What You Don’t Know About Sell-side Analyst Price Targets

Five Pernicious Influences to Price Targets

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

There is a podcast of this memo that is available if you prefer listening to it. You can find it on our podcast feed here (Apple, Spotify).

If you are new to Speedwell Memos, welcome! We have pieces on Zara & Shein, Google’s AI risk, Why Wish Failed, Alibaba’s Accounting, What was priced into Home Depot in 1999, as well as many others! Also, if you haven’t already, check out our business philosophy pieces on The Piton Network (Part 1 and Part 2), as well as our Series on The Consumer Hierarchy of Preferences. A directory of our memos can be found here.

Intro.

Investing is easy.

All you have to do is buy the stocks that the sell-side analyst says to buy and sell the ones that they say to sell.

They even offer this service for free and tell you the exact price the stock will increase to!

Now, most people aren’t so naïve to trust a sell-sider’s price target on a stock and many are aware of their woeful track records of being correct, but you could be forgiven for not knowing the extreme extent to which those price targets deceive.

In fact, a price target not only has little to do with the valuation of a stock, but the factors that go into creating it are marred by many non-investment related prerogatives from career risk and marketing to financial incentives and corporate access. We identify five key factors below, the last of which is virtually never spoken of.

Career risk

Losing Corporate Access

Marketing / Building Reputation with an Out-of-Consensus Call

Influence from Compensation from Clients

Coverage Universe Constraints

But first, a story.

An Extreme: The Tech Bubble Era Analyst.

During the Dot Com bubble, equity research had fewer rules and most of the chicanery was still hidden. While we can cede that there were many regulatory grey areas and pernicious incentives that put Sell-side analysts in tough positions, they nevertheless did not act particularly admirably.

They were supposed to be independent thinkers that could analyze a business and take an opinion on the business model without any outside influence. In practice though, they effectively became marketing tools for the investment bankers.

The reason for this was simple, an investment bank could rake in tens of millions of fees from an IPO and from the many potential subsequent transactions like follow on offerings, debt issuances, or acquisitions. However, the bank’s equity research division made no money directly. Sure they also supported the bank’s trading operation, and if an analyst creates an interesting report they might be able to spur some trading, but that is a relative pittance compared to the investment banking fees in a good time.

Furthermore, large investment banking fees would reliably translate into bigger bonuses for anyone who worked on the deals—equity research analyst included. In contrast, a star equity research analyst that recommended a stock that resulted in a large stock trade would generate just a fraction of the fees. On top of that it would be fairly circuitous to show that star analyst’s impact on the decision-making of that asset manager, making it near impossible to attribute the trading revenue to the analyst’s recommendation.

Now imagine you are a sell-side analyst. You make millions more helping the investment banking team and all you have to do is help investors understand the positive attributes of the company and ignore the negative factors. If you think you wouldn’t sell yourself out, remember that if you don’t play along your bonus could get “zeroed” and you may be managed out into a different role, or the company all together, while your less scrupulous colleagues play along and collects those fatter fees.

It gets even worse though.

What if you did want to be honest and say that you believe some of the tech companies that were IPOing in 1999 were crap. Except no matter how crappy the company, everything seemed to only go up. Now you are stuck trying to make a case that a company is crappy, which will not only piss off your investment banking colleagues trying to IPO the company, but will earn you less money, hurt your career, and most definitely would look wrong in the short-term as the stock price skyrockets.

“If you have a dumb incentive, you get a dumb outcome.”

-Charlie Munger

This gets even trickier when you consider that there is considerable leeway in how optimistic or pessimistic an analyst could be on a stock. If you think of Amazon in 1998, you could muster up many reasons as to why they would not be a megalith in internet retailing. Jeff Bezos himself thought they had a 70% chance of failure. Nevertheless, an analyst who believed they would dominate books and music with the potential to add other categories may have richly valued the stock.

Below we see star internet analyst Henry Blodget raise his Amazon price target from $150 to $400 (when it was trading at $240, or on a split-adjusted basis less than $2 per share). He notes that Amazon “is in the early stages of building a global electronic-retailing franchise that could generate $10 billion in revenue”.

While he was wrong on the timing (it would take them 8 years to reach that level of sales and earnings wouldn’t show up until much later), our general impression reading retrospectively is that he wasn’t optimistic enough. Last year Amazon had over half a trillion in sales.

A sell-side analyst is trying to judge a business on its future prospects, which in the case of early-stage internet companies could be decades out, yet are stuck expressing that view in a 12-month price target. This isn’t just a hard task, it’s nonsensical.

The stock price Amazon traded at a year later has only the most tenuous connection to their earnings power. This is an easy argument to make: their stock price dropped over 90% from 1999 to 2001 and yet net sales continued to rapidly grow from $600mn to $3.1bn.

We hope we can build some sympathy for the sell-side analyst and the impossibility of the task they are faced with. Even the best traders are hardly right more often than they are wrong, and among the most successful traders, like Stanley Druckenmiller and George Soros, they self-confess to be much worse with equity predictions than other asset classes. How could we possibly expect the average sell-sider to just magically produce reliable stock price predictions?

Well, we can’t. And this is a misunderstanding of what price targets actually are.

What is a Price Target?

A price target is the price an analyst thinks a stock will trade at in 12 months. There are two key pieces to that statement: 1) trade at, and 2) 12 months. The first phrase means that it is what the analyst’s thinks the stock will be priced at; it is not a valuation. While they may use a valuation methodology like a P/E or EV/EBITDA multiple to assert that price, it fundamentally is not a valuation, but rather what valuation they think other investors would be willing to pay for it, which is a pricing.

This is very important to understand as the price target they put out, is not a fair value for the business that a rationale and sober investor would value it at, but a byproduct of the investor behavior they observe in the market.

As soon as everything AI started to become much more popular, a sell-side analyst could reasonably conclude the marketability of any AI stock has increased and thus it warrants a higher multiple. Of course, they won’t say it that way. Again though, this is a pricing factor and has no bearing on how “Graham’s intelligent investor” would value a business.

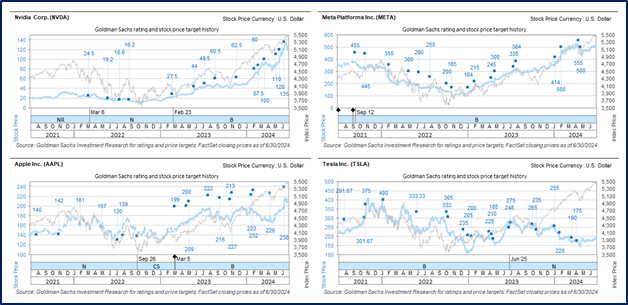

Look below at the history of price targets from four Goldman Sachs analysts. The price targets are the dark blue squares and the related stock’s price is the light blue line. You can see that the price target generally is matched to the stock’s price, with it usually being a bit higher.

If the analyst wants to have a “buy” recommendation on the stock, then they must show some upside. But if the stock moves above their price target, then they are stuck with either downgrading the stock or raising their price target. Stock downgrades usually require a longer research report and means they have to deal with the ire of management. As a sell-side analyst, one of your value adds to investors is access to corporate management. Do you think that relationship will be as strong if you decide to downgrade their stock?

Additionally, just because a stock is expensive, there is no reason it doesn’t stay expensive or gets more expensive. Do you really want to stick your neck out and say that a very popular stock is overvalued just for it to continue to be overvalued for years?

While sometimes an analyst will want to take a bold stance on a specific stock and that can help them earn mindshare with investors, like Adam Jonas who was bullish on Tesla for over a decade, it also is a risky proposition.

The New York Times opinion article above is from 2015 and chastises Adam Jonas for his bullish views. While this may be entertaining to read in retrospect given their success since, at the time, Adam Jonas was risking being seen as a fool for his non-consensus views.

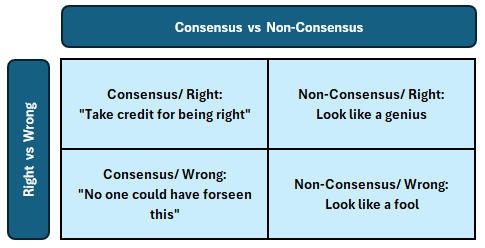

Consensus is technically what all sell-side analysts forecast in aggregate. Those earnings estimates that are commonly quoted are an average of analysts’ published estimates. Analysts can see the consensus figures just as investors can and they are very aware when they will be making an “out of consensus” call. They will only want to do so when they feel very strongly about something. However, even then they may choose to be in consensus instead of risking being wrong.

For very popular stocks that have a lot of “momentum” it could be futile to take an opinion because you could be right about the business prospects being poor, but the stock can rip nevertheless. Additionally, the market has an upward bias overtime so the probability of being right when bearish is lower. For most stocks, analysts will want to stay firmly in consensus because there is little career risk. They will then pick a few circumstances where they take a swing at an out of consensus call.

If they want to take a strong opinion on the stock, then the price target they pick will act as a sort of marketing tool whereby news articles and talking heads will quote that high price, driving more awareness to the analyst and stock. If they turn out to be right and out of consensus they will be lauded, whereas if they are out of consensus and wrong their ridicule will be persistent. (It is not just from the media, but also from clients who will love to remind them how wrong their call was and why they should listen to them ever again).

As a side note, we will get a bit technical in the note below to better explain why price targets are nonsensical. (You may skip this section and still understand the rest of the memo).

A stock’s valuation is the sum of all cash flows discounted at a certain rate. A 12-month price target has an implied 12-month return. If a stock is trading at $90 and the price target on it is $120, that implies the stock will return 33%. However, for the stock to be worth $120 in a year it still must be worth the sum of all future discounted cash flows. Thus, there will be a future discount rate associated with the stock at that point as well, which will be different from the 33% implied return. (Remember your return is equivalent to the rate at which the net present value of future cash flows = the current stock price. That’s essentially what a reverse DCF is).

The analyst is effectively saying the risk premium is too high on the stock for the risk they perceive. This is a fair statement to make, but it should be expressed as a current price target, not a future price target. If they expressed it as a future price target they are saying the risk premium is too high and will be bid down in a year. The first statement is a valuation , but by adding a timeline it becomes a pricing.

For example, they are saying that a stock should be valued at a 10% discount rate, but it currently trades at a 15% discount rate, but they think that it will trade down to a 10% discount rate by the end of the year. That excess risk premium being bid down in 12 months is essentially the investor’s “alpha”.

If this is what sell-side analysts actually did, then we believe it may be defensible, but in reality, it is the other factors that are driving their price target decisions. And as we showed in the price target graphs of Goldman Sachs analysts, they always want to show upside so they can maintain their ratings, so they are perpetually saying the risk premium needs to be bid down.

With an understanding of what price targets are (and aren’t) we will now move to factors that drive the price target.

What Factors Impact the Price Target?

To re-summarize the five main factors that have a pernicious impact to price targets:

Career risk

Losing Corporate Access

Marketing / Building Reputation with an Out-of-Consensus Call

Influence from Compensation from Clients

Coverage Universe Constraints

The first three we mentioned and the fourth was touched on in terms of investment banking, but it is also true for their hedge fund clients, as we note below. The fifth factor, which is that price targets are “relative”, is the one that is most unknown by most investors.

To understand this, we have to first note that each analyst has their own coverage universe. A new analyst may have only a handful of stocks, whereas most senior analyst will cover around 20-30 stocks. The stocks they cover are their “universe”.

The analyst has to place ratings on each stock, which are usually either buy (or overweight), neutral, sell (or underweight). These ratings are all relative to the companies within their coverage universe. In other words, if you cover only airlines, whether you think Delta or Southwest is a “buy” is relative to all the other airlines you cover. You are essentially just picking the best airline of the group—even if you agree that airlines are generally poor businesses that the average investor doesn’t need to own.

If this seems odd, it is largely because of how hedge funds operate. Many hedge funds will put on what are called “pair trades”. This is a trade where they pick one stock to go long and another stock to go short, both within the same industry sector. For example, the idea is that by buying the best airline and shorting the worst one you are eliminating a lot of the industry and market specific risk. Thus, if fuel prices spike, which increases flying costs, and both stocks fall, the best airline is thought to fall less or at least no more than the worse airline. This provides the hedge fund a “hedge”. They make money not when something that impacts all airlines happens, but when the individual business outperforms the worse business. (Of course, it’s not so simple because of expectations and whether or not something is priced in…).

This and similar strategies generated the need for stocks to be long and short. Furthermore, many hedge funds have specialists that only cover one or a few sectors. This set up is thus mirrored on the sell-side where analyst effectively pick stocks to go long (buy recommendations) and short (sell or neutral recommendations). Because a sell-side analyst doesn’t want to burn their corporate access relationship, they tend to prefer neutral recommendations to sell recommendations.

Now once an analyst knows the stocks they like most and least, they have to have the price targets reflect that opinion. So if an analyst was positive on AAPL, but AAPL moved up 30%, they are forced to either increase their price target so they can continue to show it has upside (and thus is still a “buy”) or they must downgrade the stock. This is a tough position to be in as the stock’s valuation and the business’s fundamentals may commonly move out of step for some period of time. The rest of the analyst’s coverage may also just be a bunch of low quality consumer electronics companies. So this analyst is stuck with the choice of either continually increasing their price target as the stock moves up or writing a downgrade note for what is probably the highest quality company they cover, which will also draw the ire of the investors who are long the stock. Then there is the awkward fact that these same funds rank the analysts (the so called “broker votes”), which greatly impact their pay… and employment. On top of that, as mentioned prior, a downgrade is sure to sour relationships with the company’s executive team, meaning they get cut out of the information loop.

In short, the analyst usually ends up just continually increasing their price target so they can continue to show upside.

So the price targets you see are a mix of the analyst trying to manage their career, keep corporate access, market themselves, and keep their clients happy to influence their compensation, all while keeping their target prices in line with their relative recommendations.

So maybe there is no free money and it’s not as easy as just buying the stocks they tell you too.

Conclusion.

While we may criticize sell-side analysts, there is no doubt that faced with the realities of their position, they have too many non-investment prerogatives that cloud their ability to offer an untainted recommendation.

Lucky for the investor though you have an easy solution: ignore them.

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

If you aren’t ready to become a Speedwell Member yet, sign-up for our free content below!

I'm late to this article, but loved it. Thank you.

Great explanation of the mechanisms and incentives that drive the sell side