EVO: 3Q24 Business Update

Inflections, Cyber-Attacks, RNG Surprises and Georgia Strike Impact

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

We will provide an update on Evolution through our podcast too. Follow our feed here (Apple, Spotify).

If you haven’t already checked it out, we have a 2+ hour discussion just on Evolution. You can listen to it here (Apple, Spotify).

Evolution: 3Q24 Business Update

Evolution reported 3Q24 earnings and their stock was up ~15% in response.

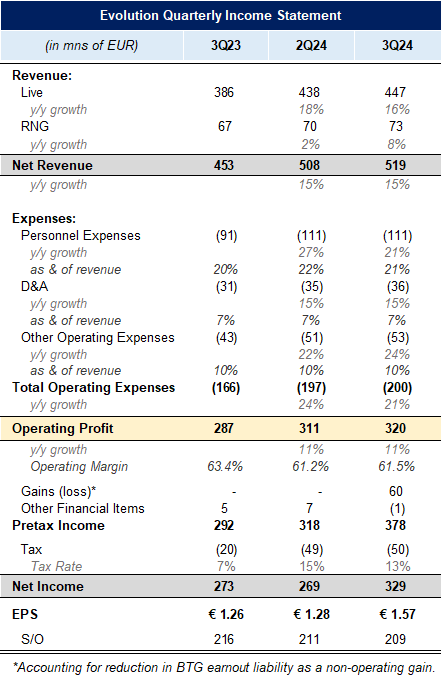

Total 3Q24 revenues were +15% y/y or +19% y/y in constant currency. This not only quelled fears of stagnation, but in the context of the Georgia Strike setback and the Asia-focused Cyber Attacks, these figures look even better.

As we see below, their Live segment grew +16% and RNG grew ~9%. While live decelerated ~200bps q/q, that is still very strong growth and in the call they suggest it would have been even better absent of operational issues, which we will detail below.

After many quarters of lackluster growth, RNG strongly inflected positive. This wasn’t because of an increase in acquired RNG revenue (like in the past), but because of operational improvements, namely from OSS and a slate of new games.

Evolution by Market.

In terms of geographies, we can see that North America inflected +1,000bps q/q to +18% y/y growth. As a reminder, Evolution was the first live casino provider in North America and has since faced a little more competition from Playtech and Pragmatic, nevertheless they are a clear market leader and will continue to benefit not only as more states legalize, but also as they build out more studios and offer more gameshows in each state. They also noted that in terms of RNG they lost market share but grew for the first time in the quarter.

Asia growth decelerated 500bps to +17% y/y, primarily driven by increased cyber-attacks. These cyber-attacks result in increased counter measures, which potentially block players that are playing honestly, but also siphon players away from their legitimate games.

They gave a little more detail on the nature of the attacks on the call: “Cyber criminals use advanced technology to intercept our video feed, manipulate it and redistribute it without authorization, which leads to loss of revenue”. Management also clarified that they did not see any difference in underlying demand and expect it to take a couple quarters before they are back to their “earlier faster growth rate”.

CEO Martin Carlesund said the above quote in the context of Asia’s revenue growth rates being hindered by the attacks.

Impacts to Revenue.

The other big impact to revenues was the Georgia strike disruption, which resulted in them losing some gaming activity. In Mid-July 550 employees went on strike, out of the 7,500 to 8,000 employees in their Georgia studio (this is one of their largest). While this was only a relatively small portion of the workers, around the beginning of August, they started blocking entrances to the studio, vandalizing the workplace, and harassing other employees. Given that Evolution felt they provided fair work conditions, in-line pay, and that negotiating with unreasonable activists could set especially poor precedents, they decided to permanently downsize the Georgia studio.

Many employees were let go and they are now going to keep this studio at only 60% capacity permanently. Below we see that net employee count actually dropped q/q despite increased hiring across many new studios. While this wasn’t a desirable situation, management handled the strike well by properly redirecting resources to minimize client disruptions and not relenting to a minority of activists, which could cause a negative ripple effect across their other operations. (Not that we can’t sympathize with the union employees, but it is almost always a mistake to negotiate after protests turn violent).

While they shifted game priorities around to the highest revenue generating tables, they still lost betting activity.

Below we can see that the activity in the network dropped -5% q/q, a rare occurrence.

CEO Martin Carlesund provided the below commentary on the activity index (which directionally is helpful, but in absolute it is hard to discern any signal from—i.e. it is unclear what a 357 of “activity” means when every game has different betting mechanisms, payoffs, and betting sizes).

Between the strike and counter-cyber security measures, gaming activity was hampered, but new game launches like Lightning Storm and Lighting Dragon Tiger helped to the positive. They are also still early with new features like BetWithStreamer, which allows a player to bet alongside an influencer (there are many popular influencers on YouTube and Twitch who record their betting sessions for entertainment).

Additionally, SpinGifts will help them offer more promotions. If you recall from our report, promotions was historically a weaker spot for Evolution as competitors had better tools to know exactly when and to who an operator should offer a free spin or bet to in order to keep the player engaged. It is good to see further developments here (and OSS, mentioned below, also helps with this because it makes integrations across games and tools easier with the operators’).

Additionally, the inflection in RNG, which management talked about for the past several quarters, finally started to crystallize in the numbers. They attribute OSS to a large part of this success. OSS is One Stop Shop and is basically their integrated gaming lobby that directs users to more of their games when they are done playing, instead of going back to the operators lobby. They have layered in AI-driven recommendations into OSS so the likelihood that a player picks another Evolution game versus a competitor is all the higher.

P&L.

Adjusted EBITDA margins came in at 68.5% for the quarter, driven by the mentioned Georgia strike and increase counter cyber-attack measures. They now expect EBITDA margin for the year to be 68.5%, below their original full year guidance of 69-71%.

These figures are adjusting out an earn-out liability of €60mn related to the BTG acquisition. While this is recorded as “operating revenue”, it is not including in any of the revenues figures in this update (or our tables). Instead, we treat it as a non-operating gain in the P&L below. It is also worth emphasizing that this is a reduction in the earnout they can potentially achieve (liability reduction), not an impairment charge. Evolution commonly uses performance-contingent earnouts on acquisitions to help guard against overpaying for a company.

CEO Martin Carlesund made the below comment on the earnings call in relation to the earnout liability reduction.

As shown below, personnel as a % of revenue fell slightly, which is expected given the employee headcount reduction. This drove a slight increase in operating margins q/q to 61.5%, but they are still down ~200bps relative to where they were a few quarters ago. This is primarily a result of the lower capacity utilization of their studios both because of the Georgia strike, but also because they are expanding studios which take a while to full ramp up.

The net of all of this is EPS was +25% y/y, which is more impressive given the increase in tax rate that kicked in this year (their effective tax rate will about double to ~15%). As a reminder, their earnings do correlate pretty closely with FCF with an average FCF conversion of 95%.

Below we drop in some other updates on the quarter before moving to our business commentary.

Other Comments.

YTD repurchased ~€680mn of stock, leaving them with ~€515mn cash

They noted on the call that they extinguished the existing authorized buyback since the end of the reporting date, which reduced cash by about ~€150mn

Acquired Arcade Gaming Solutions in September

Rumored €2.5mn + an earn out

They help connect mobile players play on physical slot machines

France potentially could regulate

Floated 55% tax though, which is at the high end

Partnership with Atlantic Lottery so can now launch games in all of Canada

Launched first tables in Colombia and Czech Republic. Working on launching new studios in Brazil and Philippines.

Czech Republic studio will primarily serve that country, but can also serve to broaden Europe capacity

Their second studio in Colombia will be a main studio to serve South America, while also serving Europe and Asia

First Philippines Studio shows confidence in regulatory environment in Philippines and broader Asia business

Brazil regulating is a key event in 2025

“We anticipate this market that will pick up the pace in terms of growth during 2025 as the Brazilian market would regulate in early 2025.”

Business Commentary.

While there tends to always be a contention around Evolution, the last several months very much seem like a case of the stock price driving the narrative. Prior to earnings, they were down -24% YTD with speculations that their Asia business was deteriorating on competition, their North America business was stagnating, and new regulatory scrutiny would dispel the end of their unregulated business.

While none of these concerns were new, and readers/ listeners of our Extensive Research Report and Synopsis Podcast knew why this was just a re-airing of old fears, the stock price nevertheless drove much “analysis”.

Most of these concerns were put to rest (again). North America growth inflected a positive +18% y/y. The Asia slowness some 3rd party data trackers observed was due to cyber-attacks, not competition. And the regulatory environment is unchanged. In fact, their opening up of a studio in the Philippines shows their commitment and confidence in their Asian business. (You might recall that most of Asia is grey or black market, but gambling is legal in the Philippines so many operators are based out of there. See our report for a fuller discussion on this).

The Georgia strike was a new (and valid) concern, but management handled that well too. Additionally, after many quarters of promising high single digit growth in RNG, which many discounted, including us, they actually delivered it.

Another “concern” is margin compression. After peaking around 63% EBIT margins, some investors were worried that the increase in studio builds would mean less operating leverage going forward. While this is true to an extent, especially when new studios are ramping up, it is a little wild to lose the perspective that this business still has comfortably earned among one of the highest margins of any public business ever. The cyber-attacks also may increase costs in the short term, but it also increases their competitive position as sub-scale players struggle to invest in proper counter cyber-attack measures. Even with cost pressures they generated a 60% EBIT margin for the past 9 months (61.5% for 3Q24).

At the end of the day, their competitive position is very strong with no competitor having ever gained meaningful market share at their cost in the past several years. (Please read the “Evolution Model” section in our report to understand their competitive position better). And they operate in a very attractive industry, with the economics of not just a casino, but an internet platform.

They are not “a” dominant player in the live casino industry, but “the only” dominant player. And they operate in a market that should continue to grow overtime as more people gamble online and more areas legalize. Remember, there is about a €30bn TAM for online casino (live + RNG) and this is against a global gambling TAM of close to half a trillion. If gambling proves to be similar to other sectors of the economy like advertising and food delivery, then the internet + mobile will only help to continue to grow the TAM.

Lastly, we touch on many risks in our Evolution report, but to be clear slowing growth isn’t a business risk, it’s an investor risk depending on the price they are paying. To better understand how much growth is required for a given investment return, we re-ran our Reverse DCF below.

The rest of this update is accessible only to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

If you are not a Speedwell Member, click here to become one.

Members will receive not just updates from our covered companies, but all of our Extensive Research Reports and our Shorter Exploratory Reports. See the full list of our covered companies here.

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

Solid quarter with plenty of positive surprises. I’ve appreciated your recent podcasts with some fintwit accounts. Keep putting out great content.