Meta: 4Q25 Business Update

Is AI a Business Accelerator or Cash Incinerator?

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members click here for a longer version of this post or here for a PDF version of this post here)

4Q25 Update.

Meta reported 4Q25 earnings and the stock popped +7% after hours.

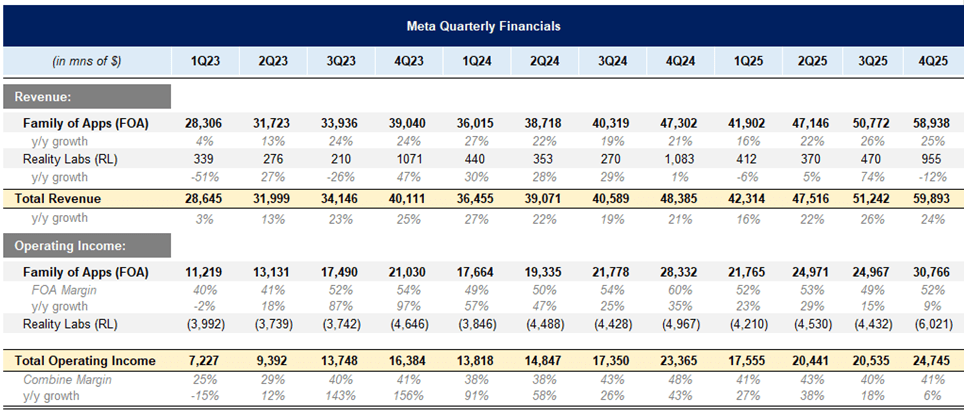

Their core business continues to perform very strongly with top line revenues up +24% y/y. While that is a slight 200bps decel from last quarter, it still is impressive.

Daily active people grew +7% y/y to 3.58 billion.

Ad impressions grew +18% y/y, which was an 800bps jump from last quarter’s +10% y/y.

Ad pricing increased by +6% y/y, which was 400bps less than last quarter. This is a positive as the better Meta is with ad targeting, the more ad pricing decreases initially, which improves ROAS for advertisers.

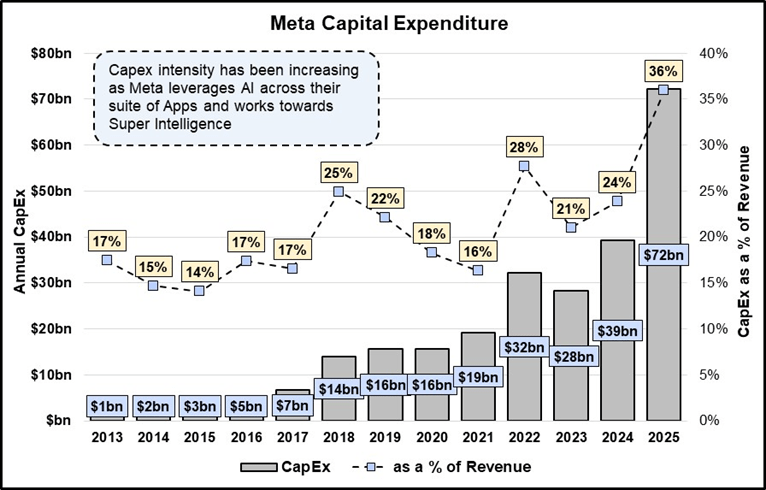

While the business is performing well, their spending has exploded. Total costs and expenses are +40% y/y and operating income was up only +6% y/y.

In 2026 they anticipate another huge jump up in expenses, with guidance calling for $162-169bn in costs, up about +41% y/y at the midpoint. Part of this is because of an increase in depreciation (as readers will recall we anticipated this over the past several write-ups), and also growing infrastructure costs (again).

They also note that the second-largest contributor to total expense growth will be employee compensation, which includes AI hires. (Next year will be the first full year of all of those very high AI researchers pay packages that grabbed headlines).

Unsurprisingly, investors should not expect much earnings growth next year. Meta’s press release noted 2026 operating income would be “above” 2025, suggesting barely any growth.

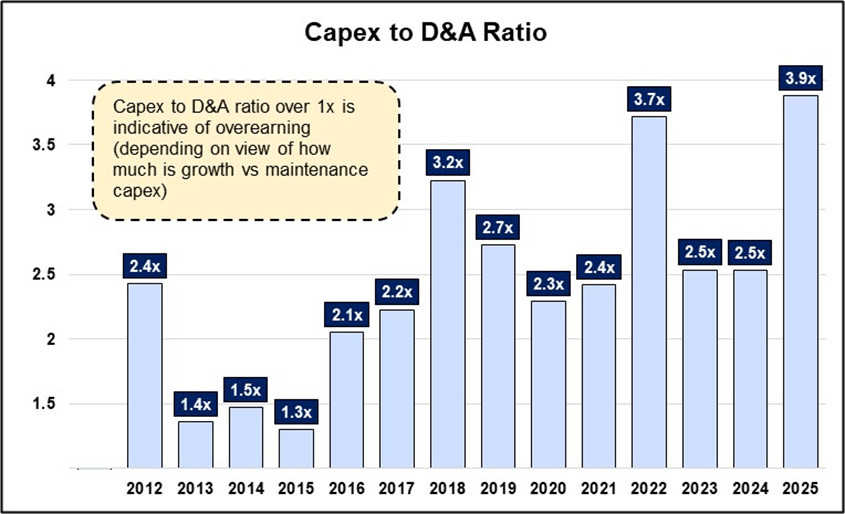

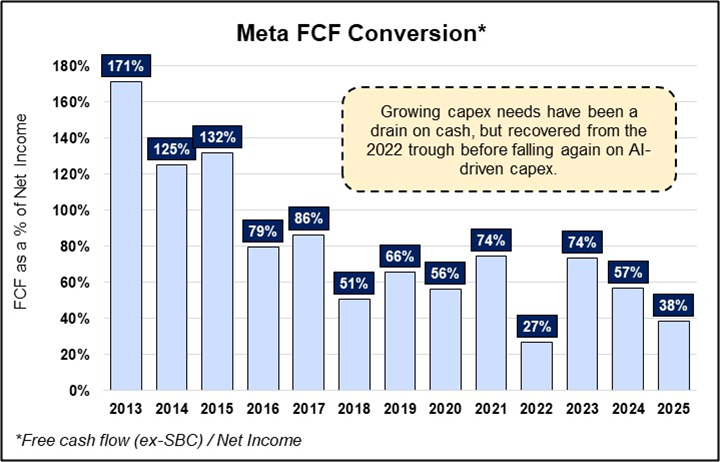

The discrepancy between cash flow from operations and free cash flow is as large as it’s ever been. On the one hand they have generated an impressive $95bn in operating cash flow in 2025 (after subtracting SBC and despite Reality Lab losses). However, after capex and financing lease payments, free cash flow drops to just $23bn.

Capex is expected to increase even more next year to $115-135bn, meaning free cash flow will likely all but disappear.

Business Commentary.

Zooming out, Meta is killing it. They seem to be one of the clearest beneficiaries of AI and every stat on the call mentions how AI is improving time spent or ad conversion. Instagram Reels watch time was up +30% y/y in the United States. Facebook optimizations resulted in a +7% lift in organic feed and video posts, which resulted in the largest quarterly revenue impact from Facebook product launches in two years. A new ad attribution model drove a +24% increase in incremental conversion vs their standard attribution model. Their “GEM” model drove a +3.5% lift in ad clicks on Facebook and a +1% gain on Instagram. And adjusting the timing of when an ad is shown on Facebook drove a 4x larger revenue impact than just increasing the ad load, suggesting ad optimization can continue on a new vector besides matching the right ad to the right person.

Even outside of content recommendations and ad targeting, AI is benefiting the actual ad copy. Their video generation tools hit $10bn in revenues in 4Q, with q/q growth outpacing the increase in overall ad revenue by nearly 3x, suggesting this will be a new driver to increase advertisers’ willingness to spend.

There also is AI agents, which they think will help them build new products and work more efficiently internally. They noted that they saw a 30% increase in output per engineer with agentic coding.

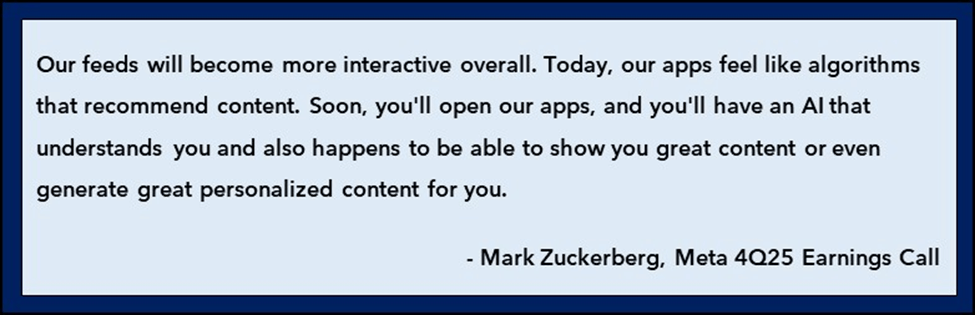

Zuckerberg also talked about how AI can change the app from an algorithm to a more personalized experience. He was sparse on details (and historically there haven’t been too many changes to the core app that they have invented that users appreciated. The original Feed idea was a Facebook invention, but Stories and Reels were copied).

Zuckerberg is really trying to tie together their family of apps, AI, and their Reality Labs efforts. He noted that: “Glasses are the ultimate incarnation of this vision” with automatic data collection feeding an AI that can create a custom UI for the user. Zuckerberg seems so impressed with his own vision that he commented: “It’s hard to imagine a world in several years where most glasses that people wear aren’t AI glasses.”

While the glasses are more popular than Apple’s VisionPro and they are best positioned for the shift to AR/VR, the existing products have yet to find a compelling use case for consumers with lackluster retention. Of course that could change… and Meta has bet close to hundred billion believing it will.

For the first time this quarter they noted that Reality Lab losses will start to go down after next year (starting in 2027). This will no doubt be more than welcomed by investors, but the $20bn in RL losses are quickly overshadowed by their expenses expected to increase beyond $162bn (at the low end) next year.

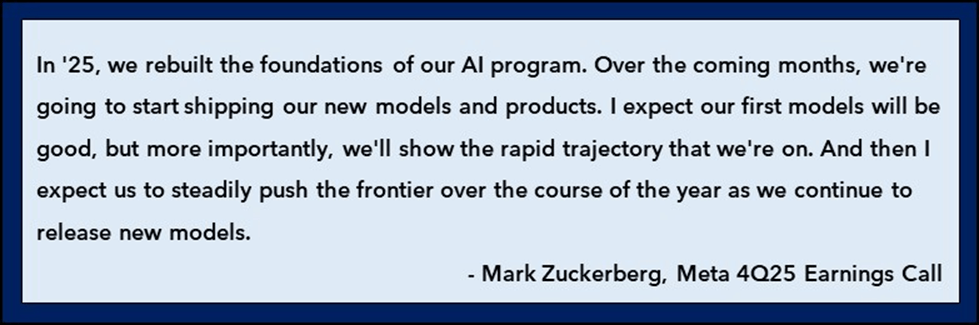

The real call option is not Reality Labs, but AI. They are spending as much if not more than any other player to research and build infrastructure for AI. While they have been largely lacking from the AI race leaderboards, Meta spent an incredible amount of money to attract top talent last year to change that. Zuckerberg expects that in the next few months they will start to ship new models. He doesn’t expect the first model to be revolutionary but believes the system (and money) they have in place will allow them to reiterate faster than competitors to eventually push them to the frontier.

It doesn’t seem like many investors (or AI researchers) necessarily believe that, but that would be the real blue sky scenario. If such an outcome happened, they could spin up a new consumer app or increase engagement on their existing family of apps with deep AI integration. Although, out of all the big tech players, it is hard to see people trusting Meta with all of their personal information, and even if they have a better model, competitors have already built a habit with users regularly using ChatGPT and Gemini. That only means that the bar has risen even more for them to displace existing usage.

However, they don’t need a knock out consumer product to be successful here. Even creating better models that are lighter (require less compute and thus money) could be a big win for them. Right now they can’t deploy their biggest models for ad targeting and have to create lighter ones. These are cheaper to use and have a better ROI, but are not as effective.

While AI is no doubt benefiting Meta and they are getting an ROI with revenues reaccelerating to 20%+ from -1% in 2022 and +16% in 2023, it is worth remembering that expenses increased +40% in this quarter (+25% for 2025) and it is unclear how much of this was needed to support this growth. While we suspect a majority of these expenses are “growth” and not “maintenance”, which implies they are not ongoing, it is possible that pinging all of these AI models costs more than their legacy machine learning models. They may be driving revenue growth, but the cost to get that revenue growth is going up too. FOA margins were 60% in 4Q24 versus 52% this quarter—and that is before a lot of the elevated capex runs through as depreciation.

That is not to say that it is a bad ROI or a poor investment, but just something to be aware of. Said another way, they had to increase investment if they wanted to continue to grow. We just don’t know yet how much of this investment can be curtailed with them keeping much—or all—of the benefit.

To understand what is priced in and the growth an investor needs to assume in order to make a return, we turn to our Reverse DCF.

Valuation.

Meta currently…

The rest of this update is only accessible to Speedwell Members.

If you are a Speedwell Member, click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post! You will also get our 166-page Meta Research Report and a large library of our other reports and updates!

For further reading, check out our Meta Extensive Research Report here.

Meta 4Q25 Call Notes

FOA

More than 3.5 billion DAUs. Includes more than 2 billion daily actives each on Facebook and WhatsApp and just shy of that on Instagram.

Q4 total Family of Apps revenue was $58.9 billion, up 25% year-over-year. Q4 Family of Apps ad revenue was $58.1 billion, up 24%

Ad Impressions & Pricing

In Q4, the total number of ad impressions served across our services increased 18% Impression growth was healthy across all regions, driven primarily by engagement and user growth and, to a lesser degree, ad load optimizations.

The average price per ad increased 6% year-over-year, benefiting from increased advertiser demand, largely driven by improved ad performance.

Reality Labs

We are directing most of our investment towards glasses and wearables going forward while focusing on making Horizon a massive success on mobile and making VR a profitable ecosystem over the coming years.

I expect Reality Labs losses this year to be similar to last year, and this will likely be the peak as we start to gradually reduce our losses going forward while continuing to execute on our vision.

Sales of our glasses more than tripled last year, and we think that they’re some of the fastest-growing consumer electronics and history. I think that we’re in a moment similar to when smartphones arrived, and it was clearly only a matter of time until all those flip phones became smartphones. It’s hard to imagine a world in several years where most glasses that people wear aren’t AI glasses.

The year-over-year decline in Reality Labs revenue is due to us lapping the introduction of Quest 3S in Q4 of 2024 as well as retail partners procuring Quest headsets during the third quarter of 2025 to prepare for the holiday season, which was recorded as revenue in Q3.

Today, our apps feel like algorithms that recommend content. Soon, you’ll open our apps, and you’ll have an AI that understands you and also happens to be able to show you great content or even generate great personalized content for you. Glasses are the ultimate incarnation of this vision. They’re going to be able to see what you see, hear what you hear, talk to you and help you as you go about your day and even show you information or generate custom UI right there in your vision.

Cloud & Compacity Constrained

We are compacity constrained. Demands for compute resources across the company have increased even faster than our supply. So we expect over the course of 2026 to have significantly more capacity this year as we add cloud. But we’ll likely still be constrained through much of 2026 until additional capacity from our own facilities comes online later in the year.

Agentic AI

Our vision is building personal super intelligence. We’re starting to see the promise of AI that understands our personal context, including our history, our interests, our content and our relationships. A lot of what makes agents valuable is the unique context that they can see. And we believe that Meta will be able to provide a uniquely personal experience.

Today, our systems help people stay in touch with friends, understand the world and find interesting and entertaining content. But soon, we’ll be able to understand people’s unique personal goals, and tailor feeds to show each person content that helps them improve their lives in the ways that they want.

Our ads today help businesses find just the right very specific people who are interested in their products. New Agentic shopping tools will allow people to find just the right very specific set of products from the businesses in our catalog. We’re focused on making these experiences work across both our feeds and across business messaging, significantly increasing the capabilities of WhatsApp over time.

I just think the fact that agents are really starting to work now is quite profound. And I think it is going to allow — we’re already starting to see the people who adopt them are just being significantly more productive. And there’s a big delta between the people who do it and do it well and the people who don’t. And I think that’s going to just be a very profound dynamic for, I think, across the whole sector and probably the whole economy going forward in terms of the productivity and efficiency with which we can run these companies

Content Evolution

People want to express themselves and experience the world in the most immersive and interactive way as possible. We started with text and then moved to photos when we got phones with cameras and then moved to video when mobile networks got fast enough. Soon, we’ll see an explosion of new media formats that are more immersive and interactive and only possible because of advances in AI.

We’re going to see the generation of media improve the quality of content, which, coupled with the improvements in the recommendation systems, we expect to generally accelerate the quality and effectiveness of the core business, both for people who use it organically and for businesses. So I think that will have a compounding effect.

Flattening Teams

We’re investing in AI native tooling so individuals at Meta can get more done, we’re elevating individual contributors and flattening teams. We’re starting to see projects that used to require big teams now be accomplished by a single, very talented person

There are two primary factors that drive our revenue performance

Our ability to deliver engaging experiences for our community

Instagram Reels had another strong quarter with watch time up more than 30% year-over-year in the U.S.

Facebook, video time continued to grow double digits year-over-year in the U.S. The optimizations we made in Q4 drove a 7% lift in views of organic feed and video posts on Facebook, resulting in the largest quarterly revenue impact from Facebook product launches in the past two years.

Our effectiveness at monetizing that engagement over time

AI Dubbing

One area we’re already seeing promise is with AI dubbing of videos into local languages. We are now supporting 9 different languages with hundreds of millions of people watching AI translated videos every day. This is already driving incremental time spent on Instagram, and we plan to launch support for more languages over the course of this year.

Video Creation Tool Traction

We are also seeing strong traction with our media creation tools. Nearly 10% of the reels people view each day are now created in our Edits app, almost tripling from last quarter. Within Meta AI, the number of daily actives generating media tripled year-over-year in Q4.

The combined revenue run rate of video generation tools hit $10 billion in Q4, with quarter-over-quarter growth outpacing the increase in overall ads revenue by nearly 3x.

Threads

Threads is also seeing strong momentum again, benefiting from recommendation improvements. The optimizations we made in Q4 drove a 20% lift in threads time spent.

Within threads, we’re beginning to expand ads to all remaining countries this month, including the U.K., European Union and Brazil.

On WhatsApp, we expect to complete the rollout of ads in status throughout the year with the level of ads remaining low in the near term while we follow our standard approach of optimizing ad formats and performance before ramping inventory.

Paid messaging within WhatsApp continues to scale as well, crossing a $2 billion annual run rate in Q4.

Business AI

Click to message ads revenue growth accelerated in Q4 with the U.S. up more than 50% year-over-year, driven by strong adoption of our website to message ads which direct people to a business’s website for more information before choosing to launch a chat.

We’re seeing good early traction with our business AIs in Mexico and the Philippines, with over 1 million weekly conversations between people and business AI is now happening on our messaging platforms. This year, we will expand availability of our business AIs to more markets, while also extending their capabilities so they not only answer questions on topics like product availability, but can help people get things done right within WhatsApp.

Guidance

We expect our first quarter 2026 total revenue to be in the range of $53.5 billion to $56.5 billion. Our guidance assumes foreign currency is an approximately 4% tailwind to year-over-year total revenue growth based on current exchange rates. We expect full year 2026 total expenses to be in the range of $162 billion to $169 billion. We anticipate 2026 capital expenditures, including principal payments on finance leases to be in the range of $115 billion to $135 billion, with year-over-year growth driven by increased investment to support our Meta Superintelligence Labs efforts and core business. Despite the meaningful step-up in infrastructure investment, in 2026, we expect to deliver operating income that is above 2025 operating income.

I expect both full year reported and constant currency revenue growth to be below the levels in Q1 for a few reasons. First, we would expect that currency tailwinds will dissipate later in the year based on current rates. Second, we’ll be lapping stronger periods of growth later in the year that benefited from our 2025 ad performance investments and the strong macro landscape. And finally, we expect there could be some headwinds from our introduction of the revised less personalized ads offering in the EU that begins rolling out later in Q1.

Manus Acquisition

You have a significant number of businesses that already pay a subscription to basically use their tool to accelerate their business results and integrating that kind of thing into our ads and business managers, so that way we can just offer more integrated solutions for the many, many millions of businesses that use and rely on our platforms is going to be really powerful, both for accelerating their results using the existing products that we have and I think adding new lines as well.

Online Commerce

The online commerce vertical was the largest contributor to year-over-year growth. That was followed by professional services and technology. So in online commerce, year-over-year growth was strong. It was actually relatively consistent with Q3 levels and that was broad-based across advertiser regions and sizes.

3 Ways Meta is Improving Recommendations

Scaling up the models and increase the amount of data we use, including a longer history of content interactions to further improve the overall quality of recommendations.

Continue to make recommendations even more adaptive to what a person is engaging with during their session. So the recommendations we surface are more relevant to what they’re interested in at that moment.

Deeply incorporating LLMs into our existing recommendation systems, given their capability to more deeply understand content. And so this will, I think, in particular, be useful for content that has been more recently posted since there’s less engagement data to base recommendations off of.

Meta AI

Now available in over 200 markets.

Will be available to more advertisers, so each business has an AI assistant they can chat with that remembers their businesses’ goals and provides personalized recommendations on how to improve performance.

Capital Allocation

Right now, we think the highest order priority for the company is investing our resources to position ourselves as a leader in AI. And so that is really the — that’s kind of the first order of use of capital, but we’ll continue to be opportunistic and evaluate repurchases versus other uses of cash.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Meta (Apple, Spotify).

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Meta report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered Appfolio, APi Global, Airbnb, Axon, Casey’s, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, Meta, Perimeter Solutions, Porsche, RH, Shift4, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in Meta. Furthermore, accounts one or more contributors advise on may also have a position in Meta. This may change without notice.

Hi Drew.

First of all, big fan.

Second, do you back out "Taxes paid related to net share settlement of equity awards" to get to FCF. Just like SBC. If not, why not. Its around 18 billion for Meta for FY 2025.

Feels to me like its a real cost.

Thanks!

Ps. Alex should be on the Synopsys at least once a month!