The Investor's Briefing #15

Constellation Software's Largest Ever Drawdown, Amazon's AI Agent Risk, Copart & Floor and Decor Sell Off

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the fifteenth edition of our weekly newsletter: The Investor’s Briefing.

Announcement: 3Q25 Earnings

Speedwell Members have already received 10 earnings updates and will receive another 2 next week. Become a Speedwell Member today to stay up today on all of the great businesses we cover! See our full coverage here.

Published: Appfolio, Axon, APi Global, CoStar Group, Coupang, Evolution, Floor & Decor, LVMH, Meta, Perimeter Solutions

Upcoming: Airbnb, Copart, Constellation Software, Dream Finders Homes, and RH

Get all of the updates plus our in-depth research reports today and lock in our current pricing forever. If you are at a fund, reach out to info@speedwellresearch.com for help getting your subscription expensed.

In Financial News.

U.S. markets declined this week as investors reassessed elevated valuations across technology and AI-related stocks. The Nasdaq led the losses, falling -4% for the week, while the S&P 500 lost -2.2%, reflecting broad weakness in high-growth sectors. Renewed warnings of a potential “AI bubble” and generally high valuations resulted in investors dismissing several strong earnings reports.

Adding to caution, private-sector layoff announcements increased to their highest level in any October in more than 22 years to over 150,000, reinforcing concerns that the labor market is beginning to soften. The data arrives amid the ongoing government shutdown, which has already delayed key economic reports and complicated the Federal Reserve’s assessment of employment conditions.

Separately, the Supreme Court signaled skepticism over the Trump administration’s use of emergency powers to impose wide-ranging tariffs on imports from more than 100 countries. Several justices questioned whether the executive branch had exceeded its constitutional authority, suggesting that the measures may infringe on Congress’s power to regulate trade. A ruling against the administration could require unwinding portions of the tariff program—potentially reshaping U.S. trade policy and altering cost structures for businesses just months after businesses adjusted to the new trade reality.

Company News.

Constellation Software is it Doomed?

Constellation Software is down -34% from peak, representing the largest stock drawdown in the stock’s almost 20 year trading history. While attributing any stock movement to a single variable is fraught with imprecision, there is no doubt that investors are worried that AI will mean more competition and thus customer losses for Constellation Software.

AI is no doubt impressive and we can never no for certain how the future will unfold, but this investor fear seems misplaced because Constellation’s moats never did stem from a lack of competition. This is exactly backwards causation.

As we all know, the TAMs for vertical market software can be very small, usually around ~$5mn. The reason why competition for a niche vertical doesn’t exist, isn’t because of costs or barriers to entry. It is because the market cannot support more than one player and once a customer is adequately served, there is no incentive to switch. Even before AI though a single software engineer could whip up a competing product. There is nothing particularly complex about most of this VMS software and it is often clunky with very rudimentary UI.

The reason why this software engineer wouldn’t find success is because creating a similar product doesn’t solve any customer problems. The customer is already happy with the existing software. Sure you could charge less, but their existing software cost is already such a small portion of their expense base it doesn’t really make a big difference for them. Plus there is the headache of pulling out your existing solution, reintegrating with all of your other software, retraining your employees, and risking an issue with the new software not working which will lose you revenue or customers. In fact a cheaper solution may be more expensive after accounting for all of this. Why would the customer care to do all of this for the same product that cost a little less?

There is more though. That professional service revenue Constellation Software collects is for setting up a customer’s software and often customizing it for them. The customer already did create the software they wanted—it is the software they have. If AI allows software to be made easier, than they still are going to have to go out and hire someone to use AI on their behalf to create that software because they don’t know how to. And it still doesn’t get rid of the issue that using AI to create new software doesn’t solve anything for them. Lastly, if AI does allow new software capabilities, Constellation can just use AI to build those functions cheaply.

Ultimately, the idea that now there is more potential competition misses the fact that great companies don’t win because competition is lacking. They win because they have solved a customer’s problem better than anything else. And as Peter Thiel notes, if you are an upstart you can’t just have a 10% better solution, you need a 10x one in order to get people to care. “The same software you have, but I saved money building it” is hardly solving any problems.

If you take Constellation’s FCFA2S metric and back out the IRGA liability, they trade at about 26x trailing free cash flow.

Perplexity AI Accuses Amazon of “Bullying” Over Comet Browser

Perplexity AI publicly accused Amazon of “bullying” on Tuesday after receiving a cease-and-desist letter demanding that it stop allowing users of its artificial intelligence browser, Comet, to make purchases on Amazon through automated agents.

In a blog post, Perplexity said users enjoy asking its Comet Assistant to find and buy items on Amazon, calling it a popular feature. However, the company said Amazon sent what it described as an “aggressive legal threat,” alleging that Perplexity had violated the e-commerce giant’s terms by using unauthorized AI agents to access its platform.

According to the letter, Amazon’s attorneys accused Perplexity of committing computer fraud by concealing when its AI agents act on users’ behalf. The letter stated that Perplexity “does not have authorization to access Amazon’s store, Amazon user accounts, or account details, using its disguised or obscured Comet AI agents.”

The dispute highlights the threat agents are to businesses that fear losing their direct customer connection. Agents have the ability to effectively modularize many businesses and also eliminate the opportunity for marketplaces to sell sponsored ads. In Amazon’s case, they want the most frictionless experience the customer can have. However, if it becomes easier for a user to just ask AI to buy XYZ for them and the AI agent can just as easily scan every internet store in existence, as well as, Amazon to purchase it, then their competitive postioning is ever so slightly weakening.

Now Amazon still has strong advantages in logistics, selection, and price, but the it opens the door for more competition in purchases where customers don’t care about fast delivery and maybe found another item cheaper elsewhere. And just like how Amazon offered to help Target operate their online commerce business initially because it increased their selection to only eventually steal those sales later on, the risk is an AI agent intermediates them the same way. While it is a long shot an AI platform will be as successful as Amazon was with it, why should Amazon help them at all?

Amazon defended its actions, saying that third-party shopping agents must operate transparently and respect platform boundaries. It claimed Perplexity’s AI agents were evading safeguards and degrading the shopping experience by surfacing products that lacked personalization, variety, or accurate delivery estimates. The real issue of course is that it is also bad for their business.

In its response, Perplexity argued that Amazon’s position prioritizes advertising and upselling over user experience. “Amazon should love this,” the company wrote. “Easier shopping means more transactions and happier customers. But Amazon doesn’t care. They’re more interested in serving you ads, sponsored results, and influencing your purchasing decisions.

On Amazon’s recent earnings call, CEO Andy Jassy signaled openness to potential partnerships with AI agent developers but said integration must preserve a “good customer experience.” …and perhaps a sponsored recommendation where they can still collect ad revenue wouldn’t hurt.

McDonald’s Leans on Value Deals to Regain Cost-Conscious Consumers

McDonald’s said its renewed focus on value meals is helping drive sales as more consumers face economic pressure. McDonald’s reported higher quarterly revenue and same-store sales, reflecting increased spending on promotions, new products, and marketing aimed at reinforcing its reputation for affordability.

“We continue to remain cautious about the health of the consumer,” Chief Executive Chris Kempczinski said on the earnings call.

After raising prices during the post-pandemic period, McDonald’s has been working to reestablish its value positioning. The company resumed advertising its Extra Value Meals in September and committed tens of millions of dollars to marketing and discounts. These bundles now account for roughly 30% of U.S. transactions. Executives acknowledged that the promotional push weighs on margins in the short term but said the goal is to strengthen long-term customer perception.

“This is an environment where you just have to grind it out,” Kempczinski said.

For 3Q, U.S. same-store sales rose 2.4% y/y, outpacing expectations, while global same-store sales climbed +3.6% y/y. Higher average check sizes helped offset slower traffic. Revenue grew 3% y/y to $7bn, which was in line with forecasts. Shares traded up after the report.

Inflation continued to pressure margins at company-owned restaurants, particularly due to higher beef costs, and McDonald’s expects input costs to remain elevated into next year. The company spent about $40mn promoting its value meals last quarter and plans to provide roughly $90mn in total support to franchisees this year.

Despite inflation and tighter household budgets, McDonald’s maintained its full-year outlook for operating margins, capital expenditures, and unit growth. However, management noted that the consumer backdrop remains uneven. Fast-food traffic is down 2.3% this year, compared with a -1.6% decline for restaurants overall.

Kempczinski said the U.S. economy remains “bifurcated,” with lower-income consumers pulling back on visits while higher-income customers are dining more frequently. Rising rents, food costs, and child-care expenses are pressuring budgets, and uncertainty over federal food-assistance programs could further constrain spending.

Amid those challenges, they noted that new menu items have performed well. Sales of cold coffees, fruit refreshers, and crafted sodas, now being tested in about 500 U.S. restaurants, are exceeding expectations.

McDonald’s currently trades at 25x earnings with a market cap of $213bn.

If you enjoyed reading this, consider sharing it so we know it is worth continuing to produce!

Coverage News.

Copart

Copart shares have fallen -36% from their peak this year, reaching a new 52 week low at $39.60 per share on Thursday. Investors remain pessimistic on short-term revenue growth as auto insurance carriers are optimizing for growth and profitability, and the growing number of uninsured and underinsured motorists, which led to the loss of market share for the first time on record. While Copart says that these are cyclical ebbs and flows, it continues to show up as a headwind to insurance volumes, due to the fact that those vehicles bypass the traditional insurance loss funnel altogether. Backing out cash from the market cap, Copart trades at about 21x trailing earnings.

You can find our most recent Copart Update here

FND

Floor & Decor also hit a 52 week low this week. The stock is now down -40% YTD and back to a price not seen since their Covid drawdown. This comes as they navigate a tough housing market with the lowest existing home sales in 3 decades. Other than perhaps investors being disappointed there might not be another rate cut this year, there is little recent incremental news. FND trades at 29x LTM earnings, however, that includes store opening expenses and and new stores which are under-earning as they ramp up. Once they exit growth mode and operating in a more benign housing market, 15% mature margins are plausible. They currently trade at 12x mature margin earnings.

You can find our most recent FND update here

RH

In the past month, RH has fallen -20%, bringing YTD losses to -60%. Similar to FND, RH is navigating a tough macro environment with low luxury home turnover meaning fewer high-end home furniture buyers. This is admist an aggresive international expansion and the back of a $2bn+ floating debt financed stock buyback. However, if they can acheive even a moderate amount of success with $6bn in revenues at a 18% margin (peak margins were 25%), then that is a 8x multiple on their current EV of $6.8bn. CEO Gary Friedman has much bigger ambitons though and thinks North America alone should be $5bn+ and international should be a much larger business than North America.

You can find our most recent RH update here

Spotlight.

This week, we released several 3Q25 business updates on Appfolio, Coupang, and Axon.

This is in addition to the other 3Q25 business updates we have written on so far this earnings season: LVMH, Evolution, CoStar, Meta, Floor & Decor, APi Group, and Perimeter Solutions.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

Axon 3Q25 Business Update

Rick Smith on “It Just Works”: “Maybe 5, 6 years ago, we were having some conversations with customers about them having some concern about share of wallet, like, hey, are we too dependent like on Axon just because you’re taking up a growing portion of our tech budget. Those conversations have largely disappeared. What I’m hearing from customers now is you know what, when we deploy something with Axon, whether it’s body cameras or records, it just works.”

Read the full AXON 3Q25 Business Update here

Coupang 3Q25 Business Recap

Increasing Selection: As we have long noted, Coupang just needs to simply increase selection in order to continue to increase spend per customer. This message was repeated by Bom Kim on the call when he emphasized “one of the biggest opportunities to expand our customer value proposition and drive future growth is broadening selection”.

Read the full CPNG 3Q25 Business Update here

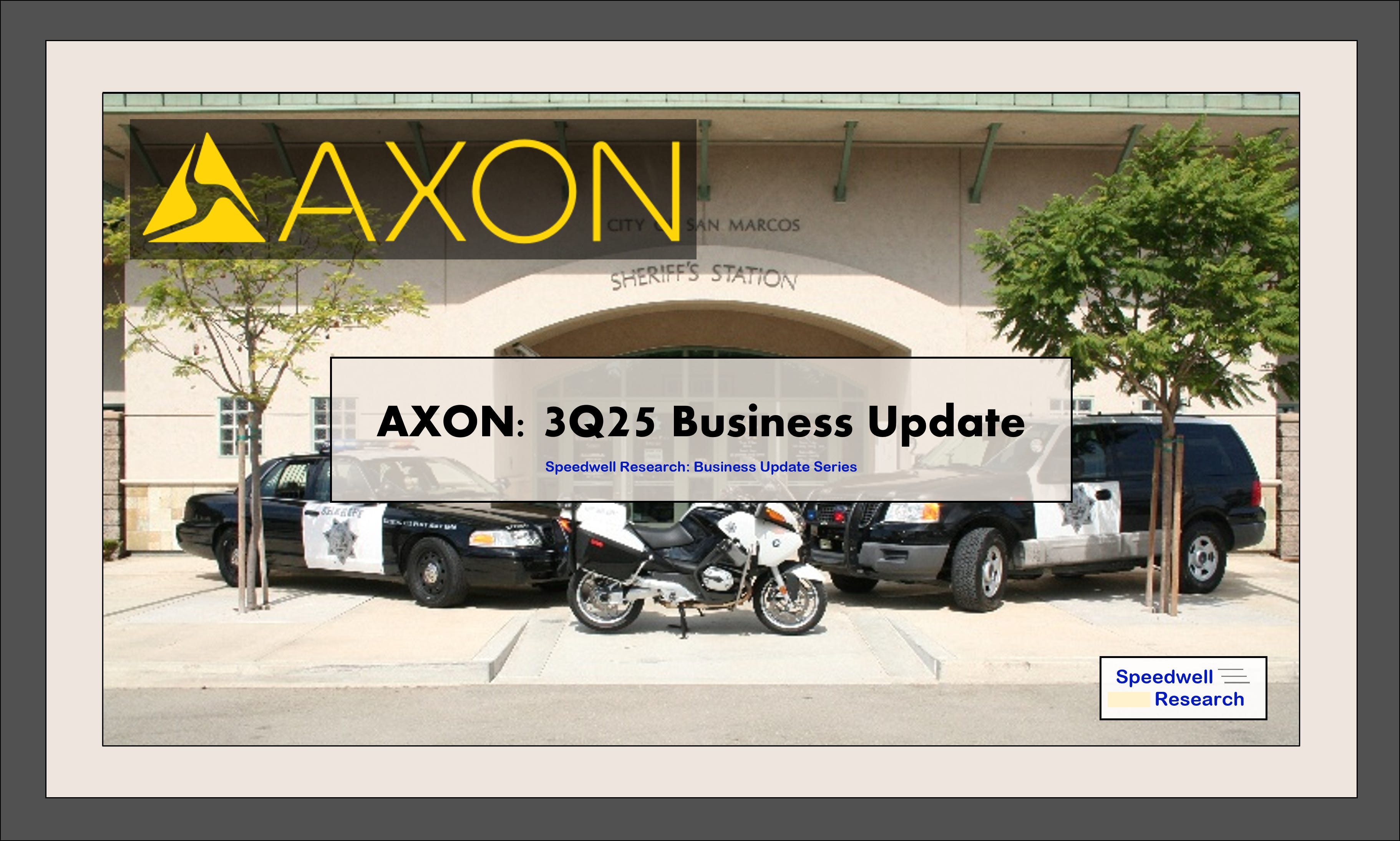

AppFolio 3Q25 Business Recap

Core Services Grows +17% y/y: “Core Services grew +17% y/y, down -200bps sequentially, with units under management growing ~200k q/q to 9.1mn, while total customers were rose +7% y/y to 21,759.”

Read the full APPF 3Q25 Business Update here

The Synopsis Podcast.

This week, we released a Dialogue episode discussing CoStar, Perimeter Solutions, and Meta’s 3Q25 earnings. We hope you enjoy!

Memo of The Week.

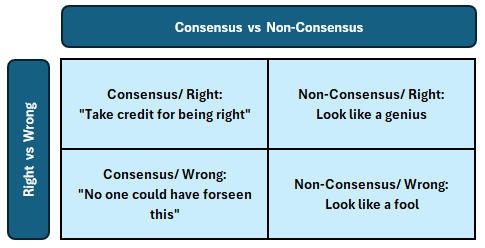

What You Don’t Know About Sell-Side Analyst Price Targets

“Consensus is technically what all sell-side analysts forecast in aggregate. Those earnings estimates that are commonly quoted are an average of analysts’ published estimates. Analysts can see the consensus figures just as investors can and they are very aware when they will be making an “out of consensus” call. They will only want to do so when they feel very strongly about something. However, even then they may choose to be in consensus instead of risking being wrong.”

Learn more about the Sell-Side Price Targets in this memo here 👇

What You Don’t Know About Sell-Side Analyst Price Targets

Company Report Snippet: CoStar Group (CSGP)

Why CoStar & LoopNet Win: “CoStar (& LoopNet) are generally disliked by clients, especially those that have to deal with their sales reps. Many find their pricing to be too aggressive and are turned off by their aggressive policing of logins. In some instances, users reported that letting an admin login on their behalf would quickly result in a CoStar insisting they must purchase another seat—and given CoStar’s litigious reputation, they feel compelled to. It doesn’t help that their subscription pricing is opaque with extreme price discrimination. While some of this is a byproduct of the fact that they used to sell CoStar products individually and by geography, with some grandfathered into old deals, even for newer clients it creates a sense that they are being ripped off. No one feels good when they hear someone is paying less for the same service as them. As a result, interactions with sales reps, who are very commonly their only touchpoint to a real person at CoStar, can be contentious, or at least not pleasurable.”

*This is an excerpt from our company report on CoStar Group.

If you are a Speedwell Research Member, read the full report here: CoStar

If you are not already a Speedwell Research member, you can purchase it here: CoStar Individual Report

Upcoming.

Research

Current research report in progress: Shift4, the payment provider. Shift4 caught our attention because it is in a generally sticky industry (payments + software), still has founder involvement, is growing topline over >20%, and is down -46% from peak. Stay tuned for more!

Business updates on Copart, Constellation Software, Dream Finders Homes, and RH

Dialogue podcast discussing Axon’s and FND’s 3Q earnings.

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: William Isvy (link)

Aswath Damodaran: A Golden Year (2025) (link)

Warren Buffett: 1977 Berkshire Hathaway Shareholder Letter (link)

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).