META, ETSY, and FND 3Q24 Business Update

Flooring, Digital Ads, and Unwanted Handmade Goods. Plus an Update on Speedwell.

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

We will provide an update on Meta, Etsy, and Floor & Decor through our podcast too. Follow our feed here (Apple, Spotify).

This is an earnings update on three of our covered companies. It is free, but in the future most updates will be paritally or fully paywalled. We had recent updates on CSGP and EVO too that you can read here (partial paywalled). Please consdier becoming a full Speedwell Member here to never miss out!

Quick Update on Speedwell Updates.

Before we get started, we wanted to write a bit on how we think about earnings updates going forward. We had recently committed to providing Speedwell Members at least 2 updates annually on each company we cover, but we have decided that we will provide at least some commentary each quarter for every company we cover.

However, the length of the updates will greatly vary based on what is going on in the business. There may be many updates where we post some figures, key highlights, and high level thoughts, but do not get into the nitty-gritty quarterly drivers. We felt that there are plenty of sell-side analysts that do this and we didn’t simply want to replicate the way they do updates.

The value we see Speedwell providing is taking a longer-term view and not getting caught up in various quarterly factors. While we may comment on several short-term variables if they misconstrue the true underlying trends of the business, the aim is not to explain every little trivial variation that could impact the 12 weeks of a business’s financial results.

We also will seldom comment on expectations. This is because they don’t matter and we reject the framing that if a business “missed” revenue or earnings it implies they have made a mistake or are facing headwinds. While this can often be true, it is not always true. And the times it tends to not be true are the times that tend to matter the most.

Meta missed many revenue and earnings expectations for several quarters in 2022 as they not only increased their expenses to address ATT and TikTok, but also decided to forgo revenue by focusing on Reels which monetized much less than the newsfeed. This was a business decision that impacted quarterly financials, but the idea that they “missed” that quarter suggests they should have done otherwise.

In contrast, Starbucks raised their prices and diluted their loyalty program which helped boost their bottom line, but now are scrambling to reverse these decisions by “providing more value” with combo purchase deals. Nike pulled back production of their iconic Jordan shoes because they overproduced too many different variations and were becoming too tired. In each quarter, these decisions would have shown up as improvements in their financials, but of course we can now say they appear to have come at the cost of the longevity of the business.

There is an idea that investors are greedy and just want a company to generate as much profit as possible. Perhaps there is truth in that, but with a huge caveat. A long-term investor wants to maximize profit across the entire life of the investment, not a single quarter! The best companies are those that can generate sustainable profits year in and year out. Applauding management for a single quarter’s “beat” or reprimanding them for a “miss” not only encourages myopic thinking, it also errors in implying that the single quarter’s financials were correlated to good business decisions, which may not be clear for several quarters, if not a few years, if they were.

Having said that we are not opposed to commenting on the narrative or investors’ “fears” around a stock because we believe addressing those concerns can help an investor have better judgement in making a decision. Additionally, we have no problem comparing results to management’s guidance, but we also believe there is limited value in that (we will save a diatribe on that for another time though).

With that preamble, this piece contains earnings from three of our companies: Floor and Decor, Meta, and Etsy.

Floor & Decor.

Floor & Decor reported 3Q24 results and their stock was up +2% to $103 the day after releasing results.

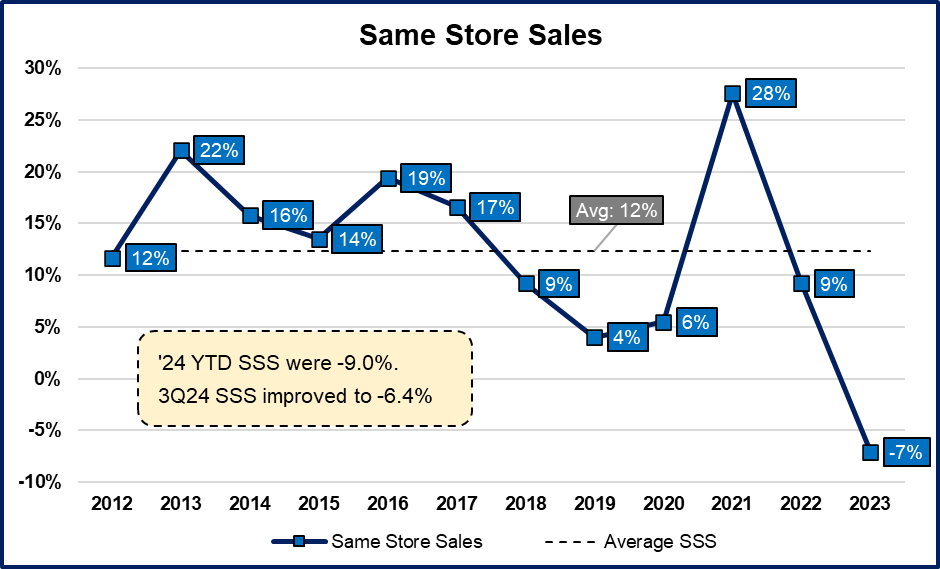

Sales increased 0.9% y/y, marking the end of 3 consecutive quarters of no growth.

However, same store sales (SSS) were -6.4% y/y. This is an improvement compared to 2Q24 and 1Q24 SSS of -9% and -11.6%, respectively.

The difference is the 20 stores they opened YTD. Most of these were backloaded in the year with 11 opening in 3Q24 and 8 opening in September. They are on plan to open 30 for the year with another 10 in 4Q24.

Looking at the components of their -6.4% SSS, we see that transactions were -4.1% and average ticket size was -2.4%. This represents an improvement of +80bps q/q for transactions and +190bps for avg. ticket.

In total they now expect $4.4-4.43bn in sales for the year (SSS range of -8.5% to -7.5%). This is a reduction of $60mn in sales at the high end of the range from last quarter.

Gross margins improved to 43.5%, +130bps y/y primarily on favorable supply chain costs and mix shift to more “better and best” products.

Below Tom Taylor notes that they continue to expect some gross margin expansion. In contrast to prior comments like in 2Q23 when Tom noted “we continue to successfully execute our plan to strategically reduce prices on specific SKUs, while at the same time growing our gross margin rate”, this quarter there was no mention of passing off savings to the consumers in the form of price reductions.

In general, there has been a renewed focus on controlling costs.

Tom Taylor notes below that they learned to be more disciplined and will continue to be as sales rebound. Like Meta with ATT and Airbnb with Covid, Floor and Decor is responding to the very soft homes sales backdrop by focusing on reducing costs and improving efficiency. Similarly, when the housing market turns in their favor, these changes should result in an increase in operating leverage.

While it is not the best comparison because of the timing of when the stores are open, we can see evidence of this efficiency in OpEx per warehouse store. In 3Q24 they had 245 warehouse stores and avg. OpEx per store was $1.71mn versus $1.84mn for their 207 warehouse stores in the year prior (we are including pre-opening costs in both). This 7% reduction in OpEx per store shows how they are becoming more cost efficient.

(However, there are other factors that can obscure this figure. For one, they note that 25% of their stores are running 25% at minimum hours--and we aren’t sure what this figure would be for the comp period).

Nevertheless, despite the renewed costs focus, operating margins are just 5.9%, or down -180bps y/y (7.1% excluding pre-opening costs). This is largely due to the operating deleveraging from same store sales being down.

While we will focus on steady-state earnings instead of GAAP, EPS for the quarter was $0.48, -22% y/y. With slightly improved trends, management raised their EPS guidance floor for the year from $1.55-1.75 to $1.65-1.75.

Store Model.

There was some interesting commentary around how they are thinking of growing their store count and their store model.

When asked about the Year 1 ROIC and initiatives to reduce the capital intensity of new stores, Tom Taylor responded:

Trevor Lang added:

They are now planning for just 25 stores in 2025, this is roughly half the rate they said they would grow store count at the beginning of 2022. From their 2021 annual report: “We intend to grow our store base by approximately 20% annually for the next several years”.

While we can understand their reactivity to the poor macro backdrop, on the other hand, if they have confidence in their 500 store long-term target (which they reiterated on this call) and their ~$30mn of mature sales per warehouse store, would they really slow the store builds? If Floor & Decor is going to be around for decades, then they will operate in a variety of different macro contexts, some much worse than the current and many much better. As long as they have the liquidity and can grow new stores at a small profit per unit, then why not continue to grow in line with the original plan? And is “right-sizing” stores about optimizing for the long-term or saving money in the short-term?

Not staying on the long-term plan they laid out a few years prior seemed a little more contradictory in the context of them talking about “using this period of disruption as an opportunity to grow market share”.

Perhaps at the extreme is RH’s Gary Friedman who hasn’t slowed down their growth plans at all despite the same poor macro backdrop and a tighter liquidity position. On the 1Q24 call Gary noted: “interest rates once again exceeded 7% post the hawkish Fed commentary… while aggressively investing during a downturn put pressure on short-term results, it also positions us to capitalize on the long-term opportunities that present themselves during times of disruption and dislocation”.

On the one hand Gary’s unencumbered focus on the long-term of the business, despite brutal short-term results, is how you optimize for long-term shareholder value. On the other hand, it scares the crap out of many investors who are less trusting of the long-term vision. Adding essentially a levered stock buyback to the mix didn’t help make these investors feel any better either, but the thing you cannot critique is that he 100% believes in his vision and acts accordingly.

Of course a Gary Friedman level of intensity is going to be rare, but in contrast the avoidance of new markets and “rightsizing” the size of new stores does make one wonder if management is having some doubts about the long-term model. To be clear, we are not suggesting they should become more aggressive at this point in time (or run the business like RH), just that they don’t need to pull back from their prior stated long-term plans in response to the housing data. Results are going to be poor in the short-term anyway, so in the words of Ben Horowitz “If you are going to eat shit, don’t nibble”.

We will now move onto to our general Floor & Decor business commentary after sharing some other notables on the quarter below.

Notable Comments.

Macro backdrop improving

“Looking ahead, the Federal Reserve finally began its much anticipated easing cycle in September of 2024, which leads us to believe that existing home sales and hard surface flooring spending could potentially grind higher over the next 12 to 18 months. However, our optimism is tempered by the recent increase in 30 year mortgage rates. Moreover, September existing home sales declined 1% sequentially and 3.5 percent year over year”. – Tom Taylor

As a reminder, Floor and Decor is much more exposed to existing home sales than new home sales because you are more likely to replace floors on an existing home than a new home, and mass home builders tend to buy directly from the manufacturer.

Hurricanes impacted some stores and they had to close them.

Historically strong weather events are positive for Floor and Decor as there is floor damage that needs to be replaced.

They note there could be a benefit over “multiple quarters in 2025”

Long-term 500 store goal unchanged

25 stores in 2025 now and said they can push those out if needed. Already plan on them being backloaded in the year.

Total Sales +0.9%

SSS – 6.4%

“We are encouraged that the sequential rate of decline in our fiscal 2024 comparable store sales improved as we cycle past easier comparable store sales comparisons.” SSS declined -11.6% in 1Q24, -9% in 2Q24, and -6.4% in 3Q24

On a monthly basis for Jul, Aug, Sep, SSS declined -7.6%, -6.4%, and -5.4%, respectively

“And so our transactions are basically in line with where we would have exited 2019 from an average ticket were higher, but that's because of all the inflationary things that have happened post 2019. So when you think about that, our ticket is higher, but transactions are almost flat. And so that is burdened with cannibalization as we have opened a lot of stores during this down macro environment. But we had transactions against that time period on a per store basis are relatively flat today from where they were, which historically in our long term algorithm that we would have given back at the Analyst Day, we would have said mid to high single digits driven by mainly transactions. So it tells you that we believe there's a lot of pent up demand in some of those kind of things within the stores given the fact that we are relatively flat to where we were back in 2019.” – Bryan Langley

Connected customer sales now 19% of total

Improving search, adding “inspiration” and user generated content

Designers

“3rd quarter design total sales penetration increased significantly from the same period last year.” – Trevor Lang

Enhanced design scheduling and functionality

Pros are now 48% of retail sales

Minimum engagement targets

Local outreach, Local marketing, CEM store tours and meet & greet

Prioritize bilingual support

Hosting Educational events (425 attendees in 3Q24) which lead to increases in purchases, particularly installation materials

Commercial

Spartan continues to grow faster than company average

Focused on the commercial floor segment for healthcare, education, senior living, and hospitality

“Spartan Surfaces aims to become a disruptive leader in the specified commercial flooring industry by establishing a comprehensive nationwide sales network. This network would prioritize high specification products and leverage strong relationships to provide superior availability, delivery and service across the country. Over the next several years, we will continue making investments, sales representatives growth and infrastructure to build out to support our growth at scale and achieve our market share and profitability objectives.” – Trevor Lang

Costs

Gross Margin +130bps y/y to 43.5%

Primarily due to favorable supply chain costs

Two distributions centers, 1 in 2025 and 1 in 2026 will weigh on gross margins

Sales, selling, and store opex +240bps y/y to 30.3%

Exceeded management’s expectations due to managing payroll and other store costs

Competitive Environment

“I would say that there will be less competitors as we come out of this cycle. There we've already seen some closures but then you heard Lumber Liquidators had to close stores. We had noise of distributors closing, noise of independents closing. So I believe that there'll be less competitors when we enter the market. I think that we'll continue to have to deal with home improvement centers ebbing and flowing, getting better, getting worse and we'll continue to have to deal with that like we always have. I don't think that's too much different than pre COVID. And I don't think the independents have changed so much in how they go about their business. So I think the competitive advantages that we have today are similar to the competitive advantages we had pre COVID, and I think they'll be the same as this bubble passes.” – Tom Taylor

Business Commentary.

Floor and Decor generally continues to execute on their long-term vision and are now almost half way to their 500 long-term store target. While we noted we thought it was unnecessary to slow down growth in response to the macro backdrop, they still are planning on adding another 25 new warehouse stores next year (about 10% y/y unit growth), and we still have a lot of trust in management.

They may be a little off on their housing predictions (as evidenced by multiple downward guidance revisions), but the business continues to perform well despite the headwinds. In contrast, a competitor—Lumber Liquidator went bankrupt—and other public peers have performed worse than them. Most impressive is that now 48% of their business is represented by Pros. This has grown from 30% at the beginning of 2022.

This is important because Pros are in the business of installing flooring and thus are recurring customers. Additionally, they tend to influence homeowners to purchase at Floor and Decor. They have grown this business by making it a priority with educational presentations (which result in an increase in pro sales, especially installation materials), as well as having the Chief Executive Merchants of each store give meet & greets and store tours with pros. They also have emphasized bilingual support and local marketing.

Additionally, their new focus on cost control is much welcomed and we would expect increased operating leverage when the flooring market improves. Their gross margin improvements put them amongst their highest ever gross margins.

By and large, this was another quarter of them executing on the long-term vision, but with a dose of short-term caution. Not only will they benefit from a more normalized environment (existing home sales at 3.8mn, down from 6.5mn in 2022 and 5.3mn in 2019), their focus on expense discipline and operational improvements should result in lasting operating model improvements, beyond the downturn.

Big picture the goal remains unchanged: 500 warehouse stores at $30mn per store and a mature operating margin of 15%. After 20% tax, this is around $1.8bn in NOPAT (and doesn’t include their commercial business, see notes above on Spartan). This compares to a market cap today of $11bn. So if an investor believes in the long-term target, the question is simply: when are they going to get there?

Meta.

Meta reported 3Q24 and their stock was down 4%, but is still up 64% YTD.

Revenues were +19% y/y, driven by impression growth of +7% y/y and ad price increases of +11% y/y.

As a reminder, the dynamics of improved ad targeting are to first decrease ad prices, followed by a subsequent increase. This is because as ad targeting improves, conversions increase, and thus an advertiser shows fewer ads to get the same result. This frees up ad slots for other advertisers. If it took 100 ad impressions to get a sale before and now it takes only 80, those are 20 ad impressions that are free for others to bid on. This has an impact of effectively increasing ad supply and thus the price of ads drops.

The dropping ad prices means that the return on ad spend (ROAS) improves. With a higher ROAS, more advertisers enter the bidding (or existing advertisers increase their budgets) as they can now profitably acquire sales. As more advertisers enter the auction, they bid up the price of ads, which drives the ROAS back down.

This process can basically continue as long as Meta can persist in ad targeting improvements. While if we rewind a couple years ago that was very much drawn into question with the reduction of data they could get from ATT, today their solutions to ATT (Conversion API on the server-side and Advantage+) seem to not only have returned them to strong growth, but together with their huge capex spend, point to a long runway for targeting improvements.

(Note: As we talk about in our report, targeting and measurement are different. The former is about matching an ad to the right person, while measurement is about knowing what ads were effective. Both were impacted by ATT and both have improved since. When we say “ad targeting”, we are also referring to measurement).

Family of Apps (FOA) Revenue was also up +18% y/y, which represents an addition of $6.2bn in revenues y/y. This is a slight deceleration from last quarter where FOA grew +22% y/y. They are guiding total 4Q24 revenue to $45-48bn, representing +12-20% revenue growth.

FOA segment operating margins were 53.7%, +380bps q/q. They continue to show incredible operating leverage. +67% y/y or even more incredibly, +152% q/q. (FOA EBIT grew $2.4bn q/q versus revenue growth of $1.6bn q/q).

It is not crazy to think they could approach 60%+ EBIT margins one day, however, at the same time the current profitability of this segment is likely overstated.

YTD D&A is 9.5% of revenues. However, capex has run closer to 21% YTD.

A lot of their revenue growth has been the byproduct of their costly server and data center investments, which help support their AI advancements that have stitched together lost ad signal and improved targeting. However, their current D&A run-rate doesn’t reflect the level of these investments. It is true they neither break out D&A by segment nor capex, but we have a suspicion that the majority of this capex was to support FOA, even if it could have dual uses (like supporting Llama and their generative AI initiatives).

As their capex to D&A ratio is >2x, this will be a margin headwind to FOA profitability. However, with even more AI-driven ad targeting improvements, plus the potential for engagement and user growth, it may be overcome. Nevertheless, it is worth being aware of.

Reality Labs (RL) continues to be a burden to earnings, with 3Q24 losses of $4.4bn. But there is more optimism than ever before that they might actually make a hit consumer product, with the Orion showcased recently. This could position them for what many would have considered unfathomably just a couple years earlier—actually making a profit in this segment. Of course, it is likely years before that happens with RL losses nearing $20bn for the year, but some investors are a little more comfortable with at least contemplating that possibility.

Business Commentary.

This was another quarter of strong execution both on topline with FOA revenues +18% y/y and margins expanding to 54%. Zuckerberg noted previously that he didn’t know what the ROI for their AI spend would be, but he was confident that there would be a return. With each quarter that passes, we have to keep raising the floor on what that ROI can be.

Despite several quarters of strong growth, they seem to still have more runway than in recent memory to continue to improve ad targeting. Of course, as they keep getting larger, it gets harder to drive meaningful revenue. Still though, they seem to have no shortage of experiments they are running that are driving improvements, and that is before touching generative AI, which can create various ads on the behalf of the advertisers and continue to test and improve them.

Furthermore, AI advancements can improve recommendations which can increase the time spent on their apps. Additionally, they are experimenting with AI-generated content, which could also increase the length of user’s session if they can make it more compelling.

When we first wrote our Meta Research Report, we noted that there was four drivers to revenue: 1) # of users, 2) time spent per user, 3) ad load, and 4) ad price. Today every variable seems to be trending towards improvement—even # of users in North America, which was a major concern a few years ago. And this is Facebook Blue, not Instagram, that they said is trending positive with young adults in the U.S.

Additionally, Tiktok will potentially be banned in United States and all of the AI developments required to compete in digital direct response advertising (not to mention increasing regulation and cost to moderate) suggests there may never be another start-up that can be competitive against Meta without a “Masayoshi Son—WeWork” sum of money.

Their AR/VR efforts are also beginning to look promising, but it is too early to claim any sort of success. However, this remains a potentially very valuable call option. Other AI developments could also spin off businesses that Meta—or investors— haven’t envisioned prior like charging for AI agents to interface with customers.

With the stock up >330% since the beginning of January 2023, a lot of these improvements are starting to be priced in. And in contrast to when we ran our first Reverse DCF in January 2023, which showed an investor could get a historic stock market return assuming Meta grows just 0-3% growth, at ~25x 2024 earnings today an investor would likely need continued double digit growth in order to rationalize an investment.

(We will update our reverse DCF for members soon, but Members Plus can run it themselves in the meantime).

Other Notables.

Usage

3.29b daily active people, +4.7% y/y

“Seeing rapid adoption of Meta AI and Llama”

U.S. is one of WhatsApp’s fastest growing countries

“On Facebook, we continue to see positive trends with the young adults, especially in the U.S.”

Threads us almost at 275mn MAU

“continue to be on track towards this becoming our next major social app.”

Revenue

Revenue growth on an advertiser basis (different than revenue by user disclosure)

Strongest in North America and Europe at +21%.

Rest of World +17%,

Asia Pacific was the slowest-growing region at 15%, decelerating from our second quarter growth rate of 28% due mainly to lapping a period of stronger demand from China-based advertisers

FOA other revenue was $434mn, +48% y/y due primarily to business messaging growth from WhatsApp

Click-to-message ads are the focus for monetizing WhatsApp

“ Impression growth was mainly driven by Asia Pacific and Rest of World”

“Pricing growth was driven by increased advertiser demand, in part due to improved ad performance. This was partially offset by impression growth, particularly from lower monetizing regions and surfaces.”

Opportunities to grow ad supply on lower monetizing surfaces like video.

New modeling approaches, for example a techniques that enable our ad systems to consider the sequence of actions a person takes before and after seeing an ad

This one change has already driven a 2-4% increase in conversion in testing

Product Development

Facebook, is seeing strong results from the global rollout of their unified video player in June.

The new experience plus predictions drove a 10% increase in time spent within the video player

Reels seeing continued traction

More than 60% of posts recommendations now are original content in the U.S.

Last year developed new ranking model architectures capable of learning more effectively from significantly larger data sets.

Tested this with Facebook Video and now exploring if this new architecture can work on other services

Working on cross-surface recommendations (i.e. what someone’s video recommendations can say about feed recommendations. Also sounds like this is across app).

Advantage+ solution seeing strong retention with new tools for AI generated image expansion, background generation, and text generation

Search

“Meta AI draws from content across the web to address timely questions from users, and it provides sources for those results from our search engine partners. We've integrated with Bing and Google, both of whom offer great search experiences. Like other companies, we also train our Gen AI models on content that is publicly available online, and we crawl the web for a variety of purposes.”

AI

“we're seeing AI have a positive impact on nearly all aspects of our work from our core business engagement and monetization to our long-term road maps for new services and computing platforms.”

Meta AI has 500mn MAU

AI-driven feed and video recommendations drove an 8% increase in time spent on Facebook and a 6% increase on Instagram this year alone

>1mn advertisers used GenAI to make 15mn ads last month

Businesses using AI image generation tools seeing +7% increase in conversion

“Llama 3 models have been something of an inflection point in the industry”

“Training the Llama 4 models on a cluster that is bigger than 100,000 H100s or bigger than anything that I've seen reported for what others are doing.”

More adoption of Llama means we can incorporate updates for our own uses and that chip designers like Nvidia and AMD will optimize their chips more for Llama, which also benefits Meta

RL

“Demand for the glasses continues to be very strong. “

The new clear addition that we released at Connect sold out almost immediately and has been trading online for over $1,000.”

Working closely with EssilorLuxottica for new models

Orion is their first full holographic AR glasses.

“We've been working on this one for about a decade, and it gives you a sense of where this is all going. We're not too far off from being able to deliver great-looking glasses to let you seamlessly blend the physical and digital worlds so you can feel present with anyone no matter where they are.”

As noted prior, we aren’t going to write in-depth updates every quarter for every business, but for more on Meta’s 3Q24, check out Mostly Borrowed Idea’s update here. He does a great job pulling out many insights from the earnings call (and is also usually quicker than us!).

Etsy.

Etsy reported 3Q24 and was up +7%.

We haven’t written about Etsy since our original Extensive Research Report, but we spoke about them in this podcast back in February.

We made a few key points that I want to rehash before getting into the results.

The problems that they talked about included search, shipping times, separate charges for shipping, and a generally inconsistent experience across sellers.

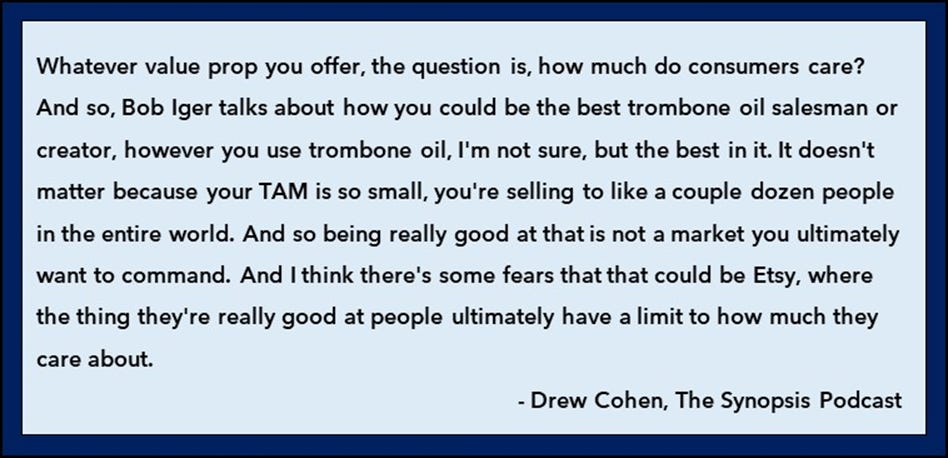

While they made strides in addressing all of these, the ultimate problem that Etsy is facing is that their core value prop—handmade—people don’t care that much about.

In 3Q23 Josh Silverman noted “there's no question that Temu and Shein are having an impact in the market. You don't get that big that fast without taking share from many people. And I think we and most players in e-commerce have had some impact.”

But then he goes on to say that “If I had to think about what is the polar opposite of Etsy, I'd probably get pretty close to Temu”.

The problem with this is that even if you assume that Temu was distorting the ad market with their large ad spend, it still implies a problem with their business. (There is some credence to their claim, as Meta noted a slowdown of growth to +15% from +28% in Asia on a tough comp period of Chinese-based advertisers, but ad prices in Asia Pacific were still +8% y/y. Generally, it seems unlikely that one ad player could materially distort the market).

Either way, the issue is that a success-based advertiser basically only pays when they get an action they desire. In theory, each key word is only being bid on by advertisers with similar products. (Etsy primarily advertises on Google). In other words, if someone spent a ton of money promoting a streaming service it shouldn’t impact the cost of acquisition for athleisure company Vuori because they are bidding on words like “exercise pants”. However, if Alo, another athleisure company, aggressively spent on ads then perhaps it could (although the digital ad market is so big that even that is doubtful).

But, even if we believe Etsy that it was true that Temu distorted the ad market, then the problem is it suggest these products are seen as somewhat substitutable in consumers eyes. If a customer searches for “pillow”, for Etsy’s sake they better not be indifferent between a special handmade pillow and cheap mass-produced one from Temu.

If consumers do not care about “handmade” then Etsy has built their entire value prop around something that is not an important preference for consumers. Unfortunately, there is building evidence that that is the case. Other preferences like lower prices and faster shipping speeds tend to be more important considerations in most consumers purchases.

Since we first put that theory forward and generally shied away from how much consumers' value Etsy’s value prop, the business has continued to struggle.

(For the record, it is not that our analysis followed the stock price: the stock price was $70 when we originally published the report in September 2023 and was ~$75 when that podcast came out in February 2024).

Etsy 3Q24 Results.

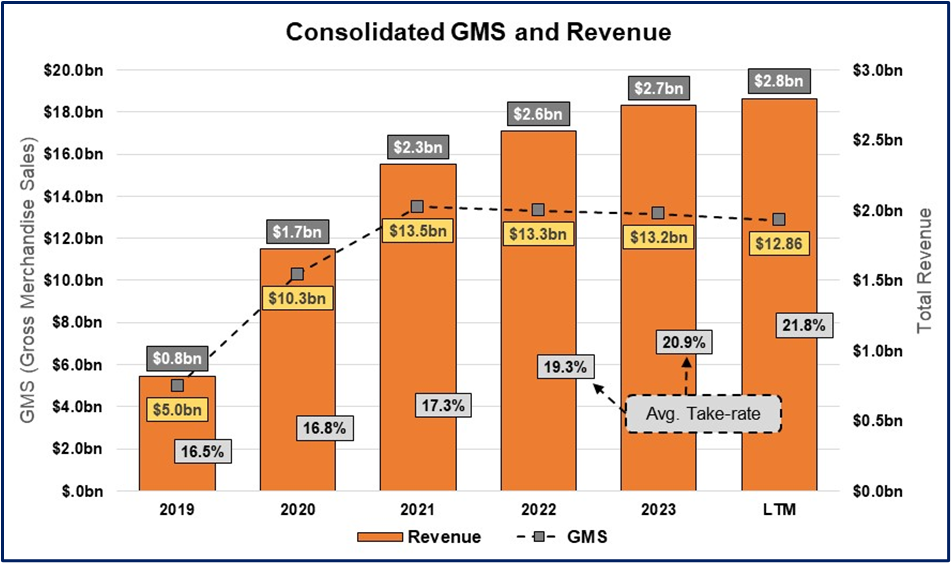

Moving to 3Q24, Etsy marketplace GMS (gross merchandise sales) was down -6% y/y and active buyers decreased -0.4% y/y to 91.2mn.

Habitual buyers, their most loyal who bought more than 6 times a year, fell -4.8%.

However, take-rates improved to 22.7%, +70bps q/q, which helped drive revenue growth of +4.1% y/y.

We can see the trend of GMS and revenue growth below. Every year take-rate has gone up to help boost revenue growth, but GMS continues to fall.

While Etsy guides to adjusted EBITDA, the problem we have with this metric isn’t actually adding back the D&A. D&A runs about 2.5x higher than their capex plus capitalized software costs, so adding that back (and then subtracting out capex) is fair. However, their ample SBC, which runs at close to 11% of revenue must be taken into account.

So instead, we look at them on an operating income basis, with the understanding that normalized margins are probably 3-4 points higher than what GAAP shows below.

As we can see it’s not pretty. After peaking at 25% margins, they have continued to suffer margin compression, despite layoffs and a focus on cost cutting.

S&M is 29% of revenues YTD compared to 26% in the same period last year. Despite the increased marketing investment, growth was negative. R&D is 17% of revenues YTD, down from 18.4% in the same period last year. We will pick back up on mature assumptions after some general business commentary.

Business Commentary.

We fully believe that Etsy has a unique value prop and it would be extremely hard to compete against them in their core offering of a wide selection of “handmade” and idiosyncratic goods that are hard to find anywhere else.

As we noted, the problem with Etsy isn’t that they don’t have a unique offering, it’s that people don’t seem to care much about what that is.

Also in contrast to the business’s recent performance, we actually think very highly of Josh Silverman. From when he took the business over in 2017, he has implemented many changes in the organization and focused on revenue generative R&D. (See our Extensive Research Report for a full history).

And make no mistake, there is still opportunity ahead of Etsy. There is a large friction point of people searching on Etsy and not seeing what they want quickly, so they leave. They have been working on improving search for some time, but with new AI advents, it seems more possible for them to make real headway on this soon.

Many consumers do not want to sift through multiple pages of items to find something they like, but if Etsy could instantly surface it for them, then they have a much better chance of winning that sale—even if it does mean longer shipping and a potentially inconsistent experience. Additionally, AI agents could help the customer service aspect and generative AI can make listings look more distinct.

Silverman has helped lead a very experimental culture, which is quite good at finding places to squeeze more improvements from Etsy. As he noted on the 3Q24 call, “in one experiment, we drove 3 million incremental app downloads from placing a prompt on the signed out listing page on mobile web”. This is important because getting a buyer to download the app increases their lifetime value by 40%.

All of these changes could absolutely help drive growth and profitability, but ultimately, we think the key problems they need to solve is to get people to care more about handmade and idiosyncratic items, and less about shipping, ease of ordering, and price. That is not easy to do. This problem reminds of a Buffett point:

As an investor you have the luxury of deciding what assumptions you feel comfortable making and, of course, making no assumptions if you do not feel like you have basis too.

Valuation Thoughts.

With their recent financial performance, it is hard to have confidence in mature margins because results could deteriorate further if they cut marketing. We originally assumed a mature margin of around 25% (with a range of 20-30%), which still seems feasible, but a conservative investor would likely want to see more stability in their business before having confidence in such an assumption.

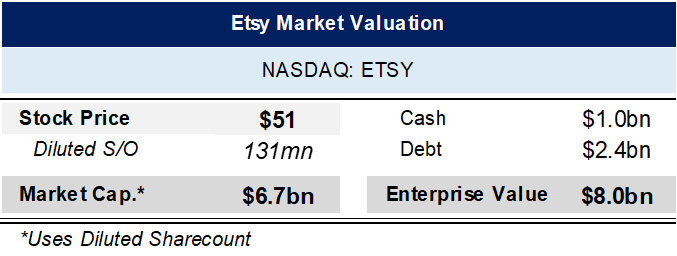

At 25% mature margins and about $2.8bn in revenues, they would have about ~$550mn in NOPAT. At today’s enterprise valuation of $8bn, that is a ~14x multiple. An investor must make their own judgement on whether they deem that to be attractive, but we should point out that if they can’t stabilize at their current business at an elevated cost structure, then there is less reason to believe they could do so with less spend on marketing and R&D.

We hope you enjoyed these business updates! Speedwell Members will not only receive regular business updates, but also our Extensive Research Reports and Exploratory Researcg Reports. Become a Speedwell Member below:

The Synopsis Podcast.

Follow our Podcast below. We have company episodes, which are multi-hour deep dives on a single business on META, FND, and ETSY, among many others. Just look for the episodes that start with “Company” or check out our podcast directory here.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

*At the time of this writing, one or more contributors to this report has a position in META and FND. Furthermore, accounts one or more contributors advise on may also have a positions in META and FND. This may change without notice.