CoStar Business History

Creating the Bloomberg Data Service of the Real Estate Industry

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

There is a podcast of this memo available if you prefer listening to it. You can find it on our podcast feed here (Apple, Spotify).

We also have a Company podcast episode on CoStar Group, which you can find here: Apple, Spotify

Founding History.

Andrew Florance was born to a prominent architect, Coke Florance, who designed several notable buildings in the Washington D.C. area, including the Verizon Center and the Torpedo Factory. Coke’s love of buildings fell to his son, Andrew, who also had a fascination with real estate and architecture.

Matriculating to Princeton in 1982, Andrew, who went by Andy, discovered an affinity for computers and the live data they could retrieve. He was on the student committee that oversaw the purchase of Princeton’s first four computers.

While at school, he got a job writing code for a Washington D.C. based developer. Andy poured hours into creating complex discounted cash flows models for commercial and mixed used developments, but was awestruck at the futility of such precision when all of the key inputs were essentially made-up. This was in stark contrast to the data that was available for financial markets.

As he neared graduation, he couldn’t shake the disparity between the incredible data that computers could fetch on the stock market and the near total dearth of information available for real estate.

In 1986, in his Princeton dorm room, Andy started putting together the skeleton of a real estate data service and called it Infonet. He started by collecting publicly available data from the city and cataloging it on his self-modified computer. While he successfully shrunk the file sizes to a workable program, real estate brokers didn’t have computers back then, so he pivoted to a low-tech solution: print.

Using the data he gathered, he started publishing a phonebook-sized real estate guide called “Cornerstone”. This project would run its own course for a few years before being acquired, but it was always limited by his ability to distribute the publication. After college, Andy wanted to take on his own real estate projects, noting retrospectively to the Washington Post in 1994 that “I was going to become a real estate tycoon”.

However, Andy struggled to find a property and again was struck by how low quality the available data was. The best data was manually collected by each individual broker, which was inefficient and greatly limited by their network. So, he shifted to creating a software program that could collect data from building owners and brokerage firms, not just limiting his data service to the select, and often dated, information that the city’s public filings contained.

Working out of his parents’ basement, he started manually collecting as much data as he could. As a one-man shop though, it was challenging. A year in, he was broke. Luckily, a local lawyer, Michael Klein, who was dealing with a slew of S&L bankruptcies, was shocked by how poor most of the commercial data that banks lent on was. When he happened upon Andy’s real estate data service, it seemed like the perfect solution to help banks stave off future poor lending decisions. Michael helped arrange a small pool of investors that included David Bonderman, and with that, in 1987, the Reality Information Group was born.

The Greyhound Building was one of Coke Florance’s favorite projects in Washington D.C.

Business History.

As the real estate industry went through a period of softness driven by high interest rates and a lending contraction, brokerages and commercial real estate owners were especially receptive to a data service offering that could help them cut expenses. Their core offering, CoStar, focused on office buildings and was distributed via floppy disks. Real estate brokers, usually guarded with details of their listings, had more of an impetus to share data in hopes of generating more activity as their limited networks weren’t sufficient in the weak macro backdrop. In the coming years, Reality Information Group would try to gain dominance locally with the most comprehensive offering and would outcompete competitors like Cor/Net for clients.

By 1992 they started expanding beyond Washington D.C., first to Baltimore and then to New York in 1994, followed by Los Angeles, Orange County, Chicago (through the acquisition of Chicago ReSource, Inc.), Philadelphia, San Francisco (acquired New Market Systems), and Boston. As Reality Information Group built out or acquired commercial real estate data for more cities, they slowly moved from local to national player. More geographic coverage helped them get firms, rather than just individuals, to sign-up for the service, which was important for reducing churn.

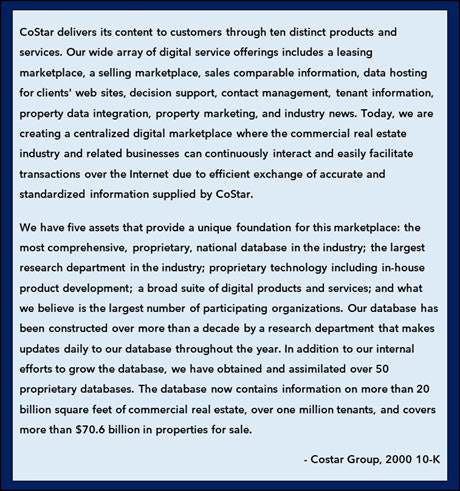

By 1998, Reality Information Group already felt they had no national competitors for their database tracked 122k buildings, 76k tenants, and over 6.9bn square feet, but the market was still in early innings. They prepared for an IPO while eyeing acquisition targets to expand their local datasets.

By 1997, Reality Information Group was generating ~$8mn in revenues with two main products: 1) CoStar, a product primarily used by office and industrial real estate professionals which granted them access to a database to analyze leasing options, property comps, and market conditions, as well as helped with making presentations, and 2) CrosTrac, a product that helps tenants find office space and for office building owners to fill vacancies. Reality Information Group also had a significant and growing amount of advertising revenue from the placement of ads on their site and software products.

With strong revenue growth and a favorable IPO environment, their 1997 operating loss of $3.3mn was no obstacle to going public. In 1998, Reality Information Group went public with an offering of 2.5mn shares at an initial offering range of $9-11, giving them a market cap of ~$80mn at IPO. They used their proceeds to continue to expand their offerings and acquire more related businesses.

One of their first post-IPO acquisitions was Jamison Research, which was the leading provider of industrial real estate information in Atlanta and the Dallas/Fort Worth area. They originally tried to IPO in conjunction with the acquisition of Jamison, but it complicated the IPO and was ultimately put off until after their IPO. This would be the first of many times that Andy would use proceeds from an equity offering to fund an acquisition.

A year later, in 1999, they renamed the company CoStar, after their most popular data offering, and consummated a second primary offering, this time raising ~4x as much money—just shy of $100mn.

They used a portion of those proceeds to acquire several more companies: LeaseTrends (Midwest and Florida expansion) and ARES in 1999, Comps.com (San Diego expansion), First Image Technologies in 2000, Napier Realty Advisors in 2002 (Portland Expansion), and Property Intelligence plc in 2003 (which gave them a foothold in London and other UK markets). Since IPOing, revenues ballooned almost 10x to $80mn, but losses stayed roughly flat at $4.7mn.

Explaining the lack of operating leverage though was the fact that their P&L aggregated more “mature” markets with emerging markets. Despite consolidated losses by the end of 2000, CoStar noted that “established regions”, regions that have been in operation for at least 18 months, had positive cash flow. These established markets, like Washington, New York, Los Angeles, Chicago, and San Francisco, helped support the growth in their emerging markets. Their expectation though was that as long as they kept growing and investing in new offerings, GAAP profitability was not going to be the short-term aim. It wouldn’t be until 2003 that they turned EBIT neutral and not until 2004 that they showed a profit with a 6% EBIT margin.

By 2008, CoStar exceeded $200mn in revenues with a strong revenue growth CAGR of 17% since 2003. With such top line growth came increasing operating leverage—by 2008, margins had expanded to 19%.

As was similar for many companies, the financial crisis revealed weaknesses in many business models. There were fears that CoStar, as a provider to the industry hit hardest by the financial crisis, would prove to be a very cyclical business, and one that was potentially unduly benefiting from the early 2000s real estate boom.

Instead of exposing weakness though, the financial crisis proved CoStar’s resilience.

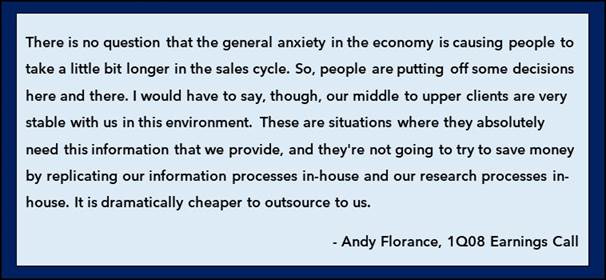

In 3Q08, Andy noted that firms that had been with them for more than 3 years had a 95% renewal rate versus those who were with them for less than 3 years having 70%. This difference was explained by the large number of new firms and brokers that entered the market during the frothiest years of the real estate boom. For those that stayed in business, as CFO Brian Radecki points out below, no matter how bad the industry was, their product was still in need.

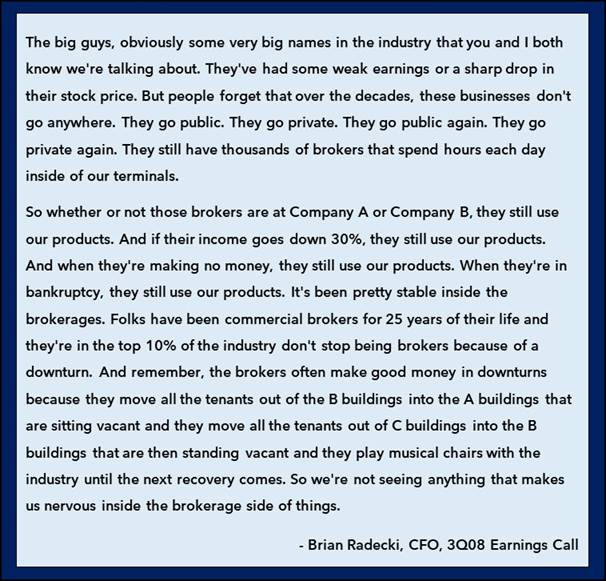

This meant that despite the worst economic crisis since the great depression, CoStar not only pulled through unscathed, but actually hit their ambitious U.S. EBITDA margin target of 30% by the end of 2008—a quarter early. In 3Q08, their U.S. business hit a 33% EBITDA margin, showing the leverage in the model. This was in spite of CoStar continuing to invest more in their offering.

While competitors and most of the industry focused on cutting costs, Andy was focused on providing customers a more detailed and encompassing scope of information. As he noted in 4Q08, “keeping an eye on costs and minimizing spending are the watchwords of this recession, but even more important, I believe, is keeping the focus on our customers and ensuring that CoStar continues to provide the type and quality of information they expect”.

On the same call, he made clear that “the last thing we want to do in our position is to harm our business by reducing the quality or scope of our research product. Those of you who followed our company for any length of time know that we invest for the long term and have managed our business conservatively over the past two years”. With ~$200mn in revenue in 2008, they believed this business could be a $1bn opportunity and were focused on distancing themselves from their “weakened competitors”.

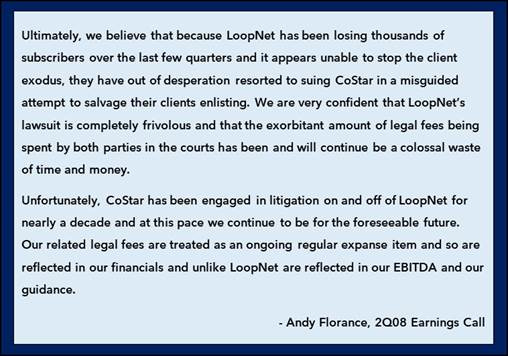

One competitor, LoopNet, CoStar had been in litigation with for years. LoopNet is an online commercial real estate marketplace that enables users (typically property owners, landlords, and commercial real estate agents) to list and market properties for sale or lease. One of the earlier lawsuits was about whether LoopNet violated copyright law by hosting pictures on their site that CoStar took. The hiccup was LoopNet’s claim that it wasn’t them, but rather the users that posted photos to LoopNet. In 2004, this case’s verdict was ultimately in LoopNet’s favor, holding that they were not liable for direct copyright infringement. Interestingly, this case set some of the first precedence on internet service provider liability.

In 2007, LoopNet filed a complaint over CoStar’s use of data contained on a LoopNet listing when it was forwarded to CoStar by the very broker who inputted the data on LoopNet in the first place. CoStar filed a cross-complaint that LoopNet had violated and breached the terms of an earlier agreement that stated CoStar may use listings for the public portion of LoopNet’s website.

Andy’s position on the lawsuit was clear:

Such litigation is important to not just defend CoStar’s intellectual property, but also ensure users don’t take their data without paying. It was all too common for a firm to get a single login and share it with all of their brokers, or for one broker to use another’s login. Unlike Netflix, which was aware of such password sharing but allowed it as a means to acquire additional customers and reduce churn in the early years, CoStar was in a very different position. They already had very high customer retention (by 2Q10 it was up to 97%) and the cost of a seat was far greater than any potential “free advertising” benefit. Additionally, it is a business product that helps generate revenues, and thus CoStar has much greater leverage to compel a user to pay for their service (versus Netflix where a consumer can find alternative forms of entertainment). For these reasons, CoStar has always clamped down on product theft and quickly built a reputation for being litigious for misuse. Customers would have to abide by the terms of service or risk getting sued.

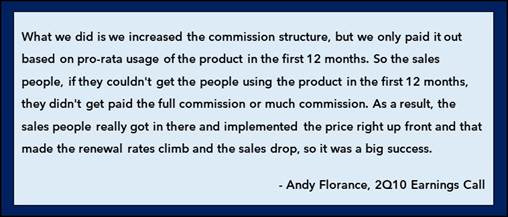

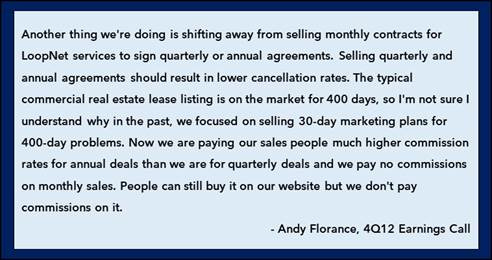

CoStar wasn’t just concerned with paying users though, but the actual usage of that product. Whereas competitors would incentivize their salesforce on product signups, CoStar created a commission structure for their salesforce where they couldn’t earn their full commission unless the people they signed up actually used the product. This incentivized the sales people to focus a lot on new customers and make sure usage was high in the first year in order for them to earn their full commission. CoStar benefitted because users who actually use the product are much more likely to be retained. This was a key reason why CoStar’s retention through the crisis was so high.

By 3Q10, reengaging dormant users (what they called creating “green bar users”) helped boost retention on clients who had been with the firm for less than 5 years from 74% to 87%.

While focusing on their core product, CoStar continued to add to their suite of services, mostly through acquisitions. In 2009, they acquired Property and Portfolio Research (commercial real estate research) and Resolve (real estate portfolio management software), among other businesses. These acquisitions helped them improve existing offerings, but the four CoStar Services (called CoStar Property Professional, CoStar Tenant, CoStar Comps Professional, and FOCUS services) were still the main cash flow generators, contributing over 94% of total revenues.

A few years later though, CoStar had embarked on one of their most ambitious acquisitions to date—acquiring the company that they had spent the better part of a decade in courtrooms suing. In 2011, they offered $860mn in cash and stock for LoopNet. CoStar’s market cap was ~$1.5bn at the time, making LoopNet easily their largest acquisition to date.

LoopNet is a commercial real estate marketplace that focuses more on casual users versus CoStar’s core professional customers. As such, LoopNet’s traffic handily exceeds CoStar’s with 4.8mn registered users and 6mn quarterly unique visitors. Listings are typically input by the real estate agent or owner in order to market the building to a seller or lessor. While this saves cost, it also means fewer listings and that real estate data is limited to properties that are or were recently on the market. Additionally, their focus on casual users led to lower pricing and shorter-term contracts, which came alongside higher churn.

By 3Q12, just shortly after the acquisition closed, Andy would boast that the average LoopNet commitment increased from $37k to an aggregate commitment of $4.6mn. This incredible 125x increase was attributable to 1) price increases, 2) contracts that moved from monthly to quarterly or yearly, and 3) signing up whole firms rather than just single individuals. Together this didn’t just mean they monetized the platform better, but also reduced churn, increasing both variables of LTV.

Prior to CoStar’s acquisition, LoopNet’s listings were a mix of free and paid. LoopNet couldn’t charge for listing creation because they needed a critical amount of data in order to stay relevant. CoStar however already had a much more comprehensive database. With LoopNet’s already large audience, eventually CoStar was able to make all listings on LoopNet “paid”. This helped separate out the functionality of the two platforms: CoStar would primarily be about data and analytics, while LoopNet was for marketing. (This transition would not be completed for a several years though, in part because of conditions of the consent agreement from the FTC in order to get approval for the acquisition).

Each acquisition typically diluted their margin as these services under-monetized and the amortization expense running through the P&L grew from the acquired intangibles. Because of the large amortization charge, free cash flow tended to run higher than earnings—almost 2x higher than earnings in 2012 for example (when operating margins hits a local minimum).

Just a few years after the LoopNet acquisition, CoStar undertook what would become possibly their most important acquisition: Apartments.com. No longer just a commercial and professionals focused real estate service, the acquisition of Apartments.com would mean CoStar would now serve the general public.

CoStar purchased Apartments.com for $585mn in cash. With Apartments.com having 2013 revenues of...

This concludes the free excerpt of our report, to read the rest of the 94-page report, become a full Speedwell Research Member today or you can purchase a single report!

CoStar Group Table of Contents.

Founding History

Business History

Business

Industry

Residential Home Sales

Multifamily Rentals

Commercial

Competition

The CoStar Suite & LoopNet

Apartments.com Network

Other Assets

Other Initiatives

Ten-X

Residential

International

ROIC, Capital Allocation, & Culture

Valuation

Risks

Summary Model

Historical Model

Summary Model

Conclusion

(Please reach out to info@speedwellresearch.com if you have any issues or need to speak to us to become an approved vendor in order to expense the membership).

Read more about our CoStar Group Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our memos, and “interviews”.

Check out our 2 hour+ podcast on CoStar Group: Apple, Spotify

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).