RH: 2Q25 Business Update

Inflection just Around the Corner… (Again)

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Members can get an extended version of the post here or a PDF of this post here).

2Q25 Update.

RH reported 2Q25 and revenues grew +8% y/y, down from the +12% y/y they did last Q. This isn’t surprising given this is the first full quarter that the tariffs impacted operations. In the letter they note that they have gained share and see demand currently ahead of revenue, which suggests a re-acceleration of revenue is to come in the back half of the year. It’s worth mentioning though that public competitor Arhaus also had a strong quarter, accelerating revenue growth to +15% (albeit on a lower revenue base).

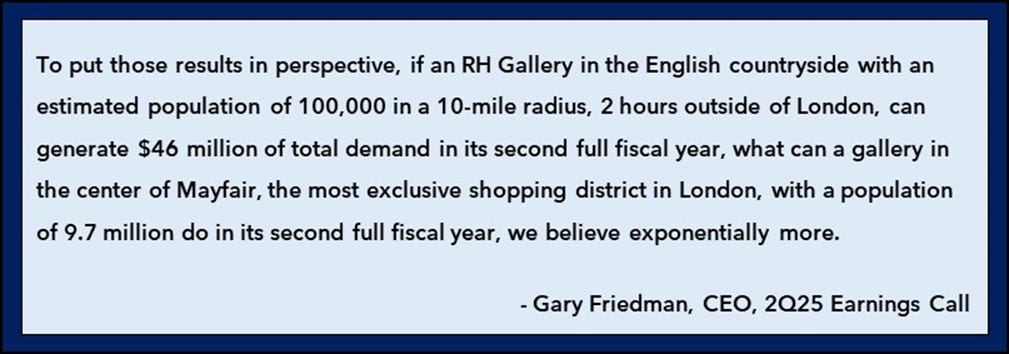

RH disclosed that RH England is enjoying a strong reception with $37-39mn of demand expected in 2025. This is in line to slightly better than their initial expectations with England given its proximity away from a populous city center. The idea was always to introduce the brand in a big and novel way, while elevating it, which they have achieved. While the sales figures are relatively inconsequential for their business, the bigger takeaway is that the brand is being well received.

RH opened their Gallery in Paris on the Champs Elysees in the first week of September. Gary spent several paragraphs in the letter explaining all of the unique things they did to make the seven floor gallery memorable. All of this is aimed at providing a sort of “wow” experience for the consumer to help elevate the RH brand.

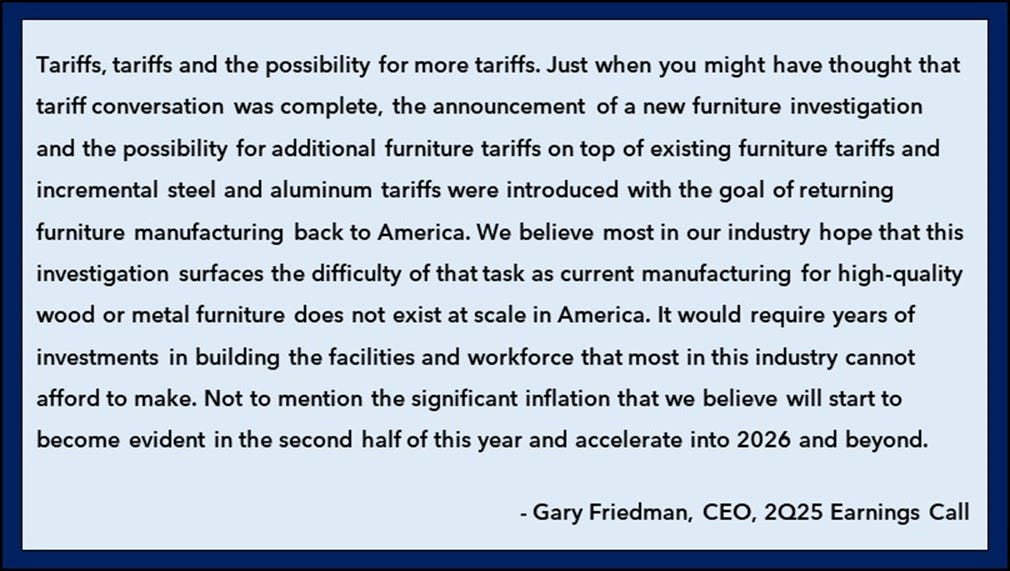

Other than new Gallery opens, the big topic was tariffs on the call.

China supply chain exposure has been whittled down over the past few years and is expected to be just 2% by 4Q (from 16% this quarter). They note that their vendor partners are currently absorbing a meaningful portion of the tariffs. The newly announced 50% tariffs on India will impact about 7% of their products.

Due to the tariffs, they continue to delay their brand extensions that were planned for the second half of 2025 and Spring 2026. They also delayed the shipping of their interior source books, shifting $40mn of revenue into Q4 and 1Q26.

Despite tariff pressures, gross margins expanded sequentially to 45.5%, +180bps q/q. Operating margins also improved sequentially to 14.3%, up from 6.9% last quarter and 11.6% in 2Q24.

However, interest expense still remains meaningful, consuming $57mn of their $128mn in operating income. But this is an improvement from last quarter where it was actually higher than EBIT. Their debt load, including operating leases, stands at $3.75bn, down about $50mn from last quarter.

Inventory is down $50mn q/q, which helps them unlock more working capital, but is still elevated. As a reminder, last quarter they noted they had $200-300mn in excess inventory from their launch of new collections. As they learn what works and doesn’t, they prune their lines.

For the full year they expect 9-11% revenue growth with adj. operating margins of 13-14% and free cash flow of $250-300mn.

Business Commentary.

RH continues to execute on what they can control with their work on the Paris Gallery garnering more foot traffic than RH NYC received. They are slated to open London and Milan in Spring 2026, which is going to give them a European foothold in several key cities. RH England is also doing well, despite a somewhat slow start.

The big near term focus though is tariffs and how they could potentially impact the supply chain. The Trump administration is leading an industry “investigation” to see the feasibility of onshoring the production of furniture. Gary Friedman makes clear that this is not realistic and it would take many years to build up that production capacity. However, he does note that they would be able to weather this relatively better than peers, but that it would still be a net bad for the industry.

While RH has no doubt endured a tough macro environment from high interest rates and depressed luxury home sales to tariffs, Gary’s vision for RH has remained remarkably consistent. They maintained their gallery expansion plans and never wavered in the belief that if they build very elevated and cool stores and experiences, that the traffic would come. They know that this traffic will eventually translate to sales.

Some investors and analysts like to point out that RH now regularly discounts their furniture and that’s not how a true luxury business would behave. That is true. However...

The rest of this business update is paywalled.

If you are a Speedwell Member, please click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post, our RH Research Report, and a large library of our other reports!

For further reading, check out our RH Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on RH (Apple, Spotify)!

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our RH report and all of our other research reports, business updates, and Plus members also receive Excels.

We have covered Appfolio, APi Global, Airbnb, Axon, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, LVMH, Meta, Perimeter Solutions, RH, Porsche, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in RH. Furthermore, accounts one or more contributors advise on may also have a position in RH. This may change without notice.