APi Group Business History

From a Small Plumbing Company to a Global B2B Service Provider

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is an excerpt from our research report on APi Group. If you prefer to listen to it, you can find a podcast reading of it here: Apple, Spotify.

Founding History.

The founding of APi Group traces back to 1926 when Reuben Anderson started a small plumbing company in St Paul, Minnesota. Over time, his company grew, and a division focused on insulation contracting and distribution emerged, which would become the roots of what we now know as APi Group today. In 1948, this division was incorporated as a separate company, and a few decades later, in 1964, leadership transitioned to the next generation. The family business continued to diversify, particularly into construction and construction-related industries, while at the same time starting to expand globally. 2002 marked their next phase when current CEO and President of API Group, Russell Becker, took over after spending seven years leading a subsidiary. The most recent catalyst for change came in 2019 when J2, a SPAC, acquired APi Group for $2.9bn.

To understand APi Group, we have to know Martin Franklin. Martin Franklin had a long history of acquiring companies through more traditional means—usually buying underperforming companies that he felt had more potential to operationally improve and a runway to acquire related businesses. Martin Franklin’s career began by partnering with his dad, a merchant banker who was partners with James Goldsmith, to LBO a paper and packaging conglomerate. He was just 24 at the time, at the beginning of a long career of acquiring, improving, and flipping companies.

Franklin’s acquisitions have extended to various industries including financial services, media, fast-food franchises, and consumer products. The SPAC that acquired API Group, J2, was named after Jarden. The original Jarden traces back to a 2001 acquisition of Alltrista, a spin-out from Ball Corp., which was renamed to Jarden at deal close.

Jarden focused on the consumer space and acquired a variety of brands including Crock-Pot, Mr. Coffee, Coleman, and Yankee Candle, among many others. Originally purchased for ~$300mn in 2001, in 2015 they would sell Jarden for ~$15bn, making Martin Franklin an estimated ~$500mn in the process.

In 2017, Martin Franklin, alongside Jarden business partners James Lillie and Ian Ashken, set up J2 and raised $1.25bn. J2 was just the latest in a string of Franklin’s SPACs dating back to 2006. Other businesses he was involved in include Restaurant Brands International—which owns thousands of Burger Kings and Tim Hortons, in addition to some other franchises, Element Solutions—a specialty chemicals producer, and Nomad Foods—a frozen foods conglomerate.

With a long history of dealmaking and improving businesses, Martin Franklin’s endeavors into the safety and specialty services business through API Group in 2019 piqued the interest of many investors who began to wonder how much the business could improve and just how long the growth runway could be.

Business History.

In 2019, J2 acquired API Group for $2.9bn with the intention of improving their existing operations and making it the vehicle for subsequent acquisitions in the commercial safety solutions space. The purchase was funded in part by a $1.2bn term loan. At the time, APi Group had around $4bn in revenues and listed on the NYSE in April of 2020.

In 2019, APi Group had over 40 operating businesses with over 200 locations, primarily all located in North America. Their group of businesses served a variety of essential business needs like HVAC systems, fire sprinklers, water & telecommunication infrastructure, electricity & natural gas distribution systems, security systems, and fire alarms.

Immediately after acquisition they started to face headwinds from Covid, which shut down a lot of their business. Revenues further contracted in 2020 because APi Group deliberately shifted focus to service revenues over contract revenues, which were lower-margin and by nature, one-time.

To grow service revenues, they focused on the inspection business because for every dollar they earn with an inspection, they tend to generate an average of $3 to $4 of annual service revenue. This is because as businesses use APi Group for inspections, they are more likely to continue to use them for various maintenance services that might come up during inspection.

Additionally, a lot of systems are statutorily required to be inspected and serviced regularly, which is work they can take over. This shift from contract services to higher margin service work had the byproduct of improving revenue predictability and customer relations. CEO Russell Becker comments on this dynamic below.

Their original goal was to generate 50% of their revenue from services, which they would meet a few years later. The growth of service revenues had the added benefit of allowing them to be more selective in contract revenue, so they can pick better, higher-margin projects. As Russell Becker pointed out in the 2Q20 earnings call, they do not “bid” on projects” because they are not competing primarily on price.

Many contracts may come to them through their inspections or services, where a client needs to upgrade or build out their infrastructure. In these instances, the client is more likely to use APi Group since they already trust them.

While the markets they operate in are very fragmented, APi Group is well positioned to consolidate it because small businesses are much more focused on winning large contracts, whereas the APi Group system allows them to efficiently serve the smaller ticket size work that gets less attention.

Their initial goals were to grow EBITDA margins to 12%+ by 2023 versus about a 7% EBITDA margin at the time.

Earnings growth would come not only from margin expansion but also acquisitions. They completed over 60 acquisitions between 2005 and 2021. In most cases, APi Group engages directly with the seller and, similar to the reasons why someone may sell their business to Constellation Software, many of the owners looking to sell to APi Group are concerned about finding the right steward and home for their employees.

While M&A is frequent, it is done with price discipline. While they have paid up for a strategic acquisition in the past, like with their acquisition of SK FireSafety at 12-13x EBITDA in order to gain ground in international markets, they usually pay closer to a mid-single digit multiple. Co-Chairman James Lillie shed some light on their M&A philosophy, saying “I’m not going to die over a $20mn price differential in something like SK FireSafety that really sets up a platform for us in Europe and can help our existing businesses be better and can drive incremental M&A down at the 4, 5, 6x level.”

As of 2021, they had over 200 locations and were the #1 provider of fire protection and life safety services. These are high quality businesses because legally customers’ facilities are required to be inspected at least annually, and sometimes more. This allows APi Group to not only drive recurring revenue with inspections, but the services they provide help to keep their customers up to code. The inspection and service revenues are sticky, and keep them in contact with the customer, so that should the customer require a one-off project, they are well positioned to capture it without having to go through a bidding war.

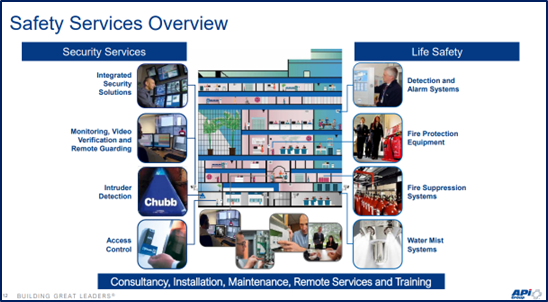

Below we see many of the services APi Group offers. Cross-selling services—like adding fire extinguisher inspections when they already service their fire alarms—is a key driver of value and helps further embed them with their clientele.

Their largest acquisition came in 2021 when they acquired Chubb with revenues of $2.5bn in a transaction valued at $3.1bn. They raised their EBITDA margin guidance to 13% by 2025, with a target of over $800mn of adj. EBITDA before considering additional acquisitions.

Chubb is a full-service provider of fire and electronic security services. They design, install, service, and monitor security and fire systems. In contrast to APi Group, who was primarily based in North America, Chubb’s presence was mostly international. With 13k Chubb employees, the transaction doubled APi’s size.

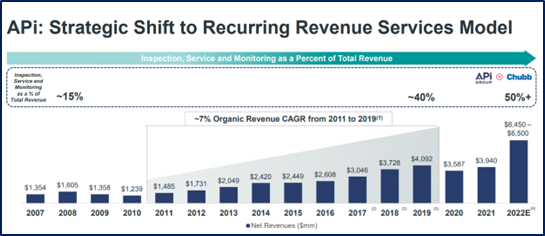

The acquisition pushed APi’s service mix to over 50% of total revenues and thus they raised their target guidance to 60%. This is prized revenue because not only are service revenues usually recurring, but inspections and service revenues generate an average of 10% higher gross margins than contract revenue.

In 2022, they had an investor day which showed their progress on their long-term targets. Whereas revenues were just $1.7bn in 2012, they reached ~$6.5bn only 10 years later. While this ~14% revenue CAGR includes significant M&A, they note that organic revenues grew ~7% for the years prior to Covid and the Chubb’s acquisition.

Over the next few years, APi Group would continue to focus on higher quality revenue sources, with their inspection-first model driving service contracts and relationship-based projects where the customer is less price sensitive. While greater discipline in customer selection has been a headwind to revenues, they consider a mid-single digit organic growth rate to be the right cadence for the company. This is before considering their bolt on M&A strategy, which by 2023 exceeded over 100 acquisitions during CEO Russell Becker’s tenure. In 2024 they generated just over $7bn in revenues.

With plenty of room to go before they hit their 13/60/80 targets (13% EBITDA margin, 60% revenue from services, and 80% cash flow conversion), they have already teased that there could be much more room to grow beyond that…

This concludes the free excerpt of our report, to read the rest of the 61-page report, become a full Speedwell Research Member today or you can purchase a single report!

APi Group Table of Contents

Founding History

Business History

Business

Industry and End Markets

Competition

Safety Competition

Specialty Segment

APi Group Model

Capital Allocation & ROIC

Revenue Build and Valuation

Risks

Summary Model

Conclusion

(Please reach out to info@speedwellresearch.com if you have any issues or need to speak to us to become an approved vendor in order to expense the membership).

Read more about our APi Group Report here.

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).