Adobe Business History

From a Garage Start-Up to Industry Standard

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

In the future we will release a Company podcast episode that covers all things Adobe, so make sure to follow The Synopsis Podcast! (Apple, Spotify).

Founding History.

In the early 1980s, two Xerox employees, John Warnock and Charles Geschke, noticed common nuisances when printing a document. Since most graphics and fonts were created with “bitmaps” at the time, if you enlarged them to print the product, it looked “jagged” and “blocky”. However, most of the time a user couldn’t even print the low resolution document because each printer had a proprietary language.

Initially, John and Charles solved this problem with a new language called Interpress that they created at Xerox. This language could have created a universal standard, however in classic innovator dilemma fashion, Xerox worried that propagating this language would threaten their core printer business by making it easier for enterprises to swap out their expensive printers for alternatives. Instead, they just used it as a new internal standard. While Xerox wasn’t wrong to worry about universal communication protocols threatening their hardware business, they were wrong to think they could prevent it.

Seeing that this technology was just going to sit, John and Charles quit Xerox and decided to start a business that could take advantage of this technology. Adobe was founded in December 1982, named after the creek behind their first offices—John Warnock’s garage.

Business History.

They would rewrite code and then buy or build a bunch of printers that would support a high end printing service. Their software was called PostScript and some advisors pushed them to create a software business instead of a service.

The ease of use and massive improvement in printer quality got the attention of non other than Steve Jobs who tried to buy them outright for $5mn. Instead, they settled on selling 19% of Adobe to Apple in 1985 and Apple’s LaserWriter printer became the first to use PostScript, launching the “desktop publishing” industry. While this printer was still pricey at $7k a pop, that was still a step-function cheaper than Xerox’s $500k set-up.

In 1986 Adobe IPO’ed at a ~$100mn valuation with $16mn in revenues. This would jump to $39mn in 1987. The same year they took their first step into the retail software market with Adobe Illustrator. This was followed by an acquisition of software that would turn into Photoshop in 1990. By year end 1990 they had over 1,300 employees and $300mn in revenues for an incredible 4-year revenue CAGR of 109%.

In 1993, Adobe introduced the Portable Document Format (PDF), a technology designed to solve a persistent and costly problem in digital communication: document inconsistency across devices. At its core, the PDF ensured that a file would appear exactly the same regardless of operating system, software, or hardware. Initially, adoption was slow. Creation tools required payment, and network effects had not yet materialized. However, Adobe made a critical strategic decision to distribute the Acrobat Reader for free. Over time, this choice proved decisive, as it allowed PDF to spread organically across businesses, governments, and eventually consumer workflows.

As adoption expanded, the PDF gradually became the default standard for formal documentation. By the late 1990s and early 2000s, it was widely used for legal documents, technical manuals, financial reports, and government forms. Eventually, in 2008, it was formalized as an ISO international standard, cementing its role as infrastructure rather than just software.

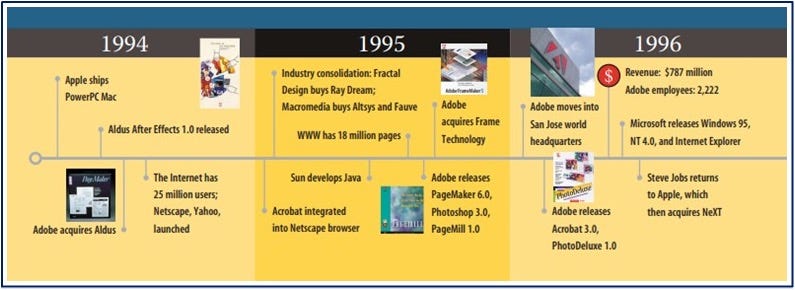

In 1994 they merged with Aldus Corporation, the creator of “PageMaker”, creating the 5th largest personal software company. Aldus helped launch the publishing revolution, alongside Apple and Adobe, and their PageMaker app was the key application that users used to create layouts for printing. However, they struggled with profits that were 90% less than Adobe, despite revenues that were only 1/3rd smaller.

While Aldus’s flagship product PageMaker had already lost market share to QuarkXPress, the acquisition included an internal project—code-named K2—that would eventually evolve into InDesign. After several years of development, InDesign was released in 1999 and quickly became the new standard for professional publishing. Crucially, it was designed to integrate seamlessly with Photoshop and Illustrator, creating a unified ecosystem rather than a collection of standalone tools, which would be the seed for the creation of Creative Suite (CS) in the coming years.

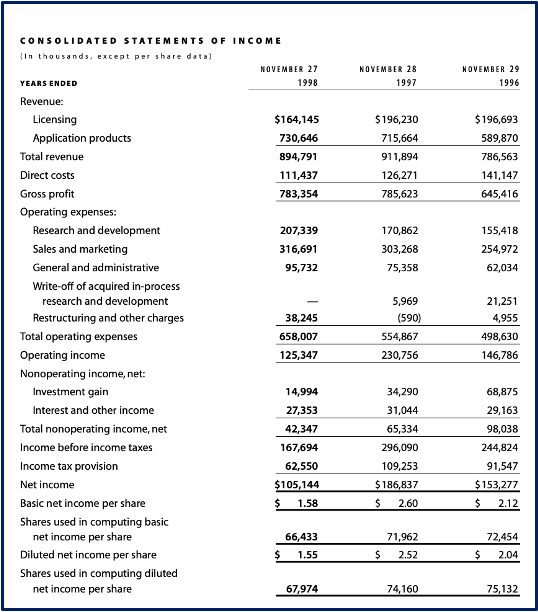

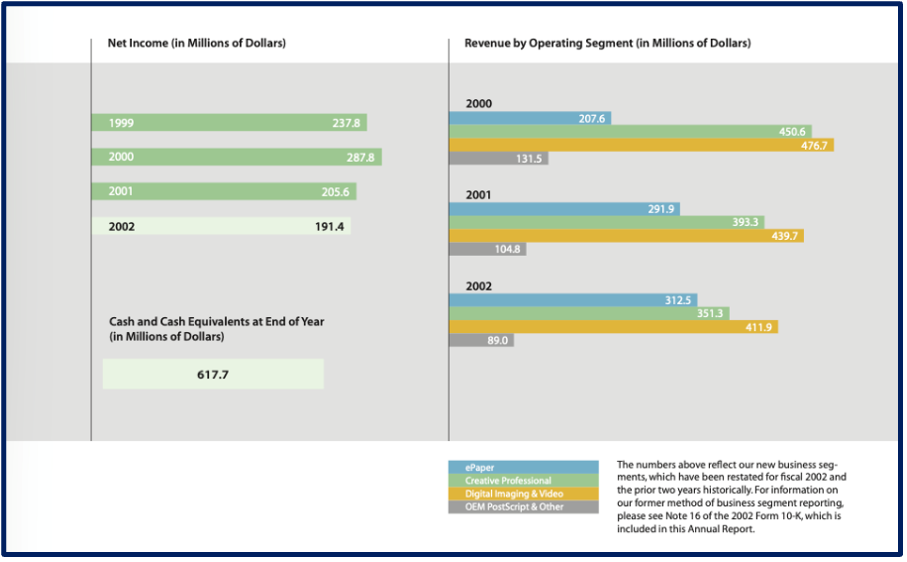

By 1997 almost 80% of Adobe’s revenues came from application sales. In 1997, Hewlett-Packard (HP) decided to stop licensing Adobe’s PostScript when it developed its own clone version of the software. By 1998, Adobe was feeling the effects of HP’s decision and their licensing sales suffered as a result. In addition, due to the Asian Financial Crisis, sales in Japan, one of Adobe’s stronger markets, fell 40%. The next quarter, they reported revenue of $101mn, which was down from $179mn a year ago. In an effort to streamline profitability and balance declining sales, they announced a major restructuring that would eliminate 12% of their workforce and shift concentration to corporations and businesses over their traditional audience of designers and graphic artists.

Seeing Adobe’s weakness, competitor Quark Inc, the developer of the leading QuarkXPress professional publishing software, sent a hostile takeover bid to acquire Adobe for $1bn. Quark at the time, was much smaller than Adobe with annual revenues of $200mn, compared to Adobe’s $900mn.

Adobe would successfully fend off Quark’s attempt to takeover Adobe. CEO Warnock would state in an interview “I don’t think Adobe’s struggling. We’re not a company that’s in a turnaround situation. What we are is a company that was letting expenses get out of line.” With that said and the hostile takeover out of the way, Adobe began it’s restructuring process.

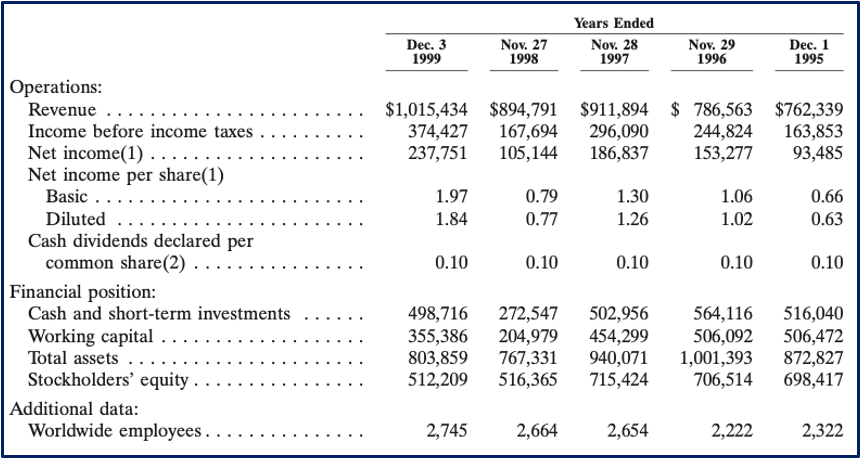

The following year, in 1999, Adobe released InDesign, or as many back then called it “a Quark Killer”, since InDesign would target the high-end professional publishing segment, a segment that was dominated by Quark products. InDesign created the largest backlog for a new product by Adobe. As a result, revenues accelerated past the $1bn milestone and Adobe’s stock would more than triple during the year.

In 2000, Adobe underwent a CEO change when founder and CEO, John Warnock, stepped down from his role, and COO Bruce Chizen taking his place. The two co-founders would remain on the board at the time.

By 2001, Adobe’s internet publishing product revenues made up more than 50% of Adobe’s revenues, with more than 90% of all websites using Adobe’s Photoshop software, while roughly 75% of all web pages were designed with Adobe Illustrator.

In late 2003, Adobe introduced its first unified Creative Suite offering, which fundamentally changed how creative professionals interacted with its software ecosystem. For $999, users could get Photoshop, Illustrator, and InDesign, compared to $1,847 buying each separately. Throughout 2004, a significant migration occurred as customers transitioned from licensing individual applications, such as standalone Photoshop, to purchasing the comprehensive Creative Suite.

This behavioral shift caused a notable realignment in Adobe’s financial reporting, moving substantial revenue from the Digital Imaging and Video segment directly into the Creative Professional segment. Building on this momentum, Adobe launched Creative Suite 2.0 (CS2) in the second quarter of fiscal 2005.

The new CS2 integrated full updated versions of Adobe’s core design and publishing applications. The market reception for CS2 was overwhelmingly positive, with the higher-priced Premium version outselling the Standard version at a rate of three-to-one at launch. This successful platform strategy drove record quarterly revenues, including a 21% y/y revenue increase in the second quarter of 2005 to $496mn. Strong adoption of the Creative Suite, coupled with growth in Acrobat desktop products, pushed Adobe’s total annual revenue to a record ~$2bn in 2005, an 18% increase over the prior year.

Shortly thereafter, Adobe made another transformative move with its 2005 acquisition of Macromedia for $3.4bn. This merger was designed to expand Adobe’s reach beyond desktop publishing and imaging, positioning the company to capitalize on the rapid growth of interactive digital content and online business processes. This deal brought Dreamweaver, ColdFusion, and most importantly, Flash into Adobe’s portfolio. At the time, Flash had become a dominant technology for interactive web content, animation, and video playback across the internet. Therefore, the acquisition was poised to extend Adobe’s reach from print and static design into the emerging world of interactive digital media.

By 2007, Creative Suite (CS) grew to become 60% of Adobe’s revenue. With a growing ecosystem, and revenues accelerating 23% to over $3.1bn, CEO Brian Chizen announced he would retire from Adobe. This opened the door for Shantanu Narayen to become CEO. Shantanu was at the company since 1998 and worked his way up to COO before getting the promotion. He also was an early Apple senior executive prior.

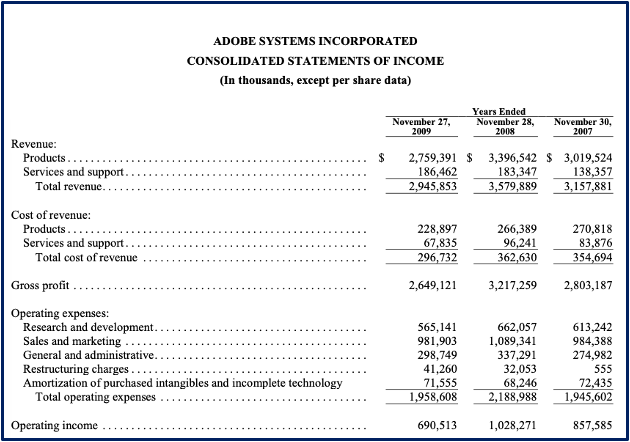

The following year, when the Great Financial Crisis hit, marketing agencies and creatives pulled back on software product spending. This caused revenues to drop -18% y/y from $3.6bn to $2.9bn, which sent shares falling down 65%. Experiencing how cyclical their product sales could be pushed him to find ways to better diversify out their revenues. One solution was to move into a new market by acquiring Omniture in 2009 for $1.8bn, which gave them a bigger position in the online marketing and web analytics space.

While Adobe was dominant on the desktop, the world would soon be moving to mobile. While Apple had been a close partner with Adobe for most of the company’s history, that would change. Adobe’s Flash was a primary platform for developers on the internet. With the introduction of the iPhone in 2007, Apple and Steve Jobs refused to support Adobe’s Flash on its mobile devices, citing performance, security, and battery concerns. Subsequently, industry momentum shifted toward open web standards such as HTML5, which offered similar capabilities without requiring proprietary plugins. In 2010, Apple formalized its position in a public letter from Steve Jobs, called Thoughts on Flash, accelerating the decline of Flash.

Ultimately, Adobe discontinued Flash Player for mobile in 2011 and altogether in 2020, marking the end of what had once been a core strategic product (where they ran a sort of freemium model with it being free for the public to use, but charging developers for tools).

Despite this setback, Adobe’s broader ecosystem continued to strengthen. Creative Suite adoption continued, with more and more users trying Adobe products. This would accelerate in the years ahead when they rolled out a subscription pricing model.

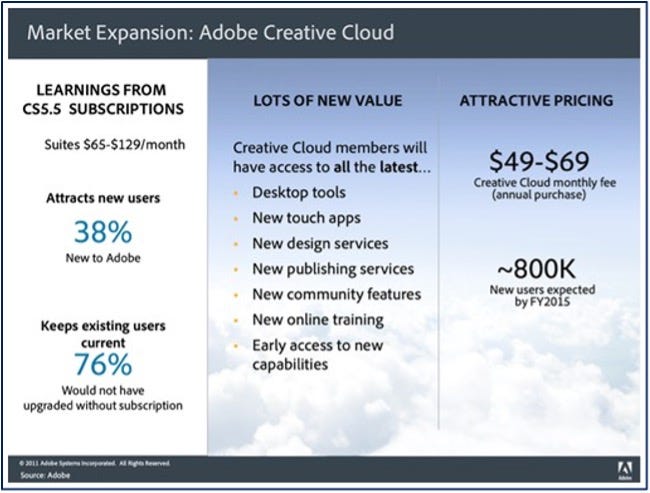

In late 2011, in an effort to bridge desktop apps with cloud storage and services, Adobe announced the first version of Creative Cloud, introducing the first subscription-based pricing the company has done. Now instead of paying $1,700-$2,500 for the full suite of products, customers could now pay a subscription fee of $49-69 and their work would be saved in the Adobe Cloud.

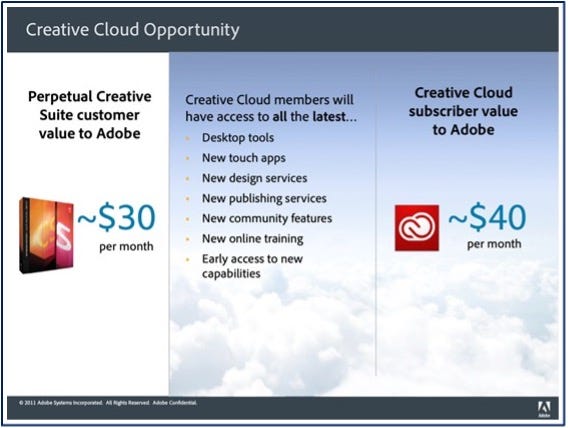

In a 2011 presentation, Adobe stated that the customer value to Adobe across all CS suites for their perpetual licensing product was $30 per month. In contrast, the customer value to Adobe across all Creative Cloud offering was $40. By moving from a large licensing fee to smaller monthly cost, they effectively took a hidden price increase. Instead of collecting ~$1,200 from a user who bought a perpetual license and used it for 3 years before upgrading, they would earn >$1,400 from that same user who paid a smaller monthly fee over the same 3 year period. This was a “win” for the user because they would always get the latest version of the product and had a lower upfront cost. The downside was that they would never “own” the product again and be stuck paying subscription fees. Adobe would benefit from more predictable revenues that didn’t rely on pushing out new features to convince users to upgrade to a new version and the higher effective price. There was a downside though: the transition to the subscription would result in a period of far lower revenues as they swapped $1,200 licenses for $40 monthly payments. At the time, 70% of revenue was derived from licensing of their Creative Suite product.

With the GFC in the rear view mirror, CEO Shantanu Narayen knew the pivot from a less volatile product that relied on a renewal cycle to a subscription model with the launch of the Creative Cloud was the right move… but it wouldn’t necessarily be easily adopted by consumers.

Users expressed frustration with the plan and threatened that they would switch to a competitor before becoming a subscription customer. As a result, the stock fell over 30% in mid-to-late 2011, which led Adobe to guide to slower revenue growth in 2012.

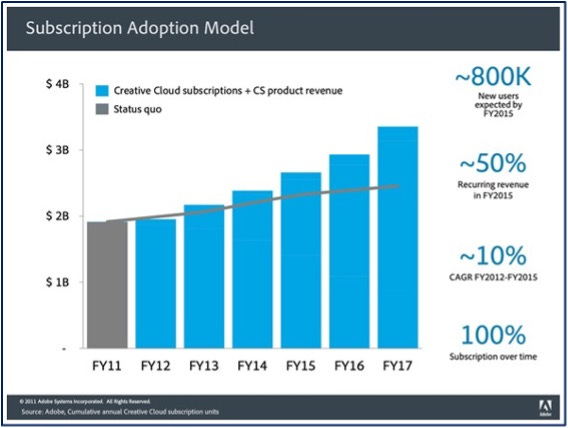

Despite this, in 2013, the company committed to the most consequential business model transition in their history. At its MAX conference, Adobe announced that it would eventually discontinue the perpetual software licenses in favor of the subscription-based model under Creative Cloud.

Initially tensions with the business shift were high as 2013 revenues fell -8% to $4bn, a very rare revenue contraction outside of the Great Financial Crisis. The revenue headwind was predictable, but it was still an open question whether consumers would succumb to the subscriptions or milk their perpetual licenses as long as possible before switching to a competitor.

The following year revenues started to recover, growing 2% y/y to $4.1bn. Adobe was confident this SaaS model would work and pushed more into the subscription business by launching the Adobe Document Cloud in 2015. Similar to Adobe Creative Cloud, which bundled all of the creative tools a digital creator would use, the Document Cloud combined Adobe Acrobat and Adobe Sign to create a comprehensive platform to create, edit, sign, track, and store PDFs.

In an effort to compete in the low-end of the market against Canva, who disrupted the market with a freemium web-based app that was quick to set up and easy to use, Adobe released Adobe Spark in 2016. Adobe Spark (which got renamed and relaunched as Adobe Express in 2022) was an all-in-one, cloud-based content creation app designed for quick, easy design on web and mobile. It allows users, especially non-designers, to create social media posts, videos, flyers, and PDFs using templates.

In March 2017, Adobe launched Adobe Experience Cloud. This was a platform designed specifically for enterprise marketing, advertising, and analytics. In 2018, to further build out their e-commerce and enterprise marketing capabilities and bolster their Digital Experiences segment, they acquired Magento for $1.68bn and Marketo for $4.75bn.

Magento, their largest acquisition yet, was a marketing e-commerce platform that would underpin what would become the Adobe Commerce Cloud. Marketo would help solve high-end lead generation and automation for clients, which rivaled the likes of Salesforce’s Pardot, and create a “one-stop-shop” for marketers. Marketo allowed Adobe to connect both marketing and sales teams, allowing a business to go from high-scoring warm lead to email in one place. In addition, they would acquire Workfront for $1.5bn a few years later in 2020 to enterprise marketing teams manage their project workflow from start to finish. These tools helped move Adobe from just focusing on content creation to actually delivering that content to consumers, which embedded them more in workflows.

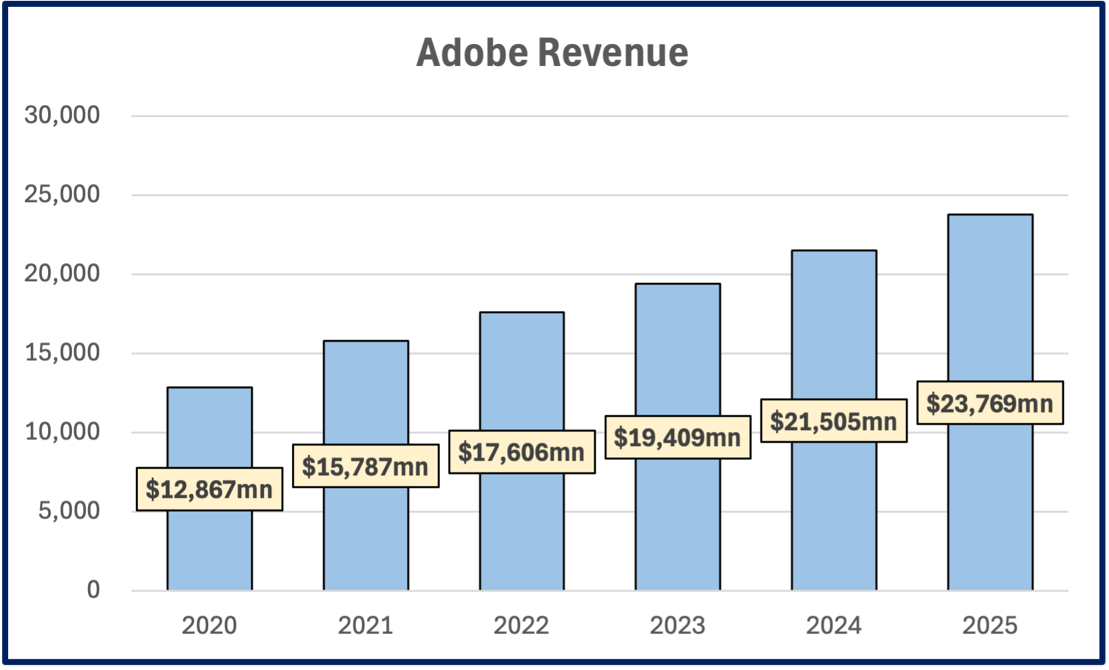

In 2020, the Covid Pandemic drove more digital creation as people started new businesses and hobbies online. In contrast to prior economic crises, Adobe was able to grow revenues +15% y/y in 2020. Adobe’s revenue would accelerate the following year +23% y/y to $15.8bn as the creator economy grew.

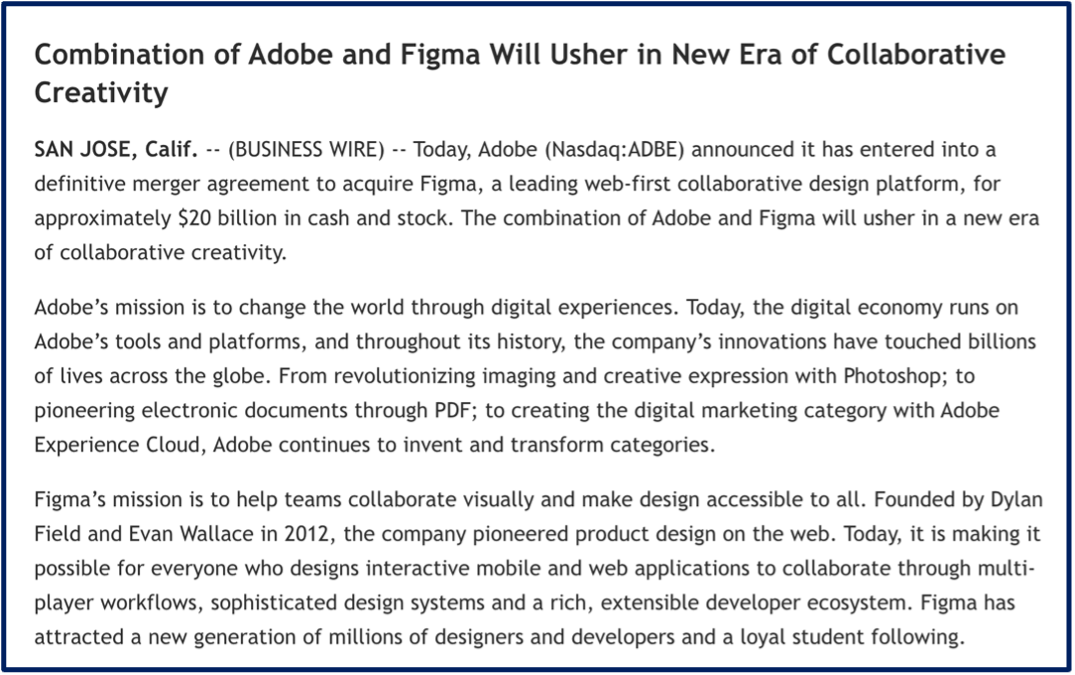

In September 2022, Adobe management had eyes on a rising design competitor, Figma. Figma helps designers create aesthetic and intuitive user interfaces & user designs for software, websites, and apps. Adobe had their own product design software called Adobe XD to rival Figma but didn’t gain as wide of an adoption compared to Figma. Adobe would seek to acquire Figma for $20bn, their largest acquisition in its history, which was double Figma’s private market valuation of $10bn and 50x Figma’s annual recurring revenue.

Figma agreed to the acquisition, however, after a year of trying to get regulatory approval, the deal hit a wall in the UK and Europe, where they feared that Adobe would become a monopoly. As a result of these regulatory hurdles, Adobe decided to terminate its acquisition of Figma in December 2023 and pay a $1bn termination fee.

As a result of the failed Figma acquisition, Adobe essentially decided to seed that market to Figma and partners with them where they can. Adobe would still maintain their competitor Adobe XD product, but management has diverted their focus elsewhere, seeing that it was a lost cause.

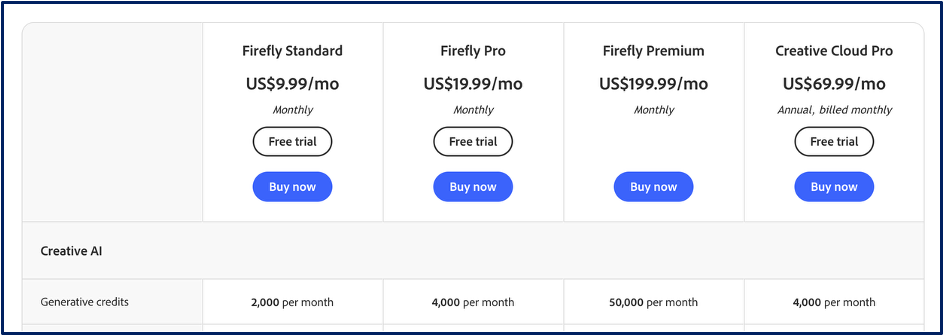

That focus turned to AI as not only an opportunity, but potential existential threat. They quickly adapted AI into as many of their products as possible. They rolled out the Firefly model to allow users to generate AI images in 2023, with the ability embedded across their suite of apps.

Firefly was trained on licensed and public domain content (drawing on their Adobe Stock image business), which positioned them to have the only “commercial safe” generative AI product. The thinking was that enterprise clients, particularly global brands, would care most about the rights of the images created. While this may have been decent intuition, ultimately they would not be able to invest at the level of other AI companies to stay competitive in AI image generation and instead opted to partner. Within a couple years they integrated all of the largest AI models directly into their apps, giving users a choice of what models they could use.

They would also adopt AI into workflow automation. Products such as Gen Studio and its agent orchestration tools are aimed at streamlining end-to-end marketing processes, positioning Adobe not just as a creative software provider, but as an integrated platform for enterprise content production and distribution.

Alongside charging a subscription for Adobe tools, they are also supplementing with a usage-based model, where users will be charged on how much AI credits, they use (but on a subscription basis to buy more credits).

The company reported record revenue in 2024 and 2025, with enterprise deals tied to creative and marketing solutions growing at a triple-digit rate year over year. This was driven in part by increasing demand for AI-enabled productivity tools.

Even so, the central question of whether AI is an existential risk remains unresolved in many investors’ minds. Adobe has successfully integrated AI into its existing ecosystem, but investors are concerned about the ramifications for Adobe as AI continues to improve at a rapid pace.

In that sense, Adobe’s challenge is not simply adoption, but ensuring that they are well positioned for the many different ways AI could threaten their business model. The company has strong distribution with a large customer base and is a gold standard for creative asset modification. Still, there is a lingering fear that even if they survive AI, it could reshape their business for the worse.

Today, Adobe is the largest creative design software company with 850mn monthly active users across Creative Cloud and Acrobat, with over 41mn paying subscribers, generating $24.5bn in LTM revenues at a 37% operating margin. Their revenues have continued to grow, despite AI and they remain very cash generative. Management is betting that by partnering with AI companies they can mitigate the threat and have continued to buyback stock aggressively.

But will that be enough…

This concludes the free excerpt of our report, to read the rest of the 99-page report, become a full Speedwell Research Member today or you can purchase a single report!

AdobeTable of Contents

Founding History.

Business History.

Business.

Industry.

Competition.

Digital Media Competition.

Canva.

Figma.

Video Tools.

Other Competition.

Digital Experiences Competition.

Salesforce.

Other Competitors.

Adobe’s AI Threat.

Adobe’s Moats and AI Strategy.

ROIC and Capital Allocation.

Valuation.

Other Risks.

Conclusion

(Please reach out to info@speedwellresearch.com if you have any issues or need to speak to us to become an approved vendor in order to expense the membership).

Read more about our Adobe Report here.

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).