Meta: 1Q25 Business Update

Running Capex at ~40% of revenues seemed to solve all their problems

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members please click here for a members version of this post or here for a full PDF)

Business Update and Commentary.

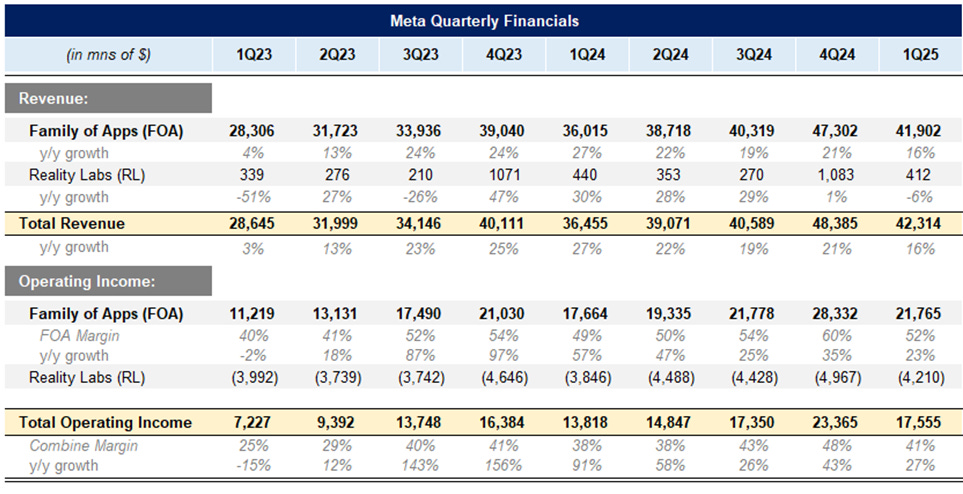

Meta reported 1Q25 and the stock rose +6% the trading day after.

All aspects of the business seem to be humming along nicely. Revenues grew +16% y/y (+19% on a constant currency basis), compared to expense growth of +9% y/y. This netted to $17.5bn in quarterly operating income, +27% y/y.

Meta’s core business, their Family of Apps segment, continues to put up strong growth and profitability, despite choppy macro. On the call, CFO Susan Li made clear that they haven’t seen anything in April that suggests a material weakness in the ad market. Some investors feared that results would be inflated by a short-lived increase in ad spend, driven by a rush to sell products ahead of the implantation of tariffs, but that does not seem to have been the case.

On the call they emphasized the auction dynamics of the platform, which is very resilient to advertisers pulling out with de minimis impact—even if those advertisers pulling out are a huge swath of Chinese ecommerce businesses.

They generated $6.1bn in free cash flow, even after accounting for a massive ~$13bn capex spend for the quarter. Capex is now running at 3.3x D&A, which suggests a margin compression headwind in the future as their structurally higher base of PPE phasing in overtime.

Offsetting the potential margin headwind from higher D&A is that fact that the capex spend is improving engagement, ad targeting, and ad attribution. This has been driving revenue growth over the past several quarters and there is no slowdown in sight. As CFO Susan Li noted on the call, “there are a lot of opportunities also for us to improve our core business by putting more compute against our ads and recommendation work.”

They are now planning to spend $64-72bn in capex for the year, a figure that puts them within throwing distances from the largest hyperscalers. This massive amount of compute is driving their AI research, which Mark Zuckerberg sees benefiting them in 5 ways:

Improved advertising

More engaging experiences

Business messaging

Meta AI

AI devices.

The first is self-explanatory, but also extremely impactful to their business. They mentioned a Reels recommendation model already increased conversion rates by +5%. Using their Llama model in Threads helped boost time spend by +4%. They noted new recommendation systems, driven by AI, have increased time spend by +7% on Facebook, +6% on Instagram, and +35% on Threads. All of these improvements may seem small in and of themselves, but the continual improvement in all of these areas translates showing more and better ads, which drives topline.

For a reminder on the dynamics of the ad auction, we quote below an explanation from our 3Q24 update:

The dynamics of improved ad targeting are to first decrease ad prices, followed by a subsequent increase. This is because as ad targeting improves, conversions increase, and thus an advertiser shows fewer ads to get the same result. This frees up ad slots for other advertisers. If it took 100 ad impressions to get a sale before and now it takes only 80, those are 20 ad impressions that are free for others to bid on. This has an impact of effectively increasing ad supply and thus the price of ads drops.

The dropping ad prices means that the return on ad spend (ROAS) improves. With a higher ROAS, more advertisers enter the bidding (or existing advertisers increase their budgets) as they can now profitably acquire sales. As more advertisers enter the auction, they bid up the price of ads, which drives the ROAS back down.

This process can basically continue as long as Meta can persist in ad targeting improvements.

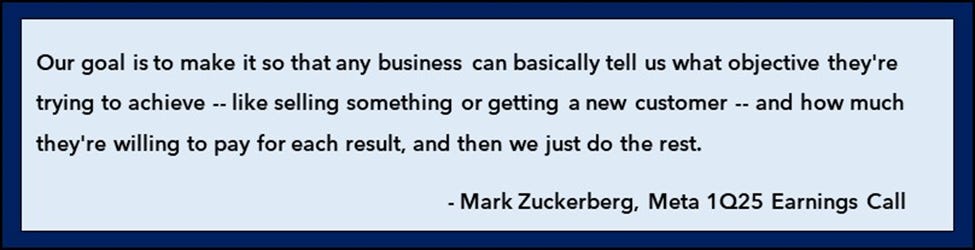

The new areas that AI is going to help open up for Meta is getting involved in the creative and eventually getting to more interactive content (including ads). Ultimately, they just want an advertiser to tell them what they want from Meta—whether that be sales, follows, clicks, etc.—and how much money they want to spend. Meta will do the rest.

As Zuckerberg, mentioned on a recent Stratechery interview, advertisers may say they want a specific audience, but Meta knows better than them who their real audience is. This will become increasingly more true in the future with AI advancements.

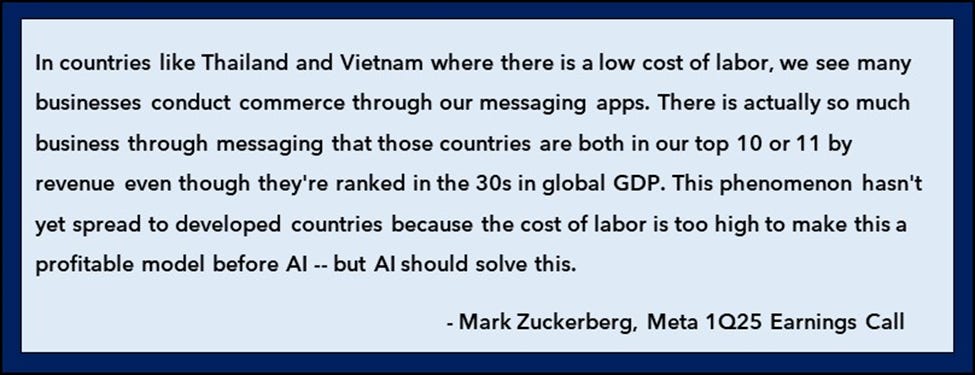

On business messaging, Zuckerberg believes that most businesses will eventually have an AI just like they have an email address. This AI will interact with the customer on the businesses behalf. Many enterprise businesses are already implementing AI in their chat-based customer services, but no one really is offering that capability to SMBs in an easy way to implement. Meta intends to fill that role.

Family of Apps other revenue was $510 million, which was +34% y/y and mostly driven by business messaging growth from WhatsApp (as well as Meta Verified subscriptions). While half a billion for Meta isn’t a large number, it does show that this tool is gaining adoption.

Other AI efforts include Meta AI, which is incorporated into WhatsApp and their other products, and will also become a stand-alone app in the future. It is also a natural fit to help enable their AR/VR initiatives, as glasses do not have hand controls, so voice (enabled by AI) is the best way to interact with the devices.

While we still tend to think of their AR/VR efforts as a call option, it should be noted that their Meta Ray Ban glasses have 4x’ed monthly users y/y. With Apple seeming to have had a very lukewarm reception to their Vision Pro, it isn’t impossible to think that Meta could eventually be the leader in this market. Now exactly what this market looks like and how profitable it ultimately is isn’t known. (In our Meta Extensive Research Report we attempted to value Reality Labs).

What is clear though is that AI is more than just a buzzword, but becoming an increasingly important driver of revenues for Meta. Zuckerberg provocatively said that “AI will make advertising a meaningfully larger share of global GDP than it is today”. This wouldn’t be the first time Meta expanded the advertising TAM: digital ads were perhaps a $25bn market in 2010 versus well over half a trillion today. Meta (and Google) are largely responsible for that growth. Will AI extend this tremendous TAM growth even further?

While everything seems to be going swimmingly for Meta today, the question is what assumptions an investor will need to make in order to earn a return. We answer that in our valuation section by updating our reverse DCF. But first, our call notes are below.

1Q25 Earnings Call Notes.

AI

Five major opportunities that we're focused on: improved advertising, more engaging experiences, business messaging, Meta AI, and AI devices

Long term investments are downstream from us building general intelligence and leading AI models and infrastructure

Testing a new ads recommendation model for Reels, which has already increased conversion rates by 5%

30% more advertisers are using AI creative tools in the last quarter as well.

“In the near future I think we're going to have content in our feeds that you can interact with and it'll interact back with rather than you just watching it.”

Engagement

In the last six months, improvements to recommendation systems have led to a +7% increase in time spent on Facebook, +6% increase on Instagram, and +35% on Threads.

Threads now also has more than 350 MAU and continues to be on track to become our next major social app.

Testing using Llama in Threads recommendation systems at the end of last year given the app’s text-based content, and have already seen a +4% lift in time spent from the first launch

It remains early here, but a big focus this year will be on exploring how we can deploy this for other content types, including photos and videos.

Other Revenue

FOA other revenue was $510 million, up +34%, driven mostly by business messaging revenue growth from our WhatsApp Business Platform as well as Meta Verified subscriptions.

Capital Allocation

Repurchased $13.4bn of stock

Paid a $1.3bn dividend.

$70.2bn in cash and marketable securities

Products

New experience on Instagram in the US that consists of a Feed of content your friends have left a note on or liked is seeing good results.

Launched Blend, which is an opt-in experience in direct messages that enables you to blend your Reels algorithm with your friends to spark conversations over each other’s interests.

Launched a standalone Edits app, which supports the full creative process for video creators - from inspiration and creation to performance insights. Edits has an ultra-high resolution short-form video camera and includes generative AI tools that enable people to remove the background of any video or animate still images, with more features coming soon.

Broadening access of Video Expansion to Facebook Reels for all eligible advertisers, enabling them to automatically adjust the aspect ratio of their existing videos by generating new pixels in each frame to optimize their ads for full screen surfaces.

Rolled out image generation to all eligible advertisers and this quarter they plan to continue testing a new virtual try-on feature that uses genAI to place clothing on virtual models, helping customers visualize how an item may look and fit.

Reality Labs

Seeing very strong traction with Ray-Ban Meta AI glasses, with over 4x as many monthly actives as a year ago, and the number of people using voice commands is growing even faster as people use it to answer questions and control their glasses.

fully rolled out live translations on Ray-Ban Meta AI glasses to all markets for English, French, Italian, and Spanish.

Ad Efficiency

New Generative Ads Recommendation model, or GEM, for ads ranking. This model uses a new architecture we developed that is twice as efficient at improving ad performance for a given amount of data and compute.

This efficiency gain enabled us to significantly scale up the amount of compute they use for model training, with GEM trained on thousands of GPUs.

They began testing the new model for ads recommendations on Facebook Reels earlier this year and have seen up to a +5% increase in ad conversions

Seeing continued momentum with our Advantage+ suite of AI powered solutions.

Incremental Attribution feature, which enables advertisers to optimize for driving incremental conversions, or conversions they believe would not have occurred without an ad being shown.

They’re seeing strong results in testing so far, with advertisers using Incremental Attribution in tests seeing an average +46% lift in incremental conversions compared to their business-as-usual approach.

Y/y conversion growth remains strong.

Continue to see conversions grow at a faster rate than ad impressions in Q1, so reflecting increased conversion rates, and ads ranking and modeling improvements are a big driver of overall performance gains.

Continue to make advertising, performance-driven advertising, in particular, more performant relative to other forms of advertising. That has continued to sort of move share towards them, but also grow the advertising pie broadly.

Guidance

2Q25 total revenue to be in the range of $42.5-45.5 billion.

Assumes foreign currency is an approximately 1% tailwind to y/y total revenue growth, based on current exchange rates.

Expect full year 2025 total expenses to be in the range of $113-118 billion, lowered from prior outlook of $114-119 billion.

Full year 2025 capital expenditures, including principal payments on finance leases, will be in the range of $64-72 billion, increased from our prior outlook of $60-65 billion

Full year 2025 tax rate to be in the range of 12-15%.

Regulatory Landscape

European Commission recently announced its decision that our subscription for no ads model is not compliant with the DMA.

Based on feedback from the European Commission in connection with the DMA, they expect they will need to make some modifications to our model, which could result in a materially worse user experience for European users and a significant impact to our European business and revenue as early as the third quarter of 2025.

Appealing the Commission's DMA decision but any modifications to our model may be imposed before or during the appeal process.

Macro

Have seen some reduced spend in the U.S. from Asia-based ecommerce exporters, which they believe is in anticipation of the de minimis exemption going away on May 2nd.

A portion of that spend has been redirected to other markets, but overall spend for those advertisers is below the levels prior to April.

Q2 outlook reflects the trends we’re seeing so far in April, which have generally been healthy

Some of our Asia based advertisers cut spend to the United States in April. Again, some of that spend has been redirected into other geographies, but not fully. And we have not we’ve not heard advertisers tell us explicitly that they are pulling forward spend.

Valuation.

Moving on to valuation...

The rest of this update is only accessible to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post! You will also get our 166-page Meta Research Report and a large library of our other reports and updates!

For further reading, check out our Meta Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Meta (Apple, Spotify).

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Meta report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered APi Global, Airbnb, Axon, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in Meta. Furthermore, accounts one or more contributors advise on may also have a position in Meta. This may change without notice.