Copart: 2Q26 Business Recap

Buying back stock for first time since 2019, Volumes Contract (Again),

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(If you are a Speedwell Member, click here to get the full version of this post or here to download a PDF).

2Q26 Update.

Copart reported fiscal 2Q26 and the stock sold off -3% the next day, after recovering from being down -10%.

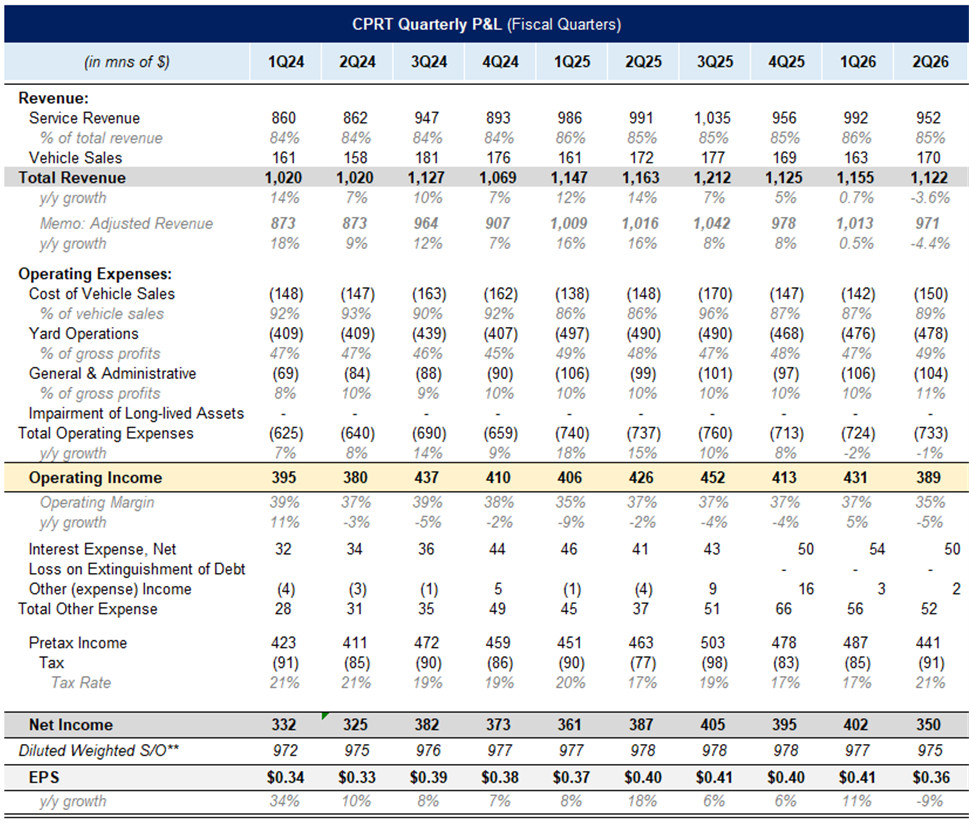

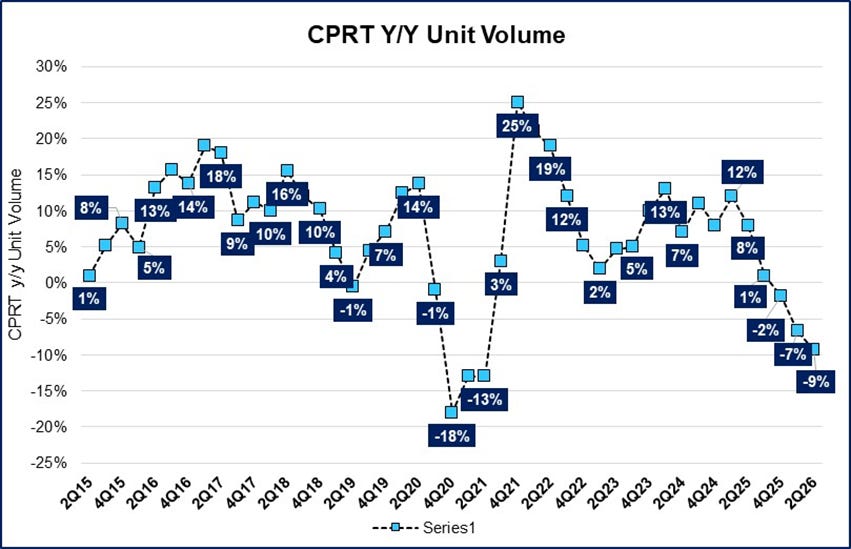

The quarter was bad with revenues down -4% y/y, gross profits down -6% y/y, and U.S. insurance units declining -11% y/y.

While there is no doubt that this was poor performance, it wasn’t quite as bad as it looked after you back out the CAT event in their comp period.

Backing out the CAT event, global gross profits were +0.4% y/y and U.S. insurance units were down -4.8%. While the contraction in U.S. insurance volumes is particularly bad, the reasons they attribute to it are unchanged from the past few quarters.

The fact that they clarified they didn’t lose any accounts and that their ASPs have increased again (U.S. insurance ASPs +6% y/y), does support management’s claims that the volumes losses are from a higher portion of drivers going underinsured and that volumes on the carrier side is driving their poor performance (Progressive in particular is rumored have been gaining share and is an IAA customer).

However, it should also be mentioned that this comes alongside some claims that IAA has stepped up their game and improved their operations. In particular, reducing the amount of time it takes a car to go from picked up to sold has become more competitive with Copart. For years Copart has benefited from IAA’s relatively worse-run operations, which helped push more wins to them. Going forward, it looks like that will no longer be the case.

An AlphaSense expert call with a former VP of Geico said “The last data point I had about three months ago was they were neck and neck. They were both at around 52 days, and they had dramatic improvements”.

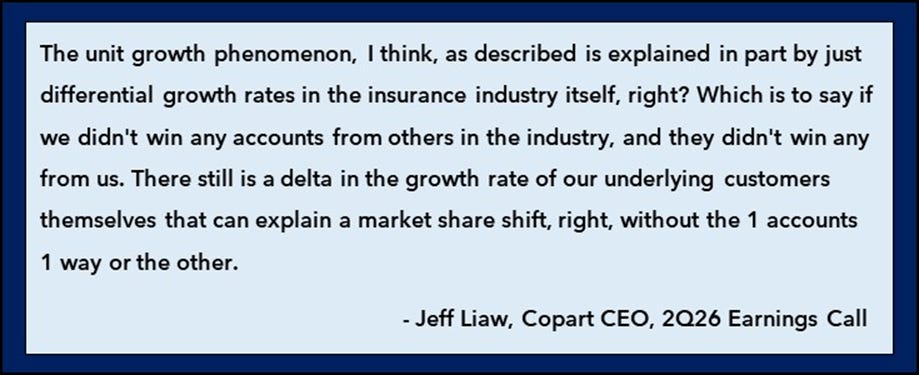

While the fear is that these volume losses were the result of IAA becoming a better run business, that thesis doesn’t hold water. There have been no carrier losses and contract renewals are every several years. Unless you believe Jeff Liaw is being misleading saying there have been “no accounts” lost, but not specifying that an account could have lost volumes, it doesn’t seem like IAA’s improved business is the result of volume losses. Nevertheless, this could weigh on future RFPs contracts.

Having said all of that, a competitor catching up, doesn’t mean they will lose volumes. The industry wants a duopoly and so has been more willing to help IAA to stabilize the competitive balance, but that is only to a point. They don’t want IAA to be dominant either, and it still is likely that Copart’s operations are faster to turn cars and could possibly offer slightly higher returns because of their better auction liquidity from more global buyers (although that point is also contended).

In terms of potential future price competition, Jeff Liaw had this to say:

You can read our last update for more on this and the dynamics driving the volume losses.

In short, it is a negative, but is likely a cyclical phenomenon and not secular. But competition intensity in the U.S. is picking up. To the positive, international gross profits for this fiscal year are up 10% y/y and they have a more benign competitive environment in those markets.

Valuation.

At a $34 stock price...

The rest of this reserved for Speedwell Members.

If you are a Speedwell Member, please click here to read the rest of this post.

If you want to become a Speedwell Member, click below to get access to the rest of this post, our Copart Research Report, and a large library of other reports!

For further reading, check out our Copart Extensive Research Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a Company episode just on Copart (Apple, Spotify)!

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Become a Speedwell Research Member to receive our Copart report and all of our other in-depth research reports, shorter exploratory reports, updates, and Plus members also receive Excels.

We have covered APi Group, Appfolio, Airbnb, Axon, Constellation Software, Copart, Coupang, CoStar Group, Dream Finders Homes, Etsy, Evolution, Floor & Decor, LVMH, Meta, Perimeter Solutions, RH, Shift4, Porsche, and Walker & Dunlop, with many more coming each year!

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in CPRT. Furthermore, accounts one or more contributors advise on may also have a position in CPRT. This may change without notice.

Do you think the risk for Copart isn't so much about "losing" accounts to a better-run IAA, but rather that the industry's desire for a stable duopoly will naturally cap Copart's ability to push for higher margins or more aggressive contract terms in the future?

I’ve subscribed and would be happy to support each other. :)

Jorrit