Dream Finders Home Exploratory Report

Releasing Free Our First Exploratory Report

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

We have a podcast episode on Dream Finders Homes too, which you can find here: (Apple, Spotify).

We decided to release for free our our first exploratory research piece. The idea of these pieces is to do preliminary research on a company or industry before we decide to do a full deep dive that requires many hundreds of hours of research. That means that we will most certainly overlook certain aspects of the business. While it is our intention to get a reasonable understanding of the company and industry, since we are not doing our full multi-week research process, these pieces are likely to have some omissions. However, they should still be helpful in getting a reader exposure to new industries, businesses, and ideas. These pieces also may serve as a launchpad for a future full deep dive.

In this piece we cover Dream Finders Home, a capital-light homebuilder that is essentially copying the NVR model. Their high ROIC and very high founder-CEO ownership, in addition to very cogently written shareholder letters is what originally piqued our curiosity about the company. However, as they have a limited public history and have limited investor materials (no earnings calls or conferences and very few founder interviews), we decided to only do an “exploratory” piece on them for now.

Become a Speedwell Member today for access to all of our Extensive Research Reports, including reports on CPRT, CSU, FND, RH, META, and more! Members will also gain access to at least two annual updates on each covered company.

Founding History.

Patrick Zalupski started his professional career at FedEx corporate headquarters after graduating in 2003 from Florida-based Stetson University with a bachelor’s degree in finance. He quickly became disillusioned about the career mobility FedEx offered and instead opted to work with his mom, a realtor in Jacksonville. He learned what made an area desirable and how to price homes. He also learned how to rehab homes and flip them. In 2005, Patrick bought his first foreclosure to renovate, and moved into new construction the following year. His ambitions were limited by the booming real estate market though, which priced him out of much activity. But when the real estate market eventually crashed, that all changed.

Business History.

With the insight that the rapid rise of home prices left behind many buyers at the low end out of the market, he thought that there was still demand for homes at very affordable price points. Lots that were going for $80k a piece two years earlier were now $24k, and with the help of affordable housing financing, he thought this swath of buyers could now afford cheap homes.

In 2008, Patrick and a partner took out a $200k loan from the Clay County Financing Authority, which helps provide affordable housing for those that are below income thresholds. Patrick would convince a landholder to allow them to pay him back after the three homes they wanted to build on his land were sold. Having no other offers, the landholder agreed, and Patrick had inadvertently engineered what would become a pillar of the company: a capital-light strategy where they never outright acquire land before they are ready to build on it. In December 2008, DF Homes LLC was formed.

They expanded quickly, and by the end of 2009, they had closed 27 units. In 2013, they passed 1,000 cumulative home sales and Patrick’s partner wanted out, so he purchased his stake in the business. Patrick then started to bring Dream Finder Homes to new markets: first with Savannah, Georgia in 2013, then Denver, Colorado in 2014, followed by Austin, Texas and Orlando, Florida in 2015. They would continue to add more markets in the subsequent years, and by 2019, they exceeded 2,000 home closings in a single year.

Dream Finder Homes then embarked on a slew of acquisitions: Village Park Homes in 2019, H&H homes in 2020, Century Homes and MHI in 2021. Each acquisition expanded their operations and opened new markets for DFH. The acquisitions were all relatively small apart from MHI, which was ~$580mn including liability assumptions. Keeping in line with their capital-light strategy, DFH did not acquire MHI’s 1,000 finished lots, but did retain a right to purchase them.

In just under a decade and half, Patrick Zalupski has grown DFH from 27 closings in 2009 to >6,800 closings in 2022 for an incredible >45% CAGR. In 2022, DFH generated >$250mn net income with an ROE >40%. Patrick Zalupski, in his early 40s, plans to continue to grow DFH into one of the nation’s premier homebuilders. His nearly 65% ownership stake in DFH makes him a billionaire, and the fact that he has never sold any of his stake shows his belief in DFH.

With that background, we will now move into the business.

Business.

Dream Finder Homes designs, builds, and sells homes in various U.S. markets. They group their markets geographically into six homebuilding segments: 1) Jacksonville, 2) Colorado, 3) Orlando, 4) The Carolinas, 5) Texas, and 6) Other. DFH picks these areas because they are relatively easier to build in compared to other states, have positive population migration, strong local economies, and above national average household income. These factors help ensure newly built homes will find buyers when they are completed.

Entry-level and first-time move-up homebuyers are the primary source of demand (prices start at $300-400k+ depending on market), but they also build some higher-end homes. DFH has a design studio where homebuyers can pick from different finishes and fixtures to customize their homes. They also allow buyers to suggest their own customization features for a premium. The average price of their homes is ~$500k, which has increased primarily as more sales come from the higher-priced markets of Texas and Orlando (their average home in Texas goes for ~$660k versus ~$310k in Jacksonville).

They also operate Jet Home Loans, which is a mortgage originator JV they have a 49% stake in (with the option to buy the remaining 51% in the future) and DF Title, which offers title insurance. These businesses are part of the homebuying process and help them deliver a more streamlined experience. They also have a 49% stake in DF Capital, which is an investment manager focused on investments in land and land development that provides DFH a proprietary source of capital that can typically close on land acquisitions faster than other financings. All of these other businesses are currently not material to DFH’s financials, and their existence is principally to support their core homebuilding segment.

Of their $3.6bn in LTM revenues, over 99% are from their homebuilding segment. Revenues have grown from $500mn to $3.6bn in just 4.5 years, representing a CAGR of ~55%. Revenues have mostly been driven by an increase in home closings, which have increased from 1,408 in 2018 to 7,221 LTM.

Industry.

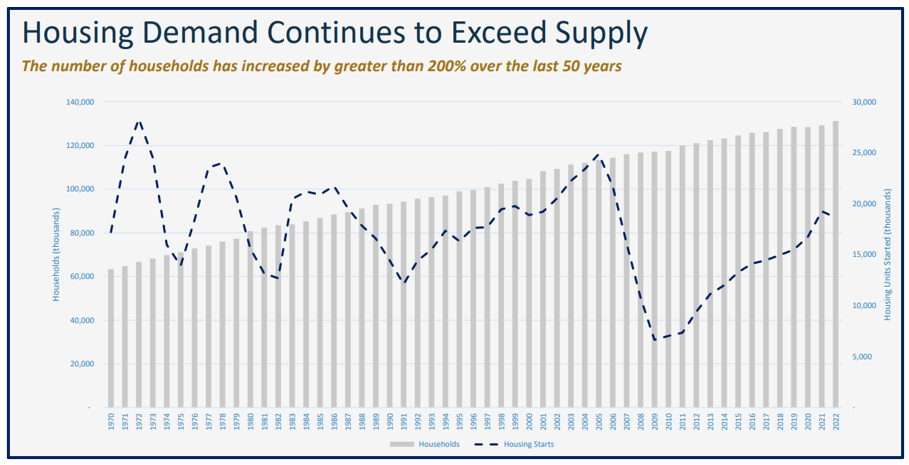

The homebuilding industry has few to no barriers to entry with the Better Business Bureau reporting that there are over 400k homebuilders in the US. However, the vast majority of these are small builders who may have just a small number of projects. There are over a dozen publicly traded homebuilders, the largest of which (DR Horton) closed about 83k homes in 2022. This represents just 8% of the 1.02mn single family homes completed in 2022. Showing how fragmented the industry is, the top 100 homebuilders are estimated to be responsible for completing only half of all homes.

The slide below is from the second largest homebuilder, Lennar, with 66k homes sold in 2022. They note that the annual housing demand of 1.5mn (household formations of 1.2-1.3m, obsolescence of 200-400k, and second home demand of 100-200k) have been outstripping new supply since the financial crisis.

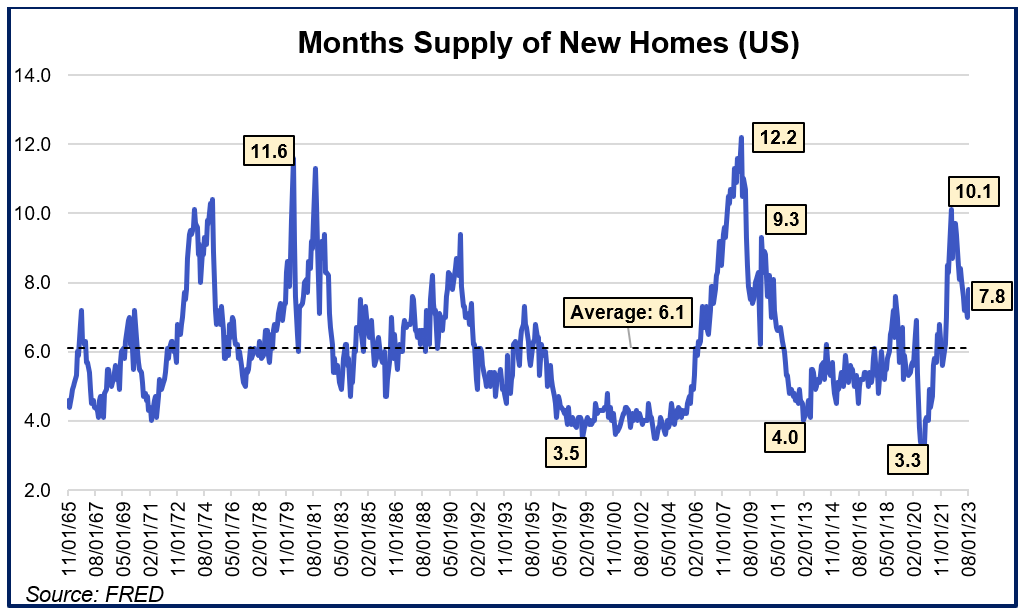

While there was excess inventory in the aftermath of ’08, this was worked through by 2012/2013 where the months supply of new homes was ~30% below average. (Months supply of new homes is the total number of homes for sale divided by the number of homes sold in a month).

Homebuilder Pulte Group (29k home sales in 2022) also estimates housing demand, which includes multi-family, at 1.5mn annually.

DFH notes that new households have continued to exceed new housing starts, suggesting housing demand fundamentals are strong. Freddie Mac estimated in 2020 that there is a 3.8mn housing shortfall.

However, despite most of these charts pointing to a need for more housing, it ultimately is always going to be a question of affordability. Homebuilders can focus on building smaller and lower cost homes, which many of them do, but they cannot create potential homebuyers by making them wealthier. The Fed’s recent interest rate hikes have resulted in 30-year mortgages reaching 8%, an incredible spike from 3% just a few years ago, and 4.5% pre-Covid. Nevertheless, while we may have been used to low interest rates, from 1975 to 2000, 30-year mortgage rates seldom dipped below 7%. Furthermore, from 1979 to 1991, 30-year mortgage rates were in the double digits. While the real rate was lower back then, because inflation ran higher, it doesn’t entirely matter because many homebuyers didn’t have guaranteed inflation-adjusted raises (and loans aren’t originated on future income).

DFH and other homebuilders saw elevated cancellation rates as mortgage rates spiked in 2022, but have already seen that trend reverse and are already just about back to historical rates. (Homebuyers typically put a deposit down prior to the home being built, but can walk away. They may lose some or all their deposit though depending on the agreement).

Higher interest rates are also impacting the mix of existing homes versus new home sales. Higher interest rates make it much more unattractive for an existing homeowner to sell their home as they would face materially higher payments. On a $500k mortgage, the difference between a 4% and 8% mortgage is almost $1,700 a month, which is high enough to dissuade many from moving. Freddie Mac noted that new home sales were up +31% y/y in July 2023. New home sales now represent about 15% of total sales, which is about 4 points higher than the historical average (which is ~+36%).

This section has more macro analysis than we typically do, but it is important to be aware of the big picture home trends and have a sense of the fundamental health of the industry. We are not attempting to time a cycle, but rather build an awareness of the industry where we could potentially spot structural issues. This is all to say there is still a need for more housing in the US, and despite higher interest rates, we still expect people to move and buy homes. High mortgage interest rates will likely sap the supply of existing homes being put on the market, making new home sales all the more important. It may also increase the demand for smaller, lower-cost homes.

It is important to keep in mind that local demand factors are ultimately more important than the national aggregated demand when looking at DFH, which, at ~7k homes built annually, is responsible for <1% of the total new homes built in a given year. DFH focuses on areas that they believe are better than the average American market because of net positive migration, higher than median income levels, and strong local economies. To the extent that DFH is correct in their assessment of an area, it can help insulate the business from macro headwinds. The reverse is also true though, and building in an undesirable area could be disastrous regardless of how strong the economy is.

DFH Business Model.

Referring to homebuilders as “homebuilders” can be a bit of a misnomer because they don’t actually build homes. Instead, they outsource to a network of subcontractors who are responsible for building the homes. Thinking of homebuilders as “home coordinators” would perhaps be more apt as their role is to vet subcontractors, order home designs, locate desirable land, procure materials, oversee the building, provide capital, and then find buyers. (The exception to this is some homebuilders, such as NVR, who have manufacturing facilities that prefabricate walls and other home pieces). DFH will decide to build 200 lots in a certain community and organize all these functions through 3rd parties. While this creates risks as they outsource critical functions of their business, it also makes the homebuilding model easier to scale.

Traditionally, homebuilders like DR Horton and Lennar outright purchase land and then develop it. Land development involves turning unadulterated land into developed lots that are ready for constructing homes on. This process includes installing plumbing, electrical wiring, phone lines, sewers, roads, and getting the proper entitlements (the necessary legal approvals to use the land).

Traditional homebuilders have anywhere from a 1- to 3-year pipeline of land on their balance sheet, and will often develop the land themselves (through subcontractors). Since land development can take anywhere from 20 to 30+ months depending on zoning approvals, this is a relatively unproductive use of capital. To speed up the process, traditional homebuilders may only buy land after they have received entitlements or it has been developed, but they are not consistent in that approach. Traditional homebuilders typically want to purchase land outright because they want to ensure that they have the lots to build on, which makes them more competitive for desirable locations. In contrast, NVR and DFH only buy finished lots that are ready to build on.

To support NVR’s and DFH’s “capital-light” strategy, they rely on land options and land banks. Land options give them the right—but not obligation—to purchase a given plot. They typically have to put a deposit of up to 10% of the price and will forfeit it if they walk away. A land bank is a 3rd party that purchases land and holds it on their balance sheet while it gets developed, and then sells it back to the builder at a predetermined price (more common for DFH than NVR).

This capital-light strategy results in NVR and DFH paying a premium for land, but allows them to have much less capital tied up in the lower return business of land development. (Traditional homebuilders also option land in addition to acquiring it outright). The concern is that a downturn will leave their balance sheet saddled with land that may not be developed for years and that finished homes that can’t be sold, which would require them to freeze future development while stilling incurring construction loan costs. Despite DR Horton and Lennar having an ample pipeline of land, they option 2-3x more land than they own outright.

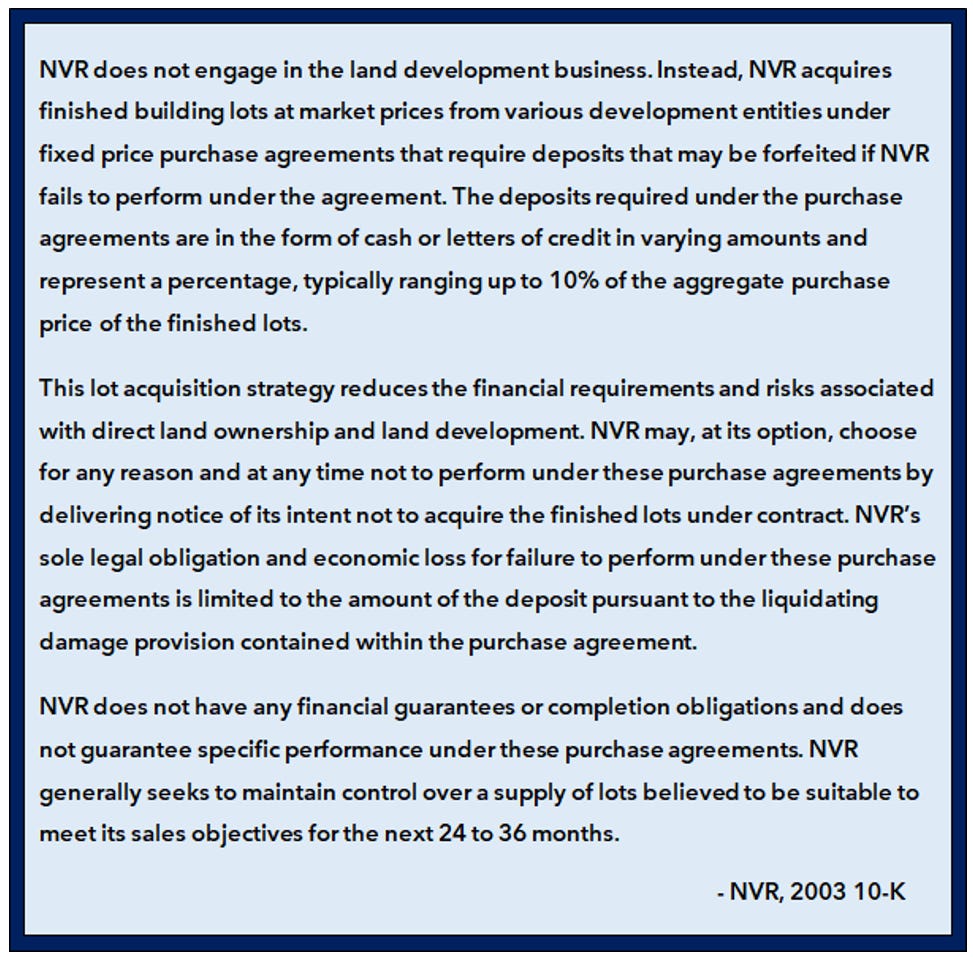

The excerpt below from NVR’s 10k explains their strategy.

DFH notes that they essentially copied the NVR model. The “capital-light” strategy means that they do not buy land until they are ready to build a house on it and they do not build a house until they usually know they have a buyer (spec homes are a small portion of DFH’s buildings, whereas NVR does not spec build any homes). This is in contrast to most builders who will hold many thousands of acres of land in advance of building on it. They do this because they want to ensure that they will have land in desirable areas far ahead of actually needing it. However, land prices can be much more speculative than real estate prices, and are thus more volatile. It is completely possible that a national homebuilder buys a lot for $90k, but when they are ready to build on it, it is only worth $50k, wiping out most of the gross profits of that home. The flipside is that if the value of land increases, the national homebuilder has already locked in their cost basis. (There are also “true ups” that give the landholder the right to participate if there is some upside).

Buying land ahead of time not only opens the builder up to land price risk, but also means they have capital tied up in an asset that could take years to return any cash. It would sort of be similar to an EV manufacturer purchasing stockpiles of lithium years before they ever expect to put it in a car. On one hand, you protect against prices rising and lithium supply unavailability, but on the other hand you tie up capital and take the risk prices fall and you must absorb the difference to be competitive.

Below is Patrick Zalupski’s commentary on why DFH is asset-light and why he admires NVR.

We can see the impact of the asset light approach on DFH and NVR’s inventory turnover versus more traditional builders DHI and LEN. DFH, despite being a fraction of the size as LEN or DHI, has an inventory turnover ratio that is 50% higher. Incredibly, NVR is even higher at more than twice the traditional homebuilders.

While we have been grouping NVR and DFH in same “capital-light bucket”, today NVR has several distinct elements that allow them to be much more efficient than DFH. First, they only start building a home once they get a nonrefundable deposit from a buyer. They never spec build homes. They also will exercise the land option contract only after they have received a deposit. This means that the land is never on their balance sheet until they are ready to build on it, essentially eliminating their cash locked up in unproductive inventory. Over 86% of balance sheet inventory is homes under construction that are in contract to be sold.

The next important element is that NVR has local build density. This means that they will build many homes next to each other. This is important for two reasons. The first is that it allows them to have a building product manufacturer nearby and save on transportation of materials. Second, they can start work on multiple homes at the same time. This is only enabled by getting enough orders placed close by within each building community. For instance, they may ship doors for 6 homes at once and then install them all in the same day. This local building leverage for certain jobs helps save costs. Similarly, having many of their homebuilding community projects nearby also rationalizes NVR setting up manufacturing facilities for building products, which in turn reduces the cost to build homes as production line manufactured products have much higher labor utilization rates and lower defection rates due to standardization. The close proximity between building product manufacturer and home site not only reduces cost, but saves on shipping time.

Also saving costs is NVR’s standardization of homes and home features. Whereas DFH allows more home customization and is willing to incorporate buyers’ desired fixtures for a premium fee, NVR standardizes their builds to a larger extent, with very limited premium features available and fewer styles to choose from. While DFH has a design studio to mix and match different desired finishes, NVR has just a handful of styles to choose from and typically does not allow much customization.

Lastly, the larger a builder is in an area, the more they can spread their selling costs across a larger base of homes. NVR, like other homebuilders, has a direct-to-consumer advertising effort to attract buyers and does not just rely on 3rd party real estate agents to bring them business. The larger the building community, the more they can spend on advertising and the less reliant they become on realtors. Homebuilders have their own sales force that is usually paid a commission on sales, but that is typically less than what a 3rd party realtor gets. (For context, DFH paid $140mn in commissions in 2022, or 4% of revenues). All of these elements from the capital-light approach and local build density to building product manufacturer and larger advertising push translate to NVR’s industry-leading turnover as well as high margins.

While DFH copies some of NVR’s model, they have a more spread-out footprint with building sites spanning from Denver and San Antonio to D.C. and Orlando. (NVR now has a national footprint as well, but their larger scale means each of their four segments are still solidly profitable; even their least profitable geography puts up 16% segment margins).

DFH has continued to open or acquire new markets, which have buttressed their very strong growth, but comes at the cost of worse operating leverage. Starting up new markets can also be lossmaking until they reach critical building density. They entered Orlando in 2015, and by 2018 only had 4% segment margins in that geography. In 2017, they entered the Washington D.C. metro area and weren’t profitable until 2020 with 4% segment margins. The new market opens partially explain their lower margin profile versus other builders. As they gain scale in these markets, we would expect margins to continue to improve, but that could still take many more years until they gain maximal leverage.

While DFH has a better turnover ratio than DHI or LEN, in theory it should be higher given their asset-light model. DFH’s lower turnover vs NVR means they are slower to build and deliver homes. This makes sense given DFH offers more customizations, has smaller scale, and is relatively new to several of their markets. However, looking online at the hundreds of buyer reviews suggests there is another possibility.

It is very easy to find complaints about builds that are slower than promised and homes that aren’t finished on time. Some of this could no doubt be related to the supply chain and labor issues broadly felt in 2021-22, but we didn’t see proportionally as many complaints for NVR or other builders. NVR has a home on its balance sheet for an average of 115 days whereas DFH is at 192 days.

Buyers had many other problems with DFH homes as well from build quality, lack of responsive customer service, and a reluctance to fix problems that shouldn’t have existed on new homes. While they are not alone in having poor reviews as nearly all of the homebuilders have nearly unanimous 1-star reviews, taking into account their smaller size, they have proportionally more bad reviews than their peers. The Better Business Bureau rates DFH a B versus DR Horton, Lennar, and NVR who all got an A+. The ratings do not take into account customers reviews but include items like unanswered complaints, unresolved issues, and volume of complaints.

Looking through employee complaints and online commentary, it seems like DFH is going through growing pains with many employees feeling that they do not have clear roles or the right managers. Others think the company is letting customer issues fall through the cracks. It also seems like the latest string of acquisitions, in particular the McGuyer Homebuilders (MHI) acquisition, which increased their annual home closings by >2,000 (DFH only did 3,000 total in 2020), stressed their managers and operating structure. DFH’s growth is impressive, increasing from under 1,000 home deliveries in 2016 to over 7,200 LTM, but it seems such growth may have come at a cost of consistency and operational efficiency. A conservative investor would likely want to see these issues ameliorated, as a homebuilder who overlooks build quality could have a hidden liability that doesn’t appear until much later. (For the record though, the majority of DFH home buyers do not complain and seem happy with their purchase.)

Looking at ROIC, we can see that NVR has a much higher return on their capital.

ROIC and Capital Allocation.

Below, we calculate DFH’s ROIC and ROE. While we typically prefer looking at ROIC because it is capital structure agnostic, the capitalization of interest in homebuilding costs and inventory makes this a somewhat distorted metric (this is because if they were 100% equity funded, their profits would be higher and inventory on the Balance Sheet would be less). However, even if we were to account for these adjustments, it has a relatively minor impact on ROIC.

Nevertheless, we opted to also show ROE, which rightfully includes all interest expenses. We see that DFH ROIC has increased in recent years. This is partly because of them reaching the local density required in more communities to reach scaled margins.

The slide below shows how in Denver and Orlando gross margins improved significantly as they gained scale in those markets.

We also see though that NVR still has significantly higher ROIC and ROE. This is a product of their higher inventory turns, but also their superior cost structure and more mature markets. NVR’s homebuilding segment has 20% pretax margins for 2022 versus DFH at 9%. NVR also has been a large repurchaser of their stock, reducing their share count by ~20% since 2015, which shrinks the equity base. (ROIC is higher than ROE because they have net negative debt with ~$2.7bn of cash on their balance sheet today. This conservatism is possibly the result of having gone bankrupt in 1992). Free cash flow conversion is also much worse than NVR. Since 2018, only 29% of net income was converted to free cash flow. A figure that has since improved to 88% LTM, but has also been very volatile. NVR in contrast has been near 100% free cash flow conversion.

Part of this is arguably the opportunity: if DFH can improve operations and scale, they could be the “next NVR”. However, creating such a well-run company is no easy feat. Growing and managing an organization well are two very different skills. Whereas NVR has a decade of refining their operations, DFH is still very early in their life.

Additionally, DFH has a shorter history of capital allocation than NVR. In support of DFH is that the couple of acquisitions they have made so far have been at reasonable to arguably cheap prices. The largest acquisition, MHI, they acquired for $582mn including assumption of liabilities. That price included $473mn of inventory and $40mn of land deposits. While they entered Texas in 2015 with building operations in Austin, the “Texas” segment is only MHI (they explicitly note in the 10-k that “the MHI operations comprise the Texas segment” and “other” includes legacy Austin). Knowing this allows us to figure that they ended up paying just a 5x multiple of 2022 earnings (MHI generated $1.3bn of revenues and $112mn in earnings before taking into account their earnout for 25% of profits for 4-years).

Like any homebuilder, ensuring capital is not deployed on projects that take too long to develop is also critical to their long-term success. DFH has division leaders for each market and delegates a lot of the project sourcing to them. They will then get a final approval from corporate, who compares the best use of funds across the company.

While Patrick Zalupski and DFH seems to be saying a lot of the right things, a conservative investor would feel more comfortable after seeing this show up more consistently in the results (especially given scuttlebutt market research). On the flipside though, an investor could argue that DFH is not priced to perfection and the market is already discounting their internal growing pain issues.

Valuation.

DFH trades at a discount at ~7x their LTM earnings versus NVR at ~12x. Both multiples seem to assume a softer housing market will weigh on earnings, but the numbers haven’t shown that yet. New orders have increased from 2022 and while backlogs are down from peak, they have seemed to have stabilized. The limited supply of homes for sale has favorably impacted new home demand, but there are still concerns that higher mortgage rates will impact affordability and ultimately, home sales.

These macro concerns are of course short term in nature, and the market could already be discounting some or all of this (NVR’s average 10-year P/E is ~16x). As a long-term investor, you know that eventually someone will have to build enough homes to close the housing gap, and it seems likely that the existing builders, with claims on desirable lots and a process in place to build, will continue to hold or gain share. While higher interest rates do make homes more unaffordable, people are not willing to push off a home purchase indefinitely.

A 4% versus 8% mortgage is about $1,300 a month more, which is no doubt a considerable amount of money for most Americans. But many who desire a home are likely to cut other expenses or take on second jobs to realize their home ownership dreams. Also, remember that with less existing home inventory for sale, more buyers will be chasing the supply that does exist. Some home buyers may even lower their expectations and buy a cheaper home. Whoever the buyers end up being, the historical data supports that higher mortgage rates do not slow new home building activity. The US built over 12mn homes in 1980, which was more than the ~9.5mn homes built in the 1960s and the same as the 12mn homes built in 1970s. This is despite mortgage interest rates that averaged ~13%. While any given quarter or year could have softer home demand, it seems unlikely that the higher interest rate environment represents some paradigm shift where people no longer buy homes. The important thing is that the builders can withstand any prolonged downturn (whether that comes from softer demand or an increase in existing homes for sale from a recession doesn’t matter). The capital-light model clearly has advantages there, as NVR was able to remain profitable through the housing crash of 2008.

With Patrick Zalupski only in his early 40s and owning ~65% of the company, he has ample time and influence to continue to grow and streamline Dream Finders Homes. We will continue to keep tabs on the company.

Historical Financials.

Conclusion.

Thank you for reading our first Exploratory Piece. As a reminder, these are much shorter and less researched than our typical full research reports, but we nevertheless hope you learned something and enjoyed it!

Please Follow us on Twitter @Speedwell_LLC, Threads @speedwell_research and subscribe to our newsletter at speedwellsnippets.substack.com for periodic updates on DFH and more business content. You can also find our podcast, The Synopsis, here (Apple, Spotify). Please feel free to reach out at info@speedwellresearch.com if you have any questions or comments.

*At the time of this writing, no contributor to this report has a position in DFH. Furthermore, accounts that one of more contributors advise on do not have a position in DFH. This may change without notice.

Thank you for reading this sample Exploratory Report! If you’d like to subscribe and gain access to our full Research Reports and future Exploratory Reports, you can do so below!

Dream Finders Homes Podcast.

Speedwell’s Podcast, The Synopsis, released an episode just on Dream Finders Homes. You can find it below!

If you like DFH, you will love Vistry (VTY.L). Capital-light homebuilder fully focused on a partnership model (land coming from a land bank provided by the Partners - typically housing authority of REIT). Although its has 12% Op margin, it can reach up to 40% ROCEmployed. It has a former NVR board member and plans to return 25% of today's market cap to investors in the next three years through buybacks. Also, it reached 16k homes delivered in 2023, $310m in Op profit and valuation still $3.9B