Constellation Software PM Summary

PM Summary: Our PM Summaries are designed to make our content more accessible to readers who have time constraints or want to get a sense of whether a business could be of interest to them before having to go through the full report. These PM Summaries are very high-level compared to the granularity of our full reports, but they give an investor the most critical information.

For the best reading experience, please view on our website or via the PDF (download below).

If you are trying to solve a Puzzle, our PM Summaries are like getting an outline of a "mountain" whereas the full reports are a high-definition picture of the puzzle. We believe it could be most helpful for an investor to get an outline of the picture through the PM Summary before potentially getting lost in the more detailed picture.

This is our first PM Summary, which we have decided to make free so prospective readers can get a sense of what to expect. Going forward, they will only be available to PM Summary subscribers (as well as Members and Members Plus subscribers).

Constellation Software Inc. (Published 10/7/2022.)

Stats: Market Cap: ~$32bn. ’21 Revenue: $5.1bn. ’21 EBITA: $1.4bn.

Tickers: CSU:TSE and CNSFW:OTC.

Executive Summary. Constellation Software is a holding company that owns a portfolio of over 750 different software businesses that each dominate a specific vertical market. Each of the 750 software companies are rolled up into one of six operating groups, which are then all consolidated to Constellation Software (acronym CSI). Constellation itself acts as a portfolio manager, helping lead large acquisitions, organize business hierarchies, and set investment policies. This makes for significant autonomy at not just the operating group level, but within each operating group at the business unit level. Growth is achieved primarily (but not exclusively) through acquisitions, with Constellation now acquiring over ~100 companies annually. While most of these acquisitions are small due to the nature of vertical market software, they add up to Constellation generating ~$5.7bn of revenue LTM and ~$1bn of FCF (normalized).

The big question with Constellation is whether their ROIC will drop as they have to deploy ever increasing amounts of capital. We run a reverse DCF sensitizing for capital deployment, acquisition hurdle rates, and organic growth to help answer this question in the context of what is priced in today. (Page 7).

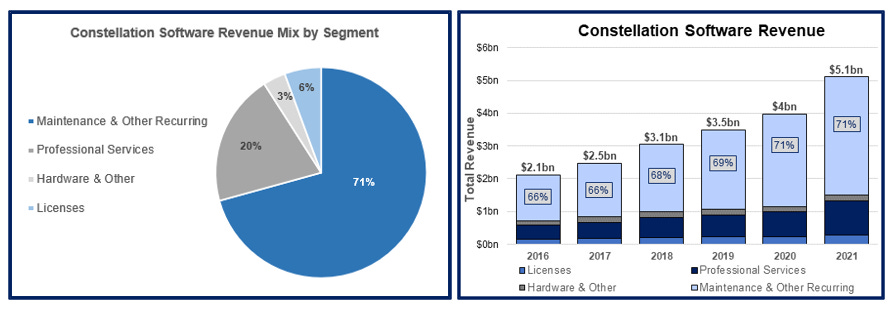

Business Segments. Constellation reports revenues in four segments, which are split by revenue type (with the six operating groups consolidated). Each revenue segment is listed below and most of Constellation’s businesses will collect several streams of revenue from each client, the most important of which is maintenance revenue (>70% of total and recurring).

Licenses: The software licensing fee is a charge for the use of the software, generally licensed under multi-year or perpetual agreements. This revenue stream is high margin, but lumpy and under pressure with the transition to SaaS.

Professional Services: These are fees charged for implementation and integration of their services, customization programs, product training and consulting. This is important as it makes customers stickier through customization of the products, but is comparatively low margin.

Maintenance & Other Recurring: These are fees charged for customer support on their software products “post-delivery” and also includes recurring fees derived from software as a service subscription (SaaS), combined software/ support contracts, and hosted products. These fees generally entitle a customer to product updates “when and if available”. This is their most important stream of revenue and Constellation considers the growth of Maintenance revenues as a good barometer for the health of the company.

Hardware & Other: This includes the resale of 3rd party hardware as well as sales of custom hardware assembled internally on a customer’s behalf. They report this line net of the 3rd party hardware cost (similar to a gross profit) so there is less topline distortion. Selling hardware is done mainly as a convenience to the customer and is not a material profit pool.

Vertical Market Software. We will first touch on vertical market software (VMS) and why it is a good business with strong competitive advantages.

The software Constellation’s VMS businesses offer are usually mission-critical ERP solutions that are essential to a business running properly. Whether that be Trapeze’s public transportation scheduling software which is relied on to make the busses run on time or Harris’ North Star Utilities Solutions customer billing system which invoices hundreds of thousands of customers, these are all software offerings that cannot be removed without replacements once adopted. Such reliance, stemming from supporting essential business functions, means that while elimination isn’t a question, replacement could be. But replacement isn’t easy, as each of the verticals they operate in tend to only have a few competitors, of which CSI’s businesses are almost always the #1 or #2 provider. The small TAMs become insulation for leading players as a newcomer cannot rationalize trying to break into the vertical since it is already largely served. An early mover advantage isn’t usually thought of as a sustainable advantage, but it can turn into one if the market is small enough that you can totally serve it before another player can enter and your customers are captive. It is far more expensive for a competitor to rebuild an existing VMS business than it cost the early mover because it is far more expensive (and difficult) to convince customers to leave a solution that largely meets their needs for an unproven solution they are not familiar with. This is especially true because the switching costs of leaving means a potential total disruption of business operations, which can directly lead to customer churn and lost sales. A new software system could also present issues that weren’t apparent to a business when they originally decided to switch, like integration issues with other software they utilize. A competitor’s product would have to be much better than the existing solution for a business to even fathom switching ERP software. Thus, a new entrant has to do far more to win a customer than the original software entrant did when their target customers weren’t served by any solution.

Importantly though, Constellation’s competitive advantages as a holding company and buyer of VMS businesses are distinct from the businesses themselves. The VMS businesses clearly have strong competitive positions, but Constellation’s advantages are more tenuous.

Constellation’s Advantages. Constellation’s competitive advantages pertain to factors that help them win acquisitions and run companies. While in Constellation’s early days they often were the only buyer of these small VMS companies, that has changed with several other copy-cat VMS roll-ups focusing here now too. Similar to Berkshire Hathaway, if the seller solely cares about squeezing the buyer for the highest bid, Constellation often loses the deal. CSI’s advantage comes from their reputation of letting entrepreneurs run their company without interference and being savvy operators who can help them, should the seller desire that. The other factor that helps Constellation win deals is simply knowing about the companies: there are over 50,000 companies in their database that they monitor. However, despite such large coverage, only 30% of companies that are sold in a given year were previously on their list. Given how many companies they must monitor just to close a deal (these figures suggest they monitor ~500 companies per successful acquisition in a given year), having a distributed capital allocation function is critical to their success.

In contrast to most M&A that is C-suite driven (even at Berkshire), Constellation pushes down the capital allocation responsibility as much as possible to the individual business units. The idea is that since there are so many VMS companies to potentially buy, having the business units be responsible for ultimately deploying the capital forces each unit to monitor their space aggressively and put more employees to the task, leading to more success than if they had a distant corporate office trying to understand hundreds of different niche markets. Employee bonuses can be docked if they cannot successfully deploy enough capital accretively. The only way having so many capital allocators across the company works though, is to have strict return requirements and rigorously monitoring all deals.

ROIC and Hurdle Rates. Mark Leonard focused much of his early letters on the topic of hurdle rates and tracking investments. With it being typical for the average corporate transaction to miss initial expectations and then be buried in the financials to protect the managers’ poor decisions, it is rare for a company to be so zealously focused on not only consistently hitting their benchmark hurdle returns, but regularly reviewing past transactions to learn from them. Every operating group in Constellation annually reviews each transaction and shares learnings across the company. This has allowed Constellation to make far fewer bad acquisitions and gives them better price discipline when bidding as they know what the highest assumptions they can comfortably underwrite and still meet their hurdle rate. This granular level of deal data that spans ~2 decades and across hundreds of niches cannot be replicated easily.

The net of all of this is very high ROIC that is consistently well over 20%. Below we show how ROIC has trended since 2015. Our methodology is detailed in our full report, but in short we use a figure called free cash flow available to shareholders in the numerator and an invested capital figure that adds back accumulated amortization. (This is different from how Mark Leonard calculates it in their shareholder letters; our full report details the discrepancy in depth, but both calculations show very strong ROICs). It is also worth noting the drop off in 2021 can partially be attributed to certain accounting treatments of the Topicus transaction, with an alternate calculation showing an ROIC that is ~10% higher for an estimated ~24% 2021 ROIC (detailed in the full report).

Valuation. The key questions with Constellation Software are: “How much capital can they continue to deploy?” and “What will the hurdle rate of subsequent acquisitions be?” Given that an investor cannot regularly earn anywhere near the ROI that Constellation can on their investments, there has been shareholder pressure to lower their hurdle rates rather than return capital (they did a large special dividend in 2019). In 2021, Mark Leonard capitulated and lowered the hurdle rate, but only for large acquisitions, as there is a fear that if they lowered the hurdle rate across the entire company, then all small acquisitions would be bid up to the new hurdle rate, lowering ROIC on investments that could have been preserved otherwise.

We believe that giving a potential investor a single number for a valuation would not be that helpful as an investor doesn’t know what we are assuming and their judgement of risk for return can differ. This especially varies based on the investor’s particular situation and whether they are investing under a stringent mandate. Ultimately, all investing comes down to a judgement on whether the return is adequate for the risk, so we view our role here as helping best frame the discussion so the investor can decide for themselves (but that doesn’t mean we are unbiased, and our opinions may leak out quite loudly at points). Thus, in order to best equip an investor to make such a judgement, we find it most useful to lay out the critical assumptions implicit in paying a certain price. To do this, we run a reverse DCF sensitized around various key assumptions.

Below is the table that shows our assumptions. Just looking at the top half of the table, the “Variable Set 1: % of FCF Deployed”, we see three scenarios: 1) 50% FCF deployed, 2) 80% FCF deployed, and 3) 100% FCF deployed. For each scenario, the 50%, 80%, and 100%, is in reference to the starting amount of FCF deployed and it drops based on how much FCF Constellation generates (that is the y-axis that starts with <$5bn). The idea is that as they generate more FCF, it will be harder to deploy it, so we drop the % deployed. If you look at the bottom half of the table, “Variable Set 2: ROIC”, the three scenarios are: A) 15%, B) 20%, and C) 25%. Again, these figures are in reference to the starting ROIC and it drops based on the amount spent annually on acquisitions.

The amounts we model CSI spending on acquisitions may seem rather large, as they quickly compound already large figures. However, in just the past few years, they have increased their total spend on acquisitions materially from ~$580mn in 2019 to $1.7bn LTM. The larger >$10bn acquisitions don’t show up in our models until over ~30 years in the future (depending on ROIC and % FCF scenario). While this may seem unfeasible (and it very well could be), them finding new areas to deploy capital and accepting somewhat lower hurdle rates could materially open up their investment universe. Lastly, we can also think of this ROIC as an ROE, with leverage helping them boost returns (but that would also imply that the amount spent on acquisitions is larger). Of course, an investor is free to only pay for whatever they feel comfortable with. We are just attempting to make explicit the assumptions that are implicit in the current valuation.

The assumptions mentioned above were then fed into our DCF, where we then solved for the discount rate that set the present value of cash flows equal to the current price. The table below lists the assumptions based on the assumptions above, with the starting figures (what is highlighted above) shown on the x and y axes. Lastly, we ran the analysis twice, assuming 0% and 2% organic revenue growth. We assume the 2% revenue growth has a linear impact on free cash flow (i.e. incremental FCF margin is equal to current FCF margin), which may be conservative.

This analysis shows that within our parameters, an investor can expect to earn around 8-13% over the super long-term if these assumptions hold true. We honed in on the 80-100% FCF deployed and 20-25% ROIC scenario as that is around what they are doing currently (Constellation actually deployed over 100% of FCF on average over the past few years). It is on an investor and their judgement to decide whether they believe this to be a fair return (see the full report for risks, and Members Plus subscribers can adjust the model however they wish).

Get much more. Thank you for reading Speedwell’s first PM Summary! We created PM Summaries to make our work more accessible and give readers a quicker synopsis of the investment merits of each business. These PM Summaries will be 5-7 pages (compared to the full 50+ page reports) and cover the core areas of each company. PM Summaries will be released 2 weeks after the full report and cost $9/mo or $99/yr. You can subscribe here: visit www.speedwellresearch.com/subscribe/ and pick the monthly or annual option.

Full Report: Table of Contents

Introduction

Founding History.

Business History.

Business.

VMS Moats.

Other Business Virtues.

Hold Co. Philosophy.

Capital Allocation.

Hurdle Rates and ROIC.

Topicus.

Valuation.

Risks.

Model.

Conclusion.

To read the full report, you can subscribe (or purchase an individual copy of the report) here: