Floor & Decor 2Q23 Earnings Recap

Speedwell Research: Business Updates

We are going to periodically share updates on companies we have covered in the past here. These will sometimes show up as Twitter threads first, but we want readers to be able to easily access the archive of earnings recaps. The start here tab allows for easy navigation. We may occasionally refine or expand our analysis based on feedback.

This week, we’re covering Floor & Decor. We last covered their 2022 earnings. Previously, we’ve covered Meta, Coupang, RH and Constellation Software.

Floor & Decor 2Q23 Earnings Recap

Floor & Decor reported 2Q23. Results might look weak, but in the context of the macro backdrop they are fine and management continues to execute on their 500 store plan.

Total sales were +4.2% y/y at $1.14bn, but same store sales (SSS) were -6%. (Last quarter they disclosed 2Q QTD sales were -6.2%)

Comparable store transactions were -7.1% y/y, which is an improvement from -9.9% last Q and -10.4% in 4Q, however, fewer transactions were the main driver in the lagging SSS figures. They attribute this largely due to weak home sale activity and a pressured consumer who has shrunk average project size. They also noted that higher interest rates impact the affordability of financing.

Average ticket increased just +1.1% y/y, a stark deceleration from +7.3% last Q and they expect it to continue to be pressured in the back half of 23. This is partly due to their decision to decrease prices on select SKUs, rebating cost savings back to consumers after having to raise pricing from 21-22 supply chain issues, but also because of the factors mentioned above.

While pricing may have dropped though, they are offsetting that with lower COGS. Gross margins expanded 220bps y/y to 42.2% from 40% in 2Q22 or up +40bps sequentially. They noted that they expected gross margins to continue to expand throughout the year and that they have the ability to exceed their historical gross margin rate. (Gross margins peaked in 2020 at 42.7%).

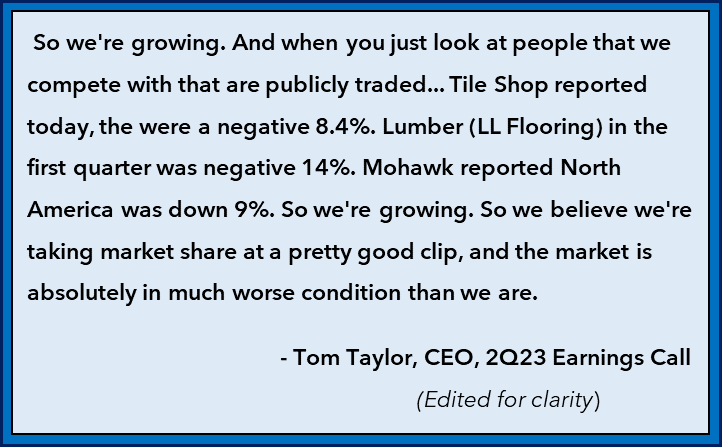

With price changes and a tough macro backdrop, they spoke about their confidence in their value prop and expectation that they will gain market share. CEO Tom Taylor called out competitors on the call, noting they were shrinking as FND was growing. Their net store adds and ramp up of new stores more than offsetting the negative SSS headwind.

With 9 new warehouse stores this quarter (now at 203 total) and sales from other new stores that are still ramping up (it takes ~3 years for a store to be considered “mature”), analysts questioned whether the new store additions were hiding weakness in their mature stores, implying mature store productivity could ultimately be less than assumed.

Mgmt disclosed that mature stores were indeed performing a bit worse, about ~200bps worse than the total SSS figure, but CFO Brian Langely addressed the real concern upfront: “there’s no reason they wouldn’t earn back to where they were. We don’t believe they overachieved their long-term goals”.

Pros account for 43% of sales, up +90bps sequentially and over 80% of pros are in their membership loyalty program. The strategy of going after Pros is working well and they continue to roll out more services for Pros including workshops and CRM which helps increase sales and loyalty.

They also noted Spartan (commercial) grew +40% y/y and RAMs (Regional Account Managers) grew +39% y/y.

2Q operating income was $190mn -4.9% y/y with operating margin of 8.4% compressing 110bps y/y. This is attributed to occupancy deleveraging as they ramp up new stores, as well as the lower store productivity. They also noted that a decline in inventory and other working capital initiatives improved working capital by ~$250mn.

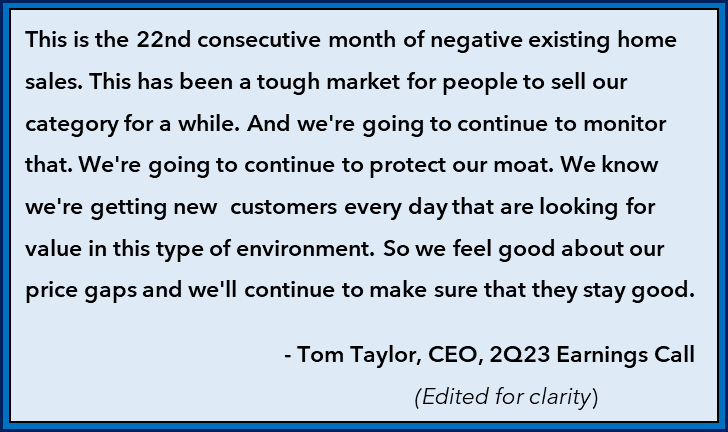

Throughout the call they emphasized the tough macro environment, particularly the weak home sales figures which they expect to be 4.1mn to 4.3mn for the full year (600k lower than prior assumed). This is the lowest since the financial crisis. However, they coupled this commentary with a confidence in their offerings vs competitors and belief that Floor & Decor will be a market share gainer.

Nevertheless, they were too optimistic in 1Q and lowered their sales guidance $150-220mn to $4.61- 4.75bn driven by lower SSS expectations of -7% to -5.5% from prior guidance of -3% to flat. The new guidance now represents +8-11% y/y sales growth for the full year.

In summary, this is a tough environment to be a specialty hard surface flooring realtor. They sell a product that can be deferred for some period of time, with one of the largest key sales triggers–home sales– near a multi-decade low. However, floors will still wear out and when they do, consumers will still want the best quality product for the least money. Pro’s will continue to value the in-stock inventory and wide selection that is critical to allowing them to finish a job in the same day. Floor & Decor’s value still stands.

A great company is like a well built ship. Any ship that ventures on a long journey will hit a storm that will slow it down or blow it off course. The value in a great ship isn’t its ability to avoid storms, but rather endure them.

Floor & Decor continues to focus on reaching their 500 warehouse store target and is gaining market share through this macro calamity, while improving their consumer & pro value props, and spinning up tangential opportunities like commercial sales. With 500 stores earning the ~$30mn that a mature store does, that is $15bn in sales. With operating leverage expanding mature margins to ~15%, that is ~$1.75bn in owner earnings after tax. Today’s market cap is $11.1bn.

If you enjoyed this post please like and share so we know to produce more content like it. Also follow our new podcast, The Synopsis (Spotify Here, Apple Here), where we will cover $FND in the future. Our second episode, which covers $RH, will be released this Sunday.

For the full >50 page $FND report, become a Speedwell Member today where you will also get access to our $CSU, $CPRT, $RH, $META, $WD reports, among others.

If you liked this post, please share it so we know to post more content like this. Follow us on Twitter @Speedwell_LLC or Threads @Speedwell_Research for more business and investing content!

Good work, thanks for sharing Speedwell!

Thank you.

I appreciate reading the FND material awhile ago and listening to the podcast (just yesterday).

I am not sure, I may be wrong, but I think the incentives topic is missing. You discuss a little bit about

Thomas Taylor but I don't think I read or heard anything about the incentives.

1. Management quality assessment

2. Management (NEOs) incentives

3. Insider ownership

4. Other NEOs things if relevant