10 Lessons from Copart's 40 Years in Business: Learning from Willis Johnson & Jay Adair

$29mn Failed ERP System, Levered Recap, Cleaning Wrecked Cars, Holding Vacant Land, and Withdrawing from International Markets

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

There is a podcast of this memo available if you prefer listening to it. You can find it on our podcast feed here (Apple, Spotify).

We also have a 2 hour Company Podcast Episode just on Copart, linked here: Apple, Spotify.

Background.

Copart is a global provider of online auctions for mostly salvaged vehicles. A salvaged vehicle is a car that has been damaged beyond the point that it makes sense to repair it. Copart mostly works with the insurance company to pick up salvaged vehicles and help them sell the vehicles on their Copart platform. Copart was founded by Willis Johnson in 1982 and was later joined his son-in-law, Jay Adair. Both have proven to be savvy operators with an intuitive business sense. Copart has grown from a single junkyard in California to a global business with a market cap of over $45bn. Together they have been the main leaders throughout Copart’s history and are whose decisions we will be focusing on.

Below are the 10 Lessons we will be elaborating more on in the rest of this memo.

10 Lessons

Don’t Postpone Addressing Core Systems Issues, Running Multiple Systems has a Cost.

Plan for the Future Well in Advance, Act Like a Long-Term Owner.

Align Incentives with All Parties and Share Economic Gains.

Demonstrate Your Value.

Maintaining a Conservative Balance Sheet Allows You to be Opportunistically Aggressive.

Experiment… but if Something Doesn’t Work, Don’t Fix It. Drop It.

Expand Carefully and Deliberately.

Don’t Fall Prey to The Sunk Cost Fallacy.

The Better Your Service and Treatment of Customers, The More They Will Do Your Marketing.

Know Your Job.

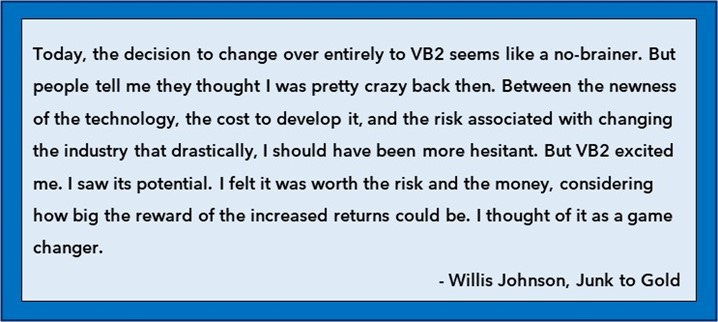

1) Don’t Postpone Addressing Core Systems Issues, Running Multiple Systems Has a Cost.

From our Copart Report:

In the late 90s, Jay started hearing about “.coms”. At first, he thought they could list their cars online to limit the paper they were wasting—it took over 8,000 sheets of paper to circulate the weekly auction list of cars.

But then he realized that they could use the internet to help solve one of their largest pain points: buyers were hiring people to bid on their behalf at the car auctions, paying them $150 every time they won a car. He thought it was silly that people could make $2-3k a day just standing around and raising a paddle. This was a prime use case for the internet to serve—buyers could come the day before and view the cars, then place a bid online for $35 instead of paying a contractor to stand in the live auction. Jay was right. Copart’s online platform generated $1mn in sales the first quarter it launched.

There was a problem with this system though: bids were not being placed live during the auction, only prior. So they moved to mesh online bidding with the live auction by connecting a row of computers manned by employees to the internet. This was called Virtual Bidding 1, or VB1.

While it generally worked and was showing financial success, it created operational havoc. Employees were limited to monitoring the screens for just 60 minutes at a time because any longer would cause their error rates to skyrocket, and they wouldn’t try to adapt VB1 to their largest yard for fear that the size would lead to lost bids.

The problem was compounded by the fact that VB1 was hurting live auction attendance, making it a worse in-person experience. Supporting both online and live was an optimization of mediocrity.

Instead of letting indecision run and supporting these two parallel systems, they decided to eliminate live auctions entirely. Looking back it may seem that this was clearly the right decision, but their largest competitor, IAA, wouldn’t make the same decision until Covid forced their hand in 2020. Copart made this decision in 2003, seventeen years prior.

2) Plan for the Future Well in Advance, Act Like a Long-Term Owner.

Copart always had a policy of owning the land they operated on when possible. When they acquired a yard, they also negotiated to acquire the land, or at the very least lease it with an option to buy. Even if land they didn’t need, but might be able to use in the future, came up for sale, they would buy it.

Copart was of the opinion that land in a good location was absolutely key for their business, so not only did they want to control a lot of land, they insisted on owning it. In contrast, IAA, partially influenced by a chorus of Wall Street analysts, preferred to lease. In the short term, this meant that IAA could grow more quickly since instead of “tying up” capital in the land, they could use it to acquire more lots. For a while, this made IAA look like it had a stronger return on invested capital, while growing at a faster rate (this is before ASC 842 lease accounting standards were adopted, requiring operating leases to show up on the balance sheet).

As time passed though, these leases would come up for renegotiation and IAA was put in a very awkward position. Their entire business would stop functioning without these scarce lots of lands, which were hard to replace since they required special licenses while also being close densely populated areas—and the of course the landowners knew that. IAA could expect the landholder to ritually test the limits of how much value they could squeeze IAA for on each lease negotiation.

In contrast, Copart thought like business owners (in no small part because Willis Johnson and his son-in-law had significant ownership) and wanted to own all their land. Not only did it seem like poor strategic planning to them to not own this key asset, they also thought it would be a bad financial decision as this land would be in much higher demand in the future than currently. In fact, even once they bought a yard, they would buy land nearby for potential future expansion.

Whereas IAA’s strategy may have initially juiced their ROIC, today we estimate that IAA would have a 50% higher ROIC if they owned their land. And Copart doesn’t have a 3rd party that can periodically threaten the continuation of their local business.

3) Align Incentives with All Parties and Share Economic Gains.

From our Copart report, which covers one of the big early changes to the business model Willis Johnson made:

The biggest business transformation was a change in the incentives and economics of the auction business. Just as cleaning the car parts he sold increased the price he could command, doing the same for his salvaged cars yielded a similar result. He wanted to make the cars look nicer, but knew the insurance companies would be reluctant to spend money on this. So instead, he thought, what if there was a way to split the increase in price from making the cars look nicer?

At the time, it might cost about $200 to pick up, store, and auction off a car. Willis wanted to instead incur that cost, plus the cost of cleaning up the car, in exchange for a percentage of the proceeds once the car sold: 20% for old and highly damaged cars and 10% for everything else. The result was that both the insurance companies and Copart generated higher proceeds.

This arrangement, which Willis called the Percentage Incentive Program, or PIP, also solved another issue insurance companies had. A burned-out car may have fetched only $25 in an auction, but cost that same $200 for Copart to pick up and process. The insurance companies were losing money on each of those units. Under PIP, Copart instead would be the one to lose out on that car by incurring expenses less than their portion of proceeds. The kicker is that Copart would only offer PIP if an insurance company contracted out all of their cars in a region to Copart. So Copart would lose on a fire-damaged vehicle, but make it back on a lightly damaged, newer car. Economics aside, Willis liked how he was now aligned with his customers: they both wanted the highest price for the cars, whereas before his revenues only increased with volume.

Once insurers were introduced to the PIP model, they vastly preferred it and pushed other competitors to follow suit. Willis, though, simply started with the idea that cleaned up cars would fetch more at auction and worked on how to make that happen. He even accepted that he would lose money on some units as a byproduct of his PIP model.

When Copart entered the UK, they tried to roll out PIP but the insurers were unfamiliar with it. So Copart started buying cars directly from the insurance companies, cleaned them up, and sold them for more. Despite the fact that they actually made more money doing this, they shared their data with UK insurers to show them why they should join PIP. Instead of taking all of that sale price increase from the cleaned-up car, they gave the majority of it back to UK insurers. Copart’s always tried to act fairly with its partners and aligning incentives is an important aspect of that.

4) Demonstrate Your Value.

When Copart rolled out PIP, they instantly saw that the cleaned salvaged vehicles, despite being heavily damaged, still sold at higher prices than uncleaned cars. When they had enough data collected to prove this, they would go to each insurance carrier and show them why they were better than the competition. Their early pioneering of PIP, in addition to aggressively pursuing insurance companies, meant that by 2004 Copart had 65% of their vehicles sold on PIP, whereas IAA was at less than half, with 28%.

Additionally, when Copart pioneered online auctions, they were also quick to put the data in front of insurers that proved vehicles sold with online bidders garnered higher ending auction prices.

Copart showing how they can generate higher returns1 versus the competition was part of how they moved from a small player in a fragmented industry to dominating it.

5) Maintaining a Conservative Balance Sheet Allows You to be Opportunistically Aggressive.

Copart never repurchased shares for almost a quarter of a century as a public company. There are two broad reasons for this. The first is that they were focused on rolling up the industry to become a national player which they (rightly) thought was necessary to be competitive in the long-term. The second is because Willis Johnson had always been cash-strapped with prior business ventures and as a result wanted a very conservative balance sheet. However, he was eventually convinced of the business’ resiliency and started to put excess cash to repurchases around 2007. Whereas in 2005 they had almost a year’s worth of expenses covered by cash on hand, by 2008 that figure dropped to just 3 weeks.

From our Copart Report:

When the financial crisis hit, with the country’s largest automakers going bankrupt and the whole sector requiring relief, they paused their repurchases to build up their cash reserves out of caution. However, once they observed their business continuing to operate with little hiccups, they positioned themselves to take advantage of the low valuation the market was giving them (a ~mid-teens multiple of owner earnings at the time with consistent double-digit growth).

In 2011, they not only launched a tender offer for shares, but issued their first debt ever for $400mn to help fund their largest buyback, one that shrunk the company’s share count ~20%. After concluding that tender offer, they continued to buy more shares. Within a two-year period, they repurchased over 25% of the company for a share price that is ~10x lower than it currently trades (that comes out to a ~25% annual return on those repurchases).

Since then, they have executed a few other large share repurchases, including another tender offer in 2016. They wouldn’t have been able to be so aggressive unless they had conservatively managed their balance sheet prior. They never set an annual share buyback target, but rather just let the cash build high and got aggressive when the market turned.

6) Experiment… but if Something Doesn’t Work, Don’t Fix It. Drop It.

While most people might not think of junkyards as being innovative, Copart was selling cars online before most people even had access to the internet. They weren’t pioneering an “ecommerce strategy” in response to some industry-wide headwind—they literally led the way with virtual bidding. It was a bit of a gamble though. It wasn’t impossible to think that people purchasing vehicles would want to see the cars in person before bidding. In fact, the real oddity is that people would bid on cars sight unseen (remember VB1 started without even photos and would later then only include a handful of low-quality ones).

While Virtual Bidding turned out to be a tremendous success, other initiatives weren’t. They bought Motor Auction Groups in 1998, an auction house focused on selling undamaged cars to consumers, much like CarGurus or Carvana minus the delivery. They grew it to six locations, before deciding that the returns weren’t there and competitive moats of that business weren’t as good.

Many years later, they would make another big bet with international operations. While most were eventually successful, they notably had trouble with India once they learned more about that market. Rather than stay and throw money at making their business work for a country that didn’t suit their current model, they left. When you try something, you gain information. Copart has shown to be great at using that incremental information to decide whether to keep at it or do something else.

7) Expand Carefully and Deliberately.

In 2007, Copart entered the UK market through the acquisition of Universal Salvage. As mentioned, the UK market still operated on a “merchant” model where the Salvage operator bought the car directly from the insurer. Copart was patient and accumulated years of data on the merchant model before they successfully convinced the insurer to convert to the PIP model. This, though, was nothing compared to Germany.

In short, in Germany, after an accident, instead of the insurance company taking away a vehicle, the consumer is left with it and the insurer just cuts a check. That means the consumer is stuck trying to sell the vehicle themself while the salvaged vehicle carcass sits out in their driveway. The consumer usually relies on a variety of salvaged vehicle marketplaces to sell the car, which is also how the insurance company typically assesses the value of the car.

Copart played the long game in Germany. In 2012, they acquired WOM, Wreck Online Marketing, which gave them their first foothold into the salvaged vehicle value chain. They could use their marketplace to run tests purchasing vehicles directly from consumers and selling them on the Copart Global Platform to gauge returns. In 2016, after circumventing the myriad of European laws, they opened their first Copart yard. Their first yard, together with the data from tests on WOM, allowed them to approach insurers and show how their model not only is more profitable for the insurer, but also vastly preferred by the consumer (no one wants to deal with a multi-weeklong process of selling a salvaged car after being in an accident). And more recently, in 3Q22, they noted they were selling on consignment basis for the majority of the top 10 carriers in Germany, a full decade later.

8) Don’t Fall Prey to The Sunk Cost Fallacy.

When Copart sunk $29 million into an ERP system that turned out to not be the right tool, they didn’t try to use a subpar tool for a few years in order to rationalize some of the cost. Instead, they just wrote off the amount and fired SAP.

It is very hard to picture the average corporate manager making a similar decision. More likely, they would try to explain why the wrong software system was really good or spend even more trying to make it work.

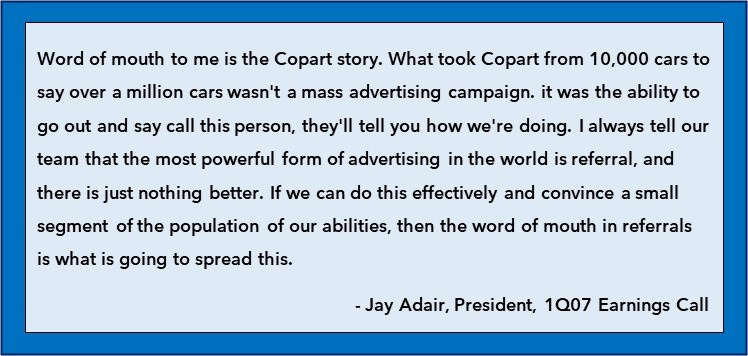

9) The Better Your Service and Treatment of Customers, The More They Will Do Your Marketing.

Here’s a quote from Jay Adair, making this point:

Copart, though, always focused on treating their customers the best they could, so these customers would always have good things to say. During Hurricane Katrina, which left over 300,000 vehicles in salvage condition, Copart built a reputation of going out of their way to work for their customers: they hired almost 300 extra sub-haulers, they spent millions buying new equipment when it couldn’t be leased, and they shipped in employees to work around the clock. They incurred a significant amount of extra cost that they never passed off to the consumer. As Jay Adair noted in their 4Q05 earnings call, “Our primary purpose right now is getting the cars in as quick as we can, servicing the major carriers. And will we make a profit on this? Probably not.”

Here again Copart acts in a way that not only would they be proud of their customers knowing about, but their customers would be quick to tell others about.

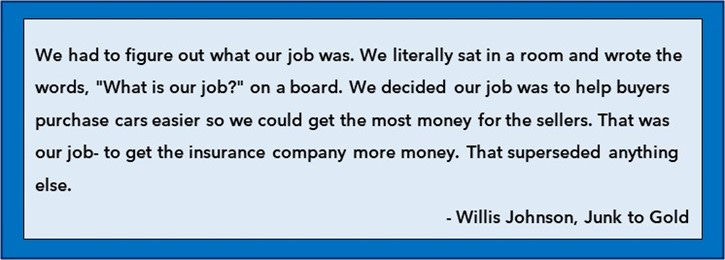

10) Know Your Job.

This isn’t just Clay Christensen-speak—in fact it seems unlikely Willis Johnson would have heard of him or his business lectures. But this is a very important and elucidating question. Asking this question gives a business a lot of clarity on its purpose and where it needs to focus.

We will let Willis Johnson have the last word.

We will be releasing a new memo every Friday morning. Subscribe below to receive it!

Want more Copart Content?

Podcast

Check out our podcast, The Synopsis. We have a 2 hour Company Podcast Episode that covers all aspects of Copart! (Links: Apple, Spotify.)

Extensive Research Report

You can get access to our full Copart Report by either becoming a Speedwell Member, which grants you access to all of our Research, or by buying an individual report. Click here for more info.

Many members have gotten their memberships expensed. If you need us to talk to your compliance department to become an approved research vendor, please reach out at info@speedwellresearch.com

You can read more about our Copart Report and see the Table of Contents here.

“Return” is a technical term that means the sales proceeds as a % of average cash value or pre-accident value. For example, if a car is worth $10k before an accident and Copart sells it for $3k, then that is a return of 30%.

Great piece thank you. Management is key in my view and this family are quite extraordinary. Your observations and snippets are invaluable to getta view