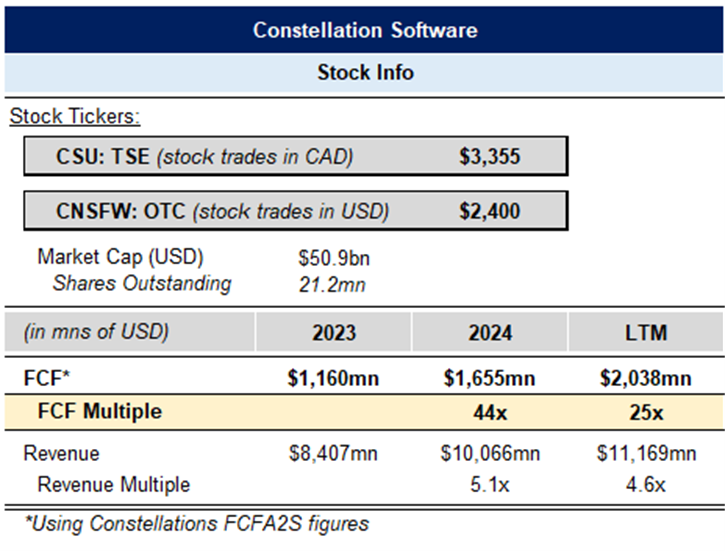

The past 9 months FCFA2S was +18% with 3Q up +38% to $565mn. The timing of acquisitions and contract renewals can impact this on a quarterly basis though. LTM FCFA2S is $2,038mn. Below we see that on LTM cash flow, Constellation trades at 25x—one of the lowest multiples its traded at in perhaps a decade. Growing cash flows at the rate they have, in a single year Constellation will be valued at a below market multiple and in two years of similar mid-teens growth it will trade at the same multiple the market has historically (~17x). This suggests the market has lost faith in Constellation Software’s long-term prospectus.

Business Commentary.

The biggest narrative, or argument that investors who are bearish are floating around is that AI will allow more software to be made cheaply, thus lowering the barriers to entry. This deluge of software will weigh on Constellation Software’s VMS business’s ability to retain existing customers. At the extreme, some investors have also suggested that the clients themselves will create their own software in the future by just asking AI to.

While no doubt AI will weaken the moats of some software businesses, Constellation’s moats never stemmed from barriers to entry. Even before AI a single software engineer could whip up a competing product. There is nothing particularly complex about most of their VMS software and it is often clunky with very rudimentary UI. A majority of their software is also quite old and that doesn’t bother clients. Software engineers weren’t deterred from entering that market because the software cost were too high, but rather because once they made the software there would be no one to sell it to.

That is because once a customer uses a VMS application it is very hard for them to switch. This is because the software becomes integrated with all of their other applications and work flow. Changing software means retraining employees on a new application and potentially going through the hassle of integrating other applications. Employers will lose productivity when retraining employees to use new software too. Switching software also presents the risk that data is lost or that there will be downtime. Since most of the VMS software they sell is mission critical, it failing means losing revenues and potential customer churn.

The business’s that buy Constellation’s software tend to be the opposite of tech savvy. They are small businesses that picked a software provider years or decades ago and have never had a reason to switch so long as it kept working.

The VMS markets they focus on are small (many as small as $5mn TAMs) and there often isn’t space for more than one provider economically. It’s true that AI can lower the cost of developing the software and so if before it was a 20-30% margin business that would be $1-1.5mn of profits to split between the owner and employees, that could now be a little higher. Maybe an AI-first VMS company could survive with 1-2 fewer employees, but they will still need employees to service existing clients, help them install and integrate the software, and sell them the software in the first place. These business owners are not actively seeking new solutions and so you would really have to figure out how to find these small businesses and then sell them on switching—certainly a very tough task.

This AI-first VMS company may be a bit leaner, but it is still not a threat to existing VMS businesses because they would not be able to steal their existing customers for one simple reason: they aren’t solving any new customer problems. The best they could do would be to compete on price, but the software is already a relatively low portion of their expenses, and most business owners don’t want to risk messing up something that is mission critical to save an inconsequential amount of money. It is key to understand that for many business owners switching mission critical software is the equivalent to gambling the business’s livelihood if it doesn’t work flawlessly. Why would you do that without a large and clear benefit?

Remember that professional service revenue line item? That is from customers already customizing the software to their liking and Constellation building the features they want for them. Customers already have a good enough software product, and it fits their needs. Something being “AI-created” doesn’t solve anything for them—there is no improved value prop. In fact, it could create more issues as the software could be buggy and not have the same level of traditional support. Many businesses are still getting their software on physical disks loaded onto on-prem servers, so you are not talking about the leading edge of tech adoption. If there are benefits to utilizing AI in software, which there no doubt will be, Constellation Software is in the best position to just incorporate that into their existing solutions and push it out to their customers.

In short, there isn’t any real benefit to the business owner for leaving their existing VMS solution. This is also why this has been such a great business for the past several decades and Constellation was able to survive the transition from on-premise to cloud just fine. While investors should have their own opinion on the AI risk, at least so far it does not seem like there is a clear benefit to a business owner to switch. And as long as there is no improved value prop, customers aren’t going to move anywhere.

At 25x free cash flow and growing mid-teens, if an investor can get comfortable with the AI risk then it could present a compelling opportunity for them, depending on their hurdle rates and comfortability with a high capital deployment assumption.

For further reading, check out our Constellation Software Extensive Research Report.

For another great update on CSU and more commentary on the quarter, check out Leandro at Best Anchor Stock’s update.

The Synopsis Podcast.

Follow our Podcast below.

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Airbnb report and all of our other research reports, business updates, and Plus Members also receive Excels.

We have covered APi Global, Appfollio, Airbnb, Axon, Casey’s, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in CSU. Furthermore, accounts one or more contributors advise on may also have a position in CSU. This may change without notice.

"While no doubt AI will weaken the moats of some software businesses, Constellation’s moats never stemmed from barriers to entry" - this is such a great and under-appreciated comment. ML said it himself the only barrier to entry is a phone and check book!

I have recently turn CSU into my biggest position in portfolio.

Hope I’m not wrong!