The Investment Matching Principle: How the Risk/ Return Profile Connects to Diversification

The Number of Investments in a Portfolio is Dictated by the Probability of Returns

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

There is a podcast of this memo available if you prefer listening to it. You can find it on our podcast feed here (Apple, Spotify).

If you are new to Speedwell Memos, welcome! We have pieces on Zara & Shein, Google’s AI risk, Why Wish Failed, Alibaba’s Accounting, What was priced into Home Depot in 1999, as well as many others! Also, if you haven’t already, check out our business philosophy pieces on The Piton Network (Part 1 and Part 2), as well as our Series on The Consumer Hierarchy of Preferences. A directory of our memos can be found here.

Intro.

Inherent in every financial instrument is a certain probability of various returns or losses. It is commonly believed that it is the instrument itself (whether that be a stock, option, bond, etc.) that determines whether ownership of such instrument is wise, but that is not always the case.

Should you write just a single earthquake insurance policy that if you had to pay out would bankrupt you, then you have made a terrible error of judgement. However, if you write 1,000 such policies across a wide geographic area, then that could be financially savvy.

The key difference is two concepts: 1) Diversification and 2) Conjunctive Probabilities.

Warren Buffett famously eschews excessive diversification, but he also focuses on investments that have very little risk of impairment of capital. A successful investor can be one who diversifies a lot or a little, but it will always be someone who “matches” risk of impairment of capital with the number of independent investments they make. The reason for this is because on a long enough time horizon, what can happen, will happen. Should an investor have too few independently correlated investments they risk incurring losses too high to come back from.

We will clarify later that correlated investments are those with related risks, not price movements, but first, bonds.

Building a Portfolio of Bonds.

Let’s assume that if a bond defaults it will be worth zero (i.e. assuming no recovery). This allows us to create a fairly binary outcome: either you get your principle and coupon, or it defaults and you get nothing. Now the return profile isn’t really in the question here: the return a bond holder will get, assuming no default or early sale, is going to only be the stated coupon. There is no chance that it returns more, and outside of default, it won’t return less. If we say that a portfolio of bonds has a 5% chance of default, then the question is what return will you demand from this portfolio and how many individual bonds would you need in order to be adequately diversified.

At the extreme, if you owned just a single bond, then there is the possibility that you lose all of your money. If you have 100 bonds but only demand a coupon of 3%, then it is highly likely that you not only won’t make any money, but will lose a little.

There are three mistakes that an investor can make: 1) purchasing a bond portfolio without a high enough yield to compensate for the default rate, 2) estimating the default rate incorrectly, and 3) not having a high enough number of bonds that are independently correlated.

With a risk-free rate of 4%, the investor would look for a yield of at least 9% so the income offsets the expected defaults and they still make the risk free rate. The default rate of 5% though is an average and if the bonds share exposure to common risk, then a much larger number of bonds could default in a given year.

As the saying goes:

Never forget the 6-foot-tall man who drowned crossing the stream that was 4 feet deep on average.

Should this investor have a portfolio of 40 bonds that all are underwritten by various gulf coast energy companies with break-even oil costs over $60, this investor may have 40 individual securities, but any event that causes oil prices to fall or production to stop on the gulf coast could ruin them. While this is a fairly contrived example, the point is that portfolio diversification should be thought about in terms of commonly shared risks. The reason for this is because proper diversification reduces conjunctive probabilities.

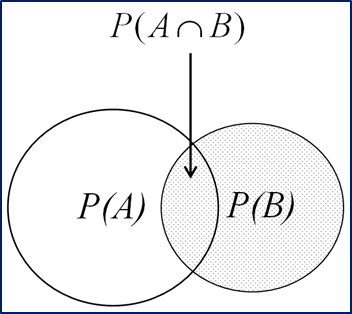

Conjunctive Probabilities.

A conjunctive probability is the probability of two or more events occurring simultaneously. Or in technical terms, it’s where the two circles overlap below.

If the probability of event A and event B are 5%, then the probability of both occurring is 0.25%. The general idea is that if you have a portfolio of multiple investments, the probability that something will go wrong with multiple investments simultaneously is much less than the probability that something will go wrong with any one investment. A condition of this being true though is independence, and few investments are truly independent.

True Uncorrelation is Rare.

Now most investors have heard of not overconcentrating in one sector, but the real thing they should focus on is the underlying risks each investment shares. You may own a bunch of China stocks and think you are diversified owning Apple, but you would be mistaken as the majority of their supply chain is based in China, as well as 20% of sales. Snapchat, Meta, Pinterest, and Twitter all had the same data privacy and mobile platform risks—ATT impacted all of them to a degree. Owning nothing but US pharmaceuticals companies puts you at risk of health care legislation impacting all of your holdings. Minimum wage laws may hit restaurants and retailers particularly hard. It is not about the sector each company is in per say, but the fact that the same event can adversely impact each company. This is essentially the lesson of the great financial crisis: do not assume something is uncorrelated just because something like the “geography” is different.

When investors bought mortgage-backed securities (MBS), they were taught to believe that grouping together a bunch of individual mortgages across different incomes stratums, geographies, home types, etc., would mean that the likelihood of the whole portfolio of mortgages defaulting all at once was lowered. This of course was erroneous because all of these mortgages were exposed to the same risk: the necessity of home prices increasing in order to avoid default. What these MBS investors conceptualize as a highly diversified bet across different income levels and geographies, was really a single bet on home prices never falling.

This is all to say that an investor must look at the common risk their portfolio of companies are exposed to. Some commonly shared risk are unavoidable, like taxes increasing for US companies. Or near unavoidable, like oil prices increasing which could adversely impact not just an airline or a cruise operator, but also a petrochemical manufacturer and food producer.

However, rising oil prices could be positive for other businesses like an E&P producer or EV manufacturer. Now the point is not to look for adverse events and see what you can own in order to offset that risk, but rather just to be aware of how exposed your portfolio is to a given risk. If an offset happens to exist, then that risk is somewhat mitigated.

Berkshire pays out a lot of insurance claims when storms rip through communities, but they also own Clayton Homes which presumably benefits in the aftermath. Google may end up paying Apple a lot more each year in TAC payments, but as an owner of both you become more neutral to the outcome of these negotiations. It would be poor practice to purchase any business just because it stood to benefit should a risk manifest in a separate business, but it could still be considered a risk mitigate in the overall portfolio.

Two Methods to Account for Risk.

To generalize, there are two methods for accounting for risk in a portfolio. Method one is to select investments that carry reduced risk profiles. CME, or Chicago Mercantile Exchange, which has been around since 1889, has much lower risk of their cash flows materially disappearing or their business becoming obsolete than Peloton or Crocs.

The second method to account for risks in a portfolio is with positioning and the number of independent investments you have. You would need fewer “CMEs” in your portfolio to adequately diversify than you would need “Crocs”, which just narrowly avoided bankruptcy in 2009.

On the other hand, the possibility that Crocs becomes a much bigger business in the future with a new hit product line is higher than CME whose business is essentially unchanged for the better part of a century.

It is an investor’s job to match the risks inherent in each investment to the number of independent investments they make so their portfolio’s “expected return” has a high probability of being realized.

For example, a portfolio has 2 investments that will either triple or go to zero with 50/50 probability of each event occurring for each investment. This portfolio has an expected return of 50%, but since there are not many investments in the portfolio (the N isn’t high enough) this investor stands a 25% chance of losing everything. If we increase the number of investments from 2 to 5, then there is only a ~3% chance that this investor loses everything and a ~97% chance at least one of their investments hits, in which case their portfolio would retain 60% of its value. If each investment had a 5x upside instead of 3x, then this portfolio would have a 97% chance of retaining at least 100% of its value. It is an investors job to match the number of investments and risk profiles so that it is very unlikely they lose money and very likely they make money. The particulars of how “likely” is acceptable to each investor is the key piece of judgement required in investing.

Warren Buffet stands at one end where he tries to focus on reducing the risk inherent in each investment he selects. His famous Two Rules of Investing are Rule #1: don’t lose money and Rule #2: don’t forget rule #1. Since he focuses so much on eliminating risk of impairment of capital in each investment, the result is two-fold: 1) Buffett needs fewer investments to be adequately diversified, and 2) each investment can appreciate less, and the portfolio will still do well because “expected losses” are minimal. Thus, returns will not be sapped away by losses.

At the other end of the spectrum is an investment strategy similar to VCs where the investor increases the number of investments they make because each individual investment carries significant risks. A VC’s “Two Rules of investment” would be closer to Rule #1: can the investment 100x?, Rule #2: don’t worry about the losers.

The increased number of investments is to compensate for the risk inherent in each, and the need for very high “100x” return is to offset the very high expected losses. A VC requires an extremely successful investment in order to offset all of their losses on their other investments. While a VC investor may be the extreme of this model, a stock market “growth” investor is similar, just lying a bit more conservatively on the risk spectrum.

Conclusion.

No matter what investing strategy an investor pursues, one thing always stays true. An investor must match the individual investment risk profile to the number of investments they make in order to reduce the possibility of totally striking out. This balancing act between the number of investments an investor makes and finding acceptable risk/return profiles is not just a key differentiator in many investment strategies, but is also the key piece of judgement an investor must develop.

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).