Perimeter Solutions Exploratory Report

Research Report on a Fire Safety Solutions and Specialty Chemical Company

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

We will also record a podcast episode on Porsche soon, follow our podcast here to get it when it’s released: (Apple, Spotify).

This is an exploratory research report, which means it is about a quarter of the depth of our typical reports. Since Perimeter Solutions has a short history of being public, the amount of research we can do is more limited relative the many hundreds of hours we spend on our Extensive Research Reports. Speedwell Members can find a PDF of the full report here. If you wish to get access to the full PDF, as well as all our other reports and updates, click here.

Background History.

Prior to gaining prominence as an agrochemical and agricultural biotech business, Monsanto was a chemical company that focused on food additives and later industrial chemicals. After WWII they acquired several companies and increasingly focused on agrochemicals, including producing fertilizer. One of the largest ingredients in fertilizer is phosphate, and as Monsanto learned how to efficiently source and produce phosphate, they started looking for alternative uses for it.

In the early 1960’s, a new use-case was found in the form a fire retardant they created and trademarked as Phos-Chek—the “Phos” referring to their key ingredient, ammonium phosphate. Trade-marked in 1963, Phos-Chek was the first phosphate-based fire retardant approved by the US Forest Service.

The product was typically dumped by air on areas to create a barrier that prevented a forest fire from spreading. Ammonium phosphate helps create a barrier over vegetation that prevents plant material from igniting. When it is exposed to fire, the surface turns to non-flammable carbon which prevents the fire from getting more fuel.

The substance is typically red or dark pink so firefighters can see where it is applied. The coating stays on the plants until a major rainfall occurs. Since the key ingredient is similar to what is in fertilizer, it helps vegetation grow. However, it’s application can be mildly to moderately harmful to certain species and particularly aquatic systems if it gets into water. Although there would be little life that survives a major forest fire anyway, so the trade-off is usually seen as worth it. Overtime, they continued to change the formula to make it more amenable to the animal ecosystem while preserving its fire retardant capabilities.

Phos-Chek stayed with Monsanto until 1997 when they divested a unit called, Solutia, that produced most of their specialty chemicals, including Phos-Chek. Solutia was burdened with debt and would face significant litigation that ultimately forced it into bankruptcy in 2003. Although, a few years prior to that Solutia transferred Phos-Chek to Astaris, a JV between Solutia and FMC. In 2005 Astaris sold Phos-Chek to Israel Chemicals Ltd, where it sat for over a decade before being sold to SK Capital in 2018. SK Capital acquired their Fire Safety and Oil Additives business, which included Phos-Chek and a few other chemical businesses. They would rename this collection of businesses to Perimeter Solutions and it would be led by Eddie Goldberg, who was previously the Business Director for Israel Chemicals’ Performance Additives and Solutions, where he held responsibility for their fire safety segment.

In 2019 an acquisition vehicle, “EverArc”, was listed on the London Stock Exchange and raised $340mn in the process. EverArc’s Board of Directors included Nick Howley, cofounder and current Chairman of Transdigm, Will Thorndike, who is best known for having authored “The Outsiders” but also founded private equity firm Housatonic Partners, and Tracy Britt Cool, who was CEO of Berkshire-owned Pampered Chef and oversaw other Berkshire Hathaway subsidiaries before cofounding Kanbrick private equity.

EverArc was created with the intention of finding an acquisition that could act as a platform to launch a new company that met the groups 5 economic criteria. While EverArc was like a SPAC, it was not technically a SPAC because shareholders did not vote on the ultimate transaction and there was no share redemption feature. Nick Howley stated his goal was to “give our shareholders private equity-like returns with the liquidity and long-term focus of a public market”. (This is the same messaging Transdigm uses in their investor communications).

They were industry-agnostic but had 5 economic criteria that they filtered acquisition opportunities through: 1) recurring revenue streams, 2) long-term secular growth tailwinds, 3) a product that accounts for a small portion of the customer’s overall costs and provides a lot of value, 4) significant free cash flow generation with high returns on tangible capital, and 5) significant M&A opportunity.

In 2021, EverArc holdings set their sights on Perimeter Solutions as their target and consummated an acquisition valued at $2bn, taking the company public in the process.

Below Will Thorndike lays out their rationale for choosing Perimeter Solutions to acquire after looking at over 200 targets.

After completing the acquisition, they listed the company on the NYSE under PRM.

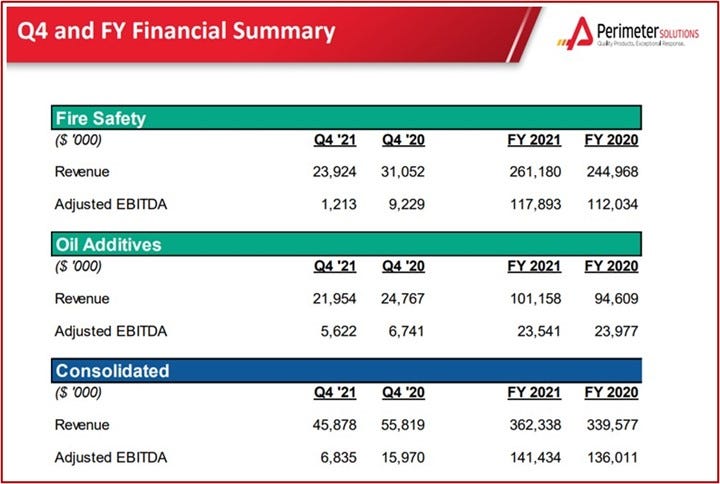

In 2021, the year of their acquisition, total revenues were $362mn, up +7% y/y. Adjusted EBITDA was $141mn, up just +4% y/y. 72% of revenues and 83% of EBITDA stemmed from the fire safety segment, with the remainder housed in “Oil Additives”, which they renamed to “Specialty Products in 2Q22.

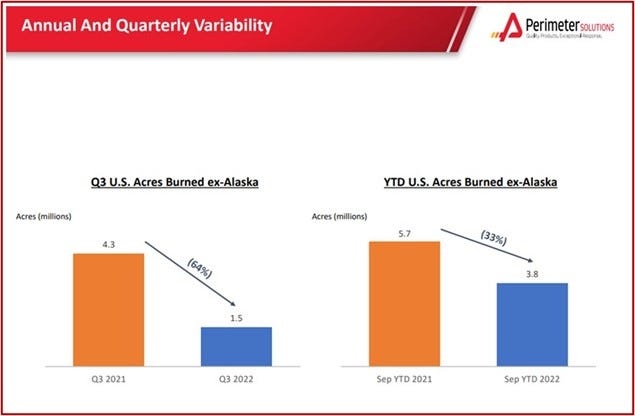

The following year the variability in the business was on full display as the number of acres burned in the U.S. fell from 5.7mn for the first 9 months in 2021 to 3.8mn. Less acres burned means less of a need for their fire retardants.

At the same time though, their oil additives segment carried the slack, increasing EBITDA ~100% y/y. CEO Edward Goldberg noted that their outperformance was driven by winning new business with existing and new customers, improving their cost structure, and increasing prices.

The following year though, it became clear that it was also the demand environment that was strongly helping drive this segment. Towards the end of the year, in 4Q22, they noted that “a couple of large customers temporarily shut down their facilities late in Q4 as they focused on working off inventories”. Their end customers had overbought product, likely driven by fears of supply chain disruptions, and now refrained from additional purchases all together.

At the same time that the fire season was unusually calm, competition started to knock. In December 2022, Fortress became the first company in two decades to threaten Perimeter’s position as the sole provider of fire retardants to the U.S. Forest Service’s (USFS), one of the largest purchasers of fire retardant in the country (in 2021 they accounted for 58% of Perimeter’s fire safety segment).

Fortress was added to the USFS Qualified Product list with approvals for two fire retardant products. In May of 2023 they entered into a contract with the USFS for 5 mobile deployed air tanker bases with the USFS having the goal of helping them build scale to increase competition in the sector. (Fortress Services was acquired by Compass Minerals, ticker CMP, in 2023 after initially taking a 45% ownership stake a few years prior).

Below, Compass Minerals CEO Kevin Crutchfield notes they are targeting 50% market share. Perimeter’s stock price was cut in half from its peak of $14 to ~$7 a share.

But, in March 2024, the USFS found significant corrosion in the air tankers that had flown with Fortress’ magnesium, chlorine-based aerial fire retardant and announced that it would not be entering into a new contract with Fortress. Compass took an impairment charge on the business and it seems that their future commitment to this business is in question.

While competition was trying to crack the domestic market, Perimeter Solutions was pushing forward internationally. As noted on their 2Q22 call, “Greece historically used cheaper and less-effective foam products rather than retardant to combat wildfires”. In 2022 they contracted for one of Perimeter’s mobile fire retardant bases, as a sort of test, which could anticipate full adoption of their products in the future.

This is what happened in Italy, where in 2022 they made “the decision to switch their entire aerial firefighting effort to retardant”. Like in the U.S., their Italy operation will provide a full service to Italian firefighters with bases, logistics, maintenance, and staffing taken care of.

At the same time, Perimeter Solutions is pushing new product innovation forward, including a fourth generation of fluorine-free fire retardant (eliminating the “forever chemical” PFAS which is harmful to the environment and people). They continue to look for operational efficiencies and new acquisition opportunities as they compound shareholder capital at “private equity-like” rates of returns. But how strong are their moats really? Is their level of debt worrisome for a business that can experience significant periodic downturns owing to the unpredictability of fires? And how have they done as capital allocators for the shareholders, and not just the “founders” who have a special compensation arrangement?

We will touch on all of that and more, but first, we will move onto the business.

Business.

Perimeter Solutions is a specialty chemicals producer with a focus on fire safety-related products and solutions. However, their objective is not to necessarily stay within their existing industry verticals but rather “own, operate, and grow uniquely high-quality businesses”. The same way the original EverArc founders did not set out to get into the fire safety business, but found it fit their target economic criteria, it is possible Perimeter Solutions ends up acquiring its way into a different industry.

As mentioned, their target economic criteria is 1) recurring and predictable revenues, 2) long-term secular growth tailwinds, 3) products that account for a critical but small portion of its overall value, 4) significant free cash flow generation with high ROTC, and a 5) potential for opportunistic consolidation.

Below we see their current two revenue segments: 1) Fire Safety, and 2) Specialty Products.

Fire Safety: Their marquee brand is their fire retardant solution Phos-Chek, but they have several other notable fire safety products including Fire-Trol, Auxquima, Solberg, and Biogema. In addition to producing fire safety chemicals, they provide full-service solutions including building and maintaining air bases & mobile units, storing & mixing product, a logistics operation to rapidly deliver product anywhere, and employing teams that can work with various firefighting agencies with no advanced notice.

They describe this segment in three distinct categories: 1) Fire Retardants, 2) Firefighting Foams, and 3) Custom Equipment and Services.

Fire Retardants: Fire Retardant helps stop and slow fires by chemically altering potential fire fuels, like vegetation, and making them non-flammable. Fire retardant can be applied aerially or through ground units and is typically laid down in advance of a fire approaching an area. The idea is it allows firefighters to draw a line where they will focus their fire fighting efforts on to limit the spread.

Firefighting Foams: These foams can be split into Class A, Class B, and Class A/B. Class A is used to fight wildfires and is formulated to make water a more effective force against fire suppression. When the water mixes with the chemical and air, it creates a foam that extinguishes fires faster than water alone. Class B foams are used primarily to address combustible liquids and are used mostly by industrial customers with flammable liquids. Class B foam is designed to rapidly extinguish a fire and secure it to prevent reignition. Class A/B is a foam with both properties are primarily used by municipal fire departments.

Custom Equipment and Services: Perimeter Solutions offers a full-service solution including a broad range of equipment and services to support the deployment of their fire retardants and firefighting foams. They support over 200 bases in their service network globally. They have specialized equipment to store, mix, and load retardant at air bases, as well as with mobile bases. Their service has to have 100% reliability with the ability to very quickly move a base from being dormant to a high level of activity depending on where fires occur.

Similar to their retardants, they offer a full solution with a fluorine-free foam, installed hardware equipment, and services to replenish foam rapidly in an emergency. They operate facilities to manufacture foam in the U.S., Europe, the Middle East, and Australia.

Specialty Products: This segment’s primary product is P2S5, which is a lubricant additive that is used in a family of compounds called ZDDP, which is used to prevent wear of engines. Separately, P2S5 is used in pesticides and mining chemical applications.

Specialty products are about 30% of revenues. While they do not regularly breakout fire retardants from fire suppressants, below you can see that fire retardants are a little over twice as big as fire suppressants.

While they only operate two segments, they note that they structure their operations into 7 business units, in a structure somewhat reminiscent of Constellation Software. This allows for more decentralized decision making and accountability. Each business unit has a business unit manager that is incentivized on operational and financial results of the individual business unit. TransDigm notes that the business unit leaders “run the business like they own it”, which creates a bias to action and acting like an owner.

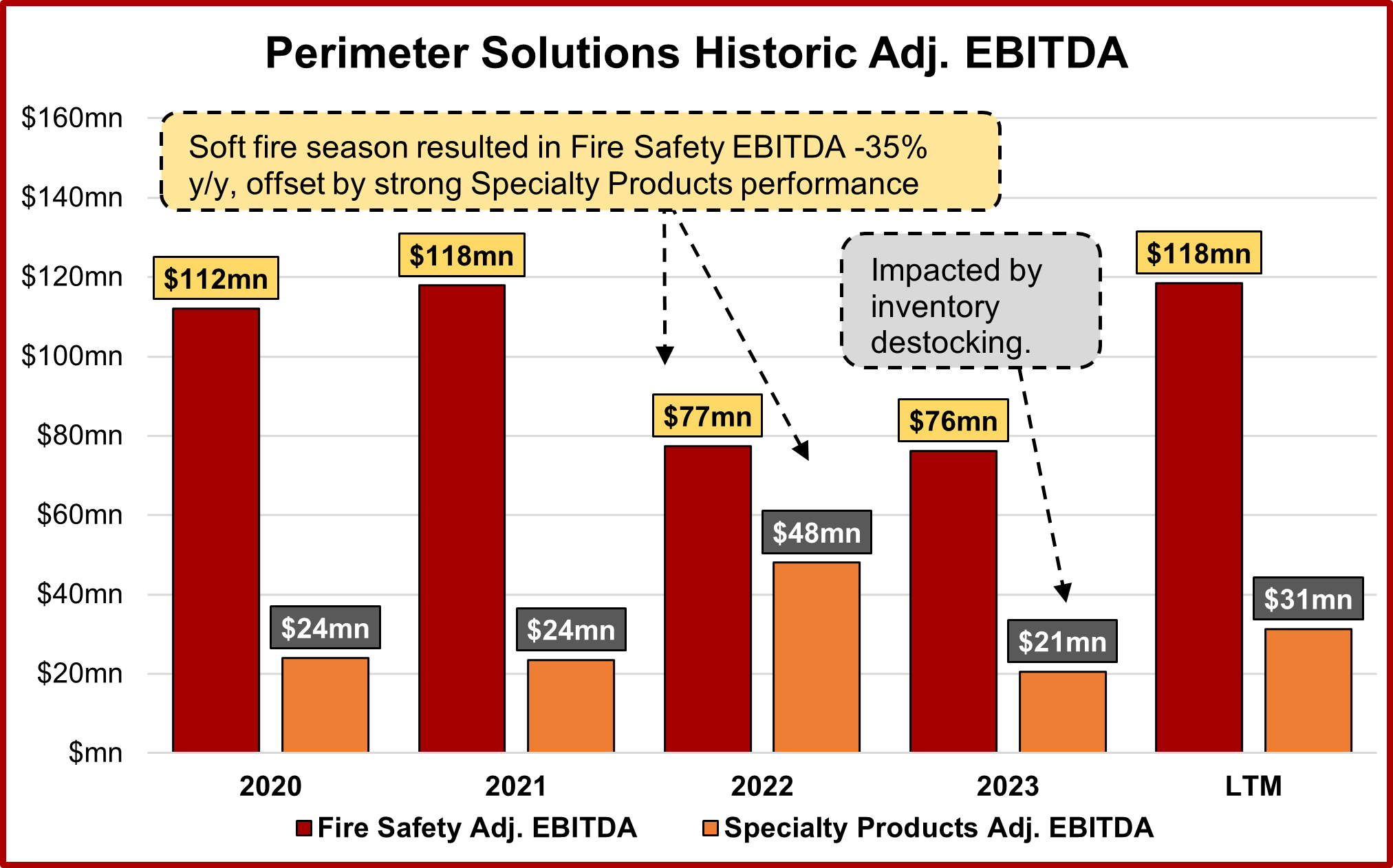

They provide Adjusted EBITDA figures by segment, which shows that $118mn of their $150mn in EBITDA comes from the Fire Safety Segment LTM. The Fire Safety segment faced headwinds in 2022 and 2023. As CEO Haitham Khouri noted on their 4Q23 call: “The 2023 fire season was very mild, with 2.3 million acres burned ex Alaska. This represented an almost 50% decrease versus 2022, which itself was a mild season and was almost 60% below a 10-year U.S. average”.

He goes on to note that despite the very mild fire season revenue and Adj. EBITDA margins were flat due to unit economic improvements, strength in their international growth, and performance from their suppressants business (which isn’t as impacted by acres burned). Whether there was any diversity in such a fire-dependent business was questionable at IPO, but the results in 2023 and LTM suggest that they are somewhat diversified from fire season unpredictability.

As noted prior, the oil segment (as it was known prior to its rename to Specialty Products) contracted severely in 2023 on end customers destocking. LTM this segment has recovered to a revenue and margin level above where they operated prior to being acquired by EverArc.

Above we can see EBITDA by segment. While we typically eschew EBITDA metrics, large amortization charges, the founders advisory fee agreement, as well as forex and nonrecurring gains do misrepresent true earnings power. In the valuation section we will estimate normalized earnings rather than just relying on adjusted EBITDA.

We will now move onto the industry they operate in and their end markets.

Industry & End Markets.

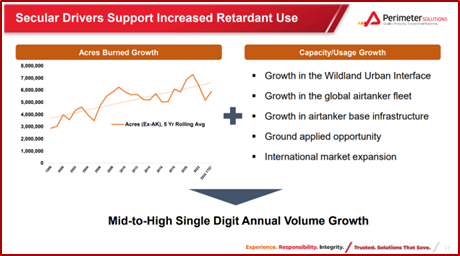

Each of Perimeter’s segments has different end markets. Their fire retardant segment is primarily driven by the number of acres burned, a growing urban area, and more use of aerial aircraft in combatting fires. From 1983 to 1993 average acres burned was 2.3mn, but over the last 10 years that number has jumped to 7.4mn acres. The number of large fires, which are defined as fires over 1,000 acres, also tripled from the 1970s to the 2010s. This increase in acres burned is expected to continue to increase. (Perimeter did clarify that “acres burned east of the Mississippi” don’t matter that much to them. Acres burned West of the Mississippi are more relevant and acres burned in California are the most relevant in terms of projecting fire retardant usage).

The second factor, an increasing urban area, means that as more people move out into “wildland” areas, there is an increased need to protect them and their homes. This is called the “Wildland-Urban Interface” and the vast majority of new homes are on this sort of land where homes are interwoven between wildland vegetation. These sorts of fires have an increased danger to people and property and it is thought that more fire fighting tactics—like an increased use of fire retardant—will be necessary for protection.

The last key variable is the availability and use of aircraft to fight fires. Since the majority of fire retardant is used aerially and historically not all aerial requests have been filled, the growth in more aircraft will directly lead to more fire retardant being consumed. The net of all of this is they expect mid to high single digit annual volume growth.

Looking at total Federal spend on fire suppression, we see that it has grown…

Become a Speedwell Member to get the rest of this report.

In the rest of this report, we cover Competition, Perimeter’s Competitve Advantages, Capital Allocation, Normalized Earnings, and Valuation!

If you are a Speedwell Member, click here and scroll down to download the full PDF on our website.

If you are not currently a Speedwell Member, but wish to join, click here.

Thank you for reading the sample of our Perimeter Exploratory Sample Report! Become a Speedwell Member today to get access to the rest of this report, as well as gain access to our growing library of Extensive Research Reports.

Members can read all of our reports on AXON, CSGP, CSU, CPNG, CPRT, DFH, DRPRY, ETSY, EVO, FND, META, RH, and WD so far!

Members will also receive on-going updates on each of our covered companies!

The Synopsis Podcast.

Check out our podcast for more business and investing content. We will dedicate an episode to Porsche on it soon! In the mean time, you can find many company-specific episodes on other businesses we have written about.

*At the time of this writing, contributors to this report may have position in companies discussed. Furthermore, accounts that one of more contributors advise on may also have a position in companies mentioned. This may change without notice. Please see our full disclaimers here.

Thanks for the report, it's well laid-out and I enjoyed reading about the history of Perimeter Solutions.

thx. I noticed that 5.9 million shares were issued to founders in 2022 for equity, but what counters this in the balance sheet to tie numbers? Same for the Liability fee went from 312 to 170, while the paid cash was 53. I am confused about the accounting world. Can u pl guide?