Floor & Decor 4Q24 Business Update

Inflection Point or Confidence Slipping?

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

4Q Business Commentary.

Floor & Decor reported 4Q24 earnings and after an extreme after-hours move (+13%) it closed the following day +2%.

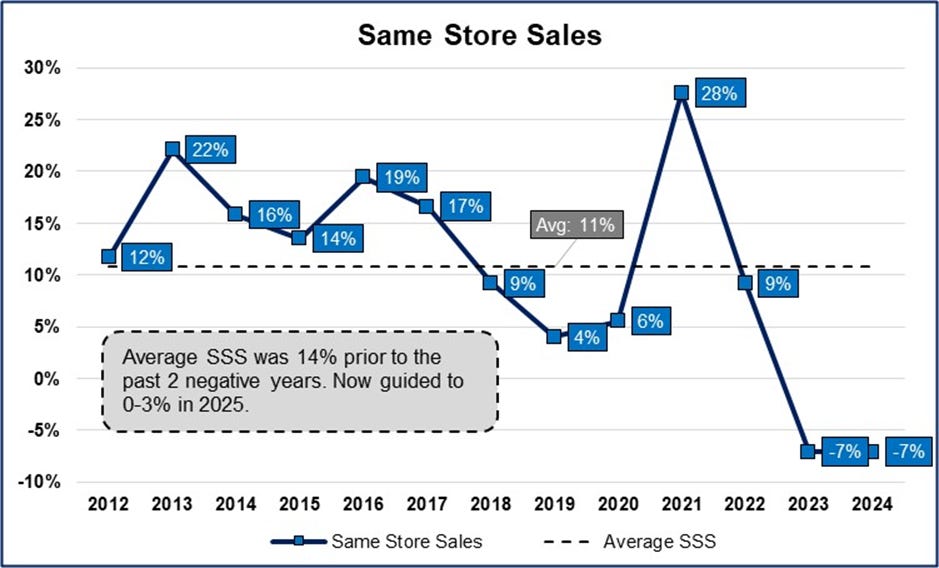

Overall 4Q revenues grew +5.7% y/y and they opened 10 new warehouse stores, putting them at a total of 251 (not including 5 design studios).

Same store sales (SSS) fell -0.8%, which compares to -6.4% in 3Q, -9% in 2Q, and -11.6% in 1Q. This likely marks the near end of their negative comps, with the worst of the existing home sales headwinds now behind them. (As a reminder, a home sale is one of the most common “trigger events” that causes someone to replace flooring.)

Since 2020, and including the last two years of -7% growth, SSS grew at a 5% CAGR. While this isn’t horrible, it is much lower than their average since 2012 of 11% (which was 14% prior to inclusion of the last two years). As a reminder, strong historical SSS was the result of new stores ramping up and was always going to fall as the ratio of new to mature stores tilted heavier to slower-growing mature stores. Nevertheless, the slowdown was much starker than expected.

In total, 2024 revenues were +0.9% y/y, boosted by 30 new warehouse stores.

2024 operating margins of 5.8%, are 150bps worse than full year 2023 (each year has about 100bps of pre-opening expenses embedded). This may look a bit surprising at first glance since gross margins expanded from 42.1% to 43.3%, a positive development as they lapped some supply chain issues. However, the margin compression is largely a result of operating deleveraging as their selling expenses are largely the same, but less volume is being pushed through each warehouse. Additionally, they have continued to open warehouses, which take a while to generate normalized volumes, but costs are not reduced in the meantime.

If you recall from last quarter, they have undertaken expense management initiatives, which means when volumes return in a more benign macro backdrop, they could be more profitable than prior.

Generally, there was not a lot new that would change the FND thesis. You can read more of our thought from last Q here, which captures our sentiment well. The quote below is from that piece.

"By and large, this was another quarter of them executing on the long-term vision, but with a dose of short-term caution. Not only will they benefit from a more normalized environment (existing home sales at 3.8mn, down from 6.5mn in 2022 and 5.3mn in 2019), their focus on expense discipline and operational improvements should result in lasting operating model improvements, beyond the downturn."

Incrementally, they announced they are focusing on more local advertising now and testing new products like semi-custom cabinets. On one hand we like to see businesses experiment, but in the context of back to back years of negative same store sales, it does add some doubt whether they are still as confident in the growth of their mature stores as prior.

CFO Brian Langley noted that “stores that are 5 years or older today are doing about a little over $22 million, close to $22.5 million, but they're still producing EBITDA in the low 20s.” While that is strong profitability (especially compared to company EBIT margins of 6%), those revenue per store figures are considerably less than the $30mn per store they pushed investors towards a few years ago. And within the context their guidance in 2022 of growing their “store base by approximately 20% annually for the next several years”, to only remove that language the following year in 2023, adds more doubt to whether their thinking on the opportunity has changed.

Having said all that, their competitive position is still very strong as they have the widest selection of the most in-stock flooring at the cheapest prices. The strength of their value prop is apparent by them now crossing the threshold of 50% of sales to Pros. This is an important indicator because Pros have all of the incentive in the world to find the best service provider at the best value.

When macro calamity hits and the business is impacted for a couple years, it makes sense that they want to try somethings differently. It also makes sense that they may caveat their statements more than usual and want to temper their growth initiatives. But at the same time, we like best when businesses use the opportunity to get aggressive. This though is one of the reasons why founder-led businesses are in a different category. It may be much harder for Tom Taylor to get the full shareholder base onboard with a continued aggressive push than it would be for RH’s Gary Friedman or Meta’s Mark Zuckerberg to just continue to gun the accelerator and invest through downcycles.

At a $95 stock price, they trade at 50x earnings. However, using mature margins of 15%, that figure drops to 19.5x. The bigger picture potential for valuation creation was summed up well in our last post:

“Big picture the goal remains unchanged: 500 warehouse stores at $30mn per store and a mature operating margin of 15%. After 20% tax, this is around $1.8bn in NOPAT (and doesn’t include their commercial business, see notes above on Spartan). This compares to a market cap today of $11bn [$10bn today]. So if an investor believes in the long-term target, the question is simply: when are they going to get there?”

Given our commentary, an investor may feel more comfortable assuming a $25mn per store revenue figure, which gets us $1.5bn in NOPAT. At a market multiple of ~20x, that is $30bn of value (and doesn’t include any cash they generate in the interim). An investor has to decide for themselves what they are comfortable assuming and the timeline they foresee as realistic.

Call Notes.

Long-Term Opportunity

“This has allowed us to grow our market share despite the industry contracting and prepared us to maximize sales and profitability once the industry's cyclical growth accelerates to historical rates.”

“The demand for housing continues to outpace supply, and the 40-year median age of owner-occupied housing is continuing to increase. We believe the supply and demand inbounds in housing and aging housing stock remains a significant secular growth opportunity as older homes will need updates after the past several years of postponed remodeling”

Opened 250th store, marking halfway point to 500 warehouse store goal

“Approximately 55% of our stores have opened in the last 5 years, leading what we believe is plenty of room for growth along the maturity curve.”

Advertising

“We cannot control the short-term cyclical pressures affecting the hard surface flooring industry and their impact on the first year sales of our new stores we opened. However, we have identified specific strategic actions we can take to maximize their chances for success during this challenging period. In fiscal 2025, we plan to be more intentional about reaching new customers. We intend to emphasize impression-driving media and messaging updates to grow local brand awareness.”

“Expand our brand awareness, attract more new homeowners and pros and create a strong foundation for long-term growth.”

Short-term Industry Factors

“The improvement of sequential sales [guiding to 0-3%] trend partially reflects long-awaited modest growth in existing home sales. Despite elevated mortgage interest rates, existing home sales rose for the third straight month in December, the longest growth streak since early to mid-2021”

New Product

“Excited to continue delivering new, innovative products and programs to our homeowners and pros. We will expand our merchandise offerings in adjacent categories including testing a high-quality, stylish semi-custom cabinet program at approximately 40 warehouse stores and online in the first quarter.”

“now offer online semi-custom cabinets, express ship plywood cabinets, cabinet accessories, decorative hardware and cabinet samples that we can ship to the job site.”

“This initiative helps our homeowners and pro customers complete kitchens and other cabinet projects and is expected to drive incremental sales growth to our stores.”

“We will reset decorative accessories to improve the customer experience and productivity further. We'll also continue expanding our outdoor and pool offerings and XL SLAB program.”

Operating Leverage

“If you think about our stores, we still average about 55% fixed cost, 45% variable. The 2 biggest variable components are labor, like our personnel within the stores. And so we need to make sure that we match that with transaction. So again, on the upside or downside, we can flex those. And then there's also some discretionary spend where we're constantly refreshing the stores. We have so much innovation and newness that we need to make sure that we showcase that.”

Supply Chain

“These trade disputes will lead to additional tariffs beyond the 25 -- previous 25% imposed on most products that we sell that are produced in China. For example, on February 1, an additional 10% tariff was announced for all products from China”

“In fiscal 2024, China accounted for approximately 18% of the products we sold, down from approximately 25% in fiscal 2023 and approximately 50% in fiscal 2018.”

“United States is now our largest country of manufacturer, accounting for approximately 27% of the products we sold”

Scale and direct sourcing model with 240 vendors in 26 countries is an advantage here

Pro

50% of total sales now Pro

“We continue to benefit from partnering with native advertising platforms that provide a practical and cost-efficient way to attract and retain new pros.”

“We benefit from our pro service managers spending more time outside of our stores and in new ZIP codes, where they directly engage with pros to build brand awareness, understand their needs and provide tailored solutions.”

“Held 144 educational events in our stores in 2024 and plan to have 155 events in 2025. We believe these events are industry-leading in hard surface flooring in fiscal 2025, we'll focus on driving growth among new pros and reengaging in active pros.”

Competition

“Price gap versus peers, we still feel pretty good. When you look back historically, our spreads versus the people we compete with are they remain intact and we're comfortable with that. We'll deal with the tariffs, the way that we've always had. We'll first negotiate with our supplier. The second is we'll try to continue to diversify out of countries that are affected. And then third, if we have to pass price, we will. Our main competition is the independents.”

“We're comfortable with our spreads, and we've got the ability to flex price if we have to flex price. So we're paying attention and trying to react to the news as it comes. Our buying from 250 suppliers in 25-plus countries is a tremendous advantage, and it gives us lots of flexibility.”

“We still are hearing anecdotal closes across the country of different competitors. I do think I've said before, the longer that this goes on, the more that plays on our benefit because we continue to invest in the stores and continue to grow. So I think from a competitive standpoint, we're in as good a shape as we've ever been. Yes. And what is a good example of you saw a competitor close a bunch of stores, we're probably seeing some of the benefit of that. “

Spartan

“Fiscal 2024 fourth quarter sales at Spartan Services declined 17.9% from the same period last year.”

“The sales decline is primarily due to weakness in the multifamily residential market, pricing pressures in the commercial LVT market and difficult comparisons against record assemble sales at Spartan last year.”

“Fiscal 2024, Spartan Surfaces sales grew by 10.1% to $215.2 million compared to last year, but EBIT declined 25.4% to $14.3 million from $19.1 million in fiscal 2023, primarily due to pressure on the gross margin rate”

“Over the long term, Spartan Services aims to become a disruptive leader in the specified commercial flooring industry by establishing a comprehensive nationwide sales network. This network would prioritize high specification products and leverage strong relationships to provide superior availability, delivery and service nationwide.”

Investing more in sales rep growth and Spartan’s Infrastructure

Guidance

“Total sales are expected to be in the range of $4.740 billion to $4.900 billion or increased by 6.5% to 10% from fiscal 2024”

Assumes 25 new stores

“Comparable store sales are estimated to be flat to an increase of 3%.”

“Gross margin rate is expected to be approximately 43.4% to 43.7%”

Adversely impacted by 2 new distribution centers, which are included in the guidance

Check our our recent business updates on Evolution, Airbnb, Costar Group, and Perimeter Solutions.

As a reminder, we named our research firm Speedwell Research after the ship that helped ferry passengers to the Mayflower. The idea is that we want to help you take your journey, but ultimately you are on your own in the decisions you make. An investor must judge for themselves whether they believe the opportunity is worth it and accepting the potential risks that could materialize.

The Synopsis Podcast.

Follow our Podcast below. We have a 2 hour Company episode just on Floor & Decor!

For those that are new to our podcast, we have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive our Floor & Decor report and all of our other in-depth research reports, shorter exploratory reports, updates, and Plus members also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in FND. Furthermore, accounts one or more contributors advise on may also have a position in FND. This may change without notice.