RH Business History

Speedwell Research: Business History

This is an excerpt from our RH research report, which goes over RH’s early history. It is just the beginning (~10 pages) of our ~21k word deep dive (80+ pages). We hope you enjoy it! Get the full RH report, among others, by becoming a Speedwell member today!

We also released a podcast episode just on RH, which you can find here: Apple, Spotify

Please email us at info@speedwellresearch.com for any questions, concerns, or comments. See our full disclaimer on our website.

Founding History.

Stumbling Upon a New Store Concept.

In 1952, in a small town nestled between Lake Champlain and the Adirondack Mountains in Northern New York, Stephen Gordon was born. His family ran three stores in the city, but his parents pushed him to be an educated professional. In 1978 he graduated with a Masters in counseling psychology. He and his wife moved to Eureka, California, and after a short stint as an inattentive therapist, he decided he needed to do something more involved. He started working as a carpenter and bar tended at nights.

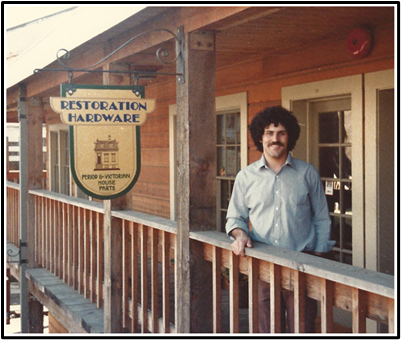

A year later, in 1979, he bought a decrepit 3-story Victorian with the intention of restoring it. However, he had trouble finding hardware, moldings, and other fittings that he needed to complete his project. Gordon worked hard to scavenge for vendors that sold these products and realized others must have the same problem. Given his limited budget, he often couldn’t even buy the items when he found them, so he got creative.

In an effort that epitomizes “minimal viable product”, he simply put together a binder of photo-copied images that came from various vendors he found and scratched in prices that were double what the vendors charged. When he made a sale, he then used his small profits to buy the item that he needed. His entire marketing campaign consisted of putting a sign out on his porch that said “Restoration Hardware”. A new store concept was born.

Business History.

Early Struggles.

After 6 months of operating out of his home, he saved up enough to rent a 300 square foot space in Old Town Eureka. But with money tight, he kept bartending at night. His first store was successful enough to justify keeping it going, but not profitable enough to be comfortable. About five years after starting the store, he still had cash flow problems around the holidays, and in one instance even needed to borrow $200k from his in-laws to finance inventory. Their core hardware offerings and an ever-growing mix of eclectic products, from goatskin gloves to English coal miner lanterns, helped the store get on stable enough footing that they could justify expanding. They proceeded to open their next two stores in Newport Beach and Marin County.

In 1994, with five stores and $4.2mn in revenues, Restoration Hardware raised their first round of outside money—$2.5mn from Cardinal Investment. They continued to expand their product offerings and entered the furniture category, where they focused on offering high-quality craftsmanship and sturdy, American-made furniture.

Gordon’s product philosophy was simply to sell things that he liked and thought were cool. Many of the items he picked had a nostalgic “back to a simpler time” vibe with boot scrapers, antique candle sticks, and vintage metal lighters presented alongside oak chests. A lot of their products were idiosyncratic, including items like Dragonfly doorknockers and aluminum Canadian lunch boxes.

Further adding to the store’s personality, he would start narrating products with curatorial labels. For $2.75, you could buy the “My Own Quirky Summer Memories Sandwich Spreader”, which had a similarly quirky description: “I remember a particular sandwich spreader from my summer sandwich-making noon times on a lake-front house on Indian Bay in upstate New York. Being the weird and wonderful or whatever guy I am I always thought this spreader was such a classy way to put mayo on that absurdly squishy white bread”. And for $39, there was a miniature Allagash River Canoe: “There are few memories as dear to me as those associated with my week-long canoe trip on the Allagash River in Maine. Our small-scale replica is beautifully executed and true to form. Ply the rivers of your mind”.

The varied assortment of whimsical, yet vaguely wistful items garnered a lot of curious consumers who could usually be coaxed into an impulsive purchase. The model seemed to be working, and after hiring more experienced managers including executives from Pier 1 Imports and Home Express as COO and CFO, they doubled their store count every year for the next 3 years and ended 1997 with 41 stores.

Total revenues approached ~$97mn in 1997 (prior to including an acquisition of Michaels Furniture Company, one of their larger furniture vendors), which comes out to ~$400 sales per square foot or about $2.4mn per store. Despite decent revenue generation, they were operating at just a ~3% EBIT margin at peak. Nevertheless, investors were starting to focus more on their growth: Restoration Hardware was slated to open 25 stores in 1998 and 30 in 1999. With strong store growth that excited investors and a buoyant stock market, Restoration Hardware looked to raise public funds for their expansion.

On June 19th, 1998, Restoration Hardware went public under the ticker RSTO, raising ~$60mn. Their shares were priced at the higher end of the banker’s range, at $19, and jumped +38% on the first day of trading. Investors and analysts at the time were very enthusiastic about Restoration’s model, with a portfolio manager noting that Restoration Hardware had developed a really “superb way of presenting home furnishings and gifts”. Investors thought that the product assortment was unique and promoted an American lifestyle that harkened back to simpler and safer times, with Gordon-created stories allowing them to charge higher prices.

Their retail model heavily depended on piquing consumers’ interest to drive foot traffic in hopes they’d make an impulsive purchase of something they’d never seen before or would see again. They noted that “discovery items and other products are cross merchandised within these core groupings to allow for surprising product combination and to increase impulse buying”. However, there was little they sold that a consumer needed, and it seemed that solving boredom through novelty was its core function.

While their hardware and furniture offerings may have been of high quality, the customers who could be drawn to such items would be turned off by the “Moon Pies”, “Atomic Robot Man” toy, and “Acme Dog Biscuit Mix” that adorned the pieces. As they proudly noted at the time of IPO, “each item must stand on its own and is evaluated on its own merits. The company does not have prescribed price points and finds it equally justifiable, for a merchandising point of view, to offer a vintage, Austrian wind-proof lighter at $5 and a solid, red oak Mule Chest at $1,990”.

In 1998 they would eke out a small profit of $3.8mn on $211mn in sales in what was becoming an increasingly seasonal business: their only profitable quarter was 4Q—driven largely by holiday gifts. What seemed like a creative way of drawing foot traffic started to be seen as a liability that drove brand confusion and a convoluted consumer value prop.

The novelty of the stores seemed to be wearing off, and in 1999, same store sales (SSS) were just +0.8%, down from +12% and +11% the two years prior. Despite sales per square foot increasing to almost $600, they struggled to make a profit and regularly relied on promotions to push immovable inventory. The furniture they did end up selling garnered too low of a margin, since >80% of products they purchased were from domestic importers (middlemen).

Compounding their issues was their store unit growth, which was described in their 1998 10k as an “aggressive growth strategy”. With cash flow from operations insufficient to open the 30 stores a year they planned on; Restoration Hardware increased their borrowings after their IPO proceeds ran out. In 1999, cash from operations was just $4mn, as their working capital needs to finance inventory consumed most of their cash. Still, they pushed ahead, spending $46mn in capex, which was financed by a revolving line of credit and their remaining cash on hand, which dwindled to just $4.6mn at the end of 1999 (technically, their fiscal year ended one month after the end of the year). After making a small profit in 1998, they were back in the red, losing $3mn on almost $300mn in sales in 1999.

The following year, they added 13 more stores despite same store sales turning negative -1%. Cash from operations improved after reducing inventory on hand (with promotions) to $19mn, but with $23mn of capex, their cash balance fell again. Ending 2000 with just $2.6mn in cash and a quick ratio of 0.33, things were not looking good for the unprofitable retailer with growing debt obligations. The stock traded under $1 per share, down ~95% from its peak; bankruptcy was looking like an ever more real possibility.

Enter Gary Friedman.

Gary Friedman.

Gary Friedman was born in San Francisco in 1957. When he was just five years old, his father passed away, leaving him and his mentally ill mother to fend for themselves. In his mom’s best year, she would make only $5,000 to support them. Food stamps and evictions characterized his childhood, with Gary living in a string of small apartments, none of which they could afford to furnish. He struggled in school with reading “going in one ear and out the other”. However, what he lacked in auditory ability, he made up for in intuition and visual capacity—skills that wouldn’t be apparent until he worked at The Gap.

He started at The Gap as a stock boy folding clothes part-time while attending community college. However, with a D average after his first year, and at the “encouragement” of a professor who told him he was “wasting taxpayer money”, he dropped out. Now fully devoted to The Gap, his work ethic helped him get promoted to store manager. During his days off, he would hang around The Gap’s corporate headquarters to help out, usually folding clothes at “Store One”, which was where they would present the next season’s clothing.

One day, the new President of The Gap, Mickey Drexler, called an all hands meeting in the lunchroom. Drexler went out to espouse the ethos that The Gap would follow going forward, and started asking the audience questions. As Gary would later recollect, a spirit moved him and a rush jolted his body with his hand shooting up as he blurted out an answer. Drexler responded, “That’s right. That’s exactly what we should be doing”, and he asked Gary what corporate department he worked in. Gary responded, “I don’t work here. I am the manager of the Market Street store, and I am here on my days off just to kind of help out”.

Drexler must have been impressed, because the next day, Gary got a request from Mickey Drexler’s secretary to join a meeting at the headquarters with all of The Gap’s top executives. Drexler tasked the 21-year-old Gary to tell them what was happening in this “effing” company. (Drexler would refer to Gary as “effing Friedman”). Gary’s career accelerated, and he was soon promoted to district manager, then regional manager, and oversaw 63 stores.

He felt loyal to The Gap, but an up-and-coming retailer, William-Sonoma, wanted to interview him. To his surprise, the job was for a much bigger position than he had: Senior VP of Stores and Operations. He couldn’t pass it up. Just like at The Gap, he would steadily move up the ranks, first to Executive Senior VP, then President of the Williams-Sonoma and Pottery Barn brands, then Chief Merchandise Officer, then, lastly, President and COO.

While at Williams-Sonoma, he was known for transforming Pottery Barn from a $50mn tabletop and accessory business into a $1bn+ home furnishing brand. He took the lead on introducing “Grande Cuisine” stores at Williams-Sonoma, which included demonstration kitchens, tasting bars, and a food hall of the company’s private label food products, helping drive the brand from $100mn to ~$1bn. He also helped develop the West Elm brand, an in-house-designed furniture and home furnishings brand.

However, Gary was shocked when he was passed over for the CEO job in favor of an external hire, a position he later alleged that Howard Lester (the then-CEO) had promised him for years. Gary remembers Lester saying, “now don’t do anything emotional. You’ve got $50 million in stock options you can’t walk away from”. Right after that conversation, he roamed the streets of San Francisco on a foggy night and saw the glow from a billboard that had plastered on it “He who dies with the most toys is still dead”. He made up his mind to leave the money and move on to the next challenge.

At that time, Stephen Gordon had been in contact with him about potentially taking over his job as CEO to try to turn around the dying Restoration Hardware. After triggering a debt covenant, Restoration Hardware could be pushed into default at any moment. In March of 2001, after 14 years at Williams-Sonoma, Friedman resigned and took over the reins of Restoration Hardware, a company with its stock at an all-time low and teetering on the verge of bankruptcy.

The Turnaround.

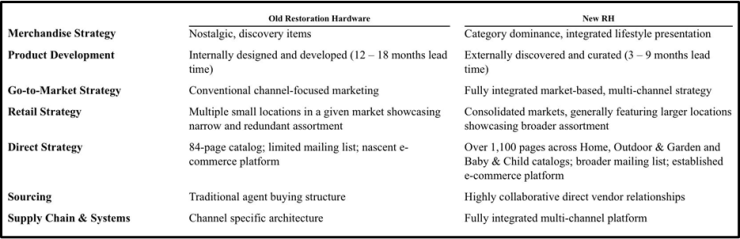

Friedman raised $15mn, $4.5mn of it his own money, to infuse into Restoration Hardware and stave off imminent bankruptcy. Gary’s immediate prognosis of the business: poor merchandising. These so called “discovery items”, that, by design, included the most random selection of products conceivable, may have driven some foot traffic and low ASP sales, but led to cluttered stores, continual discounting of unsold SKUs, and brand confusion.

He would set about curtailing these items that then-represented 50% of their business and cutting the most offensive items, like an “Aqua Troll” sprinkler, that were carried because they were “funny”. However, discovery items were not eliminated outright. In the quote below, we see that they still relied on them, at least initially, to drive traffic, and the pruning process would take years (in 2Q06, he added a gift assortment back into the store after having removed it, and rolled out a separate Restoration Hardware Gifts catalog).

More surprisingly, bringing the furniture mix as a % of sales down was also a part of the plan. Their furniture was 32% of sales in 2002, with margins too low to provide sufficient unit profitability to rationalize the overhead. At that time, they were only importing 18% of their products directly from foreign vendors, purchasing instead from importers who had added a layer of mark-ups. While Restoration Hardware worked on developing direct supplier relationships, they tried to curb furniture sales by emphasizing other higher-margin categories like textiles.

Textiles were just 3-4% of the business by revenue when Gary took over, but in ~2 years they surpassed his goal of having it reach 20% of total revenues. The higher-margin textiles helped support the company while he turned the business around. He would also deliver on doubling the bath business over the same period.

These changes brought Restoration Hardware back from the brink of bankruptcy to achieving their first annual profit in 2004, six years after going public. Gary would later say, “It was not a turnaround, because Restoration Hardware never worked. They went public in 1998, and never made money. It didn’t carry enough of anything to stand for anything”.

With the business starting to gain solid footing, Gary Friedman started to talk more about the Restoration Hardware concept and what he envisioned for it. They would focus on being a “home lifestyle brand, above the current lifestyle retailers and below the interior design trade”. He set long-term goals of making Restoration a $1bn+ brand with mid-single digit operating margins.

It would be a long journey to rehabilitate the brand and move up-market though. Friedman likes to note that the mall is a “graveyard of short-lived ideas” and that the only way for Restoration to avoid that fate is to build a core business that is strong, sustainable, and offers the customer a predictable promise.

Before signing off the 4Q03 earnings call, he remarked: “So we are all here for the long-term. I spent 11 years at The Gap and then 14 years at Williams-Sonoma. This is going to be my last stop. So, I will be here for a long time, and this will become a really great company long-term. That’s all our hopes and goals”.

However, their profitability was short-lived. In 2005, they lost $29mn, which they attributed to the housing slump. They paused new store openings, which would have been the first store growth since Gary joined Restoration Hardware (note Friedman’s quick response to business shortcomings versus Gordon’s). With the stock tanking from $9 to $3, private equity firms took interest. Catterton Partners, along with Gary Friedman, made a $267mn buyout offer which represented a 150% premium. Before the deal closed, however, Sears took a 13.7% stake in the company and tried to counter with a 5 cent higher offer. However, as the 2008 financial crisis took hold, and Restoration’s performance continued to soften, Catterton Partners was the only interested party, and they lowered their acquisition bid to $179mn.

After a brief respite with the business somewhat working, Restoration Hardware was taken private again to fix the model. After being public for a decade, they had only turned a profit once.

Restoration Hardware Reintroduced.

Despite the macro turmoil, Friedman remained steadfast in his mission to make Restoration Hardware a more upscale lifestyle brand. In the heat of the recession, with consumer discretionary spending plummeting, Friedman would raise prices and finally put an end to the cheap discovery items. Whereas in 1998 Restoration Hardware targeted customers with $75,000 in household income, they would now target those with over $200,000. To distinguish themselves from their earlier history, Restoration Hardware would no longer go by Restoration Hardware – from then on, they would just be “RH”. (That said, some stores still carry the full name).

During this time, they established direct relationships with their suppliers, which helped them not only avoid the middleman mark-up and have better visibility into their supply chain, but also let them work with manufacturers to scale up volumes as needed (which was hard as many were small family-run businesses). In contrast to other furniture retailers and specialty chains, they didn’t design their own products, but rather sought after already-in-production, high-quality, artful pieces. They considered themselves a “curator” in this role, stocking their stores with items they liked. The direct supplier relationship was necessary to scale up their orders, as many of these manufacturers were small firms with neither the capital nor expertise to sell to a large retailer.

Supporting this sourcing and curation capability is their Restoration Hardware Center of Innovation & Product Leadership that sits in their headquarters at Corte Mande, California. This cross-functional department works to develop a product assortment with their manufacturing partners, who RH considers an extension of the product development team. This allows RH to have an ability to direct the product designs while still benefiting from their “artisan partners’” ideas and leaving the actual manufacturing to them.

In 2010, RH hired Carlos Alberini as co-CEO alongside Gary Freidman, tasking him with operations, finance, supply chain, inventory, information technology, and HR, while Gary would focus on the creative functions, merchandising, and marketing. As it was a private company at the time, not much is known about this decision. However, it’s possible that as the company’s revenues contracted during the financial crisis, the PE owners wanted to bring on another, more experienced manager with prior finance experience as a CFO.

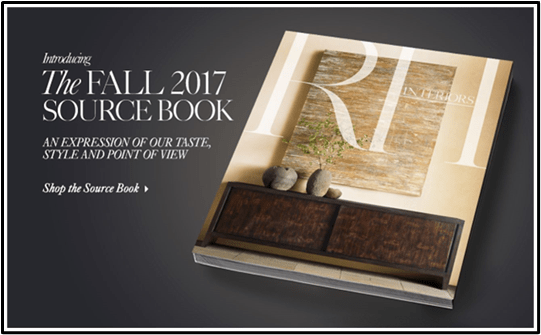

Instead of printing <100-page catalogs of their products, they compiled multi-hundred page “Source Books” that they circulated to prospective consumers. Whereas they used to send monthly mailers to capture impulse purchases and display a seasonal product assortment, they now send 1-2 books a year, which can get up to 1,000 pages. (They would continue to iterate on Source Book length and shipping frequency, and ultimately split it between different product lines, but their books continue to be in the hundreds of pages). These glossy Source Books would become a key pillar of their “direct” business, which expands their reach beyond their store footprint. The Source Books both solicit orders and serve as an advertising tool that draws foot traffic to their stores.

The multi-channel approach was synergistic, and their product catalogs continued to grow every year, incorporating an ever-growing selection of goods. Their footprint, however, had remained stagnant, meaning only a small portion of products could be displayed in-store. If you included their newly launched Baby & Child line, fewer than 10% of their product assortment was on display. This presented both a problem and an opportunity, as SKUs with retail space tended to get a 50-150% lift in sales.

To address this, they started opening up larger stores in 2011 and introduced the “Gallery” concept. No longer would their stores be sandwiched between other retailers in a mall, these stand-alone “full line” Design Galleries would be 3x the size at 21,500 square feet. The first two full line Design Galleries were rolled out in Houston and Los Angeles.

In their 2012 S1, they noted that their Los Angeles Design Gallery…

This concludes the free excerpt of our report. In the full report, we continue the Business History with their store model upgrade and go over specific challenges RH had to overcome. Afterwards, we move into their Business, the RH Model (both its creation and the value network), as well as the industry, their real estate model, and much more!

See below for the full table of contents, and subscribe to get access to the full >80 page RH research report in PDF! Members can also access our Constellation Software, Floor and Decor, Meta, Copart, and Walker Dunlop reports, as well as the DJY Research archives.

Table of Contents

Founding History.

Stumbling Upon a New Store Concept.

Business History.

Early Struggles.

Gary Friedman.

The Turnaround.

Restoration Hardware Reintroduced.

Growing Pains.

Business.

The RH Model.

Creating the RH Model.

The RH Value Network.

Industry.

Competition.

Players.

The Consumer’s Hierarchy of Preferences.

Peer Metrics.

Real Estate Model.

ROIC and Cash Flow.

Expanding RH.

Geographic Expansion.

Vertical Expansion.

Brand Expansion.

Beyond RH.

Valuation.

Summary Model.

Model Summary.

Historical Financials.

Risks.

Conclusions.

To read the full report, you can subscribe (or purchase an individual copy of the report) here:

Or if you’re not quite ready to read the full report, drop your email below for free updates. For more free RH content, see Drew’s appearance on Colossus’ Business Breakdowns discussing the company or check out our RH episode on our podcast (Apple, Spotify).