The Investor's Briefing #1

Massive Jobs Restatement, Rates Go Nowhere, Apple M&A?, Earnings Updates

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed.

Welcome to the first edition of our new weekly newsletter: The Investor’s Briefing.

In Financial News.

The S&P 500 briefly reached an all-time high at 6,427 before a weak jobs report and new tariffs sent the market down almost 3% from peak. The U.S. 10 Year followed suit, falling almost 18bps to 4.21%. The VIX, also called the fear index, jumped 30% to 20.

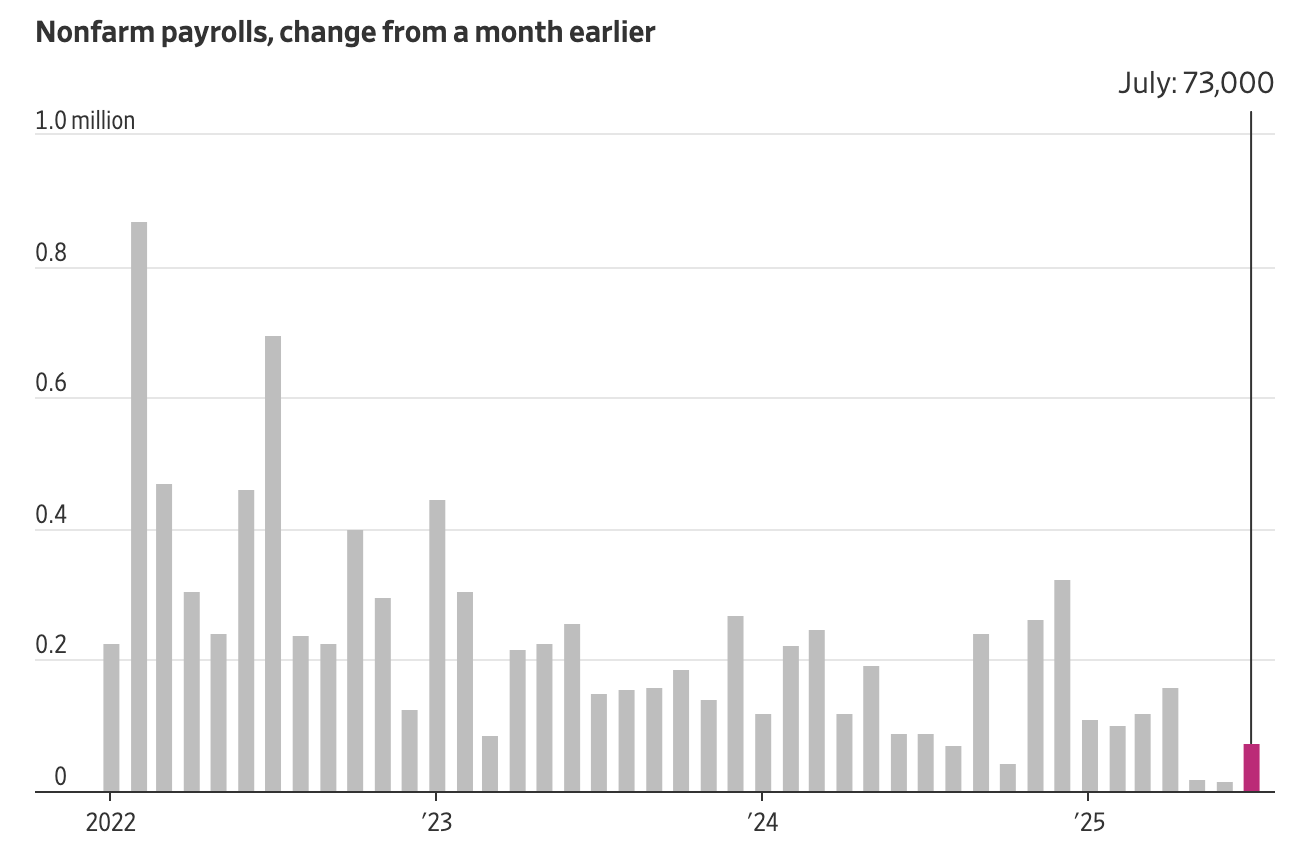

The Labor Department reported a jobs gain for July of 73k, which was 100k less than expected. The even bigger news though was that the prior two months figures were revised downward by 258k. This left the adjusted May and June jobs gains at just 19k and 14k, respectively. While this certainly invites scrutiny as to the Labor Department’s methodology, revisions aren’t uncommon. (Trump did fire the Bureau’s head in response though after levying accusations of data manipulation.)

The unemployment rate in July remained low at 4.2% (or in economic speak, that would constitute “full employment”). Nevertheless, this suggest that the paralysis experienced by businesses in the aftermath of the original “Liberation Day Tariffs”, was more than initially reported.

However, it is worth noting that 109k of jobs revised downward were from a miscalculation with public school employees. Either way, the numbers implies a softer economy, and thus gives the Fed more rationale for cutting rates sooner. The odds of a rate cut in September jumped from 38% on Thursday to 83%.

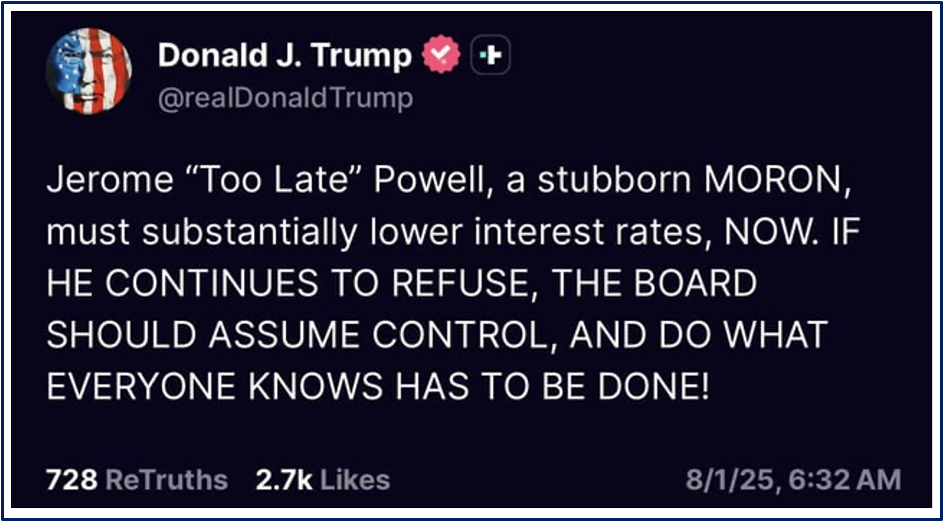

The Fed actually met Wednesday prior to the downward jobs revision and decided to hold rates steady—although that decision was met with rare dissent. For the first time since 2020, two Fed officials dissented and voted in favor of an immediate quarter point rate cut. Powell signaled a concern that inflation may not have been totally beat yet and it is better to be cautious than too early:

“If you move too soon, you wind up maybe not getting inflation all the way fixed and you have to come back [and raise rates]. That’s inefficient. If you move too late, you might do unnecessary damage to the labor market.” – Jerome Powell.

Complicating this balance is the fact that President Trump has been publicly calling for Powell’s dismissal and has vocally expressed that rates are too high. No doubt recalling Volcker’s error of lowering rates too soon in 1980 from almost 20% to 9%, only to then reverse course a year later, is fresh in Powell’s mind. After Volcker lowered rates, inflation quickly flared back up and interest rates were jacked back up to ~19%. Ironically, this back and forth rate movement caused the very recession Volcker was trying to avoid. It is widely believed the inflation was much harder to beat and caused much more economic pain as a result of this whipsaw.

While Trump may brand Powell as “Always Too Late”, Powell is trying to avoid a worse risk from materializing: inflation creeping back up and fresh rate hikes not only causing an economic slowdown, but failing to quickly address inflation. This so called “stagflation”, is especially hard to beat once it crystalizes.

With a lot of movement on trade tariffs, there is still a lot of economic distortions. Although a tariff regime is beginning to take form: Trump’s newest tariffs policy calls for 15% tariffs on countries running small trade surpluses and 10% for those with a deficit. Deals were struck with Japan and the EU at 15%. While negotiations ensue, Mexico is at 25% and China sits at 30% . A 25% tariff on India and a 20% on Taiwan were also placed. The full economic impact is still being ingesting by the American consumer and the rest of the world.

Company News.

The best way to understand the economy though is to look at individual businesses. This week many companies reported earnings:

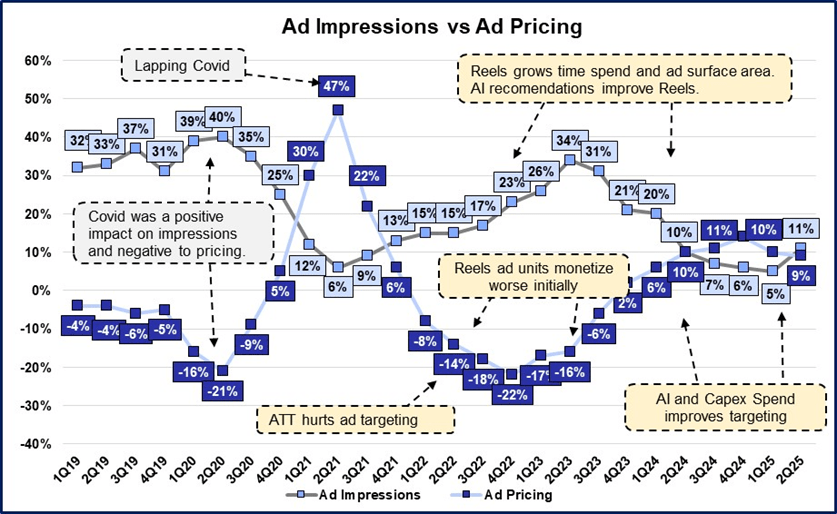

Meta revenues reaccelerate 600bps to +22% y/y. The stock reached new all-time highs at $773 before retreating to $750 on Friday.

We released a full update and calculated their ROIC on their massive capex outlay (more on it below).

Microsoft posted strong revenue growth of +18% driven by their Azure Cloud segment growing +34%. The stock jumped +9% before selling off at the end of the week and closing at $524.

Apple grew revenues +10% as iPhone 16 sales were strong. While that may seem like a strong result, looking at LTM revenues they have only grown at a 3% CAGR since 2021.

Apple has seemingly been caught flat-footed by AI. On the call Tim Cook said “we're very open to M&A that accelerates our road map”. Their last meaningful acquistion was Beats in 2014 to accelerate their Apple Music Streaming service. The need for Beats could be seen as a strategic failure though, as Steve Jobs was of the opinion that streaming wouldn’t ever be that popular because he thought people wanted to own their music. When that proved not to be the case, they had to make up for lost time.

Amazon revenues grew +13% y/y with AWS +17% y/y and advertising +22% y/y. Lower growth versus peers (Azure +34% and GCP +32%) and a disappointing guide drove the stock down -8% to $214.

Booking Holdings noted on the call that U.S. consumers, particularly those booking lower-rated hotels, are exhibiting greater caution in their travel spending. This is contributing to pressure on the domestic travel segment, especially in the more affordable hotel categories. In contrast, European markets remain resilient, with travel demand holding steady.

A former director at Coupang noted in an interview that they believe Coupang can have similar success in Taiwan:

"If they can mimic the same success they did in Korea, which I think they will, they will probably generate about the same amount of revenue from Korea, probably more because we already have all those developed." (Alpha Sense Expert Insight Interview)

We are experimenting with new content formats, so if you enjoyed this summary, please drop a comment or like so we know to keep doing it in the future! Feedback welcomed.

Spotlight.

This week, we released 4 business updates on Meta, Api Group, Floor & Decor, and AppFolio, as well as a business recap on CoStar Group.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

Meta 2Q25 Business Update.

Advertising Dynamics: “Ad impressions grew +11% y/y, mainly driven by Asia Pacific. Average price per ad increased +9% driven by increased advertising demand and improved ad performance. CFO Susan Li noted on the call that “pricing growth slowed modestly from 1Q due to the accelerated impression growth in Q2”, which is exactly what you would want to see.”

Read the full update here: Meta 2Q25 Business Update

FND 2Q25 Business Update.

FND President Bradley Paulsen on the Opportunity to Take Market Share:

Read the full update here: FND 2Q25 Business Update

APG 2Q25 Business Update.

New 2028 Long-Term Targets: “Their 2028 targets are now called 10/16/60+. Their 2028 targets are 1) over $10bn in revenues, 2) 16%+ adjusted EBITDA margin, 3) 60%+ of revenues from inspections, services, & monitoring, and 4) over $3bn in cumulative adjusted free cash flow through 2028.”

Read the full update here: APG 2Q25 Business Update

AppFolio 2Q25 Business Update.

Decreasing Churn & Improving Pricing Power: “77% of their Plus and Max plans have adopted Stack, which is important because the more they utilize AppFolio as a platform for all of their property management needs, the less likely they are to ever churn and the more pricing power AppFolio will build overtime.”

Read the full update here: AppFolio 2Q25 Business Update

CSGP 2Q25 Business Recap.

The Growing Differentiator of Matterport: “Listings with Matterport 3D tours receive 23x more leads, and consumers spent +71% more time on those pages. However, high up-front camera costs (~$6,500 for the first scan vs a 2nd costing just $3) have limited broader adoption. They plan to fix this by making Pro 3 and future Pro 4 cameras more accessible, expanding the salesforce, and embedding Matterport across its entire platform suite.”

Read the full update here: CSGP 2Q25 Business Recap

The Synopsis Podcast.

This week, we released a dialogue episode discussing one of our latest business memos called The Invisible Competitor. In this episode, we talk about reframing disruption, how good businesses can become irrelevant, and when to copy competition. Listen or read below!

Memo of The Week.

The Risk Circle: Deciding What Risks Matter and When

Every investment rests on countless assumptions, yet most investors only focus on a narrow set of “acceptable” risks within the Risk Circle. History shows that risks outside this circle, like inflation, regulatory shifts, or systemic shocks, often go unpriced until it’s too late. While not all risks can be quantified, they must be acknowledged and managed. Ultimately, great investing requires not just identifying upside, but deciding which risks you can live with, which to ignore, and which to walk away from entirely.

Read the full memo here: The Risk Circle: Deciding What Risks Matter and When

Company Report Snippet: APG

Speciality Services Tailwinds: “They note that there are various tailwinds that they can benefit from in their Specialty Services segment, including the Infrastructure Investment and Jobs Act, The CHIPS Act, and the growing data center spend driven by AI. The more money spent on infrastructure, the more of a need there is for their various services like installing power lines, HVAC systems, water and sewage infrastructure, and fabricated steel structures.”

*This is an excerpt from our company report on APi Group.

If you are a Speedwell Research Member, read the full report here: APi Group

If you are not already a Speedwell Research member, you can purchase it here: APi Group Individual Report

Upcoming.

Research

LVMH is currently in the works.

Coverage

DFH business recap

Axon, Coupang, Perimeter, and CSU are all scheduled to report earnings next week. For our latest updates on these names, click here → Business Updates

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Marc Andreessen Blog Post The Netscape Advantage (1997) (Link)

Howard Marks: Mr. Market Miscalculates (link)

Michael Mauboussin on Measuring the Moat, Assessing the Magnitude and Sustainability of Value Creation (link)

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).