Evolution: 4Q25 Business Update

The Slog Continues, 9.5x P/E Multiple

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members can access a full version of this post here and a PDF of this post here)

4Q25 Update.

Evolution reported 4Q earnings and the stock dropped -6%.

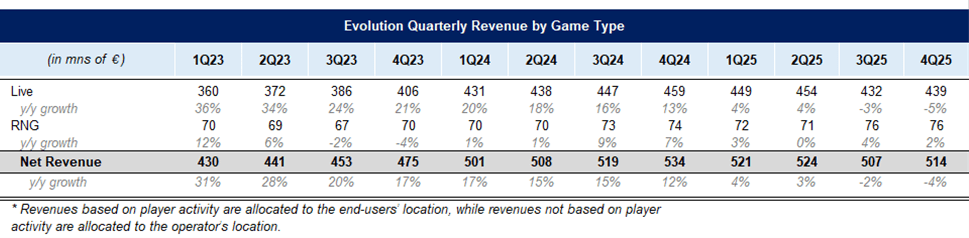

Revenues shrunk -4% y/y, but grew q/q +1.4%. On a constant currency basis, revenues were +4.9%.

Live revenues were -5%, marking the second consecutive quarter of contraction, driven by on-going Asia and EU weakness. RNG was +2%, which is down from the high single digit growth they briefly experienced in 2024 (and have been trying to get back to since). Again though, forex was a material headwind in the quarter.

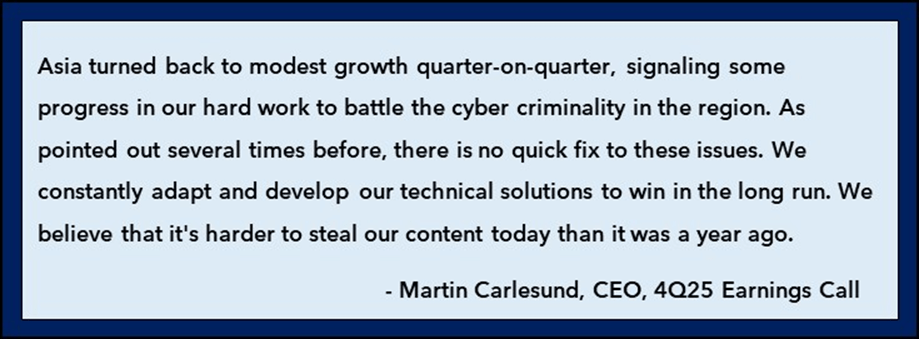

They made some progress on the Asia cyber situation, but it still is hampering their results and there is no clear timeline when that will reverse. Rather CEO Martin Carlesund frames it as a long and slow battle where they have to continue to adapt to win.

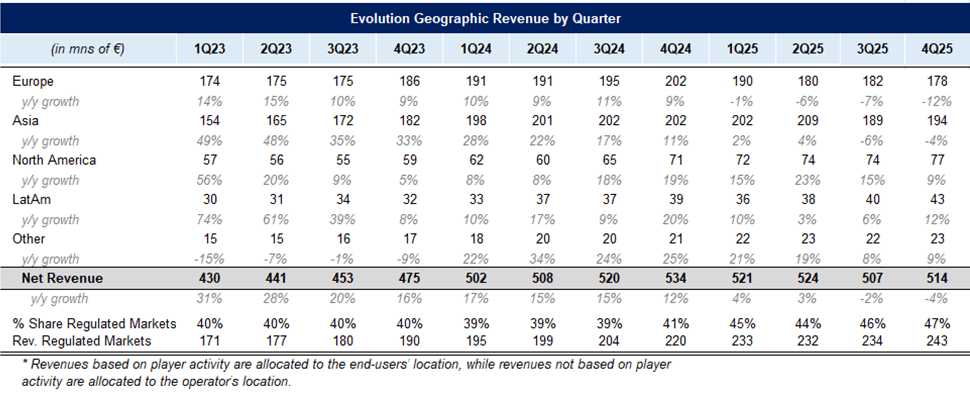

The mildly positive development in Asia was offset by Europe losing regulated market share. As a reminder, Evolution has “ring-fenced” their EU operations which makes it harder for unlicensed operators to offer their games. While on the one hand this greatly ensures compliance with local laws and regulations, it also means that unregulated sites (which haven’t been clamped down on) are simply offering competitors games.

On the call they talked about further “channelization”, which means more players are playing in unregulated markets rather than through regulated sites. This can be because regulated sites have to follow rules like monthly deposit limits that restrict how much a player can bet. The odds can also be better because these operators often skirt gambling taxes. The more onerous the taxes and regulations become, the more players would rather play illegally. This can be solved by either lightening up the restrictions that are pushing players away from regulated markets, or by increased enforcement of unregulated operators. The latter (as we know from Asia) is far harder though.

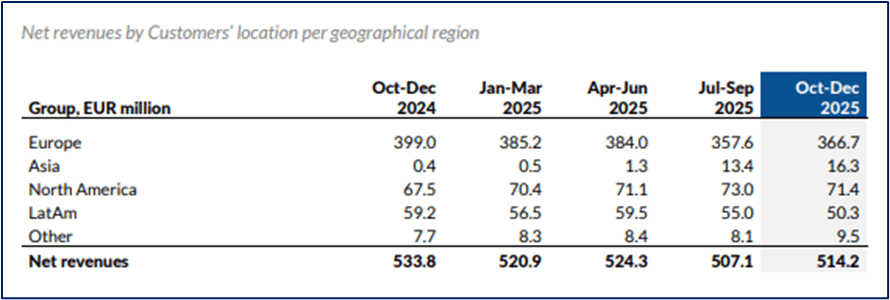

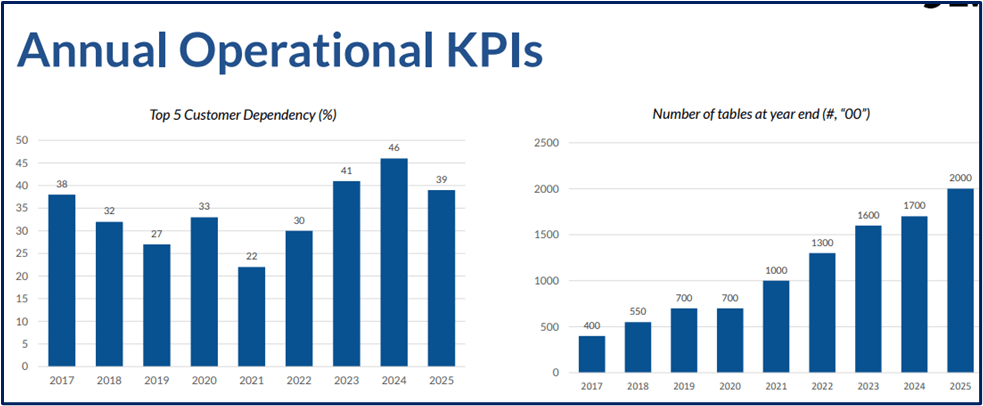

They also disclosed a new table that shows geographic breakdown by customer’s location (instead of the players). This, unsurprisingly, shows that despite 37% of revenues coming from players with Asian IP addresses, only 3% of customers are officially based in Asia (many used licenses for Malta).

Given the headwinds in Europe and Asia, it is no surprise that Evolution emphasized investing in the United States and South America more. The U.S. grew +9% y/y and Latin America was +12% y/y. They noted that one of their main Live competitors in Argentina decided to shutdown their operations.

Operating margins were 58.2% for the quarter, down 290bps y/y and 30bps sequentially. Despite the growth in expenses (+4% y/y), they noted on the call that they are starting to see the benefits of their focus on operational efficiency: “we are beginning to see the benefits of our initiatives to drive operational efficiency. Several initiatives are ongoing when it comes to optimization of our tables and studios as well as the way we work with our supporting functions”

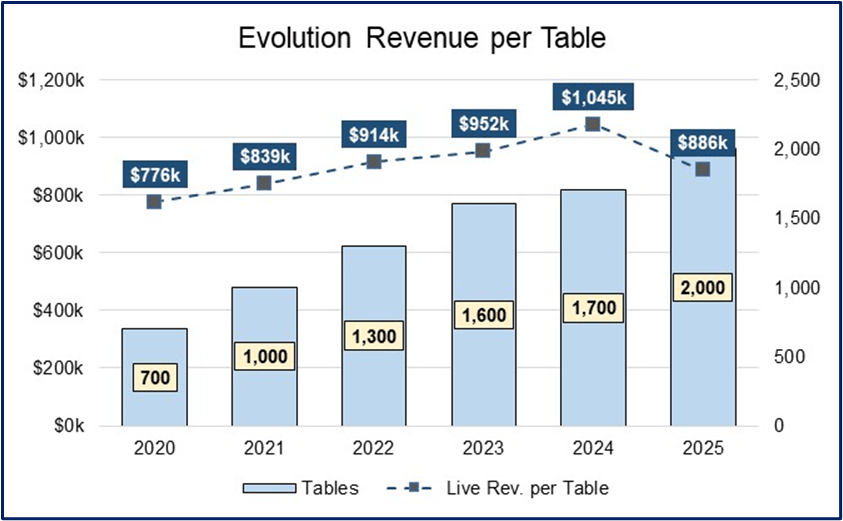

They also disclosed a new chart that shows total tables.

Below we can see that in the last year revenue per table has fallen after consistent gains since 2020. However, they increased their table count 300 or 17% last year. If we hold the table count steady, the revenue per table would be down -8% (instead of the 15% shown below). This can largely be attributed to the weakness in Asia and Europe.

On the other hand, it does support the claims that they have been making operational efficiency improvements because operating profits for 2025 are -5% versus a much larger drop in revenue per table.

They have not announced a new capital allocation plan yet, but will during the AGM in a couple weeks. They emphasized that between dividends and buybacks, investors received a 9% shareholder yield. Their dividend yield alone stands over 5% now.

Total EPS was €5.24, down from last year’s €5.94. Although a higher tax rate in 2025 explains a good portion of the reduction. At the ADR’s current price of $60 a share, that puts them at 9.5x earnings (after converting the EPS to USD).

Business Commentary.

Big picture this quarter was mixed. Currency headwinds turned a 5% growth quarter into a revenue contracting quarter. Asia was better than feared as last quarter it seemed another revenue contraction wasn’t off the table. However, the tussle between Evolution and the cyber criminals will continue to go on with no clear end in sight.

The EU developments are negative as regulation is pushing more players to play illegally. This is not something that seems like to reverse soon, but unlike the Asia situation, there could be a change to policy which quickly reverses this situation. Whether EU regulators have a desire to is another matter. But in theory if regulators are concerned about protecting players, by them being too draconian with regulations, they are pushing the most vulnerable players out to illegal markets and also helping aid a slew of other criminal activity that tends to come along side illegal gaming.

On the other hand, our fear is that regulators tend to be too idealist and may not be willing to fully accept how their well-intended policies are actually causing net harm. It is important to keep in mind that many of these countries tax gaming and if gaming revenues drop too much, that could be a trigger to reconsider policies. At the very least this will be a head wind for the next 2 quarters as they lap their EU ring-fencing efforts (but possibly longer as players won’t shift back to regulated gaming until a policy shift is enacted).

Outside of that, The United States and Latin America continue to be bright spots. Competition is also not really a factor—the only time a competitor in live casino is really winning is because they are able to offer games illegally (which comes with benefits like better odds from skirting taxes and no player deposit limits).

While few investors would have been happy owning the stock a year ago had they known Evolution would start losing revenues, at this point they now trade at 9.5x earnings. This is a multiple typically granted to companies that are thought to have no growth prospects and possibly are at risk of indefinitely shrinking revenues—a melting ice cube in other words.

Most of their earnings are now being paid out to investors in the form of stock buybacks or dividends. Any growth they do have requires relatively de minimis capex. The key question investors are faced with now is whether they think the Asia situation is likely to get worse from here or if the EU shift to unregulated gaming will continue indefinitely. Because absent of that, an investor can argue a lot of negativity is already priced in.

Below we show our reverse DCF so investors can see exactly what is priced in and the associated returns under different scenarios.

If you are a Speedwell Member, please click here to read the rest of this post.

Become a Speedwell Member to read the rest of this post and get access to all of our other research, including our 74-page Evolution Research Report.

For further reading, check out our Evolution Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Evolution (Apple, Spotify).

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Evolution report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered APi Global, Airbnb, Axon, Casey’s, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Ferrari, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, Shift4, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in Evolution. Furthermore, accounts one or more contributors advise on may also have a position in Evolution. This may change without notice.