Dream Finders Homes: 4Q24 Business Update

8x Earnings, Regions Run like Constellation Software's Business Units, Record Home Closings

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

Business Commentary.

Dream Finders Homes reported 4Q24, closing another strong year. Whereas many would have thought high interest rates and inflation would weigh on the homebuilder, DFH’s results almost make an investor question why it seems macro isn’t impacting them.

4Q revenues grew +35% y/y, which put them at +18% y/y for the full year ending 2024. This compares to 2023 revenue growth of +12% y/y. Home closings increased +40% y/y to 3,010, up from 2,150 in 4Q of last year.

In total Dream Finders Homes closed on 8,583 homes, compared to their guidance for the year of 8,250.

As we noted prior, many misunderstand the impact interest rates have on home builders. While higher rates do certainly sap affordability and thus home demand, single home demand is generally high enough to withstand a few points increase in the mortgage rate. This is especially true because the supply of existing homes for sale tends to dry up as homeowners that have locked in low mortgages are unwilling to sell their homes and forgo their attractive rates. This means the supply of existing homes for sale contracts, leaving buyers with only the option of buying new homes. Even if total home sales fall, as they did, the portion of new homes sold grows.

Now that’s not say that a recession or weak jobs market won’t impact them—it certainly could, but a few points increase in interest rates isn’t going to do it. For the foreseeable future, there is going to be demand for single-family homes; the question is simply affordability. And on that note DFH does not build in very expensive suburban markets like in California, but rather in diverse locations across the Southeast, Mid-Atlantic, and Midwest, with their average home selling price of $509k in line with the national average new home price. They also have a range of homes to cater to different price points.

Dream Finders Homes has continued to acquire more homebuilders, adding to their pipeline of controlled lots and growing their geographic presence. In a model a bit reminiscent of Constellation Software’s business units, Founder and CEO Patrick Zalupski calls out performance of each divisional unit in his last shareholder letter. While DFH has expanded into many different markets around the country, this semi-decentralized structure where each region President is responsible for the unit’s performance is an important aspect of keeping accountability and performance throughout the organization. (We reference the 2023 annual letter as it was released in December 2024. As Patrick admitted, he was very late to release to the 2023 annual letter and hasn’t released the 2024 one yet).

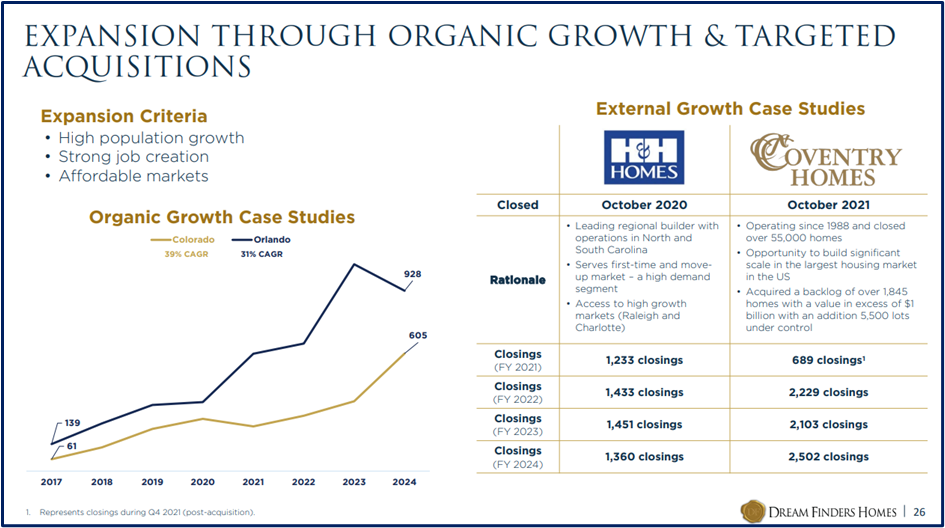

You can see their recent acquisitions and new market expansion in the table below.

Acquisitions like Crescent Homes allowed them to enter new markets in South Carolina and Tennessee. Other markets they entered organically. Orlando is one of their most successful start-up divisions, having gone from 0 to over 1,064 homes closed and $630mn in revenue in just under a decade.

Below they disclose the performance of two other acquisitions from 2020 and 2021. H&H Homes only grew slightly, at about a 3% CAGR. Coventry Homes however grew from 689 to over 2,500 home closings for a 53% CAGR. The benefit of geographic diversification is that they are less susceptible should one area experience a slow down (however they note that 77% of the states they operate in have net positive migration trends).

In terms of capital allocation and M&A philosophy, Founder Patrick Zalupski lays out a clear vision below.

In the near term, tariffs can weigh on gross profits as raw material costs increase. They have already experienced 4Q gross margin compression of 17.6% versus 19.2% last Q and 20.5% last year. For now, though, the gross margin pressure is primarily a result of construction loan financing costs increasing and not building cost increases. In fact, they note gross profits were helped by direct cost reduction.

The acquisition of Liberty Communities in Atlanta is interesting because they have a manufacturing component to the business too. As they noted in the press release, Liberty’s “offsite manufacturing and component import businesses provide cost and operating efficiencies in Liberty’s existing markets and position DFH with a potential platform for expansion to other active markets in the future.”

For those that remember in our original DFH research report, NVR is vertically integrated with their own manufacturing facilities to create material like prefabricated wall panels to reduce cost and increase building speed. NVR’s turnover ratio is about ~3x vs DFH at ~2x. Dream Finders Homes driving more cost efficiency could not only help gross margins, but also help improve turnover. (They do customize many of their homes more though, with premium features, which also weigh on turnover). This though is more speculative today.

The net of all of these impacts is that today their operating margins sit at 9.7% for 2024, compared to last year’s 11.4%

Net earnings were $335mn, up from $295mn last year. With fully diluted shares of about ~100mn, and adjusting for a contingent consideration gain from a past acquisition’s earnout, EPS comes out to $3.20 for the year. At $24 today (up about 15% since reporting earnings), DFH trades at 7.5x earnings. While they don’t have a very long history of public financials, since 2014 they have grown revenues every year, and for the years we have financials for (back to 2018) they’ve grown profits each year.

Certainly, a prolonged economic downturn could lead to deferred home purchases and thus fewer home closes and reduced earnings. On the other hand, their capital-light model, which circumvents the risk of holding and developing land in favor of land options and land banks, greatly reduces the risk that an economic calamity would be terminal for DFH (as it was for many home builders in the 2008 financial crisis). NVR, who DFH models their business after, was able to remain profitable throughout the financial crisis.

We can understand why low earnings multiples are met with suspicion. There is a tendency to believe there must be a risk that remains hidden. Though, on the other hand, investors also seek situations with very uncumbersome assumptions, and an undemanding valuation is often an important aspect of that. Perhaps there is such a hidden risk or that such situations only become obvious in hindsight. This is the game of investing, and each investor must make their own judgement.

We named our research firm Speedwell after the ship that helped ferry passengers to the Mayflower. The idea is that we want to help you get into the position to take the journey, but ultimately, we are not going to go with you. There should be no illusions—you are on your own with the decisions you make. It is an investors job to judge for themselves whether they believe the potential for profits are worth the potential risks that could materialize.

Press Release Notes.

Record Year

“We ended on a high note — our fourth quarter was by far the best quarter of the year, and, arguably, the best in Company history.”

“Record number of closings for any single quarter in Company history”

Cancellation rates were down to 16.6% from 18.3%

M&A

Acquisitions of Crescent Homes and Jet HomeLoans

Announced definitive purchase agreements of Liberty Communities (closed in January 2025)

$112mn price

Announced acquisition of Alliant Title Insurance (currently pending regulatory approval).

“We believe all four of these acquisitions are highly accretive and will contribute materially to DFH's future earnings growth.”

Guidance

This years home closings of 8,583 beat guidance of 8,250 homes

9,250 expected home closings for 2025

Liquidity

Total available liquidity as of December 31, 2024 was $816 million, including $274 million of unrestricted operating cash.

Net homebuilding debt to net capitalization was 34%

Repurchased $8mn of stock in 2024 with ~$17mn left under authorization.

For further reading, check out our Dream Finders Home Exploratory Report here.

The Synopsis Podcast.

Follow our Podcast below. We have a 2 hour Company episode just on Floor & Decor!

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our other in-depth research reports, shorter exploratory reports, updates, and Plus members also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in DFH. Furthermore, accounts one or more contributors advise on may also have a position in DFH. This may change without notice.