The Investor's Briefing #12

TSMC Dismissed Bubble Fears, Why 2%?, Warehouse Market Turns, New CoStar Threat

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the twelfth edition of our weekly newsletter: The Investor’s Briefing.

In Financial News.

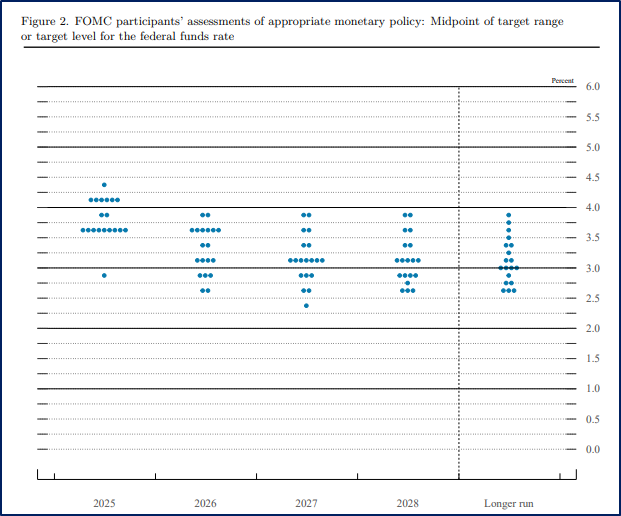

The Federal Reserve appears poised to reduce interest rates again this month as signs of labor-market weakness begin to outweigh persistent inflation pressures. However, policymakers remain divided on how far and how fast to go, leaving the path for borrowing costs into 2026 far less certain than markets suggest.

At the same time, a growing faction within the central bank is urging caution, arguing that inflation, while off its 2022 peak, remains above the Fed’s 2% target and continues to face upward risks. It is worth mentioning that the 2% target itself is somewhat abstract. According to Paul Volcker’s biography, the 2% mandate reaches back to a 1996 FOMC meeting when Janet Yellen pushed Alan Greenspan to quantify “price stability”. Prior to this Greenspan’s definition of price stability was: “The state in which expected changes in the general price level do not effectively alter business or household decisions”. Volcker points out that the idea that 2% inflation is an acceptable amount lacks empirical support. Still though the Fed has adopted it as their mandate of what constitutes price stability. Nevertheless, under Alan Greenspan’s definition of price stability, it does not seem like inflation is a common factor in household decisions.

All this is to say that even officials who are open to additional cuts this year have been reluctant to commit beyond this December, emphasizing the need for clearer data before adjusting policy further. Nevertheless, financial markets continue to price in a steady path of rate reductions through next year, betting on a softer economy and a continued easing cycle.

Against this backdrop, Chair Jerome Powell has made clear that the weakening jobs data cannot be ignored. Speaking on October 14, he warned that continued declines in job openings could soon translate into higher unemployment, a shift that would warrant preemptive action. “You’re at a place where further declines in job openings might very well show up in unemployment,” Powell said at an economics conference, reinforcing expectations of a quarter-point cut when the Fed meets on October 29.

Recent data support Powell’s caution. Payroll gains have slowed notably in recent months, and prior data revisions erased a significant share of earlier job growth, undermining the view of a still-resilient labor market. Economists now describe conditions as “low-hiring, low-firing”, a fragile equilibrium that could tip quickly if the economy weakens. As a result, market participants already anticipate another rate reduction in December, consistent with the median forecast from last month’s Summary of Economic Projections.

Fed officals are split and their comments have the typical "hedged” language. Eight of the 19 FOMC participants currently project no further rate cuts next year, citing ongoing inflation pressures and potential new tariffs following the latest U.S.–China trade tensions. The conversation is generally centered around how cautious they should be, with Donald Trump appointed Stephen Miran the outlier that is pushing for more aggresive half-point moves.

Looking ahead, personnel changes could complicate next year’s decisions. Powell’s term as chair expires in May, and Trump has pledged to install a successor more inclined toward looser policy. Furthermore, two regional presidents rotating into voting roles in 2026, Beth Hammack of Cleveland and Lorie Logan of Dallas, have both showed caution towards further rate cuts at this time.

In the meantime, economist surveys show inflation gradually easing and unemployment inching higher next year, but few expect a rapid return to the Fed’s 2% target. Overall, with growth holding firm and inflation sticky, the Fed’s October decision may be the easy part. The more difficult question of where to go next will come in 2026 when interest-rate policy moves from more restrictive to neutral.

Company News.

TSMC Raises Forecast as AI Boom Drives Record Earnings and Dismisses Bubble Fears

TSMC lifted its full-year outlook after reporting record 3Q results, supporting the narrative that AI spend still has room to run. The company’s management expressed conviction that demand for advanced chips is “real and fundamental,” countering speculation that the rapid expansion in AI investment is a speculative bubble that won’t translate to actual money being exchanged.

TSMC is the world’s largest contract chipmaker and they now expects revenue growth in the mid-30% range, up from prior guidance of roughly 30%. The stronger forecast came as net profit increased +39% y/y to $14.8bn, and revenue climbed +41% to $33.1bn.

“Our conviction in the megatrend is strengthening,” CEO C.C. Wei told analysts. “We believe demand for semiconductors will continue to be very fundamental as a key enabler of AI applications.”

Wei said demand for AI chips remains “very strong” and continues to exceed expectations. He added that even with limited sales opportunities to China, AI-related revenue is expected to grow more than 40% annually, with the computing intensity, measured in AI tokens processed, expanding at an exponential rate. “That’s why we are still very comfortable that demand for leading-edge semiconductors is real,” he said.

The upbeat tone contrasts with growing skepticism among some investors that AI investment may be inflating a speculative cycle. Critics have pointed to circular financing arrangements, such as those between OpenAI and Nvidia, as evidence of froth in the sector. But TSMC dismissed those concerns, citing broad-based, long-term demand across data centers, mobile devices, and automotive applications.

TSMC is central to the AI supply chain. It manufactures Nvidia’s advanced GPUs, Apple’s iPhone processors, Qualcomm’s mobile chipsets, and AMD’s high-performance CPUs, giving it exposure to nearly every major player in the ecosystem. The company expects AI-related chip revenue to double by year-end and grow at a mid-40% annual rate over the next five years. This up from low single digit annual growth from 2017 through 2019.

Wei said TSMC is accelerating its expansion plans in the United States to meet surging client demand. Construction at its Arizona facility is being fast-tracked, and the company is close to securing additional land to develop a “gigafab” cluster, its largest overseas manufacturing complex.

TSMC’s strong quarter aligns with improving conditions across the semiconductor industry. ASML reported better-than-expected 3Q equipment orders, while Samsung forecast its highest profit in three years, signaling that the sector is emerging from last year’s cyclical downturn.

However, trade and tariff risks continue to loom. Taiwan faces a 20% U.S. tariff on chip exports as negotiations continue, and proposals from U.S. officials to rebalance semiconductor production between Taiwan and the U.S. could complicate future investment decisions. Despite these challenges, TSMC has pledged $165bn in U.S. capital spending, reinforcing its strategic importance to both Washington and the broader technology ecosystem.

Despite policy headwinds and cost inflation, the company is postitioned to structurally benefit from demand for cutting-edge chips and there is little that seems likely to threaten that. The question an investor always needs to ask though is what is priced in? At their current valuation of 23x forward earnings, a multiple about in-line with the general market, it is clear that a lot of market participants doubt they will be able to grow at the rate they have much into the future. It seems the key assumption an investor needs to build comfortability with is to what extent the wave of AI spending can continue and whether or not there will be a large air pocket along the way.

Prologis Raises Outlook as Warehouse Leasing Rebounds and AI Demand Spurs New Growth

Prologis, a REIT that is the the world’s largest owner of industrial real estate with a focus on logistics properties, said warehouse leasing activity is picking up after three years of sluggish demand, signaling that the logistics sector may have reached a turning point. The San Francisco-based company also raised its full-year earnings forecast, citing stronger customer engagement and rising interest in logistics and data-center infrastructure.

During Covid, a lot of money was poured into logistics infrastructure as people extrapolated out the elevated ecommerce demand into the future. As demand fell to a more normalized rate, there was a lot of excess capacity that needed to be absorbed. Few were left unscathed—even Amazon had misjudged demand and had to close down some warehouses in the aftermath. Showing the lack of investor excitement in this space, Prologis shares are still down about 25% from their peak at the beginning of 2022.

Things look like they could be changing for them though. Their revenue rose +9% to $2.2bn in 3Q, up from $2bn a year earlier. Prologis now expects full-year earnings of $3.40 to $3.50 per share, up from its prior range of $3.00 to $3.15. Core funds-from-operations is higher at a forecasted ~$5.80. This is against a current stock price of $125.

“Demand has clearly turned a corner,” said Chris Caton, Prologis managing director of global strategy and analytics, during the company’s investor call. “We’re seeing greater breadth and depth in customer discussions and a willingness to make decisions.”

The broader industrial real estate market appears to be stabilizing. According to Cushman & Wakefield, the U.S. warehouse vacancy rate held steady at 7.1% in the third quarter, an 11-year high but the first period in three years where availability didn’t increase. The leveling off suggests that companies are beginning to renew leases and secure new space after pausing expansion plans post-pandemic.

Caton said Prologis is seeing “good activity across early proposals and more mature negotiations,” with momentum across both new and renewal contracts. The company manages 1.3bn square feet of industrial space in 20 countries, serving major tenants such as Amazon, FedEx, and Home Depot.

Beyond traditional warehouse leasing, Prologis is positioning itself to benefit from the AI-driven infrastructure boom. CEO Hamid Moghadam, who will retire on January 1, said the company is increasingly developing data centers alongside logistics facilities to meet demand from hyperscalers and enterprises deploying AI systems.

“We can build both massive data centers for specific tenants and smaller facilities for AI inference,” Moghadam said. “That’s the big opportunity for Prologis, nobody has 6,000 buildings located as close to population centers as we do.”

While leasing volumes remain below the highs seen during the pandemic’s e-commerce surge, Prologis’s latest results suggest the market is gradually rebalancing. The combination of stabilizing demand, disciplined supply growth, and new opportunities in AI-related infrastructure has given management confidence to lift guidance for the remainder of the year.

In short, after several quarters of muted activity, the industrial property market appears to be entering a new phase, one driven less by pandemic-era inventory hoarding and more by long-term digital infrastructure and logistics modernization.

Former Manager at CoStar Sees Potential in AI and Acquisitions to Strengthen Data Offerings (Alphasense Expert Call)

A former CoStar Group executive who spent several years building the company’s CoStar platform, which caters to real estate professionals, described how the firm maintains their database while grappling with accuracy issues, integration challenges, and client frustration over raw data access.

The executive, who helped integrate third-party datasets and develop custom modeling tools for large institutional clients, said CoStar’s strength lies in the scale of its property-level information. “CoStar has over 40,000 different types of customers,” the expert said. “That could be architecture firms or manufacturing companies to real estate companies.” Within the institutional business, the focus was on how the company aggregates data, identifies weaknesses, and supplements coverage.

For decades, CoStar has tracked occupancy, leasing activity, and transactions across commercial properties. Yet, the executive said one of the firm’s historic gaps was its inability to connect properties to the investment funds that own them. “Property-level data is great, but what they need to do is benchmark and compare the assets as they’re aggregated and sold and bought at the fund level,” the expert said. To address that, CoStar integrated data from Preqin, a U.K.-based aggregator of global capital flows, creating what the executive called “an amazing resource to see how funds are performing at the property level.”

By combining fund-level information with CoStar’s property data, institutional clients gained more timely insights. “It’s almost like insider trading,” one client joked, according to the executive, “because you can see tenant movements before quarterly filings come out.”

Even so, customers are often frustrated about the platform’s limits. “CoStar will never be 100% accurate,” the executive said. “If you’re spending the amount of money that you do for CoStar, which is a monopoly, a word you’re not allowed to use when you work there, people will inevitably be upset.”

The executive identified two major weaknesses in CoStar’s U.S. data coverage: self-storage and data centers. Both have become priority sectors for large institutional investors, who also represent CoStar’s most important clients. The company, the expert noted, has roughly 1,500 researchers based in Virginia and plans to double that to about 3,000 as it expands internationally. In our research report, we also detailed how errors with lease data and other data fields that did not rely on a regulatory filing was common. However, CoStar was still far better than the alternatives.

CoStar’s biggest constraint, though, may not be data quality, but data accessibility. “They’re very protective about their raw data,” the executive said. “The way the world is moving is raw data, and CoStar makes it very difficult for you to manipulate and use it in your own modeling. You have to go into their system to get that information.” The expert warned that if the company doesn’t modernize its data-sharing model within the next three to five years, it risks losing market share. Exactly to who though is unclear. This was another common complaint we heard in our due dilligence. CoStar does have a somewhat flexible platform and allows for data to be pulled into it, but it still stands that there is no real ability to manipulate raw data outside of the CoStar enviroment.

The company’s chief executive, Andy Florance, “is a very smart man,” the executive added, but has been reluctant to open raw data access through APIs. “If you just have the raw data, then do you need CoStar anymore?” the expert said.

When asked about competitors building data moats by acquiring appraisal firms and automating valuations through AI, the executive said such models capture only a fraction of CoStar’s scope. “CoStar does everything,” the expert said. “It’s not just the valuation of properties, it’s leases, tenant names, occupancy rates, demographics, sales data, everything.”

One of CoStar’s biggest advantages, the executive said, is its ownership of Apartments.com, a high-traffic consumer portal that indirectly feeds CoStar’s databases. “If I’m a large institution marketing my properties on Apartments.com, I’m incentivized to make sure my occupancy rates, vacancy rates, and asking rents are timely and accurate,” the expert said. “That data gets fed directly into CoStar, which means researchers don’t have to call and verify those properties.” This is one advanatge CoStar has over other platforms in terms of data quality and scope.

As for the company’s absence from the appraisal-acquisition trend, the executive said CoStar doesn’t need to own those firms because it receives valuation information directly from major partners. “A partnership with a Blackstone or a BlackRock, where they’re buying properties and using CoStar’s data, feeds cap-rate information back into the system,” the expert said. The same applies to brokerage firms such as CBRE, which have long provided transaction data in exchange for discounted platform access. “It’s a swap and trade,” the executive explained. “We’ll take $10 million off your cost per month if you give us X amount of data.”

Turning to technology, the executive said CoStar invests heavily in new tools and is already deploying AI to streamline research. “They are a tech company and they invest heavily,” the expert said. “They’re firing off economists and using AI to aggregate information and generate reports.” AI, the expert added, is also being used to identify data gaps through web-scraping and automated analysis.

Still, the company’s long-term success may depend on resolving its tension between data protection and flexibility. “If they don’t figure out that API question, they will lose market share,” the executive said. “They’re not a dumb company. They will eventually do that, but they still have a strong resistance today.”

This is from an AlphaSense Expert Call Interview.

You can get a free trial of AlphaSense here

We changed up the format of the company section to extend the story of each company. If you enjoyed this, please drop a comment or like so we know to keep doing it in the future! Feedback is always welcomed.

Spotlight.

This week, we released a short business recap on LVMH as well as a free sample of our new Casey’s Exploratory Report.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

LVMH 3Q25 Business Update

Trending Positive: “While they provide limited information in this quarterly release, investors can have confidence that LVMH is starting to trend positive again after a period of shrinking sales. Of course, new tariffs or a broader economic calamity could halt their progress, but for now it is positive.”

LVMH 3Q25 Business Recap

Dialogue. Meta’s Vibes and What Chat GPT’s Instant Checkout Means for the Future of the Internet

OpenAI Super App: “Ben Thompson talks about OpenAI kind of trying to become an OS. I think the better analogy is really them trying to become a super app, because what they want to do is they want to embed all of this functionality within their application. And over time, I believe they’re going to try to make it exclusive to it too as well. And so the way you would do that is as you are modularizing these pieces, you start creating a benefit for someone to only be on that platform.”

Listen to the full dialogue here 👇

The Story of Casey’s Thread 🧵

Click here to read the thread on Casey’s

The Synopsis Podcast.

In this Company episode, we talk about APi Global, a high-quality B2B service provider that specializes in fire safety and other important business service verticals. The company has been undergoing a transition by eschewing one-off construction projects and moving to more recurring and higher margin service revenue. We draw from our 61-page research report on APi Global to cover everything from their involvement with legendary investor Martin Franklin and the business transformation to the many types of services they offer and the large competition set they face. We hope you enjoy!

Memo of The Week.

Minimum Viable Products vs. Maximum Possible Products

“Science is a process of testing hypotheses. You create a hypothesis and test it. But there is no way to know if a hypothesis is worth testing before testing it. Similar to mining for Bitcoin, you cannot know the solution to the SHA-256 hash function without actually computing it—there is no way to know the answer to the algorithm before calculating it.

Innovation is very similar.

You can create hypotheses about what preferences consumers have and create a product that tries to fulfill those, but you won’t know until you actually create that product.

If you are unsure if a consumer preference exists, then the MVP is like running a low-cost scientific experiment to probe to see if it does. You are answering the question, “what does the customer want?”.

If you know that a consumer preference exists, but the consumer doesn’t, then an MPP can prove to the consumer this unrevealed preference. You are answering a question that the consumer didn’t even know to ask.”

Learn more about MVPs vs MPPs in this memo here 👇

Minimum Viable Products vs. Maximum Possible Products

Company Report Snippet: Copart (CPRT)

Buying Back Stock in a Crisis: “When the financial crisis hit, with the country’s largest automakers going bankrupt and the whole sector requiring relief, they paused their repurchases to build up their cash reserves out of caution. However, once they observed their business continuing to operate with little hiccups, they positioned themselves to take advantage of the low valuation the market was giving them (a ~mid-teens multiple of owner earnings at the time with consistent double-digit growth).”

*This is an excerpt from our company report on Copart.

If you are a Speedwell Research Member, read the full report here: Copart

If you are not already a Speedwell Research member, you can purchase it here: Copart Individual Report

Upcoming.

Research

Current research report in progress: Shift4, the payment provider. Shift4 caught our attention because it is in a generally sticky industry (payments + software), still has founder involvement, is growing topline over >20%, and is down -35% from peak. Stay tuned for more!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Wilf Corrigan (link)

Michael Mauboussin: One Job—Expectations and the Role of Intangible Investments (2020) (link)

Verdad: Total Concentration? (link)

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

Couldn't agree more. Your insight into the 2% target's arbitrary origin truely resonates. It brings back thoughts from your earlier briefings on policy foundations. Very smart.