The Investor's Briefing #14

AWS Reaccelerates Growth, Chipotle Signals Consumer Struggles, Perimeter’s Runway

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the fourteenth edition of our weekly newsletter: The Investor’s Briefing.

Announcement: 3Q25 Earnings

Speedwell Members have already received 7 earnings updates on and will receive another 6 next week. Become a Speedwell Member today to stay up today on all of the great businesses we cover! See our full coverage here.

Published: APi Global, CoStar Group, Evolution, Floor & Decor, LVMH, Meta, Perimeter Solutions

Upcoming: Airbnb, Appfolio, Axon, Copart, Constellation Software, Coupang, Dream Finders Homes, RH

Get all of the updates plus our in-depth research reports today and lock in our current pricing forever. If you are at a fund, reach out to info@speedwellresearch.com for help getting your subscription expensed.

In Financial News.

The S&P 500 and Dow Jones ended the week slightly positive after reaching new all-time highs after a stretch of volatile trading, with the Nasdaq gaining +0.7% supported by upbeat earnings from mega cap tech companies. The results marked the second consecutive weekly gain for the broader market, with tech once again anchoring performance.

Turning to monetary policy, the Federal Reserve lowered interest rates for the second consecutive meeting, extending efforts to shield the economy from a slowdown in hiring. Yet Chair Jerome Powell moved swiftly to tamp down expectations that another cut in December is inevitable.

“Risks to inflation are tilted to the upside, and risks to employment are tilted to the downside.” - Fed Chair Jerome Powell

Speaking at a press conference on Wednesday, Powell pushed back on market assumptions that the central bank was locked into a third straight cut. “Far from it,” he said, underscoring divisions within the FOMC over whether additional easing is warranted.

The quarter-point reduction lowers the federal funds rate to a range of 3.75% to 4%, the lowest in three years and down from a peak of about 5.4% maintained through much of 2024. Officials said the decision aims to prevent a mild slowdown in employment from evolving into something more severe.

Powell acknowledged that the easier phase of rate normalization may now be over. He described a “growing chorus” of policymakers questioning whether further cuts are justified, particularly given uneven inflation progress and resilient consumer spending. The 10-2 vote reflected those divisions, with Kansas City Fed President Jeffrey Schmid dissenting in favor of holding rates steady and Governor Stephen Miran preferring a larger half-point reduction.

The decision came amid a data blackout caused by the ongoing government shutdown, which has halted the release of key economic indicators. Powell noted that the absence of data “could be an argument in favor of caution,” since officials lack updated readings on jobs and inflation.

In a separate move, the Fed said it would halt the runoff of its $6.6 trillion asset portfolio on December 1, ending a 3.5 year effort to unwind pandemic-era stimulus with quantitative tightening.

Before Wednesday’s decision, markets had largely priced in the rate cut and turned their focus to the Fed’s final meeting of the year. Policymakers remain split: a narrow majority still expects another quarter-point reduction, while a sizable minority believes the current level is sufficient to contain inflation that remains near 3%. For now, the December meeting remains an open question.

Company News.

Amazon Delivers a Strong Quarter as AI and Cloud Momentum Accelerate

Amazon reported strong 3Q results, after investors feared it was falling behind in the AI race. The company posted double-digit revenue growth, robust profits, and a sharp revenue reacceleration in its cloud business, while outlining ambitious plans to expand its data-center capacity.

Revenue rose +13% y/y to $180bn, sending shares 10%+ higher. AWS grew +20% y/y —its fastest pace since 2022 and 300bps acceleration from last quarter’s growth rate. Though that figure trails the 40% and 34% growth reported by Google’s Cloud and Microsoft’s Azure, respectively. AWS’s gains come off a much larger base with a total revenue of $33bn for the quarter vs Microsoft at $27bn and Google at $15bn. CEO Andy Jassy emphasized that Amazon continues to lead the industry in absolute revenue and remains well-positioned to capture rising enterprise demand for AI-related workloads.

Looking ahead, Amazon expects a steady 4Q with sales estimated to be between $206bn and $213bn, underscoring management’s optimism as it enters the holiday season. The company continues to expand its logistics and fulfillment network, introducing more same-day grocery delivery services and opening warehouses in rural regions to capture incremental consumer spending. Jassy said the focus remains on balancing operational efficiency with innovation, noting that Amazon plans to double its data-center capacity again by 2027.

At the same time, Amazon has been investing heavily to support this expansion. Capex spend reached nearly $90bn in the first nine months of the year, with full-year spending projected at roughly $125bn—much of it directed toward cloud and AI infrastructure. Recently, the company brought Project Rainier, one of its largest AI data centers, fully online. According to Jassy, “as fast as we’re bringing in capacity right now, we’re monetizing it,” reflecting how strong demand has become for AI computing. He added that the primary constraint in the industry is now power availability, which could eventually shift to chip supply.

Nevertheless, the quarter was not without headwinds. Earnings were weighed down by one-time charges tied to legal settlements and restructuring efforts. In September, Amazon agreed to pay $2.5 bn to settle a Federal Trade Commission lawsuit related to its Prime subscription program. This was followed by an announcement to eliminate 14,000 corporate roles, a move expected to save about $1.8bn. Jassy said the job cuts were designed to correct overexpansion during the pandemic and preserve a “lean, fast-moving” culture.

Meanwhile, Amazon continues to address concerns that it is losing momentum in the race for AI leadership. Management acknowledged these perceptions but said demand for cloud and AI services continues to exceed capacity. To stay competitive, Amazon is accelerating automation across its distribution network. The company is deploying new robotics and predictive AI tools designed to make warehouses smaller, more efficient, and closer to customers—improvements that should lower logistics costs and shorten delivery times.

Despite broader macroeconomic uncertainty, Amazon continues to benefit from resilient U.S. consumer spending. The company said it has seen little inflationary pressure on its marketplace, suggesting sellers have absorbed much of the cost impact from tariffs and supply chain disruptions.

Jassy summed up the company’s position by saying, “I don’t know if there’s ever been a time in the history of Amazon, and maybe business in general, where it’s as important to be lean, to be flat, and to move fast.” Yet even as Amazon tightens operations, it plans to keep investing “very significantly” in automation and AI infrastructure, betting that efficiency and innovation will reinforce each other as the next phase of growth unfolds.

Chipotle Lowers Outlook as Consumer Weakness Weighs on Fast-Casual Dining

Chipotle delivered 3Q results that matched expectations, yet investor sentiment soured after the company struck a more cautious tone about future sales trends.

The burrito chain reported $3bn in revenue, with same-store sales up +0.3% from the prior year. All metrics were consistent with consensus estimates, however, management lowered its guidance for full-year comp sales, signaling that demand could soften further through the end of the year. The company now expects same-store sales to decline by a low single-digit percentage, compared with its previous forecast for roughly flat growth.

Following the announcement, shares fell -19% and are now down about -34% for the year. Consumer spending patterns have shifted as persistent inflation, higher interest rates, and slowing wage gains weigh on discretionary budgets. Many households are cooking at home more often, opting for cheaper quick-service chains, or scaling back restaurant visits altogether.

Chipotle has not been immune to that shift. While it remains one of the strongest brands in the category, its higher average ticket prices make it more exposed to income-sensitive diners than fast food chains like Taco Bell or McDonald’s. Recent promotions from rivals emphasizing value meals and bundled offerings have further intensified competition for budget-conscious customers.

Chipotle’s management appears focused on adapting to the more value-conscious environment. CEO Scott Boatwright said the company is prioritizing improvements in restaurant operations, marketing effectiveness, and menu innovation, while enhancing digital engagement to strengthen loyalty. Executives also said they would pause additional price increases despite mounting costs for beef and labor, aiming to avoid alienating budget-sensitive customers.

Ultimately, the strategy underscores the delicate balance facing restaurant operators in the current environment: sustaining profitability without alienating customers who are increasingly price-sensitive.

If you enjoyed reading this, consider sharing it so we know it is worth continuing to produce!

Spotlight.

This week, we released several 3Q25 business updates on CoStar, Meta, Floor & Decor, APi Group, and Perimeter Solutions.

This is in addition to the other 3Q25 business updates we have written on so far this earnings season: LVMH, Evolution

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

META 3Q25 Business Update

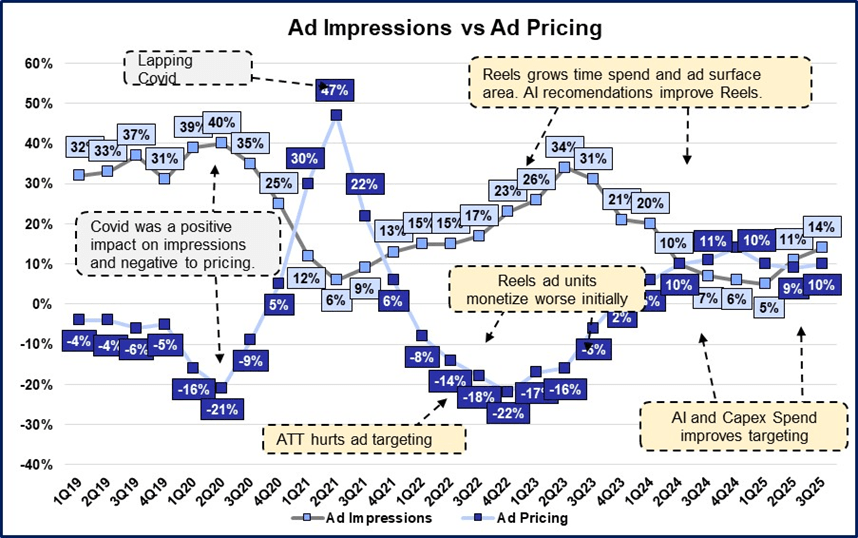

Improving Time Spent Drives Higher Ad Impressions & Ad Prices: “On the call Mark Zuckerberg noted that AI has driven 5% more time spent on Facebook and 10% on Threads. Video time spent on Instagram is up more than 30% from last year. Overall time spent on Facebook and Instagram is up double digits y/y. All of these improvements are largely attributable to AI advancements.

Revenue growth accelerated to +26%, +400bps from last Q. This was driven by Ad impressions growth of +14% (vs +11% last Q) and Ad prices increased +10% (vs +9% last Q).”

Read the full META 3Q25 Business Update here

FND 3Q25 Business Update

Tom Taylor on Playing The Long Game:

Read the full FND 3Q25 Business Update here

PRM 3Q25 Business Update

IMS Importance: “To the positive, the IMS business more than offset this, contributing $10.8mn for the quarter. Within the specialty product segment, this is a more important business for two reasons. 1) It is their first foray into a new vertical since acquiring Perimeter Solutions and so their success or failure here will say much about their ability to allocate capital beyond the fire safety business. 2) It is a larger growth opportunity to deploy more capital. The P2S5 business was a legacy business acquired in the original acquisition and is a more “average” quality business.”

Read the full PRM 3Q25 Business Update here

The Synopsis Podcast.

In case you missed it, we released a Dialogue episode discussing Evolution’s 3Q25 earnings. In the episode, we provide a high-level overview of the quarter, talk about new developments in Asia, and discuss how an investor should think if Asia goes to zero. We hope you enjoy!

Memo of The Week.

The Consumer’s Hierarchy of Preferences: Assessing Retail Strategies with The Inventory Value Capture Index

“This metric accounts for the two variables that we want to focus on—turnover and margin—to answer our question of which retail strategy creates more value (Strategy 1: convince people to pay more vs Strategy 2: charge less and sell more).

In summary, meshing these two financial figures gets us operating profit generated per dollar of average inventory held. The output essentially is how well each dollar of inventory is monetized. We dub this “Inventory Value Capture”, and think it is a clean way to compare retailers who utilize very different strategies.”

Learn more about the Inventory Value Capture Index in this memo here 👇

The Consumer’s Hierarchy of Preferences: Assessing Retail Strategies with The Inventory Value Capture Index

Company Report Snippet: Airbnb (ABNB)

Declaring War on Clones: “Chesky decided that the most fitting “revenge” for Wimdu would be to force them to run the company they were hoping to quickly flip. Instead, Brian “declared war” and personally became the Head of International. They bought a smaller company, Accoleo (without the “mercenary” culture) to build a foothold in Europe, and within three months, had opened ten more offices internationally with country managers he hand-picked. At the same time, the pressure helped them build an international “playbook” that they instituted on a country-by-country basis.”

*This is an excerpt from our company report on Airbnb.

If you are a Speedwell Research Member, read the full report here: Airbnb

If you are not already a Speedwell Research member, you can purchase it here: Airbnb Individual Report

Upcoming.

Research

Current research report in progress: Shift4, the payment provider. Shift4 caught our attention because it is in a generally sticky industry (payments + software), still has founder involvement, is growing topline over >20%, and is down -46% from peak. Stay tuned for more!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Laver Cup Chairman Tony Godsick on the ‘Ryder Cup of Tennis,’ Roger Federer, Nike, Uniqlo (link)

Howard Marks’s new memo: A Look Under the Hood (link)

Michael Mauboussin on The Economics of Customer Businesses (link)

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).

Wow, the part about the Nasdaq's gains anckored by mega cap tech companies really stood out to me; it makes one reflect on the concentrated power and innovation that continues to drive so much of our global economy, even while acknowledging the broader market's journey.