Floor & Decor: 3Q25 Business Update

Still Treading, but Reiterate Long-Term Vision, CEO Transition, Valuation Exhibits

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

(Speedwell Members click here for a PDF version of this post).

3Q25 Update.

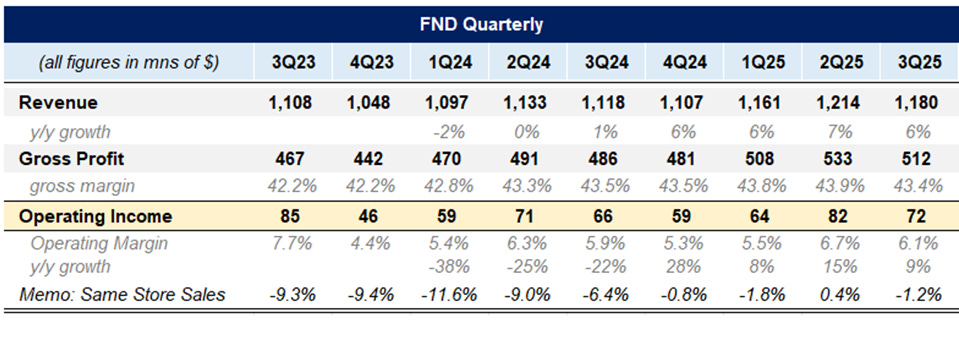

FND reported 3Q25 and the stock was up +6% after hours.

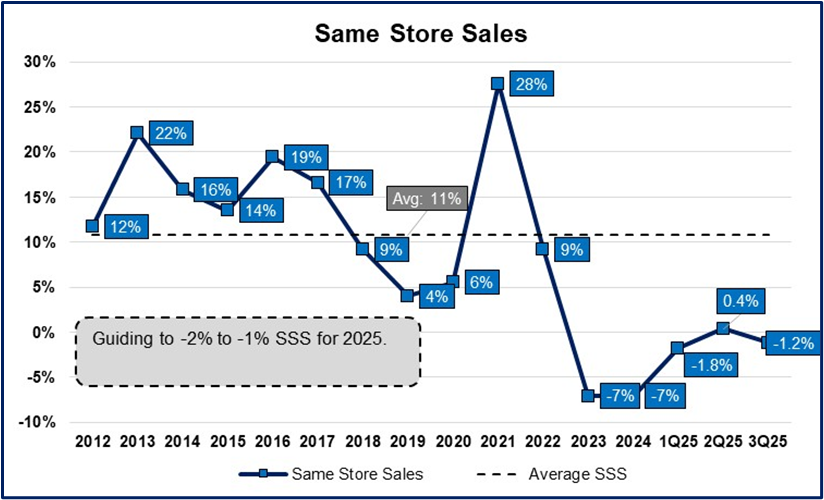

Revenue increased +5.5% y/y, while comparable sales decreased -1.2%. As a reminder, they signaled last quarter that their comps turned negative after the tariffs were enacted, which ended a very brief period of positive same store sales growth. (If you recall, tariffs delayed rate cut expectations which has the downstream effect of weighing on existing home sales). Unfortunately, same store sales (SSS) got worse as the quarter went on with September down -2.2%. For 4Q SSS are trending down -2% so far.

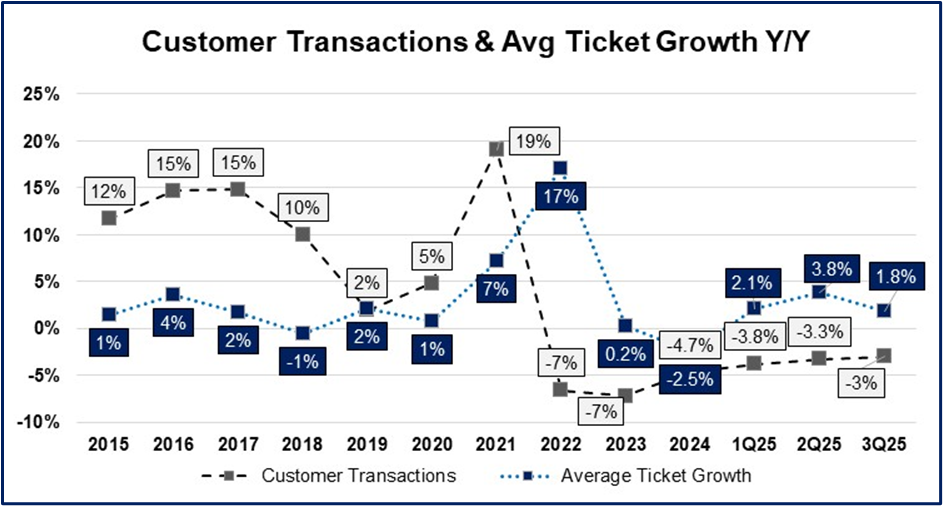

Existing home sales showed some signs of recovering and were +1% y/y in September. But a recovery in existing homes sales is far from a sure thing. Customer transactions comped negative -3%, while average ticket growth was +1.8%.

Gross margins were about flat y/y at 43.4%. and operating margins improved slightly y/y to 6.1%. Margins are still pressured by opening costs, low store level operating leverage, and a new distribution center that can support more store than it currently serves.

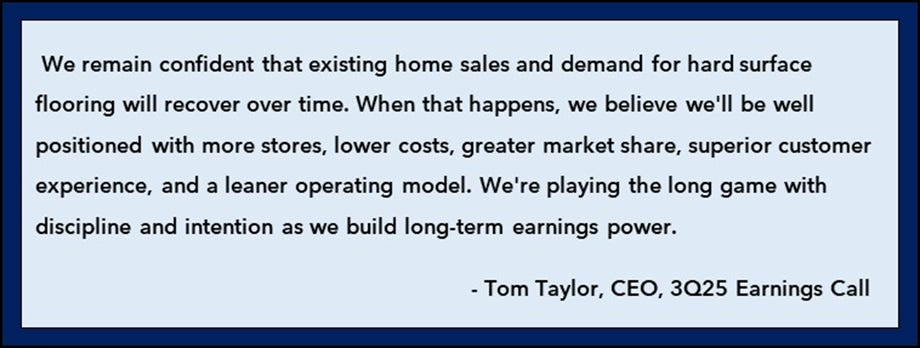

For the past few quarters they have been very focused on cutting costs, which CEO Tom Taylor notes positions them very well for when the hard surface flooring market recovers.

In addition to focusing on keeping G&A and OpEx tight, they have been reconfiguring their new store openings to invest less per store. This comes from a mix of picking built out locations, opening up smaller footprints where appropriate, and reducing building costs. “The initial investment for our fiscal 2025 class of new stores is estimated to be about $1.5 million lower than our fiscal 2023 class, with further meaningful improvement expected for the class of 2026”

They disclosed that their most recent cohorts of stores have achieved first year sales of $11 million, down from their target of $14-16 million for a first year store. However, they noted later on that growth of the new cohorts has been in line with private cohorts (although that is less impressive given the lower base).

“While our new store classes are achieving comparable store sales and market share growth, average first-year sales among classes of 2023, 2024, and 2025 are approximately $11 million, which is below our long-term target of $14 million to $16 million. Nonetheless, this performance aligns with what we would anticipate in a contracting industry and what we believe could be trough-level performance.

While we’ve seen what peak performance can look like coming out of the COVID-19 period, with first-year store sales exceeding our long-term target range of $14 million to $16 million, this is our first time operating through a sustained downturn in the category.”

Business Commentary.

By and large this was a slightly disappointing quarter because of the Same Store Sale contraction, but it was hardly surprising. Given a bad hand, Floor & Decor seems to be doing well by focusing on improving their in-store initiatives (kitchen cabinets, designers, Pro program) and controlling costs as best they can. They noted that in September their stores achieved their highest net promoter scores ever, “a clear reflection of the outstanding service they continue to deliver every day”.

They are still on track to open 20 stores this year and 20 stores next year and are well positioned for when the hard surface flooring market rebounds.

The only big surprise came when Tom Taylor announced that President Bradley Paulsen would take over the CEO role and Tom would take over as Chairman of the Board. Tom Taylor was careful to emphasis that he will continue to be involved in Floor & Decor, “where I will focus on shaping our long-term strategic vision and unlocking new avenues for growth”. The press release also suggested that he would continue to stay involved until the company hit their 500 store target.

There is no doubt that the optics of this look negative as this transition is happening in the midst of almost 3 years of poor business performance. A cynic could point out that this could suggest that Floor & Decor doesn’t fully believe their own story of the poor business performance being driven by weak end markets.

On the other hand, competitors have been suffering too. LL Flooring went out of business, and The Tile Shop is delisting from the stock market. The Tile Shop’s revenues are still 15% below their 2022 revenue level, whereas Floor & Decor is about 10% higher. While that is hardly an impressive achievement given, they have opened many stores since then, ultimately it comes down to whether or not an investor believes Floor & Decor has the strongest business model in the hard surface flooring industry because the market will eventually recover. There are no signs that they have lost share (and some they have slightly gained), but that is understandably a cold comfort as they complete almost a 3rd year of comping negative.

There also isn’t clarity as to when the housing environment is going to improve, which management generally believes is a precondition to posting positive comps. It also though is possible that the housing market is showing signs of improving right now with September sales +1% y/y. Floor & Decor investors are understandably hesitate as there has been more than one “head fake” in the past few years.

Provided though that you do believe the specialty chain store with the most in-stock inventory, lowest prices, and widest selection with a strong grip on professionals is the best positioned to win in the hard surface flooring industry, then it just comes down to the assumptions an investor needs to make and how comfortable they are with those returns.

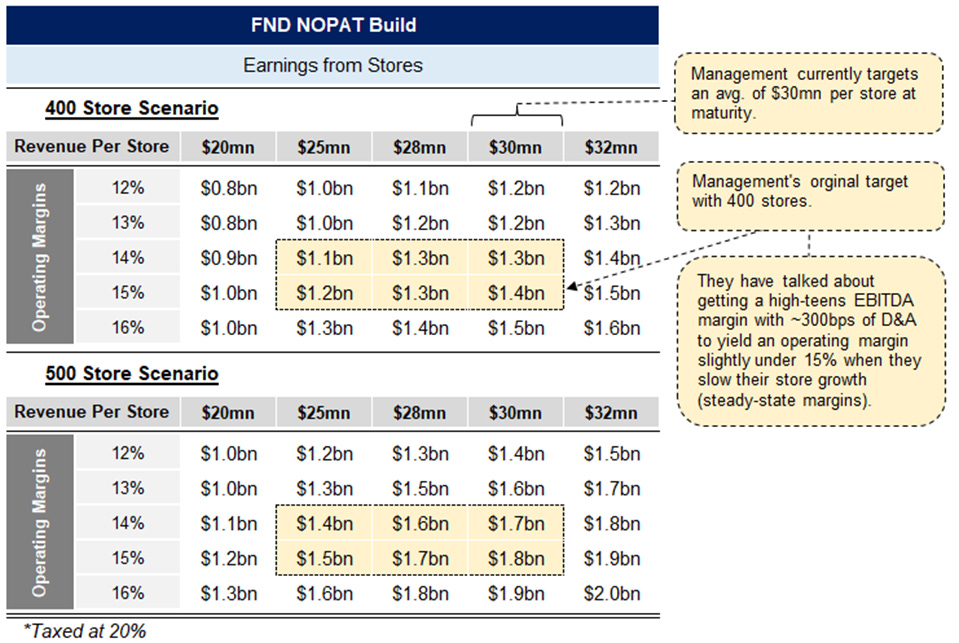

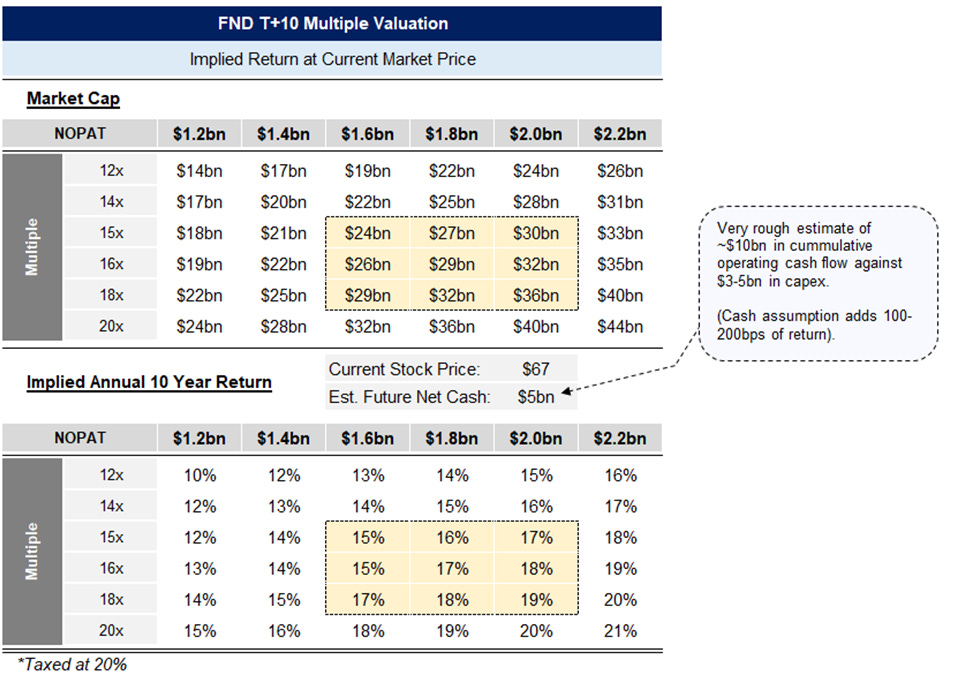

Floor & Decor has a target of 500 stores and prior commentary suggested that a store could do $30mn at maturity. Even if that was an extrapolation from a time of elevated activity, today’s 1st year stores are only doing $3-5mn less. If you assume the ramifications of that is that mature stores will also be impacted similarly, then you get $25mn in sales for a mature store. At a mature company margin of 15%, that is $1.5bn in earnings against a current market cap of $7.3bn.

Below we show various revenue per store assumptions, mature margin assumptions and then apply a multiple from 12-20x. You can even pick between a more conservative 400 store target instead of their 500. We then assume it takes them 10 years to reach that and back into the implied return. This way an investor can lower their assumptions to a level that they feel confident in and see the associated return. Of course, some investors may not be comfortable with any of these assumptions.

Below are some more notes from the call, but if you want to learn more about Floor & Decor, make sure you read our Extensive Research Report.

As a reminder, we named our research firm Speedwell Research after the ship that helped ferry passengers to the Mayflower. The idea is that we want to help you take your journey, but ultimately you are on your own in the decisions you make. An investor must judge for themselves whether they believe the opportunity is worth it and accepting the potential risks that could materialize.

Call Notes.

Tom Taylor Transitions to Executive Chair

Brad Paulson appointed to CEO, Tom Taylor will be executive chair of the board

Thinking Long Term

“We remain confident that existing home sales and demand for hard surface flooring will recover over time. When that happens, we believe we’ll be well positioned with more stores, lower costs, greater market share, superior customer service, and a leaner operating model. We’re playing the long game with discipline and intention as we build long-term earnings power.”

New Warehouses and Distribution Centers

Opened 5 new warehouses stores, re-entered the Charlotte market, and establishing their first store in South Carolina

On track to open 20 new stores in 2025 and another 20 openings in 2026

Opened their fifth distribution center in Seattle, to support growth in the Western region

Opening Costs Declining

Initial investment for 2025 stores are $1.5mn lower compared to 2023 stores

Shift to Smaller Markets

Due to permitting delays in mid and large markets, they decided to open more stores in smaller markets to mitigate those headwinds

SSS

Comp store sales for 2023, 2024, and 2025 are $11mn, below their long-term target of $14-16mn

Comp store sales declined -1.2% in 3Q

-0.6% in July, -0.4% in August, and -2.2% in September (due to elevated mortgage rates)

Due to Hurricane Helene and Milton, 4Q comp store sales will be a harder comp (110bps benefit)

3Q comp stores in the West outperformed

Homeowner comp store sales still negative but showed sequential improvement fueled by new and returning customers

Customer Transactions & Average Ticket

-3% decrease in customer transactions, partially offset by a 1.8% increase in average ticket

1.8% in average ticket was the low-end of their guidance. There were 2 drivers: slower growth in laminate and vinyl category and lower job size

3Q comp stores in the West outperformed

Core strategic priorities

Rolling out kitchen cabinets to ~200 stores by year-end

Expanding outdoor and pool product assortments to ~80 stores

Growing the XL Slab program to ~200 locations

Design Services

“We view design services as a competitive moat, a differentiated capability anchored in deep customer engagement, project-based selling, and operational excellence.”

“We think it is a big part of the moat around our castle, the service that those designers provide. The tickets are higher. The margin blends are better.”

Pros

Pro representing ~50% of total sales

Comp store sales for pros were flat, slight decline in transactions and a slight increase in avg ticket We continue to see a shift toward smaller projects such as tile-focused bathroom projects, kitchens, and restoration work.

Commercial

Spartan grew 13.3% y/y

Margins

Gross margins decreased due to the opening of the Seattle distribution center and cost related to the future opening of their second Baltimore distribution center (impacted 3Q by 90bps)

2025 Outlook & Macro

“We anticipate little divergence from the prevailing housing sector trends. Consumer spending is likely to remain restrained, particularly on big-ticket discretionary durable goods with a preference for smaller-scale projects.”

“When I see what’s selling in our store when customers are coming to buy, they’re buying the more expensive products and the better products, they’re just doing less square footage, and less projects.”

Planning on 20 new warehouse stores

Comp stores estimated to be down -2% to -1%

Avg ticket comp is estimated to be up low single digits

Stores are in the South (Texas and Florida) are being pressured due to overbuilding, and poor existing home sales

Floor & Decor Research Report

Read our our 57 page Floor & Decor in-depth research report here.

The Synopsis Podcast.

Follow our Podcast below. We have a 2 hour Company episode just on Floor & Decor!

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive our Floor & Decor report and all of our other in-depth research reports, shorter exploratory reports, updates, and Plus members also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in FND. Furthermore, accounts one or more contributors advise on may also have a position in FND. This may change without notice.