The Investor's Briefing #13

Evolution 3Q25, Netflix's Shift in Focus, Intel Shows Signs of Life, Could Yelp Save Airbnb's Services?

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the thirteenth edition of our weekly newsletter: The Investor’s Briefing.

In Financial News.

The rally in equities gained momentum this week after news emerged of an upcoming summit between U.S. President Donald Trump and Chinese President Xi Jinping, a development that helped ease trade tensions between the two nations.

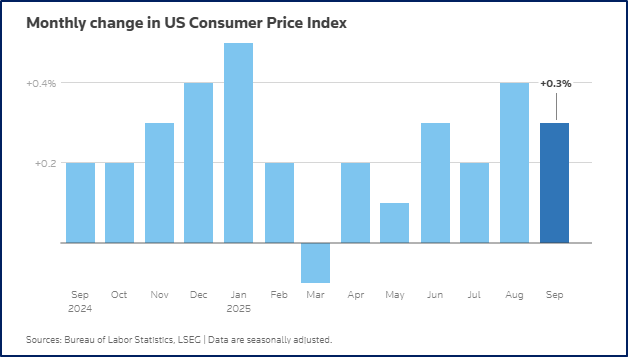

Meanwhile, inflation data offered further support to the market’s optimism. The core consumer price index, which excludes volatile food and energy components, rose +0.3% in September from the prior month—the slowest pace in three months. On an annualized basis, it advanced 3%.

The softer-than-expected reading was a welcome surprise for investors and policymakers alike. It provided reassurance to several Federal Reserve officials who have voiced caution about cutting interest rates too aggressively. While the central bank was already widely expected to lower borrowing costs at its meeting next week, the data may strengthen the case for another reduction in December if disinflation continues.

The S&P 500 reached a new record for week, touching slightly above 6,800 for the first time ever. The index closed +1.5% on Friday, putting YTD gains at +15.7%. After a similar move with the Nasdaq this week, that index is +20.4% YTD.

Elsewhere in commodities, crude oil prices spiked +5.5% on Thursday after the U.S. announced new sanctions on Russian energy giants Rosneft and Lukoil. Prices steadied around $62 a barrel on Friday as supply fears eased and OPEC signaled its willingness to increase output if needed.

Company News.

Netflix Posts Strong Quarter as Ad Sales and Price Increases Boost Growth

Netflix reported higher 3Q revenue and profit, driven by subscriber gains, record ad sales, and recent price increases.

Revenue rose +17% y/y to $11.5bn. Net income also increased nearly +8% y/y to $2.5bn, below expectations of $2.98bn, while the operating margin of 28% also came in slightly under target due to a one-time expense tied to a Brazilian tax dispute. Netflix said that excluding the charge, margins would have exceeded its forecast.

As a result, the company trimmed its full-year operating margin outlook to 29% from 30%, while reaffirming revenue guidance. Shares fell as much as -6% the next day following the announcement. However, the stock is still up 23% YTD.

Advertising remains a bright spot. Netflix recorded its best-ever quarter for ad sales and expects to more than double ad-related revenue this year as it expands its ad-supported tier globally.

Despite competitive pressure, Netflix continues to outpace traditional media rivals struggling with cord-cutting and costly streaming pivots. The desire for Warner Bros. to sell itself is but another sign of media consolidation and a limited number of winners in the streaming era. Netflix remains an undisputed streaming leader with over 300 million paying subscribers before the company discontinued the metric. For comparison, the next largest competitor is Disney+ with around 130 million subs.

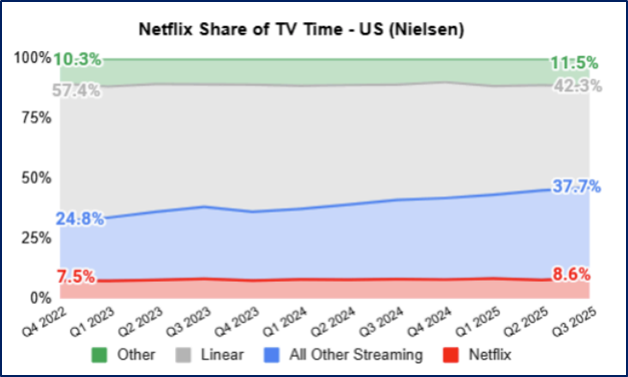

However, as streaming services emphasis advertising, a more pertinent metric going forward will be watch time on the platform—a metric that YouTube has long been number 1 in. At the end of 2024 Google announced that over 1 billion hours of YouTube were watched everyday. Netflix is estimated to be around a fifth of that at ~200 million daily watch hours. In their 3Q25 press release Netflix noted they increased their share of TV time to 8.6% from 7.5% in 4Q22. The more impressive move though came from Linear TV which fell from 57% to 42% in less than 3 years.

As they acknowledged in their earnings release though, their competition is much larger than other TV services. Anything that can take a viewers attention off of Netflix is a potential competitor. This fight for attention is more important for Netflix now as incremental growth is predicated on ad sales versus subscription sales.

Looking ahead, Netflix said it is well-positioned to benefit from advances in AI, which it is already using to improve content recommendations, localize marketing materials, and assist filmmakers in production. On the other hand, very advanced generative AI could create compelling content cheaply that competes with Netflix. Could AI advance enough that in the future a user could just ask for their own series to be generated for them with a custom plot and characters crafted to their preferences? As much choice as Netflix offers, it may be hard to compete against that. Netflix trades at 47x earnings with a $472bn market cap.

Intel Returns to Profit as Turnaround Gains Traction

Intel’s turnaround gained momentum in the third quarter as the chipmaker reported its first profit in nearly two years, driven by stronger PC processor sales, aggressive cost cuts, and renewed investor confidence following major government and industry partnerships.

The company posted net income of $4.1bn, reversing a year-earlier loss of $16.6bn and breaking a six-quarter losing streak—the longest in 35 years. Revenue growth in its core PC division and lower operating expenses, helped by layoffs and other cost reductions, underpinned the recovery. Shares rose more than +7% in after-hours trading.

CEO Lip-Bu Tan, who took over in March, said Intel is “steadily rebuilding the company,” emphasizing efficiency and sharper execution. “While we still have a long way to go, we are taking the right steps.”

Momentum in PC demand also surprised management. CFO David Zinsner said corporate customers are refreshing hardware faster than expected as Microsoft’s latest Windows rollout drives new orders. “Now we’re dealing with supply,” he said. “Demand is much stronger than we anticipated.”

The company’s shares have risen more than +85% this year—much of it since August, when Washington converted roughly $9bn in federal grants into a 10% equity stake in Intel. Confidence grew further in September after Nvidia announced a $5bn investment and plans to use Intel’s x86 CPUs in its data center servers. SoftBank also added a $2bn stake.

Still, challenges remain. Intel continues to trail Nvidia and AMD in the race to produce AI-optimized chips. Data center sales fell -1% y/y to $4.1bn, while revenue in the company’s foundry business slipped -2% to $4.2bn. The foundry arm, however, cut its quarterly loss to $2.3bn from $5.8bn a year ago, reflecting progress on cost discipline. Tan’s restructuring drive has sharply reduced headcount, down 13% sequentially and nearly 30% from a year earlier.

It also still is true though that TSMC is a generation ahead of Intel’s foundry and Intel has little differentation there beyond made in the United States. Intel’s traditional x86 CPUs are losing strategic prominence in the era of GPU and AI-accelerated computing. While they remain indispensable for general-purpose workloads and system orchestration, their growth and importance is much more muted.

Intel’s rebound remains incomplete, but the United States and other large partners have a vested interest in seeing it continue to survive. While it is unlikely to ever regain its prior importance in the semiconductor world, they can perhaps focus on their core strengths to build a stronger, yet smaller business. Intel has a $180bn market cap. In contrast, TSMC is valued at $1.25 trillion and Nvidia has a $4.5 trillion market cap.

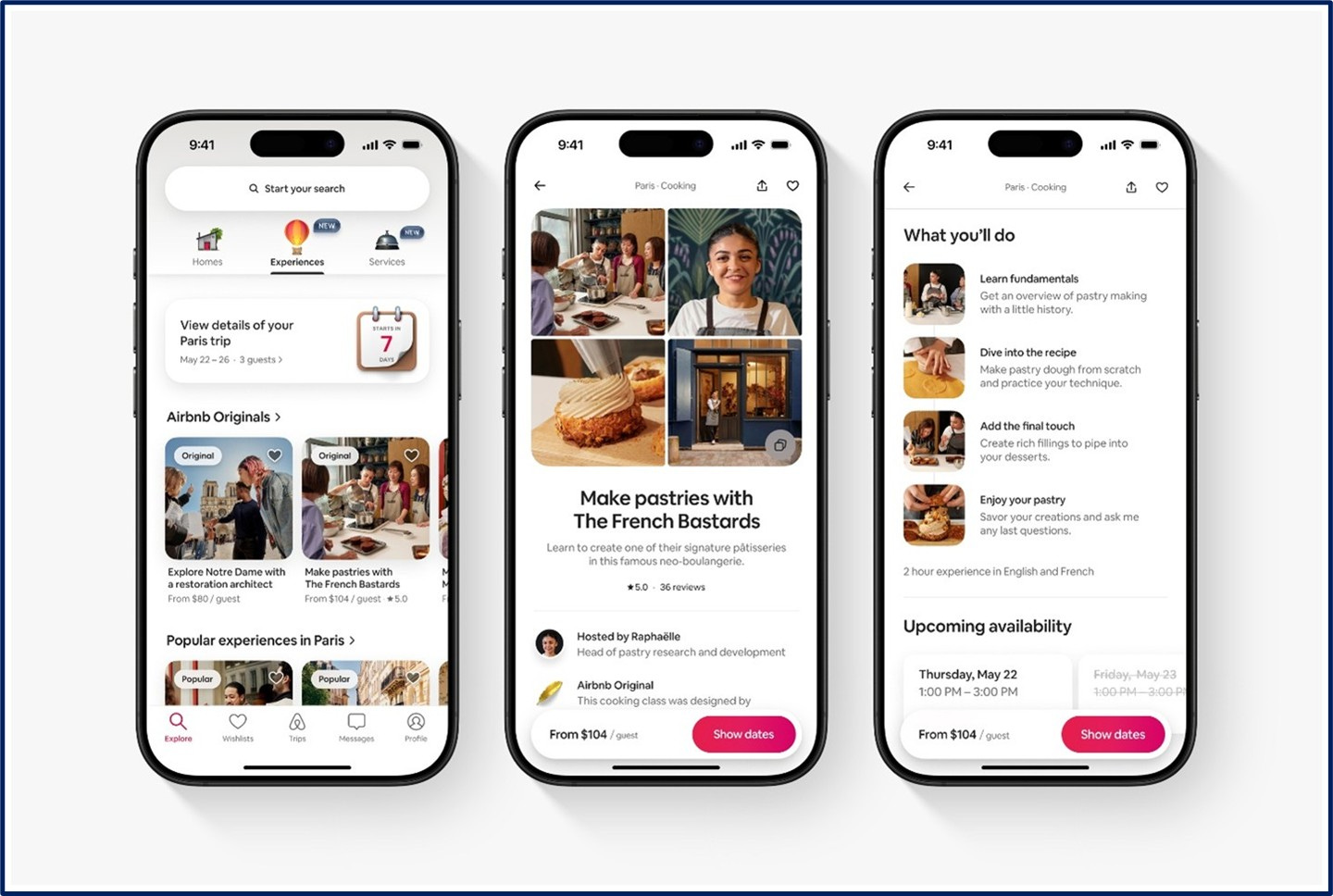

Inside Airbnb’s Push Beyond Stays (Alphasense Expert Call)

An executive who led strategic partnerships at Airbnb discusses Brian Chesky’s design-first focus, product positioning in Experiences, and monetization.

From a cultural vantage, Airbnb “thinks in a Silicon Valley kind of way,” is cloud-first, and hires top technical talent, the expert said. But the center of gravity is design and product polish. Chesky “focuses on how every single pixel looks,” often framing each biannual product release as the biggest yet, borrowing Apple’s presentation style. Internally, employees joke about the superlatives, the person said.

That emphasis shapes strategy. The expert described Chesky as a visionary who “bends reality” toward a preferred guest experience, while relying on others for technology and finance. Criticism is rare: “People do not speak up against him, and people who do, don’t last,” the person said.

The app now pivots around Stays, Services, and Experiences, after Categories, once touted as transformative, quietly receded. Public metrics behind their newer bets are sparse though The expert noted that Chesky highlights PR and star ratings more than attach rates or booking counts for Services and Experiences.

On the expansion beyond alternative accommodations, the former executive was blunt: Experiences have cycled through “three or four” iterations, with attach rates that remain “abysmally low.” The issue, they said, is not technology but demand. Airbnb hasn’t earned consumer permission to be the default for tours or local services, categories already served by incumbents and fragmented suppliers. Building sufficient awareness and price competitiveness would be “a long, long slog,” he said.

Frequency is another headwind. A typical guest might open Airbnb only a few times a year, giving them very few instances to try to cross-sell. “Why is this time going to be different?” the person asked of the super-app push.

Monetization remains the clearest lever. The executive called Airbnb “absolutely under-monetized,” pointing to long-discussed sponsored listings as “one of the most obvious” opportunities that could be done “in an elegant way.” Co-hosting could be another take-rate stream. Yet the company has avoided “me-too” moves that don’t clear Chesky’s differentiation bar, and it prioritizes smaller, individual hosts, both for brand reasons and to de-emphasize professionally managed properties because they tend to be cross-listed.

As for M&A to fill product gaps, activity has been limited. The last notable deal cited by the executive was a small AI acqui-hire in 2023 (GamePlanner), with “nothing to show for it thus far,” he said.

In our opinion, Yelp would be a very interesting acquistion for them. Yelp has the opposite problem Airbnb’s App has: Yelp has traffic, but no idea how to monetize it well. It is still very commonly used to search for local services—exactly the focus of Airbnb’s Services. Not only would they benefit from Yelp’s 180mn monthly users, which they could migrate into a combined app, but the repository of reviews and millions of businesses on Yelp would give their Services push instantly more credibility. Yelp would become the main reason that users open the app and then they could overtime push more service providers to accept a “fully integrated offering” which allows for instant booking, on-platform payment, and messaging. In return, they could boost these service providers in the search results, the same way Amazon boosts Prime products in their results. Airbnb could not doubt improve the Yelp experience too with their design asthetic.

In order to build adoption, Airbnb should probably abandon their 20% take-rate on services and wait until a consumer habit is built before attempting to monetize it. Their focus needs to be on becoming a strong demand generator for service providers first and doing everything they can to build up the supply-side of service providers.

Without a stronger base of users who have a reason to open the app regularly, it will be tough to have enough traffic to offer a cross-sell to service providers. While in our opinion Yelp could solve this, and cost less than one year of cash flows at $2bn, acquistions can be messy.

Airbnb’s Services serves a real need by helping a variety of providers find demand, which is why we like it, but it is just a hard thing to build without more user frequency. Meituan, which is similar to what Airbnb wants to build, was able to drive most of their frequency through food delivery. Ironically, Meituan actually also is a leading hotel booking provider, but the sequence matters. They used their traffic from users who ordered food delivery 1-2x a week to cross-sell hotel rooms—not the other way around.

Parts of this were from an AlphaSense Expert Call Interview.

You can get a free trial of AlphaSense here

We changed up the format of the company section to extend the story of each company. If you enjoyed this, please drop a comment or like so we know to keep doing it in the future! Feedback is always welcomed.

Spotlight.

This week, we released our 3Q25 business update on Evolution.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

EVO 3Q25 Business Update

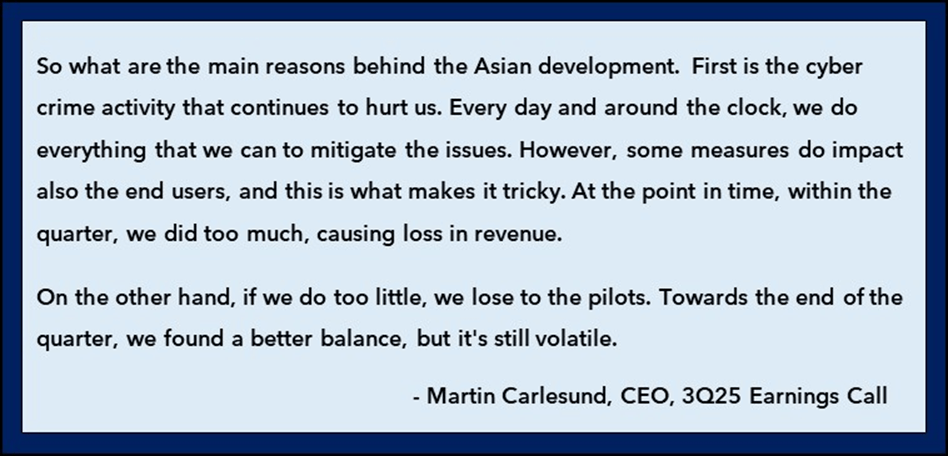

Collateral Damage: “They frame this as meaning that the revenue contraction was partially self-inflicted, but the other implication is that they cannot eliminate the stolen streams without causing collateral damage. There isn’t any reason to think that this won’t continue to be the case in the future. This balance is similar to a credit card company deciding how aggressive they should be with fraud prevention. If they are too aggressive, they risk losing legitimate transactions. If they aren’t aggressive enough, they risk allowing fraudulent transactions to go through.”

EVO 3Q25 Business Update

Company. APi Global: The B2B Service Giant Consolidator

Bleeding Construction Revenues: “Construction was very much a headwind to revenue because they kept bleeding off a lot of these contracts that weren’t making a lot of money. And so that has meant that revenue growth hasn’t looked that great, but profitability margins have been improving. And this was kind of a couple year transition. They did just get out of it now in 2025. It seems like that’s not going to be as much of an issue, but that was weighing on them, weighing on the optical performance because it’s arguably a good thing if you’re getting rid of, you know, these low calorie revenues.”

Listen to the full company episode here 👇

The Synopsis Podcast.

This week, we released a Dialogue episode discussing Evolution’s 3Q25 earnings. In the episode, we provide a high-level overview of the quarter, talk about new developments in Asia, and discuss how an investor should think if Asia goes to zero. We hope you enjoy!

Memo of The Week.

The Piton Network: Decisions that Simultaneously Support and Limit the Future Decision Space

“As Jeff Bezos notes, there are two-way door decisions and one-way door decisions. A two-way door decision can always be reversed. A one-way door decision is irreversible (at least without significant costs). Businesses who chase competitors from a sub-optimal Piton Network usually fail to fully copy the competitor’s offerings because there is a Piton in their network that needs to be moved, but it is a “Load-bearing Piton” and moving it is a “one-way door” decision. Not all Pitons can be restaked once pulled, and pulling them may permanently push a company in a different direction.

To reiterate, a Piton is a strategic decision that simultaneously supports and constrains an element of a business. The Piton Network is what the Pitons in the company are optimized for. Just like with mountain climbing, it is possible for a Pitons to be sub-optimally placed for your intended path.”

Learn more about the Piton Network in this memo here 👇

The Piton Network: Decisions that Simultaneously Support and Limit the Future Decision Space

Company Report Snippet: AppFolio (APPF)

The Sharing Surplus Growth Lever: “Their key to success was focusing on the customer. CEO Donohoo noted on their first earnings call in 3Q15, “word of mouth marketing from happy customers… is a powerful tool and a tremendous competitive differentiator that fuels our growth.”

(Share this quote on Twitter/X)

*This is an excerpt from our company report on AppFolio.

If you are a Speedwell Research Member, read the full report here: AppFolio

If you are not already a Speedwell Research member, you can purchase it here: AppFolio Individual Report

Upcoming.

Research

Current research report in progress: Shift4, the payment provider. Shift4 caught our attention because it is in a generally sticky industry (payments + software), still has founder involvement, is growing topline over >20%, and is down -37% from peak. Stay tuned for more!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Steve Mandel, Paul Buser, and Rick Buhrman (link)

Leandro (Best Anchor Stocks): Durability and Its Implications for Investors (link)

Aswath Damodaran: Accounting Returns, Market Returns, and Good/Bad Businesses (link)

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

Thank you Drew. The post on ABNB is spot on.