Copart Business Update 3Q24 (Fiscal 1Q25)

Service revenue growth reaccelerates, we update our reverse DCF, and autonomous vehicles aren't the risk investors think

Welcome to Speedwell Memos. Our main website is SpeedwellResearch.com.

This is a business update on a company we have previously written an in-depth research report on. To read the full research report become a member today. Members get access all of our research reports and all prior updates (most of which are paywalled). You can see a list of all the companies we have written on here.

Quick note: Copart uses a weird fiscal year that calls this quarter 1Q25. We think this is confusing so we will refer to this quarter and prior quarters on a calendar year. That means we will call this quarter 3Q24. The quarter technically ends October instead of September like a typical 3Q24 calendar year, but we still think this is more straightforward.

3Q24 Update.

Copart reported earnings and the stock was up +9%.

As a reminder they have two revenue segments: service revenues and vehicle sales. Service revenues are reported on a net basis, whereas vehicle sales are reported on a gross basis (they technically purchase the car and then remarket it instead of just taking a commission).

This is important to remember because if vehicle sales grows more than service revenues, we would expect to see a gross margin contraction and vice versa. However, the unit economics of both transactions are very similar. Although, there is a slight difference in risk profile of the transaction, which will only be apparent if the used car market quickly falls. (See our full report here for more of an explanation).

Service revenues grew +14.8% y/y to reach $986mn. This represents an acceleration of growth of +770bps compared to last quarter’s +7.1% y/y. (For context 2023 total service revenue growth was +11.3%). This was unexpected, but welcomed. However, it was partly driven by hurricanes, which temporarily boost volumes.

Vehicle sales were ~flat y/y at $160mn, but down about 8.5% q/q. Vehicle sales represent about 14% of total revenues.

Operating expense line items were renamed. “Yard” became “Facility”. As shown below, the expense item values did not change though, just the names.

Gross margins contracted y/y to 44.7%, down 80bps from 45.5% in 3Q23. This is despite the mix shift of vehicle sales falling y/y from 15.7% of total revenues in 3Q23 to 14.0% in 3Q24 (which should helps boost gross margins as vehicle sales are a MUCH lower margin revenue). This is primarily driven by an increase in facility operating costs, which were +21% y/y. About 4.5% of this expense growth came from incremental costs associated with the hurricanes. (There is a further $18mn of capitalized costs which will be recognized as the remaining CAT units are sold.)

Total operating income was $406mn, +2.8% y/y versus 2Q24 operating income contracting -8% y/y. Total net income was +9% y/y, which was slightly offset by +0.5% in share dilution, given us a quarterly EPS of $0.38, +3 cents y/y.

Call Notables:

Hurricane

2 hurricane’s (Helane category 4 and Milton category 3) hit in September/ October.

Picked up twice as many cars in the first 10 days of the 2024 storms compared to 2022

This is important because high service levels help insurance companies settle claims quickly, which is key to keeping customers happy and avoiding churn. Messing this up is a key event that drives churn to other insurers.

Insurance Business

Units grew 13% y/y or 9% excluding the CAT event

Total loss frequency grew almost 2% y/y to 21.7%

Units

Global unit sales +12% y/y

Inventory +6% y/y

US Unit growth +11%

International +16%

Non-Insurance Volume

“Blue Car business, which serves our bank and finance, fleet and rental segment partners continued its strong trend of year-over-year growth of over 20%.”

This is what they call their non-insurance and non-dealer business and it is a very important growth driver because these vehicles tend to be higher quality than insurance cars, which means they sell for higher ASPs and thus generate more commission on a unit basis.

“Dealer sales volume, a combination of our Copart Dealer Services division and National Powersport Auctions increased sales volumes by over +2% year-over-year, with CDS declining less than -1% and NPA increasing nearly +14%.”

“Low-value units, including charities and municipalities declining -4%”.

Purple Wave

This is a recent acquisition of a specialty equipment provider (Ritchie bros competitor).

They note: “Purple Wave has driven double-digit gross transaction value growth year-over-year for the trailing 12 months period ending October 31, which significantly outpaces industry growth in the equipment auction marketplaces they serve. This impressive growth demonstrates the value of our partnership and what it brings to the market.”

International

Showing progress in converting more cars in Germany to the consignment model.

Costs

Facility-related costs per unit increased +4% y/y from the prior year period

“This normalized increase in per unit cost reflects our ongoing investments in expanded operational capacity to support our continued growth.”

Other

Notes China isn’t a meaningful importer or exporter of cars for Copart.

Tariffs could make the value of cars in the US higher because they are already “landed here” and can avoid the tariff.

Could also increase the value of used cars in the US.

Title Express

Now managing titles for over 1mn cars annually, all on behalf of insurance carriers.

This further embeds Copart into the insurers' work flows and speeds up time to process a salvaged vehicle.

Business Commentary.

Copart continues to execute superbly and there is little to criticize. While they have been increasing investments internationally and that has weighed on earnings, this is exactly what a long-term investor would want them to do to extend the growth runway.

They also continue to increase their competitive moat even more with the expansion of tools like Title Express, which removes a critical operating function from the insurance companies to Copart, making it all the harder to ever remove Copart from their work process.

Additionally, continual improvements in the speed at which they handle CAT surge volume will only allow them to continue to gain share, despite their already dominant position. Their competitor IAA primarily hangs onto to volumes out of fear that the insurance companies will be stuck with only one salvage vehicle service provider.

Growth in Copart Blue is also exciting as these higher end cars (compared to literal junk) can carry higher ASPs and boost Copart's profit per unit as it the same, or sometimes less, work to sell a higher end car than a salvage vehicle.

Purple Wave, a recent acquisition focused on specialty equipment—or also called “yellow metal” because it is primarily construction equipment—has shown some promise as they note they are taking share in this space. Ritchie Bros is the dominant player here but it is possible they are distracted after a recent management shuffle and their acquisition of IAA. It certainly wasn’t in our base case that Copart grow a material business here, but if anyone has the competence to do it, it is Copart.

Generally, the only thing an investor can complain about is that the market valuation continues to increase and the assumptions needed to pencil out a double digit return have gone up with it. (More details in the valuation section).

This has created a bit of a problem for management as cash has piled onto their balance sheet to the tune of $3.7bn. Historically, they have been highly selective and aggressive with stock buybacks, only repurchasing shares when they felt they were very depressed. If this continues to be the case, it seems likely a dividend could be coming in the future as their growth opportunities only consume about 40% of operating cash flow.

On the call, CEO Jeff Liaw defended the long-term growth factors helping Copart as many investors question their terminal value amid a small roll out of AVs in select cities.

In the call they drew out 4 factors of growth:

1) Population growth of about 1% annually since 1960

2) Vehicle miles driven, which has grown close to 2% annually since 1960

3) Accident rate declines, which is an offset. Jeff Liaw notes:

4) Total loss frequency, which is their main growth driver, has grown more than 4 fold since 1990. Liaw said:

He also notes that overtime uninsured drivers fall, which means the insurance companies have more driver claims to handle. While the United State is fairly mature in regard to this factor, many other international markets (like Brazil) still have low rates of insurance.

We have two comments on their future long-term trends. The first is that AV as a risk is generally overblown. With 300mn vehicles in the U.S. and only ~15mn vehicles sold annually, it would take 20 years to replace the car stock of the country with AVs, and that assumes every car sold today has fully working AV technology.

Of course there will be a slow ramp up in reality, which means a long period of time when both AVs and non-AVs are on the road. This could just as likely increase loss frequency more as these advanced cars get totaled easier. International would take even longer as many people can barely afford the cheapest of vehicles today in emerging markets.

Our second comment is that for several decades the increase in the rate of total frequency has overpowered the decrease in accident occurrences. As cars get more technology they avoid more accidents, but when they are in an accident, it is much more likely to cause more damage because of the increasing complexity of vehicles. Jay Adiar once noted that he thought loss frequency could hit 35-40% (from 21% today).

While this is possible, we do wonder at if at one point the anti-accident features become good enough to overweigh the increases in loss frequency so this becomes less of a tailwind in the future. This wouldn’t be our base case anytime soon, but eventually it seems very plausible and is a key risk to slower growth for Copart. An investor should keep these factors in mind when thinking through what assumptions they are comfortable with.

With this context, we will now move onto valuation.

Valuation.

Below we update our reverse DCF and provide some other ways to think about valuation.

First we start by getting an estimate of current owners earnings. To do that we need to get a sense of growth versus maintenance capex. If you ever wondered why Speedwell reads every earnings transcript when analyzing a business, look no further then the below example. Copart only ever talked about maintenance capex once and it was in a 4Q 2004 earnings call, about 20 years ago.

As we noted in our original report:

“We consider D&A to be a fair, if not overstated, estimate of maintenance capex… In 4Q04 they disclosed that maintenance capex would be $10-15mn for 2005, whereas D&A was twice that. This comes out under 25% of total capex for the year being categorized as maintenance capex. A salvage operation requires very minimal non-recurring capex for upkeep and would seldom require a remodel or refresh like retail stores commonly do.”

As Copart is a larger organization today than they were back then, we can expect a larger portion of overall capex to be directed to maintenance capex. We assume that D&A is equal to maintenance capex, which means that about 35% of capex is spent on maintenance.

Frankly, this is probably an overestimate as they run literal junk yards, so there is almost zero need to for upkeep. However, there is tech spend and equipment that needs to be periodically updated. With over 250 yards today and our estimated maintenance capex budget of about $220mn, that comes out to over $750k per yard, which seems more than reasonable.

Together with their TTM operating cash flow (excluding SBC) of $1.5bn gets us estimated owner earnings of about $1.3bn. This has grown at about a 12% CAGR since our original report in May 2023. This is about in line with the high range of assumptions we had for our reverse DCF.

At a valuation of $55bn, they are trading at 42x owner earnings. This is up from the 33x owners earnings multiple implied when we published our report a year and a half ago. In total our owner’s earnings estimate is up about 18%, but the stock is up about 50% over that period.

Growth has been toward the high end of what we would have expected, and they do seem to have as much confidence as ever in their international operations growth and the tailwinds helping them.

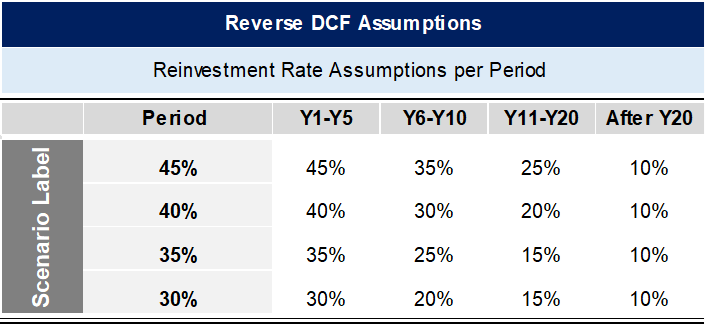

When updating our reverse DCF, we decided to simplify it to make it more intuitive. The original reverse DCF ran off of organic growth of owners earnings with incremental “growth” earnings tied to a reinvestment rate and an ROIC assumption. While this makes sense, looking at it now it seems a bit too academic and is hard for an investor to quickly conceptualize. We simplified the reverse DCF to just run off an operating cash flow growth estimate and a capex assumption.

Looking at historical operating cash flow (OCF) base rates we see it has grown at a ~18% CAGR over the past decade, 16% CAGR since 2019 and a 11% since 2020 (2020 was a very strong year for them). On a TTM basis though, OCF grew just 7%, but in this last quarter it reaccelerated to +28% y/y. An investor could draw a variety of conclusions from these results, and either assume a convergence back to historical base rates or a more conservative figure, in line with last year's performance.

We will sensitize around 4 growth scenarios ranging from low to high.

Capex as a % of OCF is currently 40%. We will sensitize this from 30-45%. When looking at the results an investor should assume a higher rate of capex if they are gravitating toward the higher growth scenarios.

Below we show the reverse DCF outputs. This is the implied discount rate for each assumption, or can be thought of as what an investor would earn if they owned the entire business and received all excess cash flows. As a reminder, these values are implied based off today's market price of $60 a share and the assumptions we input into the DCF. (See this memo for more on the reverse DCF).

It is on each investor to make their own judgement about the risks they see inherent in each investment opportunity and which assumptions they are comfortable making and whether the returns justify the risks.

Another way to think about valuation is with a $55bn EV today and TTM FCF of $950mn, that is currently a 58x FCF multiple. If you assumed a 25x exit multiple 10 years from now, then you need 6% FCF growth to break even. (We ran a seperate reverse DCF to get this figure). That means 6% growth is fully priced in today and an investor only makes a return to the extent Copart can grow cash flow above 6% annually.

So if Copart grows FCF 15% a year for 10 years and you are comfortable with a 25x multiple, your return as a investor would be ~8-9% annually. ($3.8bn in FCF x 25 plus $22bn in cumulative cash generated over 10 years, which we assume is paid out... if it's not then the return is closer to 7%).

Remember though, this assumes a 10 year FCF growth rate of 15%, which will continue to be harder to achieve as they get larger. And while not it is not out of the relam of what Copart has historically acheived, an investor has to decide if they are being compensated adequately for making such an assumption.

If you want to learn more about Copart you should start by becoming a Speedwell Member so you can get access to our Extensive Research Report. This is the most comprehensive single report written on Copart and covers everything from Willis Johnson founding the company to risks and growth opportunities facing them today.

A Speedwell Membership will also get you access to all of our other research reports (see the full list here) and on-going updates, most of which will be for paying members only.

Reach out to billing@speedwellresearch.com if you need Speedwell to onboarded with your investment firm in order to expense it.

Other Copart Sources Include:

*At the time of this writing, one or more contributors to this report has a position in CPRT. Furthermore, accounts one or more contributors advise on may also have a positions in CPRT. This may change without notice.