Coupang: 2Q25 Business Update

Boosted Confidence in Taiwan, Growing Selection, and Execution

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members click here for an extended version of this post or find a PDF here.)

2Q25 Earnings Update.

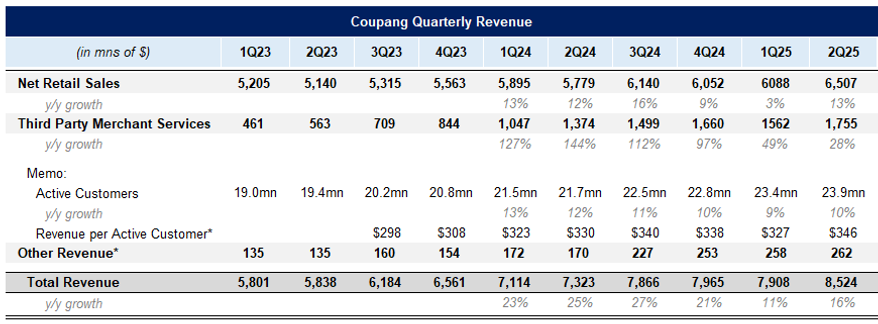

Coupang reported 2Q25 earnings and net revenues grew +16% y/y, or +19% y/y on a FXN basis.

Gross profits grew +20% y/y or +22% y/y FXN. As they shift more commerce from First-Party (or 1P, where the full item value is recorded) to Third-Party (or 3P, where only the sales commission is recorded), their revenues have been growing slower than gross profits.

Product Commerce gross profits grew +23% y/y to $2.4bn (+26% FXN). Adjusted EBITDA was $633mn, +20% y/y and yielding a margin of 9%. They are already within reach of hitting their long-term guidance of 10%+ adjusted EBITDA margins.

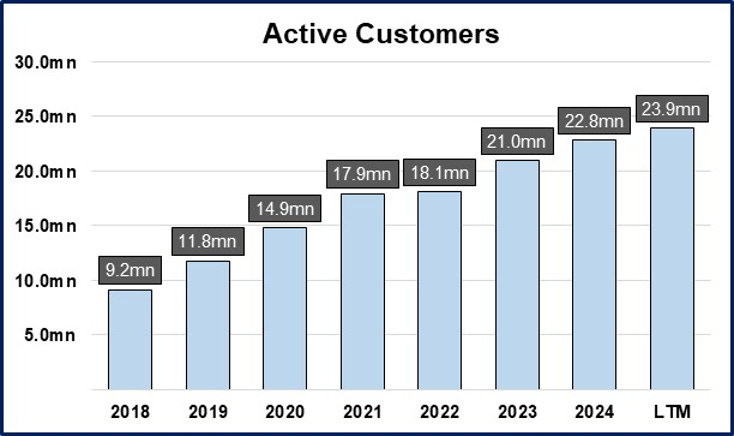

Active customers grew +10% y/y to 23.9mn. For context, South Korea has a population of about 51mn and about 23mn households.

Developing offerings continues to generate losses to the tune of $235mn for the quarter. This segments revenues grew 33% y/y to $1.2bn.

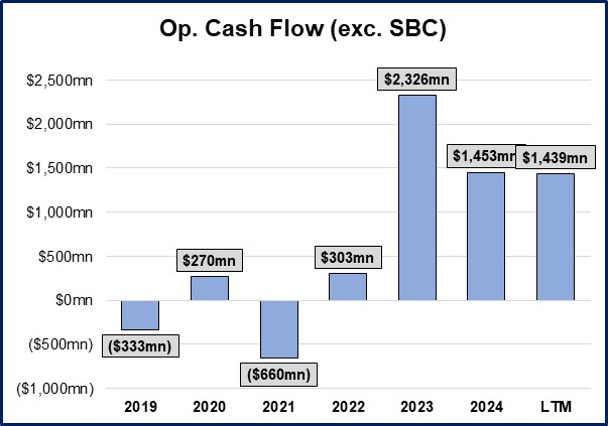

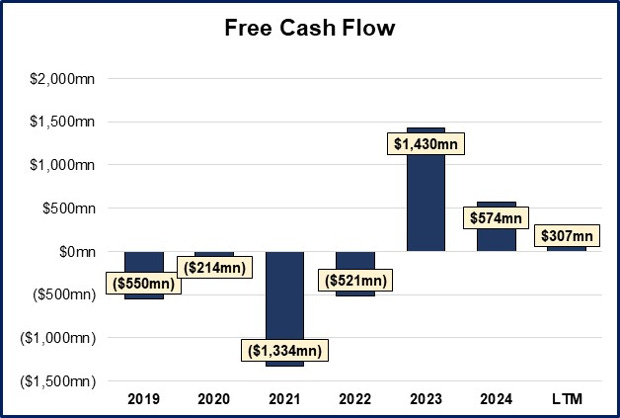

Operating cash flow was down y/y as they had positive working capital dynamics in the comp period. Free cash has compressed as they increase capex.

On the call Bom Kim noted that “we remain in the early stages of a multi-decade journey to transform commerce and WOW customers across the markets we serve”. We estimate they have about 10% penetration of the total retail TAM and remember that the South Korean retail environment lacks a lot of specialty chains stores.

We also have written about how Coupang simply needs to continue to increase their selection in order to continue to win incremental customer orders—this quarter they added over half a million new items on Rocket.

Selection growing sales was neatly exemplified in their Fresh category (grocery) where they increased selection and noted “Fresh’s strong performance underscores a broader pattern we’re seeing across multiple categories, where customers continue to respond with enthusiasm to enhancements in service levels and product selection.”

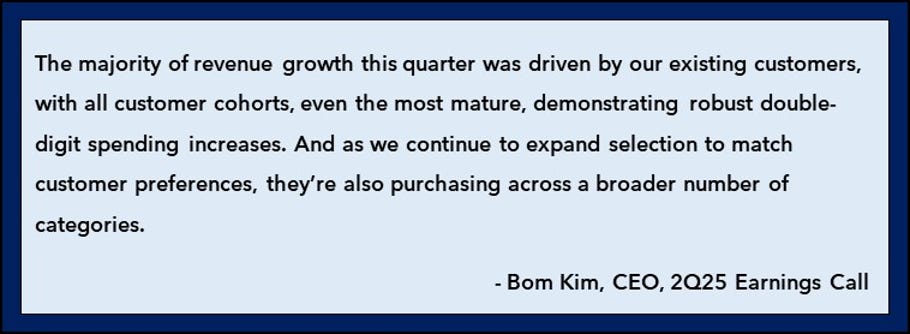

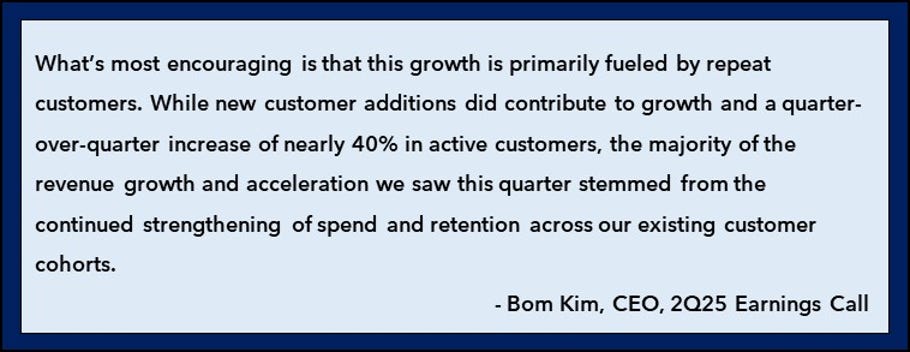

Sales continue to be driven by existing customers, increasing their activity on Coupang.

Another large driver increasing customer activity is FLC (Fulfillment and Logistics by Coupang). Bom Kim noted “FLC continues its impressive momentum, with volumes, selection, and sellers all growing several times faster than the rate of the overall Product Commerce segment.”

70% of SME sellers operate out of Seoul, which Bom Kim said helps “economic revitalization for underserved regional economies in Korea”. A point he might have included in order to help showcase the good Coupang does as scrutiny increases with them becoming one of the largest companies in South Korea.

On their Developing Offers, Bom Kim said: “Our Developing Offerings portfolio is positioned to unlock significant market opportunities and generate meaningful cash-flow streams in the years ahead.” Whereas last quarter they talked about forging relationships with global suppliers, this quarter they note they have hundreds of top brands working with them.

“Our Taiwan offering is growing faster and stronger than even the most optimistic forecasts we set at the beginning of the year.” This quarter they experienced +54% q/q growth, almost twice the run-rate at the end of 2024. Y/y growth was triple digits, and they expect it to accelerate in 3Q.

In contrast to their entry into Japan, they are quickly seeing product market fit that supports pouring more resources into the growing market. They now see a full year loss of $900 to $950mn in developing offerings as a result.

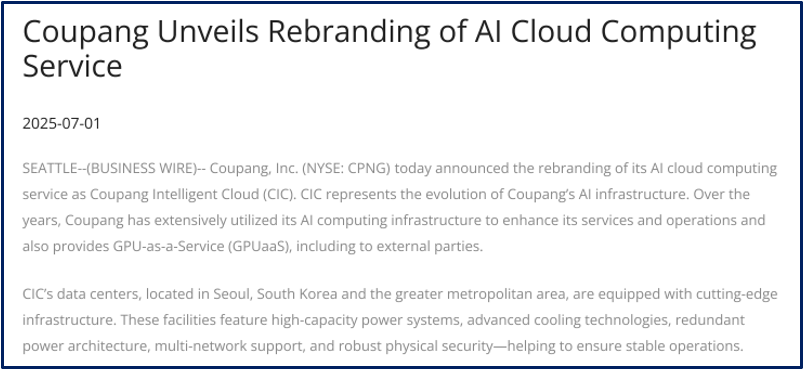

There is potential for a new offering: cloud computing. They released a press release at the beginning of the month that they rebranded their cloud computing service to Coupang Intelligent Cloud.

On the call there was a question about the news that Coupon had applied for a government project to manage some of the GPUs that the government is trying to procure.

While Bom Kim’s call commentary didn’t seem to suggest this was a focus, he did note that they have been building out their own AI compute infrastructure for internal needs for years. Similar to Amazon and AWS, they have toyed with the idea of offering it to external customers and have just started to test that. Given that they are very late to the market, they have formidable competitors in Google, Amazon, and Microsoft. However, vying for government business makes sense at they would have an advantage as they are a Korean business, which could quell some data concerns. They also could have more success selling to other Korean businesses because of cultural differences and a desire to multi-cloud their infrastructure.

Business Commentary.

Coupang continues to execute in their core business and is showing early signs of success in a new market—Taiwan. This is the first time that a developing offering has a good shot of meaningfully expanding their TAM. Eats and Play are nice churn reductions and perhaps could become a decent business at maturity, but retail is still their profit center.

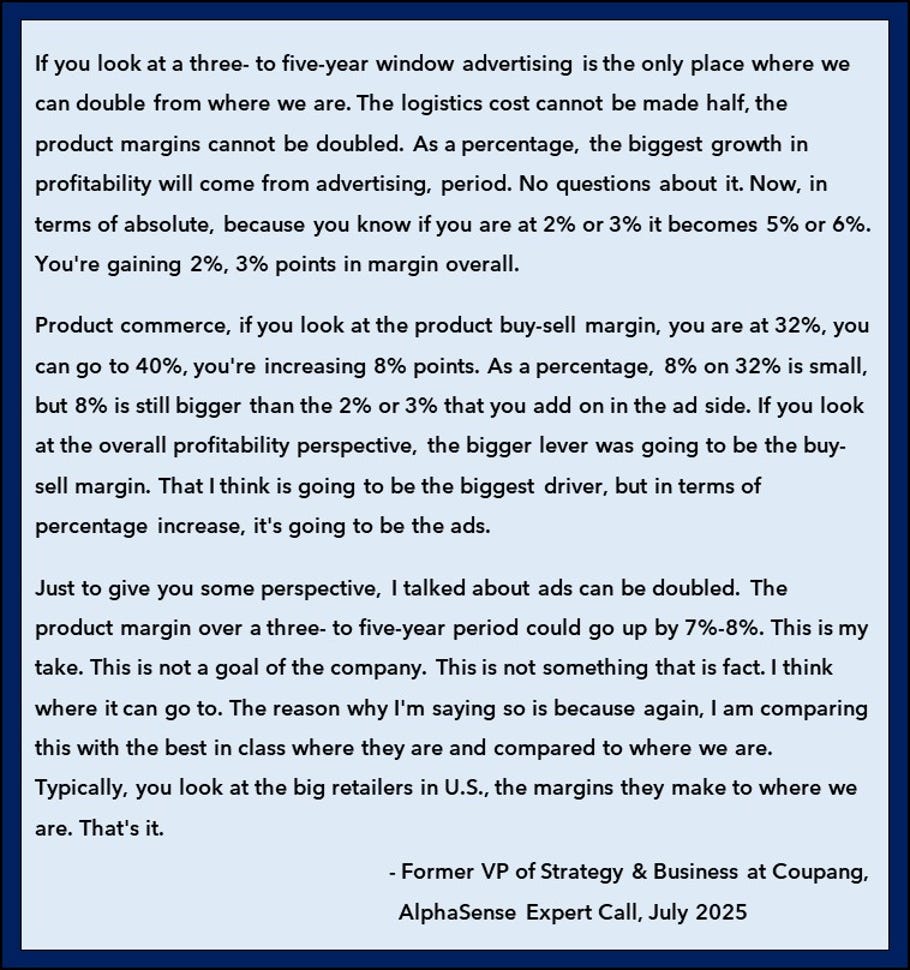

Despite already achieving 9% adjusted EBITDA margins in their Product Commerce segment, they have the opportunity to materially improve margins. In an AlphaSense expert call from earlier this month, the Former VP of Strategy & Business at Coupang believed Coupang could improve margins from advertising and gross margins expansion. (Free trial link).

He believes that advertising margins could move from 2-3% to 5-6%. It is not entirely clear how he is calculating that, but we believe when he says margin he is referring to profit as a % of GMV (not revenue). This is in-line with the general rule of thumb for marketplaces to monetize sponsored ads at ~5% of GMV.

The second, and larger, source of margin improvement this expert sees is from gross margin improvement. In the interview he talked about how he had analyzed many retailers and believes that they should be able to get closer to 40% gross margins as they increase in scale and improve product procurement. He is carful to note that this is not the companies view, but his own. Nevertheless, it seems likely that as they continue to grow, they will be able to negotiate better with suppliers and get even better bulk volume discounts. Despite them already being sizeable (~$45-50bn in GMV), getting product costs down can be a multi-decade journey.

He also noted that combining split shipments is another opportunity. Basically, Coupang customers order multiple times a day and usually each order is immediately processed for shipment so they can meet their rigorous 7 hour delivery promise. However, if they can better utilize data to know how long they can wait before they actually need to box that item, then there is a good chance that they can add a second item to the order because customers can order multiple times a day. This is a notable cost savings unlock.

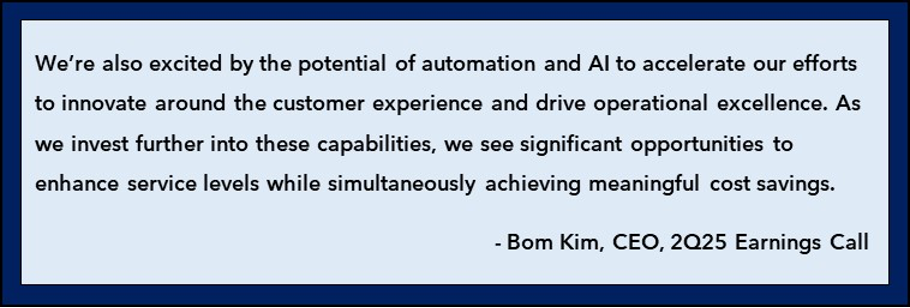

Bom Kim on the call talked about how more AI can help drive operational excellence. This is just one potential area.

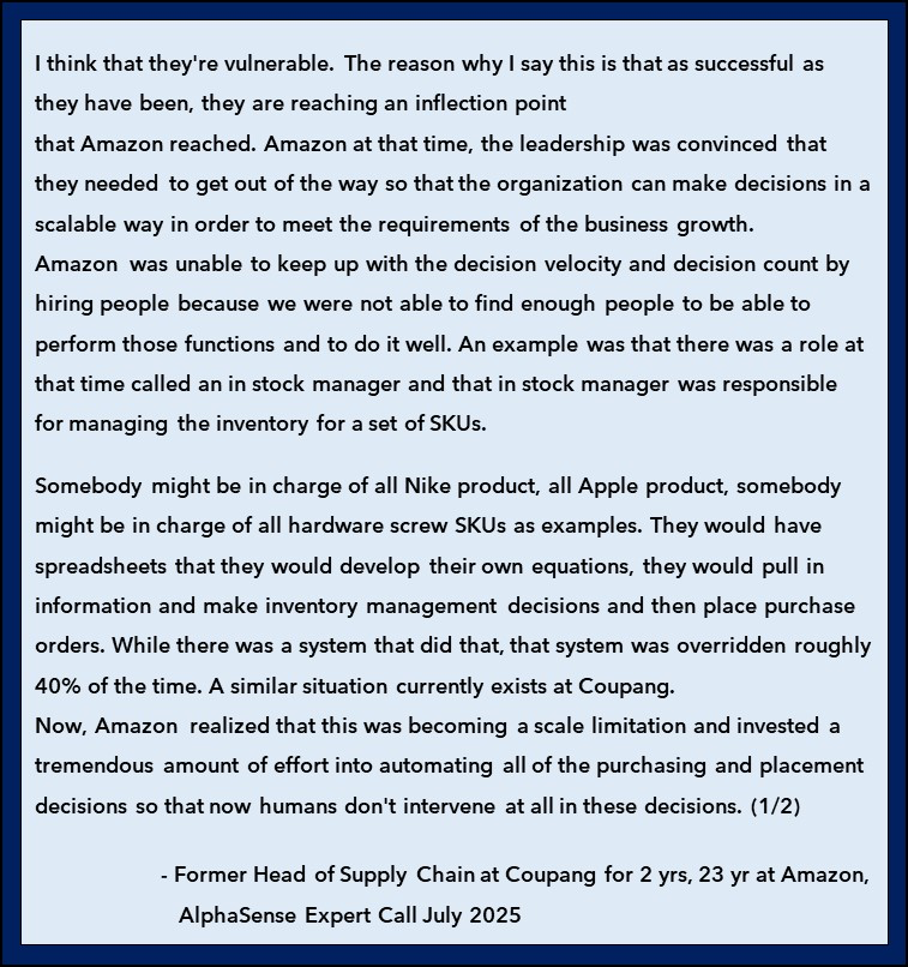

However, a former employee who spent 2 years as a Head of Supply Chain at Coupang after spending 23 years at Amazon was much more pessimistic on their ability to automate more of their back-end systems. As an example, he noted that a lot of procurement was still done manually and there was internal resistance to changing.

It is hard to know how much his experience is representative of Coupang as a whole, as it certainly seems like Bom Kim is trying to automate the process as much as possible to squeeze every last ounce of efficiency out of the system, however it is possible that throughout the organization there is more complacency. I also found his casual comment that “a company that is willing to put in that kind of investment has an opportunity to surpass Coupang” as being somewhat cavalier and seemingly misunderstanding how hard it is to operationally execute what Coupang has already done.

Coupang was not a first mover in the ecommerce industry—they were over a decade late to enter into general retail sales and won primarily on doing simple things better. While we want to respect his opinion and experience, it is hard to square it with Coupang being the first organization to deliver millions of items in under 7 hours across the entire country—and improving on that virtually every quarter.

There are certainty plenty of places that Coupang can improve on though. Among which is their advertising self-service tools. As the expert below notes, a lot of advertising still relies on relationship managers, which is inherently unscalable. Unlocking advertising from SMEs will help increase bid density and inventory for their advertising offering. This will improve their ad revenues, while also allowing them to show more appropriate ads to consumers (because of the larger pool of inventory to pick from).

By and large, this quarter was just another period of execution with no material change to the longer-term thesis.

Valuation.

Below we update our Reverse DCF, but another high-level to think of valuation is as follows...

The rest of this update is only accessible to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

Click below if you want to become a Speedwell Member to read this post and our Coupang Extensive Research Report, PLUS all of our other research!

For further reading, check out our Coupang Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Coupang (Apple, Spotify).

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Coupang report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered APi Global, Airbnb, AppFolio, Axon, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in Coupang. Furthermore, accounts one or more contributors advise on may also have a position in Coupang. This may change without notice.