Meta: 1Q26 Business Update

The Big Personalzied AI Bet

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members click here for a longer version of this post or here for a PDF version of this post here)

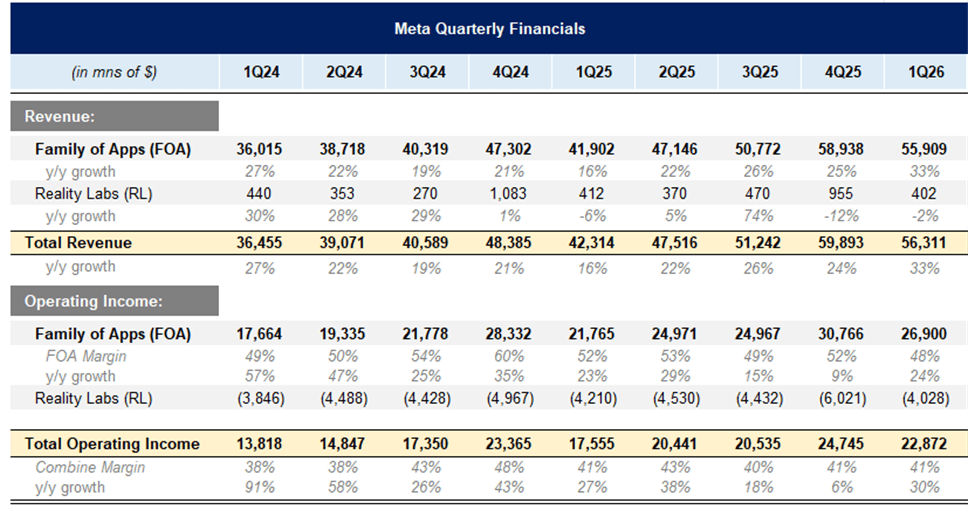

Meta reported a very strong quarter with revenue growth of 33% y/y or 29% y/y on a constant currency basis.

This was driven by ad impression growth of 19% y/y and ad price growth of 12% y/y. Generally speaking, it is a good thing that more revenue growth is coming from impressions than ad pricing.

They guided next quarter to 22-28% y/y growth, inclusive of a 2% forex tailwind.

Despite strong FOA revenue growth of 33%, EBIT segment margins fell almost 400bps as a higher depreciation expense from the large capex build out started to run through the P&L.

In terms of Meta’s core business, there isn’t much to say. Usage is really strong—and growing—with more use of video and better recommendations, ad targeting continues to improve, and their advancements in AI opens the door for a whole new level of understanding as to why a user likes a particular piece of content. This in turn can lead to better and smarter content recommendations and ads.

“So instead of just looking at statistical patterns of what types of people engage with what content, for the first time in Meta’s history, we’re going to be able to develop a first principles understanding of what you care about.”

– Mark Zuckerberg, 1Q26 Call

The list of how AI has improved the business is long:

On Instagram, the ranking improvements that we made in Q1 drove a 10% lift in real time spent.

On Facebook, total video time increased more than 8% globally in Q1, the largest quarter-over-quarter gain in 4 years.

Within the U.S. and Canada, ranking improvements they made drove a 9% increase in video watch time on Facebook in Q1.

Enhancements they made to Lattice’s modeling and learning techniques, along with advances in their GEM model architecture, drove a more than 6% increase in conversion rate for landing page view ads.

They expanded coverage of our adaptive ranking model to support off-site conversions, which drove a 1.6% increase in conversion rates across the major surfaces on Facebook and Instagram.

Advertisers using their video generation feature saw more than 3% higher conversion rates in tests.

While investors have significant doubt about what the ROI of all of these AI datacenters will be, it seems Meta has more proof points than anyone on how they are using AI to drive returns. And this is before noting that an increase of AI usage internally has supported a smaller workforce.

Meta’s AI spend though has two very different categories. 1) All of the CapEx they are spending on data centers, chips, servers, and next gen AI infrastructure. 2) All of the OpEx they are spending on hiring very expensive data research scientists and giving them valuable compute to build a frontier AI model.

Even if Meta fails though in their efforts to create a leading AI Model (although by some metrics they are very close with Muse Spark), they can still use all of the data center compute they built out for their Family of Apps to power better recommendations and ads. While there still is some risk of them overbuilding, it seems that more compute has continued to drive better results and I don’t believe we are at the edge of that already.

The second category seems to be a somewhat binary bet. Either they succeed in creating a good enough AI model that users start to adopt it in their apps, or they don’t. Meta’s ambitions with AI are very broad. They have an eye at creating everything from a stand-alone consumer AI app (Meta AI) where they can become “THE” AI a consumer relies on for everything, while also providing AI agents for business’s to accomplish a variety of tasks, and injecting AI into their apps, as well as making it the interface for AR and VR hardware.

Meta no doubt has some disadvantages. Besides being behind Google, Anthropic, and OpenAI in the race, they also will have to overcome significant user distrust. Out of all of the big tech companies, Meta is viewed with the most suspicion, especially when it comes to matters of personal data. This is problematic because Meta wants to combine all of the data they have on you to create the most personalized AI of any company. The only way they will be able to overcome that is by having a vastly superior product that makes consumers more forgiving.

They do though have some advantages. Aside from a massively profitable ads operation that can fund a multi-hundred billion dollar investment and some of the world’s top AI researchers (paid handsomely), they have ample distribution through their apps. The same way Reels became very popular by them prioritizing that interface in Instagram and Facebook, they could leverage their apps to push Meta AI onto users. They already do this to an extent, but they could get much more aggressive with it—if the product was good enough to warrant that.

Also, all of the data they have on a user probably could create a far more personalized AI than OpenAI could from chat history. Meta not only knows everything you have “liked” and what content you have lingered on, but also purchase data from successful ads, and your entire friend network—including how you converse with your friends in DMs. That trove of data is probably only matched by Google who knows your web search history, can read all of your emails and Google docs, plus has a database of every location you’ve been to through Google Maps—not to mention every video you’ve watched on YouTube. While both companies have vast amounts of user data, being able to implement this into an AI product in a respectful way will be very challenging. But, nevertheless, Meta is one of only two companies with that breadth of data that is actively creating AI agents.

The other potential advantage they have is their Meta AI Glasses. Their AR and VR devices are powered by Meta AI and so if they are able to command this category, and it grows larger, then that could force users onto Meta AI—and not just on their glasses, but everywhere. However, this assumes that glasses become an everyday device, which it is far from today. Nevertheless, Apple seems to be lagging here and there aren’t any other companies who are willing to pony up the investment as Meta is. Meta is in the best position to dominate this category when it catches on. They already sold 7 million Meta glasses, which is far from knockout success, but more than a pet R&D project.

If Meta can get to the position to be a user’s main AI, it is interesting to think how much—and little—things would change for them. Would it just be a new interface to put more ads on it? Would they just have won a smaller subscription business? Do their conversations with a user help them feed better content recommendations? Or does it help them launch AR/VR as the next compute platform? Do they sell agents to SMBs to accomplish a variety of business tasks?

It is very hard to say how any of this turns out. But what is likely is that even if they don’t become leaders in AI, people will still scroll Instagram and their ads business will be just fine.

Valuation.

The rest of this update is only accessible to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post! You will also get our 166-page Meta Research Report and a large library of our other reports and updates!

For further reading, check out our Meta Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Meta (Apple, Spotify).

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Meta report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered Appfolio, APi Global, Airbnb, Axon, Casey’s, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, Shift4, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in Meta. Furthermore, accounts one or more contributors advise on may also have a position in Meta. This may change without notice.