Meta: 2Q25 Business Update

Calculating Incremental ROIC from Capex, 5 Business Opportunities, AI Everywhere

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members please click here for the full post or here for the PDF).

2Q25 Earnings Update.

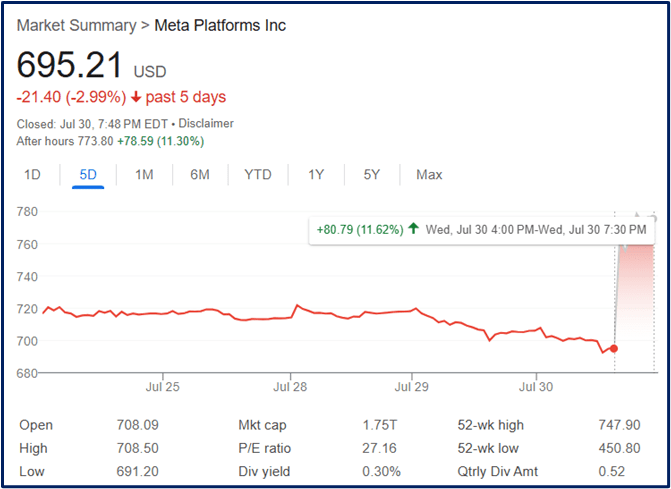

Meta reported a very strong 2Q25 and the stock popped +10% after hours.

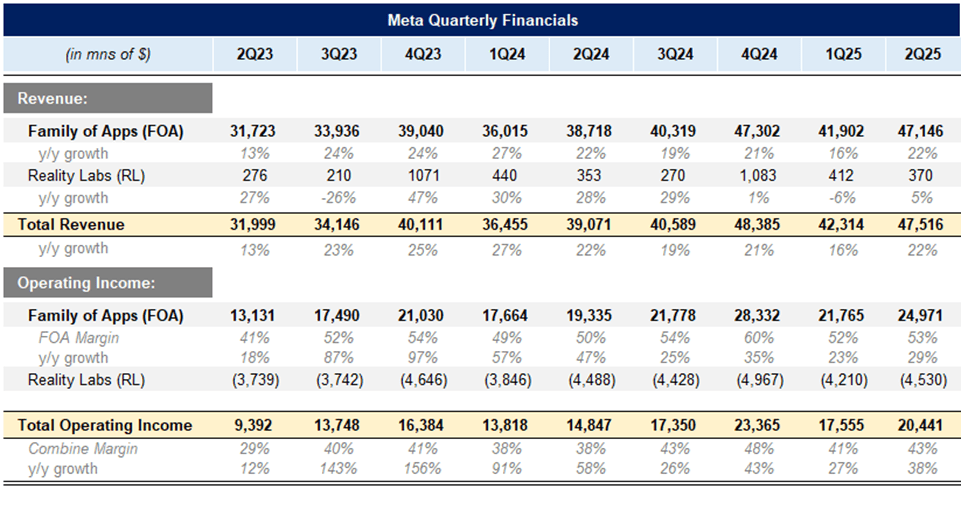

Revenue reaccelerated +22% y/y, up 600bps from last quarter’s +16%.

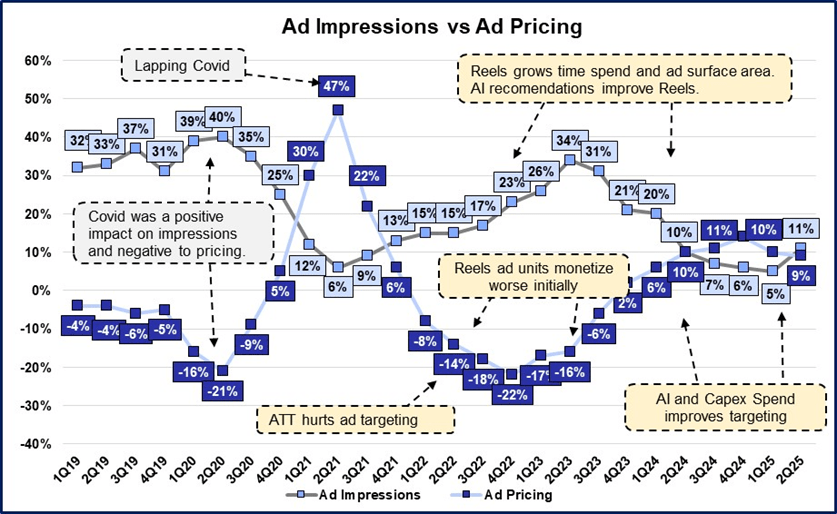

Ad impressions grew +11% y/y, mainly driven by Asia Pacific. Average price per ad increased +9% driven by increased advertising demand and improved ad performance. CFO Susan Li noted on the call that “pricing growth slowed modestly from 1Q due to the accelerated impression growth in Q2”, which is exactly what you would want to see.

Operating income margins expanded to 500bps y/y to 43%, which includes the reality labs loss of ~$4.5bn this quarter.

FOA (Family of Apps) generated $25bn in operating income for the quarter, +29% y/y. FOA Operating margins expanded ~350bps y/y to 53%.

Diluted EPS for the quarter was $7.14, +38% y/y.

Zuckerberg noted on the call that “there are 5 basic opportunities that we are pursuing: improved advertising, more engaging experiences, business messaging, Meta AI and AI devices.” Their strong execution is largely due to AI, which was credited with unlocking greater efficiency across their ad system. Their AI-powered ad recommendation model drove 5% more ad conversions on Instagram and 3% on Facebook.

He also noted progress with generative AI that improves ads on advertisers behalf. This is going to be especially helpful for smaller advertisers who don’t have large budgets to spend on professional creative.

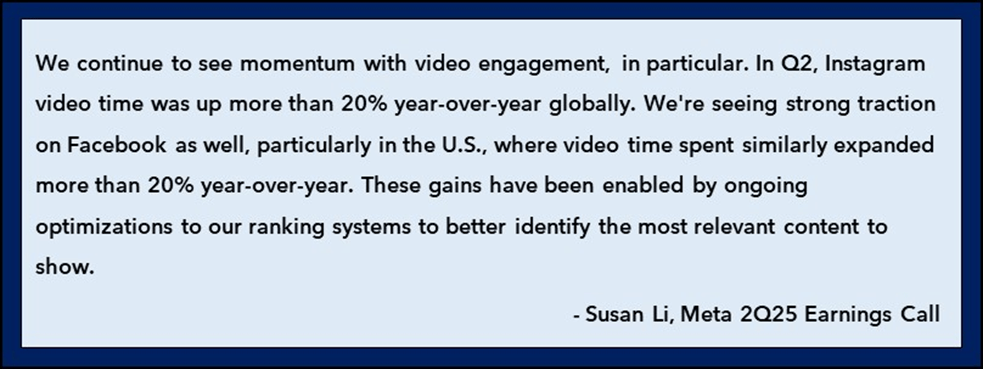

In terms of more engaging experiences, improved content recommendations have driven a 5% increase in time spent on Facebook and 6% on Instagram in 2Q alone. New AI editing tools can also improve content. On the call Susan Li noted that video growth was up 20% y/y. Within that she said that 2/3rds of recommendations are now original content (as opposed to reposts from TikTok, which was a common criticism of Reels). She said they expect further improvements this year.

The other opportunities he mentions are less impactful to the financial results today. Zuckerberg expects every business to one day have a Business AI the same way they have an email address and this will enable more business messaging. As they have the most businesses of any platform already onboarded, and together with Messenger and WhatsApp, they are well positioned to benefit from this.

Meta AI has a billion users who access it through their apps. He intends to make Meta AI the leading personal AI assistant. While the focus on an AI assistant may seem like a non sequitur for a social media company, there is some rationale. First it could improve the app experience and prevent people from leaving when they have a question. Idealistically, a lot of the activity people use ChatGPT or Google for, they could use Meta AI for. This would increase time spent on their apps.

Meta could have some unique advantages here: if you wanted to search for restaurant or beauty recommendations, surfacing a bunch of Reels could be a better experience than text or listings. They could also use the data they have on you, your friends, and your interest to better surface results.

While Zuckerberg probably hopes that they can have another consumer app (or at least product) hit, this is going to be hard given OpenAI already has a very popular consumer product and Google has many consumer touchpoints. In the current AI landscape, and given consumer trepidation of trusting Meta with too much data, they are facing an uphill battle.

Another possibility is that Zuckerberg is getting paranoid by these new AI services that are getting direct customer touch points. With enough advancement in AI-content generation, it may be possible for someone to just request the sort of content they wish to see and thus turning every AI app into de facto entertainment destination. Entertainment is one of the biggest reasons people end up on Instagram or Facebook. While this also seems a bit farfetched, there is no doubt that there will be a time spent war for consumer’s limited attention.

Sam Altman likes to point out that people don’t tend to regret the time they spend on ChatGPT as they do with social media. While a social media habit has proved to be sticky for billions of people, it is possible that consumer preferences change overtime—which could be a huge headwind for Meta. Perhaps Meta having their own AI assistant and app could be a hedge against that.

More clearly though, the AI assistant plays into their efforts to build a leading AR/VR platform, which relies on AI for the consumer to interface with it. This quarter they noted strong momentum with Meta’s Ray-Ban glasses. Zuckerberg sees the glasses as a key way that people will integrate “super intelligence” into their everyday lives.

Business Commentary.

Zooming out, everything is going well for Meta. Usage is up (Daily app users +6% y/y), time spent is growing, and their ability to target ads is improving. Even more incredible is that there doesn’t seem to be an immediate limit to how much AI can help improve recommendations of content and ads, in addition to it helping improve both with Generative AI and AI-enabled editors. They are very well positioned to benefit from AI improvements, even if their Llama model never catches up to OpenAI or Google.

While it is still unclear how much of a reality their Reality Labs efforts are, they will not lose ~$18bn a year indefinitely. An investor can assume that there will either be real value created or they will shutter the division. It doesn’t seem likely that they will continue to spend at this level 10 years from now if they still haven’t gained broad adoption of their devices. While 10 years may be a long time, the fact that it is not forever is an important consideration when thinking of the DCF.

The only real question that lingers over Meta is their normalized free cash. After adjusting for SBC and backing out their massive $16.5bn quarterly capex spend, it leaves Meta with just $4.2bn in free cash flow. This is down ~35% y/y from $6.6bn. This yields a very low 23% net income to free cash flow conversion figure. (For each dollar of net income they report, only 23 cents are actual cash flow).

Now of course this is because...

The rest of this update is only accessible to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post! You will also get our 166-page Meta Research Report and a large library of our other reports and updates!

For further reading, check out our Meta Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Meta (Apple, Spotify).

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Meta report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered Appfolio, APi Global, Airbnb, Axon, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in Meta. Furthermore, accounts one or more contributors advise on may also have a position in Meta. This may change without notice.