Evolution: 3Q25 Business Update

Revenue Falls for the First Time Ever

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members can access a full version of this post here and a PDF of this post here)

3Q25 Update.

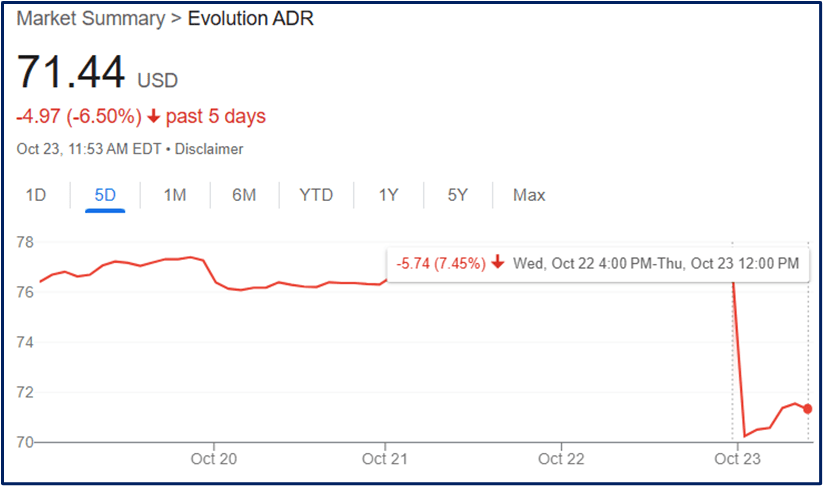

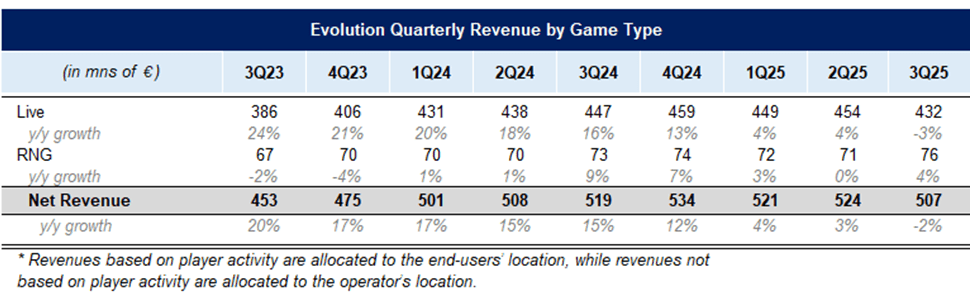

Evolution reported 3Q25 and the stock was down -7%.

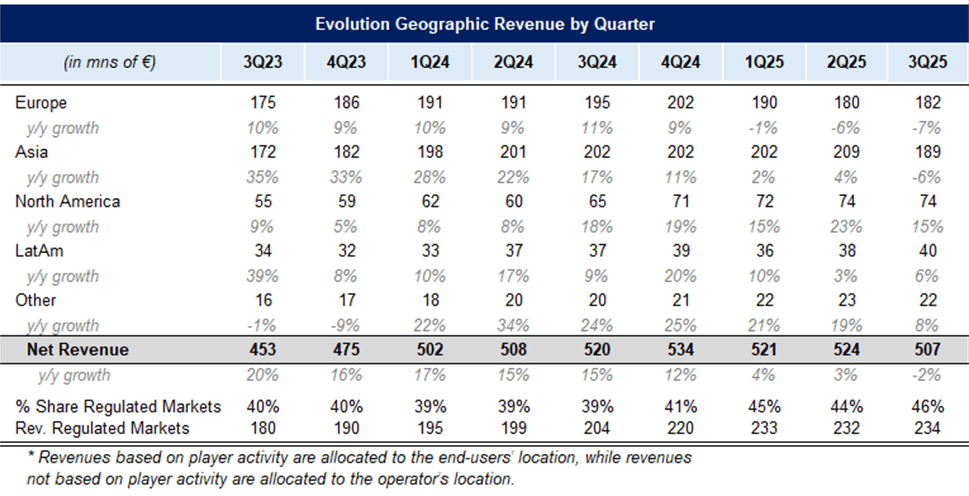

For the first quarter ever, they reported a contraction in y/y revenue. Total revenues shrunk -2% y/y, driven by weak performance in Asia of -6% y/y and Europe of -7% y/y as their ring-fencing efforts continue in the EU.

The Asia revenue contraction was a surprise as they seemed confident that they were starting to get a grip on the issue last quarter with Asia revenues growing by +4% y/y after essentially being flat q/q for the previous 4 quarters.

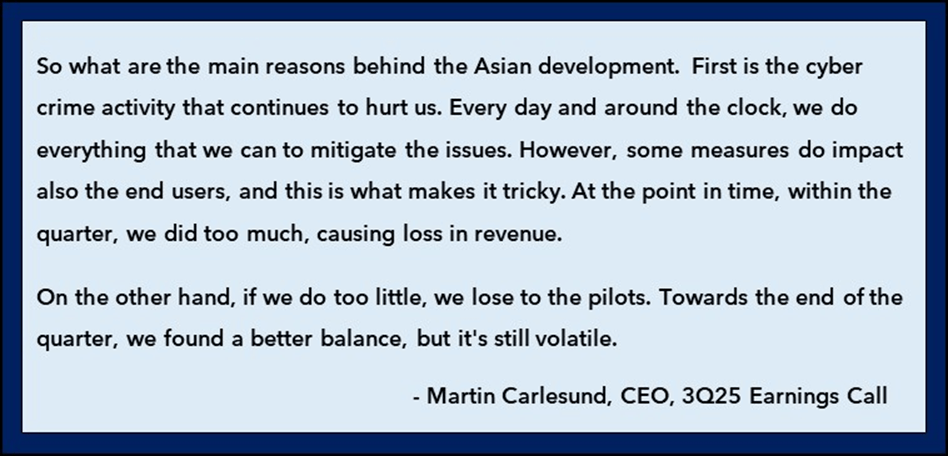

As Martin noted last quarter, “when we take measures, we take away a little bit of revenue that is good revenue and a little bit of revenue that is not—that is criminal or stealing”. This quarter Evolutions claims they were too aggressive with their measures which caused the larger than expected contraction.

Martin also noted that the Philippines is volatile as operators and players adapt to the new legal frameworks. He also mentioned India is potentially moving towards regulation, which creates more uncertainty. However, he didn’t try to quantify how much of Asia were these secondary issues versus the cyber-attacks.

Europe was -7% y/y. This wasn’t surprising as their ring-fencing efforts are expected to be a drag for a full year from when they started in 1Q25. They mentioned that one of the largest EU regulators called out Evolution as the best B2B supplier in this regard. In our view, the EU revenue contraction isn’t as worrisome as it is defined when it should end and is more clearly self-inflicted. It also is prudent for a better long-term relationship with EU regulators. The UK probe though hasn’t concluded and while Evolution seems to be very proactive to address their concerns, it isn’t clear if they may fine them or ask for even more restrictions. On a sequential basis the EU did grow slightly at +1% q/q.

North America growth was good at +15% y/y and LatAm growth improved a bit from last quarter to +6% y/y. The opening of the Brazil studio was called a success, and their Ice Fishing game was well received. As it is a faster paced game show, they now believe there is an opportunity in what they are calling the “speed game show arena”.

One piece of good news was that growth returned to RNG with 3Q25 +4% y/y, an improvement from +0% y/y last Q. They created a new RNG studio called Sneaky Slots from scratch. Because of One-Stop Shop, which is their direct integration to aggregators and operators, they can push new game titles to all of their customers without having to separate integrate new brands. This is a key advantage versus other suppliers who do not have the same direct integration and may have to convince individual operators why it is worth the effort of installing a new integration.

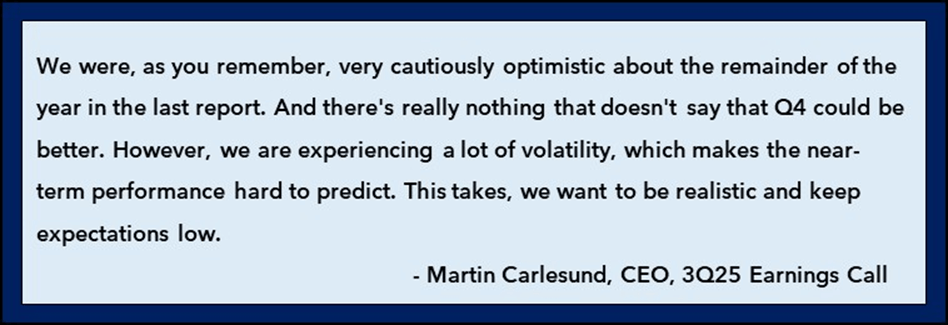

EBITDA margins were 66.4%, on the lower end of their 66-68% full year EBITDA margin guidance. However, profits or costs aren’t really the problem, it’s the revenue growth trend. By and large this was a disappointing quarter and management commentary didn’t give investors much confidence there would be a change anytime soon in Asia.

Business Commentary.

In just a couple years Evolution has gone from a strong growth stock to a deep value one where the question has moved from how long they can grow 20%+ to whether single digit growth is achievable. This has been reflected in the stock which is down almost 65% from its April 2021 peak. While many investors may have considered their 2021 valuation of ~60x earnings to be excessive, their current TTM multiple of 11x assumes significant business contractions continue. While we address how much growth is priced in today in our reverse DCF below, we don’t need complex math to see that the market is pessimistic on Evolution.

There is some reason to be so too. Issues with the Asia market have been on-going for nearly two years and there isn’t any line of sight as to when it could end. The improvement last quarter suggested that the worst was behind them, but 3Q was not only a regression, but the worst Asia revenue contraction they ever reported. On the other hand, their explanation—that they got too aggressive with security measures, which resulted in a loss of “good” revenue—is plausible.

However, they frame this as meaning that the revenue contraction was partially self-inflicted, but the other implication is that they cannot eliminate the stolen streams without causing collateral damage. There isn’t any reason to think that this won’t continue to be the case in the future. This balance is similar to a credit card company deciding how aggressive they should be with fraud prevention. If they are too aggressive, they risk losing legitimate transactions. If they aren’t aggressive enough, they risk allowing fraudulent transactions to go through.

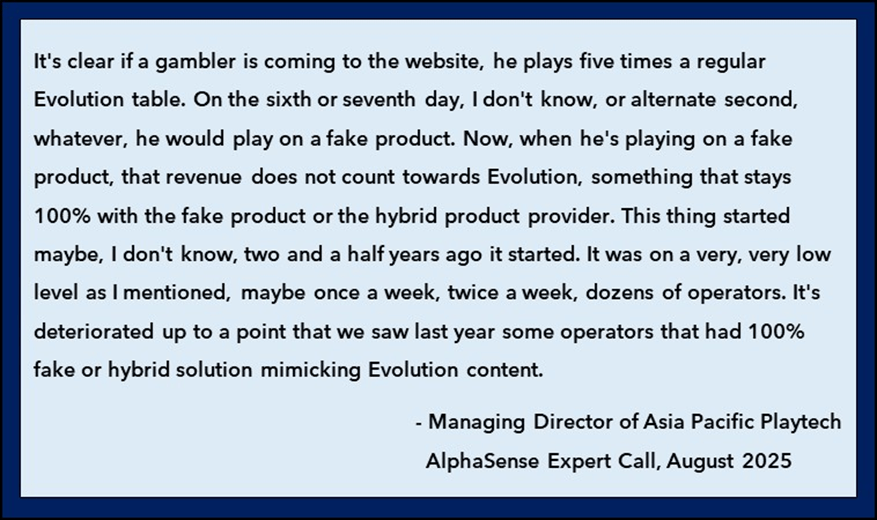

They are in a tricky situation because the illegality of gambling in most Asian countries means that there will not be any support from law enforcement. Additionally, as we noted in our last update that included AlphaSense expert call transcripts, it appears that it is their partners that are on occasion ripping them off in order to avoid paying commissions to Evolution. This puts them in a much stickier situation because one source is responsible for their good revenues, as well as stealing from them, making cutting them off completely a tough trade off. It makes sense why they are trying to find a technical solution to stop the stolen streams rather than just cut off bad actors completely.

The opaqueness of the Asian market as always been a risk. Evolution can honestly say that they are following the laws, but it still is true that most markets in Asia are black and any revenues derived from that geography often have some actor (usually the operator or player) breaking or bending the law. While this isn’t what is impacting Evolution directly, it is impacting them indirectly.

This is 1) because operators feel more brazen to steal from Evolution, knowing that law enforcement can’t defend them, and 2) since the operators are already breaking the law, they probably don’t have much to lose. However, despite the poor optics and unsavoriness, this doesn’t necessarily hurt Evolutions business. The operators who do not follow the law and get caught tend to disappear and reappear quickly. Evolution does not work with operators who operate illegally, but they sell games to aggregators who might. It is also possible for an operator to have a legal operation and an illegal operation. (It is common for operators to operate under international licenses and players to VPN in).

In an AlphaSense expert call interview, a Playtech Managing Director in Asia, noted that perhaps 60-70% of all of Asia revenue comes from Korea. While it is unclear how he would know this (especially since a lot of gaming revenue in Asia is unregulated), we have heard from other AlphaSense expert calls that Korea is one of their largest markets next to Japan.

Similar to as we described above, an operator will get the game from a supplier who resells it. In some cases, it sounds like there can be several layers of resellers that each mark the game up. As we mentioned, the customer is also often the one who is ripping off Evolution’s feeds. This makes cutting them off exponentially more complicated as commission-generating revenue is comingled with stolen revenues. In this context it makes sense that they could have been too aggressive cutting off stolen feeds not realizing the impact it would have on “good” revenues from that same customer.

The other aspect of this is the leverage it leaves with the operator since Evolution cannot full cut them off without self-inflicting harm to themselves. Furthermore though, this expert alleged that Pragmatic had aggressively...

If you are a Speedwell Member, please click here to read the rest of this post.

Become a Speedwell Member to read the rest of this post and get access to all of our other research, including our 74-page Evolution Research Report.

For further reading, check out our Evolution Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Evolution (Apple, Spotify).

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Evolution report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered APi Global, Airbnb, Axon, Casey’s, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in Evolution. Furthermore, accounts one or more contributors advise on may also have a position in Evolution. This may change without notice.