Copart: 1Q26 Business Update (Calendar 3Q25)

Do Volume Slips Threaten Quality Compounder Status?

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(If you are a Speedwell Member, click here to get the full version of this post or here to download a PDF).

1Q26 Update.

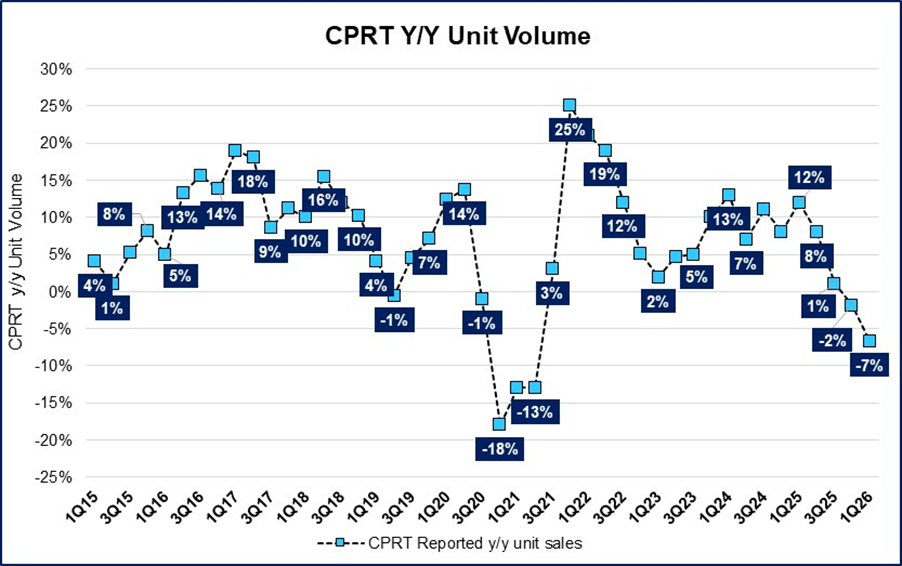

Copart reported fiscal 1Q26 (calendar 3Q25) and the stock was down -3% in trading the following day.

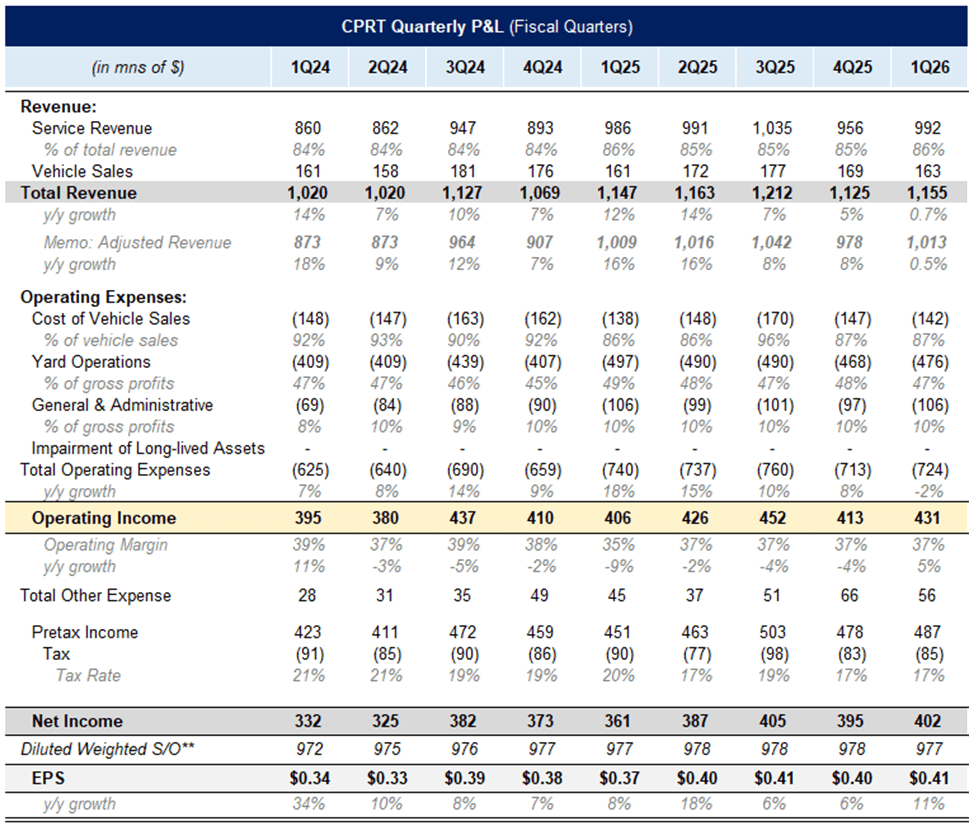

It was a bad quarter with revenue growth of just +0.7%. Adjusting revenues for the cost of vehicle sales (which makes revenues agnostic between 1P and 3P sales), revenues were still up just 0.5%. Backing out last year’s CAT event though, revenues were +2.9%. This is still down starkly from last quarter’s +8% y/y growth.

International revenue increased by +1.6% y/y or +6% y/y excluding CAT. International Service revenue was +8% y/y, or +14% y/y excluding CAT. This is slightly higher than last quarter’s +13% y/y growth. (Service revenue is a better barometer of how the international business is trending because total revenue includes 1P revenues from purchased vehicles which is a business that is volatile and they want to transition to the consignment segment).

The absent growth was driven by weak global insurance units, which fell -8.4%. Excluding CAT volumes from last year’s period, units were still down -5.6%.

The US was even worse with insurance units declining -9.5% or 7.3% ex-CAT. We will touch into what is driving the volume loss below.

ASPs offset this weak performance, with global insurance ASPs increasing +6.8% and U.S. insurance ASPs up +8.4%. In fact, they achieved an all-time high in ASPs for U.S. insurance carriers.

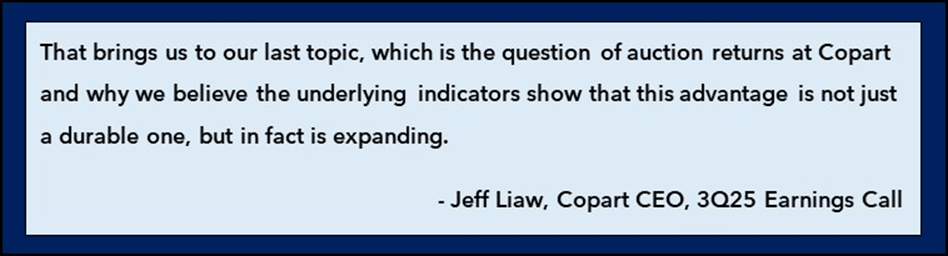

The strong ASPs were definitely a bright spot for the quarter, which is why CEO Jeff Liaw spent time on the call to elaborate on their superior marketplace liquidity, which drives the prices. He believes this isn’t just a current competitive differentiator, but one that he thinks is growing.

In contrast to peer IAA, Copart has way more global bidders, which are an important source of bidding that supports stronger ASPs. On they call they noted, “In the first quarter of 2026, international buyers have purchased vehicles that are 38% higher in value than comparable U.S. buyers by comparison.” Global buyers tend to gravitate towards higher value cars and without that global buying base it would be hard for IAA to handle higher end vehicle volume to the same degree.

Jeff Liaw continued that he thought these were long-term trends: “We believe that these are long term durable trends as population growth and mobility, demand growth outside the United States, outside the U.K., Canada and so forth continues to outpace what we are experiencing firsthand in our origin markets.” In addition, he noted that unique bidders per auction have steadily grown since 2022 to all-time highs.

Moving down the P&L, gross profits grew 5% (or 4% ex-CAT) and operating income grew 5% as they had lower CAT expenses and had tight expense control on Yard Operations.

EPS for the quarter ended up +11% to $0.41 per share.

Business Commentary.

The big debate around Copart is what the main driver of their volume loss is. While management has admitted they lost some market share, Copart has a rationale that would lead an investor to believe it will be cyclical and short-lived. Bears in contrast believe this shift could be a permanent headwind from a change in the competitive environment. Furthermore, fears are percolating that accident avoidant technology is finally showing up in the salvage volume numbers, which will be a lasting secular headwind. There are four key things an investor should know...

The rest of this business commentary, the call notes, and valuation is paywalled.

If you are a Speedwell Member, please click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post, our Copart Research Report, and a large library of other reports!

For further reading, check out our Copart Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Copart (Apple, Spotify)!

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Copart report and all of our other in-depth research reports, shorter exploratory reports, updates, and Plus members also receive Excels.

We have covered APi Group, Appfolio, Airbnb, Axon, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, RH, Porsche, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in CPRT. Furthermore, accounts one or more contributors advise on may also have a position in CPRT. This may change without notice.