LVMH: 4Q25 Business Recap

2025 Profits Contract -9%

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(As a reminder, this is a business recap, which is shorter than our business updates. We usually only post recaps to SpeedwellResearch.com to avoid spamming you, but thought there could be broader interest).

4Q25 Update.

LVMH reported full year 2025 results, which were lackluster, but in line with prior management communications.

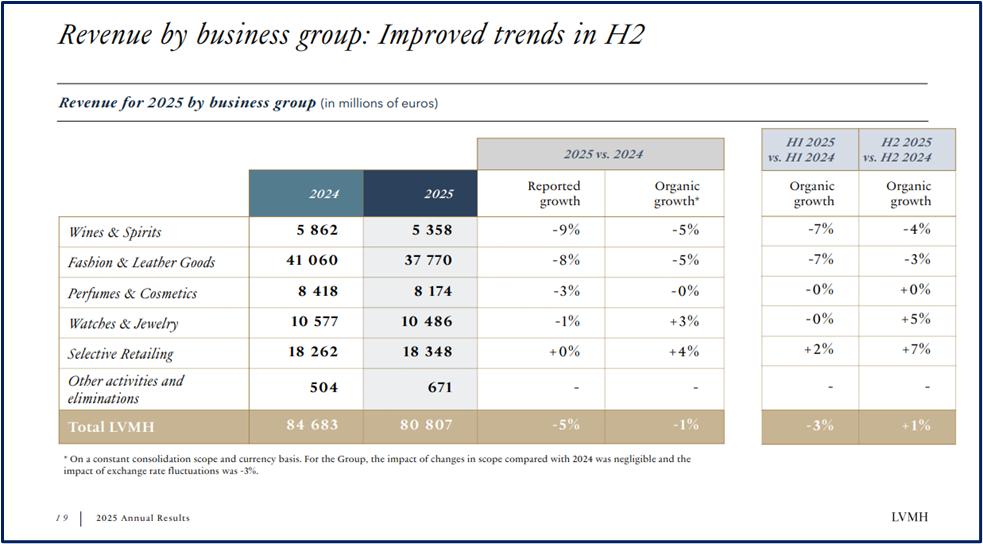

Revenues contracted -5% for the year, or about -1% on an organic growth basis. Currency was a negative -4% headwind, but they noted that it started off the year as a positive +3% and ended the year at negative -6%, suggesting that if this current currency paradigm is maintained, sales will have another headwind in 2026.

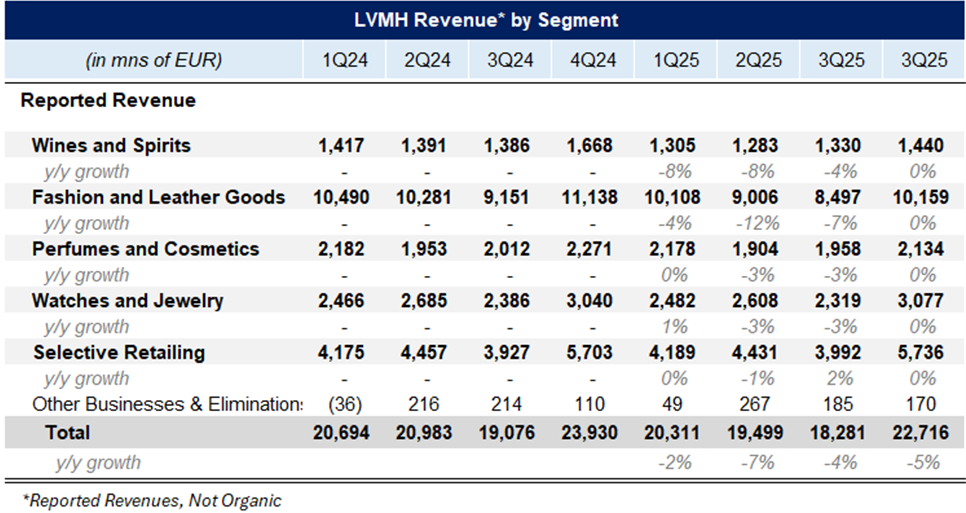

Within the business breakdown, the most important segment—Fashion & Leather Goods—generated negative -3% y/y growth for 2H25, which was an improvement over the first half of the year of -7% y/y.

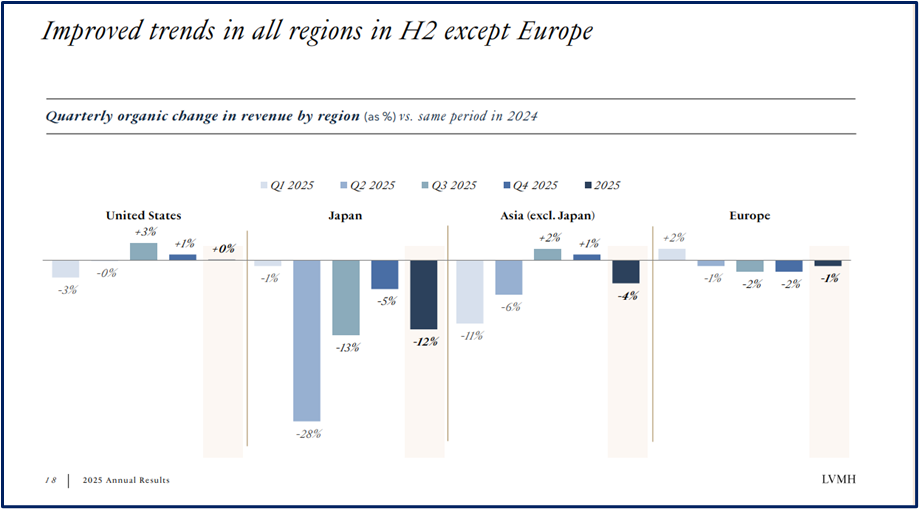

Europe and Japan experienced softness, ending 4Q25 with -2% y/y and -5% y/y growth, respectively. United States also softened q/q 200bps to +1% y/y. Asia recovered in the second half of the year, but growth slipped a bit in 4Q, down 100bps to +1% y/y.

Overall, it is not the best macro backdrop for luxury goods, with tariffs and geopolitical strives adding to consumer’s uncertainty and desire to spend. Having said that, they still generated €37.7bn Euros in their Fashion & Leather Goods division, which isn’t much lower than their all time record of €42bn in 2023.

The Wines & Spirits divisions also faced headwinds, down -5% for the year. On the call they noted the only growth market in alcohol is ready-to-drink beverages for €3.50 a pop. They believe this demand softness is cyclical though.

Perfumes & Cosmetics also had an uneventful quarter with flat growth. Watches & Jewelry did a bit better though with +5% y/y organic growth, led by Tiffany’s. On the call they toyed with the idea of Tiffany’s being the leading jewelry brand in 5-10 years.

In Select Retailing, LVMH announced the sale of DFS China operations for an estimated $400mn last week. On the call Bernard noted: “DFS, less interesting. We’ve sold most of it. We’ll continue to exit slowly, but surely.” This business had continued to suffer in the aftermath of Covid with weak international travel from Chinese citizens, who represent a large part of this business’s sales. It only recently returned to break even after plummeting losses.

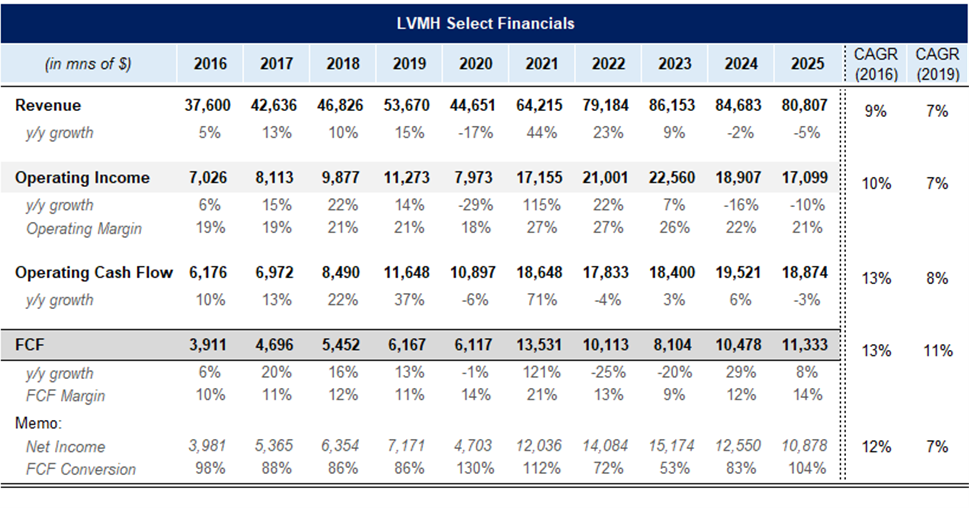

Overall operating profits for the year were -9%, with a little over half of that due to forex headwinds. In total they generated €17.75bn in operating profit for a 22% margin, down from 23.1% last year. While this may seem like a significant contraction, it is nothing that surprising. They occasionally experience some cyclicality, and it has been clear that post Covid the 3 years of strenth they experienced was at risk of contracting. In the first half of the year Fashion & Leather goods contracted -7% y/y, which already signaled this wouldn’t be a good year. Trends got better in the back half of the year, but it still looks like 2026 won’t be a record breakout year either, unless the current trend reverses.

Zooming out though, this is all part of the normal turbulence of an LVMH investment. Nothing is broken in the business and there is no clear signs that their brands are eroding or becoming more unpopular. The rest of the industry is facing similar headwinds, and in fact LVMH has generally held up better.

We can see that since 2019 they have grown revenues and operating income at a 7% CAGR. With their current margins at 21% versus peak at 27%, they probably are somewhere between the mid to the low end of what their margins could be.

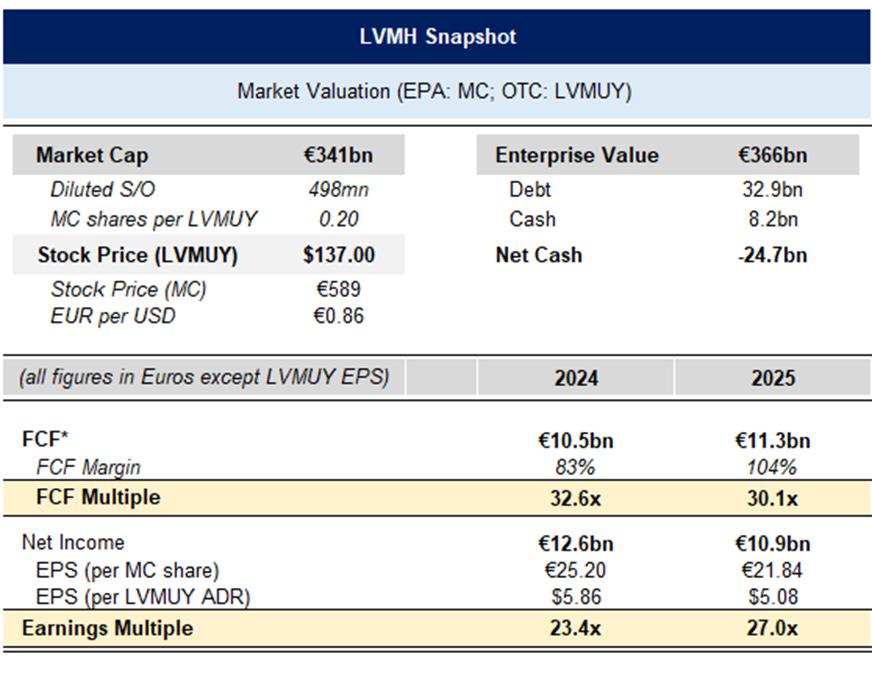

This context is important when looking at their current valuation multiples. While they are not as cyclical as an automaker or miner, they do still experience ups and downs and they are currently undergoing some consumer pressure. Below we can see that they trade at 30x trailing FCF or 27x earnings. However, in a more benign economic backdrop (like 2024) they trade on 23x earnings.

An investor will have to decide if they are comfortable paying today for a recovery and also assuming high single to low double digit operating income growth several years out into the future. On the other hand, they get a conglomerate of some of the most heritaged luxury brands that have a multi-decade history of continuing to grow earnings power (albeit with some cyclicality) that still trade 30% below their 2023 stock price.

If you haven't read it yet, make sure to check out our 121-page Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below.

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our AppFolio report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered Appfolio, APi Global, Airbnb, Axon, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in LVMH. Furthermore, accounts one or more contributors advise on may also have a position in LVMH. This may change without notice.