Google Shut the Door on Competition, AI Swung it Back Open

Assessing Risks to Google's Business Model and How AI Imapcts the Competitive Landscape

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

There is a podcast of this memo available if you prefer listening to it. You can find it on our podcast feed here (Apple, Spotify).

Intro.

This is paraphrased from the Graham & Dodd Annual Breakfast 2022 with guest speaker Todd Combs:

“[Todd] Combs recalled the first question Charlie Munger ever asked him was what percentage of S&P 500 businesses would be a “better business” in five years. Combs believed that it was less than 5% of S&P businesses, whereas Munger stated that it was less than 2%. You can have a great business, but it doesn’t mean it will be better in five years. The rate of change in the world is significant, which makes this exercise difficult, but this is something that Charlie, Warren and Todd think about.”

Monetization Contention.

In 2010 Google announced “Google Instant”, which populated search results as you typed. This allowed a user to get to the Google search result page quicker, but it also had a secondary impact. It essentially rendered the “I’m Feeling Lucky” button useless. The “I’m Feeling Lucky” button was an ode to the beginnings of Google, capturing the founders’ quirky sentiments while also showcasing that their search results were so good that you could click that button and satisfactorily be sent to the first search result.

Now though, these changes would mean more friction to using this button. And for Google, that was a good thing.

As estimated in this 2010 Business Insider article, that button was costing Google over $100mn a year. This is because any time a user clicked it, they didn’t end up on Google’s Search Engine Result Page. The obviation of the Search Result Page meant a lost opportunity to show ads. Clicking the “I’m Feeling Lucky Button” shown above would have eliminated the opportunity for Google to show the four ads below.

The idea that this runs counter to Google’s ad-driven business model isn’t new; Ben Thompson wrote about it in 2016 and again more recently. From his 2016 Article:

Google has a business-model problem: the “I’m Feeling Lucky Button” guaranteed that the search in question would not make Google any money. After all, if a user doesn’t have to choose from search results, said user also doesn’t have the opportunity to click an ad, thus choosing the winner of the competition Google created between its advertisers for user attention. Google Assistant has the exact same problem: where do the ads go? – Ben Thompson, Google and the Limits of Strategy

The problem isn’t just that it eliminates the chance to show ads, it’s also that Google cannot rank results based off who pays them the most. Many people who ritually skip past the sponsored links know the organic search results are more likely to be a higher quality result. But whether you click the sponsored links or not, the reality is millions of people do every day, and it is over half of their revenue and a much larger portion of profits1. Thus, any impairment to Google’s ability to show these sponsored search links will be material to Alphabet’s total profits. Despite Alphabet having a sprawling tech conglomerate with Android, YouTube, Google Cloud Services, the Google Play Store, DoubleClick, Waymo, Nest, Waze, and Fitbit, among others, none of these adequately diversify them away from search. Now this could change in the future, but Google doesn’t have an AWS—their success is still predicated on the Search business.

An investor would want to have reasonable certainty that they know what the business will look like a decade from now. Or more technically, have high confidence in the lower range of their cash flow estimates for the future periods that constitute a majority of Alphabet’s value.

This is all to say, we see three risks to Google that makes estimating future cash flows with a high degree of confidence particularly hard.

Competition.

Competitor products like Bing, Yahoo Search, and more recently DuckDuckGo have been desperately trying to gain market share for some time, but with very limited success. Aside from other direct search competitors, there also was a fear that with mobile phones more search would go directly to apps. This so-called vertical search threat, i.e., going directly to Yelp for restaurants or Expedia for hotels versus starting at Google, was sparked by the mobile app revolution. The mobile phone created a new opportunity for mobile apps, and should users have started their search at a specific app versus the browser, then Google would lose that query.

While this fear never materialized, it was quite plausible, after all China’s “Google”, Baidu, never reached the same level of prominence as Google in the US in large part because mobile gained broad penetration before PCs. Google did its part as well to fend off vertical search threats with a variety of vertical specific experiences like Google Hotels, Google Flights, Google Finance, and pulling in local reviews from Yelp.

Though, even today the risk of search moving from the browser to apps is ever-present. The new risk from apps isn’t them competing on “Verticals”, but rather format. Tiktok and Instagram are new venues to search for a variety of products, with a particular strength in cosmetics, beauty, and apparel. This New York Times article from 2022 quotes a Google Senior VP:

“In our studies, something like almost 40 percent of young people, when they’re looking for a place for lunch, they don’t go to Google Maps or Search. They go to TikTok or Instagram”

Google owns YouTube and pushes short clips from videos at the top of search when relevant, but once they are no longer top of mind with a user for a use case, it is hard to win them back. This still though is just a new form of an older threat: Google originally acquired YouTube because they feared people could search on the platform instead of Google.

However, in all of these cases, Google is still competing on conventional vectors. There are two ways Google has generally competed. The first is getting the users to decide to search on a browser instead of a specific app. If a user does choose an app, they hope it’s YouTube. The second is fighting to make their search engine the default on the browser. They created Chrome and Android just to make Google Search the default, and when that isn’t enough, they’ll pay billions of dollars to get the default position. Despite all of the alternatives to search, this one-two punch has enabled Google to maintain their search dominance.

But what happens when the decision is no longer just between a browser and specific app? Could an AI agent be a third option in the future? Then, even if they do win and users use Google, will Search monetize as well if the format changes? Will the partners they pay billions to ensure default position with feel they must more deeply integrate AI into their products in a way that ends up encroaching on Google Search?

Three Threats.

We will break all of these risks up into three sections:

Product Encroachment. This is the product’s functionality moving to partners or competitors.

Form Function Changes. This is how the product is used changing.

AI changes Competitive Landscape. This risk is twofold: it could be AI itself becomes a risk to Google, or simply AI allows other companies the opportunity to go after Google in a way they previously couldn’t have. Either way, it is AI changing the search landscape that has been fairly settled for the past two decades. Whether AI is a platform shift or just a product enabler, AI opens the door for more competition.

While the threat of partner encroachment and changing form function has existed for some time, we see AI as the potential catalysts that disrupts the stable competitive dynamic Google’s enjoyed. You may think of the first two risks—product encroachment and changing form functions—as kindling. Every year there isn’t a fire, the kindle keeps piling up and getting drier. AI is like a heat wave: it’s not impossible, but it seems unlikely something doesn’t catch fire. And similarly, once a fire is lit, it tends to spread everywhere.

Threat One: Partner Encroachment.

As noted, Google’s supremacy is in no small part due to maintaining optimal product positioning on web browsers and mobile phones. The so-called TAC, or traffic acquisition costs, ensured Apple would make them the default search engine in Safari. And their ownership of Android usually allows them to stipulate them making their Chrome browser the default (which in turn uses Google Search). Or if not, like in the case of Samsung’s pre-installed internet browser, Google pays them to make Google Search the default. However, their success here wasn’t just because of large revenue share agreements (36% in the case of Apple), but also because it was a business their partners didn’t have a strategic reason for owning.

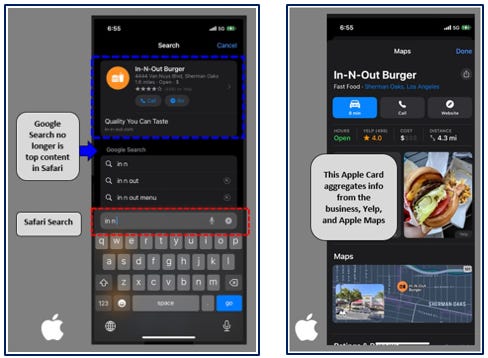

Apple has been terrorizing Google with “Spotlight” searches that show up in the safari search box for over a decade. The slide below is a 2014 internal email that was released as part of Google’s anti-trust case. The slide bluntly labeled “It’s bad” notes that Safari suggestions in search are siphoning queries away from Google. While Apple does this ostensibly to improve their user experience by directing them to their desired web pages quicker, it also gives Apple a small space to experiment with search, with the added bonus of reminding Google who has the leverage in their relationship.

Apple, though, is very aligned with Google today. Google pays them an estimated $18-20bn annually, which is a good portion of Apple’s ~$85bn in service revenues. And, owing to the virtually 100% margin on these payments, could be as much as ~18% of Apple’s EBIT. (For Google’s part, their 36% revenue share with Apple implies they make around $55bn gross from Apple mobile users. They could theoretically net out some costs of serving those users even though it is a “revenue share” agreement. With some assumptions, we estimate this at 30-40% of Alphabets total earnings).

Their alignment is supported by the fact that Apple is both making enough money from Google, but also, and critical to our point, has no strategic reason to enter search. Nevertheless though, Apple has continued and expanded the places its search results come up. The small search bar on the home screen will search your entire phone and the web for you. Apple Maps Search shows up in Safari if you look for something with a physical location. You can search for local services in Apple Maps and it pulls in Yelp results. This is all in addition to more accurate suggestions that come before a user clicks the Google Search results in safari. While it may be against Apple’s financial interest today to subvert Google, this could change in the future.

Below we see examples of Apple Search suggestions popping up instead of the Google result.

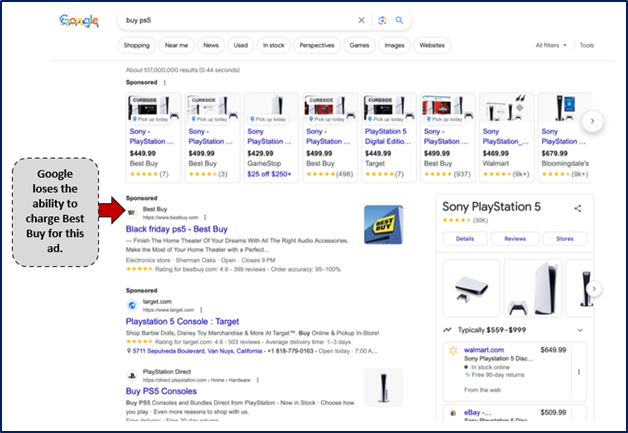

On Safari on desktop, it is similar. Below we see when in the middle of a search to buy movie tickets it suggests Fandango when we only write “buy movie”. (Effectively mirroring the original issue with the I’m Feeling Lucky Button). And in the search below for “buy PS5”, it recommends Best Buy.

Had that search been completed in Google, though, the user would have seen a Best Buy sponsored link at the top.

Exactly why Apple does this is a little unclear as it hurts them financially just like Google. We can’t help but wonder if this is their way to slowly prepare for the possibility of search without a Google deal. It’s Apple’s ethos to put user experience over all else, but if you add the risk involved in building out a full search product plus the advertising apparatus that would be required to make it profitable, then it makes little sense for Apple to feasibly want to enter the search business, and that is before considering how their privacy friendly imaged could become marred.

However, search today is a very isolated experience, relegated to a single app. A user clicks into the browser, searches, gets a bunch of links, and then clicks one. There is no reason to think this is end product of optimal user experience, and as OpenAI’s ChatGPT and Google’s Bard are showing us, they potential ways to search are broader than we have previously envisioned. Apple’s focus on user experience may one day result in them in housing or at least taking more control over search on their devices.

This leads us to our second threat.

Threat Two: Changing Form Function

The first threat, encroachment, seems more like a latent risk. One that would stay unrealized, unless another piece moved. On a long enough timescale, changing form function seems imminent though.

Voice search has been a threat for a while, and is partly why Google built out their hardware division, but after some short-lived fanfare, it generally has been underwhelming both to users and as a business. Similarly, Siri, as most of the other AI assistants, has been as much of a nuisance as a help. But the technology will continue to improve, and a future AI assistant might not just be helpful, but become a main way we interact with our hardware.

It’s not just coincidence that when we think about the future of computing our minds tend to cluster around a super smart AI we can talk to, whether it is the more dystopian HAL from 2001: Space Odyssey or the more friendly Jarvis from Iron Man; interacting with technology in such a way seems natural—provided the technology can allow for a natural experience. These aren’t unfounded speculations on how AI can change the form factor of technology—Amazon’s Alexa, Google’s Assistant, and Apple’s Siri are all manifestations of the impulse to interact with a super smart AI. You can buy a pair of Meta’s Smart Glasses today and speak to them. In this Reel, Mark Zuckerberg asks Meta AI how to tie a braid. While no doubt the current capabilities leave much to be desired, the risk of users going somewhere other than the browser when they want to search is increasingly materializing.

Beyond an AI agent though, even “traditional search” on the browser could change. Search today is really a narrowing of options with the user making the decision on which website to pick. AI can allow for new ways to “Search” that no longer require a user to pick, but rather decides for the user. Putting the onus on AI to pick, instead of the user, breaks most of Google’s business model.

Right now when you search, you get a long list of links with the top links paid for by advertisers. Scrolling past the sponsored links may be a bit annoying, but no one is bothered that much. This arrangement has allowed users to get a free service, advertisers to find customers, and Google to make money—a win-win-win. This all breaks though when search moves from picking from a narrow list of suggestions, to being given a singular answer.

When a user clicks a link, they are internally weighing a variety of different variables to come to a snap judgement on which site to visit. The few links on the top of the Google Search results page are the most convenient to click and thus many who weigh convenience will click those, despite being sponsored. Other users are habituated to scrolling right past the sponsored links, knowing that the organic results are likely to be better.

As it stands today, the weighing of variables is partly done by Google, who decides what links surface, and partly by the user, who decides which link to click. However, with Bard or ChatGPT, the weighing of variables is done entirely by the AI. Unless we as society become comfortable with the dystopian idea of a “sponsored weighting”, that is, an advertiser paying to have their product or brand mentioned in results more often, then the answer from AI will never have a commercial potential. Ask the AI for the best running shoe and it may give you a few options, but it seems at odds with the purpose of asking for AI assistant in the first place if it gives you back a “sponsored shoe”. And we can imagine users wouldn’t trust an AI that regularly recommended products it was paid to recommend.2 Google though doesn’t need to show a “sponsored shoe” to still have an opportunity to monetize.

Below is part of the results when asking Bard “what is the best shoe for running?”. We see that it didn’t give one answer, but rather structured the answer around different shoe types. With such an answer you could easily put ecommerce sites that have the shoes available below.

They do this currently with their experimental search on Google:

While these results are pretty messy and do not have the explanation that Bard provides, it gives an idea of how the product could blend being helpful with commercial potential.

In short, any opportunity for AI to put decision-making back into the hands of the user opens up the opportunity to monetize. The problem really comes down to whether or not most users will want the AI to make the decision for them. If search winds up in this sort of middle ground, with a mix of AI generated content and AI assistance in search, but still with ample opportunity to showcase multiple options on commercial queries, then Google could turn out fine.

However, this all still assumes the user thinks “Google” before asking the question. While it doesn’t have to be AI, AI does present an opportunity for competitors or partners to build new products that do the functions we traditionally use Google for, while being early in the “user search journey”.

This brings us to the final risk, and the potential tinder that catalyzes the other two risks.

Threat Three: AI opens new doors.

AI is a risk that could bring on more product encroachment as well as form function changes, while potentially opening the door for a whole new set of competition. Rather than just speculate on the future, let us look at the past.

When Facebook IPO’ed in 2012, many investors thought that the mobile phone would bring the death of their advertising business. Investors were concerned about the advertising surface space shrinking from a large desktop monitor to a tiny mobile phone screen. Thus, Facebook would lose the 5-7 block of desktop ads they had and would have to make do with just a single ad on a smaller screen, or perhaps just a mobile banner ad.

Investors weren’t exactly wrong though—ad impressions did absolutely plummet during the shift to mobile, as much as -65% in a single quarter (4Q14), on a comp which itself was negative.

From our Meta Report:

Starting with the shift to mobile, ad impressions started to plummet as they traded a right-hand column of 5-7 ads for fewer ads in the mobile newsfeed. However, as Facebook learned, these newsfeed ads were more engaging and enjoyed higher click-through rates (CTR). The higher click-through rates supported higher ad pricing, as advertisers increased their bids until they hit their ROAS [Return on Ad Spend] limit.

Essentially, it was true that mobile meant fewer ad impressions, but it didn’t matter since the ads that were shown could be more engaging and perform better. It turned out that people didn’t mind that much if an ad took up almost the entirety of their phone, as long as they could scroll past it if they didn’t like it. Additionally, since people always had their phones on them, time spent on Facebook increased.

In some sense, Meta got lucky that the new form factor of consuming social media was actually an advantage to an advertising business instead of inhibitor. The ad impression contraction they experienced didn’t matter since the ads that were shown were getting a higher price. They were able to transition their service to a new platform, while simultaneously increasing the monetization potential of the service. This was far from a given.

Look no further than their other budding business at the time, “Facebook Platform”, which was home to tens of thousands of 3rd party apps. In 2012, 16% of revenues came from users spending on games, virtual items, and other digital goods, a figure which they expected to increase to 30% of revenue. Instead, though, the mobile phone essentially brought on the collapse of this business. This is key to understanding Zuckerberg’s Metaverse ambitions.

In a leaked 2015 email, Zuckerberg wrote: “our vision is the VR/ AR will be the next major computing platform after mobile”. Whether that turns out to be true or not, it was the impetus for the Oculus acquisition and the tens of billions in Reality Labs losses. We can be coy about the “Metaverse” and say Zuckerburg is foolishly allocating capital, but his perspective is that the mobile platform shift nearly killed Facebook. Instagram, Snapchat, and WhatsApp were only made possible by the phone, and he fears a platform shift provides a similar window for new competitors to assert themselves.

Whether VR/AR is a platform shift is beyond the scope of this memo—the point we are drawing is that dominant businesses are at risk when they have to reorient their organization to new ways of serving users or customers.3 Meta in some sense was lucky that they not only survived the platform shift from desktop to mobile, but actually had a better business at the other end.

Now, whether AI is technically a new platform or just an enabler for existing platforms4 is an open question. AI could potentially turn into a platform the same way the internet is, with open models to build off of and a presence on virtually every device. Or it could just be feature enhancer for devices and products, which could be great for Google as they lean on AI to improve advertising clickthrough rates and generative AI to create more compelling ads. Frankly, exactly how AI changes things is a little hazy, but that is part of our point—the distribution of outcomes has widened.

Alphabet also owns Android and 15 products with over 500mn users each, including the most popular web browser Chrome. They also have a very formidable AI research department, including Deep Mind. But it’s important to remember that if you are valuing them off of real cash flows generated by businesses they operate today, search is by far the most important.

And on that note, it is becoming increasingly clear that Google’s Search product will have to endure changes to stay relevant in the future. The exact changes Google will need to make are unknown and speculative, and whether they leave Google as a worse business is also unclear. Perhaps they get lucky like Facebook was and AI means they have a stronger and more dominant business. Or perhaps it loosens their grip on the search market, while simultaneously making traditional search a lower monetizing business.

In the future, Apple may feel that AI will be key to their future products and so they could incorporate it deeply into their devices with an AI agent that all but obliviates the need to open search in a web browser. OpenAI showed how they could use AI to make a pretty strong search product that quickly garnered over >100mn weekly active users. AI even did the unfathomable—it got people thinking of Microsoft’s Bing as more innovative than Google. While this was short lived, it shows how much AI can mix up the competitive landscape. And this is arguably just the beginning.

Conclusion.

Our point isn’t that we have any idea how this all shakes out, but rather that we do not have any idea how this all shakes out. A conservative investor would want to be able to get a reasonable return without making Herculean assumptions about Google’s ability to navigate the changes in competitive dynamics. The problem is that as the future becomes more uncertain, it is not just harder to weigh the likelihood of different outcomes, but even to be able to see what they are.

Of course, nothing is going to change tomorrow, and many of these risks have existed in some form for years. So, we will put the question to you: Is Google going to be a better business in five years from now? How about ten?

We will be releasing a new memo every Friday morning. Subscribe below to receive it!

Also check out our podcast, The Synopsis, here: Apple, Spotify

They group search revenues in with advertising revenues from Gmail, Maps, and Google Play. Search EBIT is rolled up into “Google Services” and isn’t broken out separately. But it is higher margin than their ad network business, where they don’t own the web property, and YouTube, which has a structurally lower margin from paying out ~55% of revenues to creators. Their other segments, Cloud and Other Bets, are barely profitable and loss making, respectively.

The difference between this and search today is that people click the top search results because they are the most convenient. Thus, convenience is what Google is selling: they aren’t explicitly lying to you with product recommendations they know to be sub-optimal.

The mobile platform shift even opened up competition against Windows OS, which had near totally dominance of PC operating systems. ChromeBooks, which is Linux-based, likely wouldn’t exist unless they could lean on the Android app ecosystem, which required Android to gain broad prominence. Platform shifts are so impactful that they can even present a risk to a dominant company on a legacy platform.

Exactly what constitutes a “platform” is up for debate, but to Bill Gates defined (paraphrased) a platform as a system where the sum of all economic value created by it is greater than the economic value of the company itself.

Disclaimer: At the time of this writing, one or more contributors to this report has a position in Google. Furthermore, accounts one or more contributors advise on may also have a position in Google. This may change without notice. See our full disclaimers here.