The Investor's Briefing #16

CSU Head of M&A on AI, Disney's Lost Decade, Mr. Market's Bipolar Behavior

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the sixteenth edition of our weekly newsletter: The Investor’s Briefing.

Announcement: 3Q25 Earnings

Speedwell Members have already received 12 earnings updates. Become a Speedwell Member today to stay up to date on all of the great businesses we cover! See our full coverage here.

Published: Constellation Software, Airbnb Appfolio, Axon, APi Global, CoStar Group, Coupang, Evolution, Floor & Decor, LVMH, Meta, Perimeter Solutions

Upcoming: Copart, Dream Finders Homes, Casey’s, and RH

Get all of the updates plus our in-depth research reports today and lock in our current pricing forever. If you are at a fund, reach out to info@speedwellresearch.com for help getting your subscription expensed.

In Financial News.

The Nasdaq was down as much as -3.5% during the week before making a bit of a comeback to finish the week down -1.8%. The less tech-heavy S&P 500 had a more muted week and was down only -1.7% at lows before recovering to only be down -0.5% for the week. Investors seem to seesaw quickly between a desire to be more defensive and a fear of missing the next equity rally. Since April lows, the S&P 500 is up 35%, with many popular tech names like Nvidia, Broadcom, Palantir up over 100%. The feeling that everyone seems to be making money, paired with fears that the good times are about to come to an end with extended valuations versus history, gargantuan capex commitments, and daily talks of a bubble is a dangerous mix of emotions driving investors.

Another element in the mix is investors no longer expecting a December rate cut. The shift followed a wave of cautious remarks from several Fed officials. Neel Kashkari, Beth Hammack, and Alberto Musalem each signaled discomfort with additional near-term easing, highlighting persistent inflation pressures and the need for patience as policymakers assess incoming data. As a result, the market-implied probability of a December rate cut—which had been above 70% just a week earlier—fell to roughly 50%. The repricing triggered heightened volatility and pushed investors out of high-growth, high-multiple stocks, only for this to later slightly reverse.

At the same time, even more uncertainty is being added into the market due to a backlog of delayed economic releases following the end of the U.S. government shutdown. The absence of timely data has made it harder for markets to form a clear view of the underlying macroeconomic environment and harder to read the Fed.

Adding to the unease, corporate layoff announcements continued to surface. Verizon said it will cut roughly 20% of its workforce, its largest downsizing on record, intensifying concerns about mounting labor-market pressure. On the other hand, investors wonder to what extent can AI help improve productivity and thus corporate profits.

Despite excitement around AI and Trump trying to structurally change the U.S. Economy with tariffs and trade deals, investors are acting as they always have, bouncing between greed and fear, and letting the market dictate which emotion should lead at any moment.

Company News.

Former Head of M&A at CSU on Mark Leonard, Copycats, and AI (AlphaSense Expert Call)

A former senior M&A executive at Constellation Software described the company as entering a more challenging—but still manageable—phase in its evolution, as it navigates leadership transition, intensifying competition for deals, and growing uncertainty around the implications of AI.

He said Mark Leonard’s resignation was a genuine surprise internally and externally: “It was, and I think it was a surprise to most people. I don’t think anyone saw it coming.” Constellation has been “quite secretive” about what triggered the decision, and the timing around Leonard’s abrupt AI call struck him as odd: “Just a day earlier, he held a call on AI, and it wasn’t the most straightforward call. A day later, they announced he was resigning. It definitely was a surprise.” Asked whether the AI call and resignation might be linked, he avoided speculation but acknowledged the inference: “It’s hard for me to say if both things are related. You might certainly infer that because he decided to resign a day later, that maybe he knew.”

What is clearer, in his view, is that the market attributes a real key-man premium to Leonard. He likened it to Berkshire Hathaway and Warren Buffett: “You could think about it the same way, more or less, someone who would buy Berkshire Hathaway stock buys it because of Warren Buffett.” He added, that while Constellation typically acquires companies at roughly 1x gross revenue, its own multiple was close to 8x revenue and is now just over 5x (as of mid-October). “The decline itself is a testament to the market’s fear that things might not be the same due to Mark Leonard’s departure. That potentially could be overblown, but there certainly is a deposit of faith because of Mark Leonard’s presence.”

On day-to-day operations, he emphasized that Leonard’s involvement was selective and focused on large, complex, or higher-risk deals—typically above $100 million in equity value, or when entering a new market perceived as high risk. Leonard was also deeply involved in VMS Ventures, a growth-equity arm that incubates and invests in VMS companies. His departure therefore raises a real question about who will now drive these more creative, complex initiatives.

In the near term, that responsibility falls to Mark Miller, the former CEO of Volaris and the founder of Trapeze, Constellation’s first acquisition. Miller led Volaris until last year, when he stepped back into a chairman role, widely interpreted internally as a prelude to retirement. The expert interprets Miller’s appointment as a near-term solution rather than a long-planned succession: “The fact that they’ve appointed him to take Mark Leonard’s role… if this had been the planned succession, they probably wouldn’t have appointed him to the role.” At the same time, he stressed that Constellation’s highly decentralized model limits operational disruption: “With regards to Constellation and the pursuit of its strategy, it’s pretty much business as usual. I don’t think much would change with regards to that,” and most employees “probably won’t feel the difference from Mark Leonard’s departure.”

He repeatedly underscored how deeply decentralized Constellation is. Divisions originate and execute acquisitions independently within broad guardrails, and decision-making is pushed down, giving operators and deal teams substantial autonomy. Over time, that has produced internal competition for deals. Divisions set up as “swim lanes” by geography or vertical have grown large enough to compete directly: if you ask employees who their biggest competitor is, “they’d probably say another division of Constellation.”

To manage this, Constellation uses a centralized Salesforce-based database that logs every interaction with a target. Once an M&A professional records key data on a company after an initial call, that account becomes “protected” for a year, meaning no other division is allowed to directly approach the target in that period. When the protection period expires without a deal, other divisions are free to reach out. Business development teams routinely scan the database for accounts where protection is expiring. In practice, rules are not always perfectly followed, and a seller may find themselves fielding inbound interest from multiple parts of Constellation, which can be confusing and messy.

All of this complexity overlays a more fundamental challenge: Constellation’s scale now requires larger deals to move the needle. Historically, the “bread and butter” were sub–$10 million revenue VMS acquisitions. With a market cap that has grown dramatically and low organic growth, small deals alone are no longer sufficient: “They need to do larger and larger deals to actually move the needle… and they’re not necessarily winning these larger deals.” Competition has intensified from “copycat” platforms such as Banyan and Valsoft, which emulate Constellation’s model but often target higher-growth, higher-margin businesses and are willing to pay richer multiples. The universe is more crowded, particularly in Europe, making both sourcing and winning deals harder.

He also highlighted the lag between public and private software valuations. While public multiples have reset materially, many private sellers remain anchored to peak valuation anecdotes: “It might take two years to convince that guy that’s not the case.” That lag, combined with fiercer competition, makes it harder for Constellation to deploy its growing free cash flow at historical returns.

Despite those headwinds, he said Constellation remains extremely disciplined on price. Hurdle rates for deals are set based on the target’s net recurring revenue: below $1 mn NRR, 30%; $1–4 mn, 25%; above $4 mn, 20%. He told a story that if his modeled IRR comes in even slightly below the threshold—say 19.5% versus a 20% hurdle—the deal is rejected, with very little tolerance for “tweaking” assumptions. Management briefly considered introducing a 15% hurdle rate for very large transactions but abandoned the idea. In higher-inflation markets, Constellation now applies dual hurdles—a nominal and an inflation-adjusted rate—and a deal must clear both. He contrasted this discipline with copycats and some private equity buyers who are more willing to stretch on price.

He noted that Constellation has looked beyond pure VMS in select cases, including BPO (Business Process Outsourcing)-like businesses and payments platforms. Non-VMS targets face a higher bar: the investment committee must be convinced cash flows are recurring and predictable enough to resemble software economics. Payments deals have typically been vertical solutions that can be embedded into the portfolio, creating both direct financial returns and indirect benefits via shared learnings and playbooks.

On AI, he characterized Constellation’s posture as clearly defensive rather than aggressive: “Certainly not AI-forward.” AI only became a structured topic at internal leadership conferences in the past year, and adoption is left to individual divisions and businesses. He sees AI as both a risk and an opportunity, but noted the return profile is still too uncertain for Constellation’s culture: “The question with AI is it’s an investment for what, as of now, is still an unclear ROI. That’s why Constellation is a bit reluctant to… develop platforms internally whose returns will be unclear.”

From a customer perspective, he has not yet seen churn driven directly by AI displacement. Instead, AI has raised the bar on user experience and data access. Many Constellation products are legacy and “clunky,” but relationships are long-standing, solutions are deeply tailored to niche workflows, and switching is painful. Customers typically complain first—about UX, pricing, or modernization—giving Constellation a chance to respond. On the cost side, he sees AI as a potential support for R&D productivity and modernization, but cultural resistance among engineers and technical staff is meaningful, driven by job-security fears.

He also noted a growing internal emphasis on organic growth levers, particularly pricing and shifting from on-premise license models to cloud/SaaS contracts that better support inflation-linked increases. Until a few years ago, many businesses lacked explicit inflation pass-through, which became a problem post-pandemic. The emerging approach is to pair price increases with tangible improvements—better support, more modern platforms, cloud migrations—to justify higher pricing without triggering churn.

This is from an AlphaSense Expert Call Interview.

You can get a free trial of AlphaSense here

Disney Slumps as Market Questions Iger’s Turnaround Strategy

Disney shares fell more than 8% in early trading Thursday after the company’s latest quarterly results failed to reassure investors that its turnaround strategy is gaining traction. Despite growth in streaming and theme parks, weakness across the television and film divisions weighed on performance and pushed overall results below Wall Street expectations.

To start, revenue for the fiscal fourth quarter came in roughly flat at $22.5bn, while operating income fell -5% to $3.5bn, as declines in Disney’s linear TV and movie businesses more than offset gains in its parks and streaming units.

As a result, the lackluster report extended a multiyear stretch of stock price underperformance. Disney shares have stayed between $80 and $125 since early 2022—well below the nearly $200 reached in 2021. More incredible, shares trade at the same price they did 10 years ago, marking a lost decade for investors. The stagnant share price has heightened investor concerns over CEO Bob Iger’s ability to reset the company’s growth trajectory since returning in late 2022.

Compounding those concerns, analysts have pointed to Disney’s slow transition away from linear television and uncertainty around the returns on its $60 billion investment plan for parks, resorts, and cruise ships. In an effort to bolster confidence, Disney said it would double share repurchases to $7bn this fiscal year and increase its dividend by 50% to $1.50 per share.

At the same time, Iger emphasized the long-term opportunity in streaming, positioning Disney+ as more than a content platform. He described a vision in which the service becomes an AI-enabled digital ecosystem that allows fans to shop, play games, engage with theme parks and cruise ships, and even create user-generated content based on Disney properties. “The opportunity here is enormous in terms of increasing our engagement with Disney fans,” he said. Investors have their doubts though.

In terms of user growth, subscriptions across Disney+ and Hulu rose +12.4mn during the quarter to 196mn. Roughly half of the additions came from a new distribution deal with Charter Communications, with most of the remainder from international markets. Disney expects streaming profitability to reach 10% in the current fiscal year, up from about 5% last year.

On the sports front, Disney did not break out results for the new ESPN streaming service, launched in August. However, Iger said early indicators were positive, noting that 80% of subscribers signed up through a bundle with Disney+ and Hulu—part of a broader effort to reduce churn through packaging.

Elsewhere, the company’s experiences division, which includes theme parks, resorts, and cruises, remained a key profit driver. Operating income rose +13% to $1.9bn, led by strength at Disneyland Paris and in cruise operations. Experiences contributed more than half of Disney’s total profit. The company is currently executing a $60bn, 10-year expansion of its parks and cruise business, including major new attractions and an increase in its cruise fleet to 13 ships.

In contrast, film performance remained uneven. The quarter’s biggest release, Marvel’s “The Fantastic Four: First Steps,” underperformed expectations, especially compared with 2024’s hit “Deadpool & Wolverine.” The new quarter began with the flop “Tron: Ares,” though Disney posted a stronger opening with “Predator: Badlands.” Looking ahead, the company is counting on “Zootopia 2” and “Avatar: Fire and Ash” to help stabilize its theatrical slate heading into the holiday season.

Taken together, the results highlight the complexity of Disney’s turnaround. While streaming and experiences continue to show momentum, persistent struggles in legacy media and inconsistent box-office performance remains a hurdle. Investors, therefore, are still waiting for clearer evidence that Iger’s strategy can meaningfully accelerate growth and close Disney’s widening gap with the broader market. Disney trades at 17x earnings.

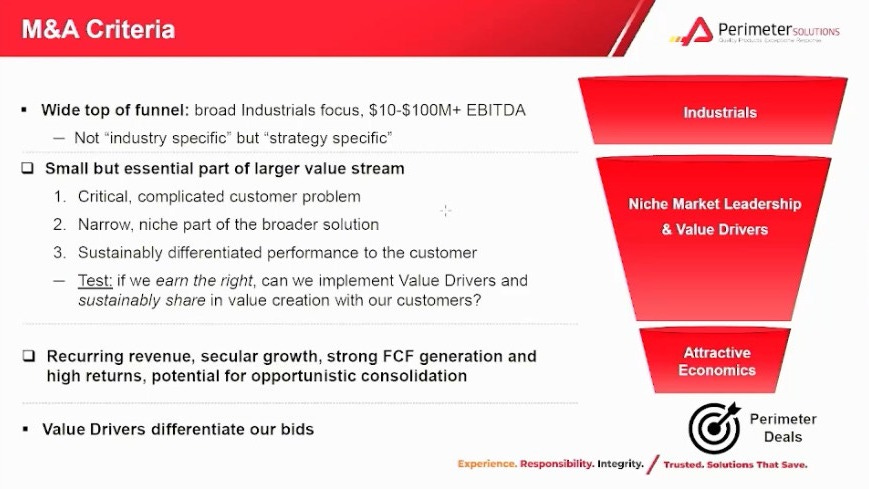

Perimeter Solutions Strikes Contract for Steadier Revenue

On Wednesday, Perimeter Solutions presented at the Baird Industrials Conference. CFO Kyle Sable talked more about the renewed U.S. Forest Service (USFS) contract and how they are shifting their revenue mix to more fixed revenues in order to be less tied to fire season volatility and to smooth out earnings. He stated that they are pursuing more deals similar to the USFS contract that are longer-term contracts and are based on fixed revenues.

He also mentioned the initiative to push more into the powder-based fire-retardant product over the liquid-based, as a way to help improve manufacturing efficiency as well as increase gross profits, since the powder-based fire retardant is cheaper to produce, but just as effective. We go into a lot more detail about this shift, along with the USFS contract, in our most recent Perimeter 3Q25 business update.

Lastly, Kyle Sable talked about their M&A strategy, stating, “We are not looking for adjacencies to our current product portfolio. Instead of being sector specific, we’re strategy specific… we are looking for high-quality businesses that have recurring revenue, growing secular tailwinds, high margins, high returns, and potential for additional M&A.” Perimeter is up +81% YTD and trades at 24x earnings at a $3.8bn market cap.

If you enjoyed reading this, share, like, or comment so we know it is worth continuing to produce!

Spotlight.

This week, we released several 3Q25 business updates on Airbnb and Constellation Software.

This is in addition to the other 3Q25 business updates we have written on so far this earnings season: Appfolio, Coupang, Axon, LVMH, Evolution, CoStar, Meta, Floor & Decor, APi Group, and Perimeter Solutions.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

We also released a free excerpt of our APi Global research report that details the business history of APi Global, going from a small plumbing company to a global B2B service provider.

Below are select quotes from our most recent business updates & recaps

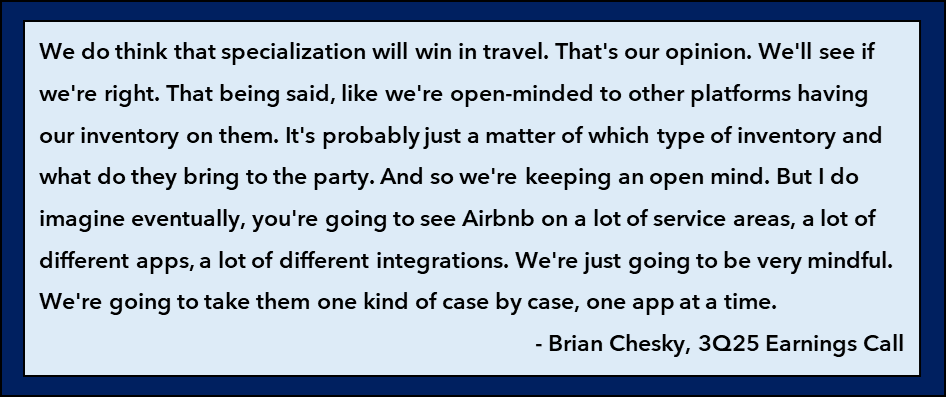

ABNB 3Q25 Business Update

Specialization Will Win in Travel:

Read the full ABNB 3Q25 Business Update here

CSU 3Q25 Business Recap

Is AI Narrowing the Moat?: “There isn’t any real benefit to the business owner for leaving their existing VMS solution. This is also why this has been such a great business for the past several decades and Constellation was able to survive the transition from on-premise to cloud just fine. While investors should have their own opinion on the AI risk, at least so far it does not seem like there is a clear benefit to a business owner to switch. And as long as there is no improved value prop, customers aren’t going to move anywhere.”

Read the full CSU 3Q25 Business Recap here

The Synopsis Podcast.

This week, we released a 2 new podcasts! The first was a Dialogue episode discussing Axon’s and Floor & Decor’s 3Q25 earnings. The second was an Article episode reading the APi Global business history. We hope you enjoy!

Axon and FND Dialogue

APi Global Business History

Memo of The Week.

WeChat, Meituan, and Grab: What is a SuperApp and Why You Will Fail Building One

“A proper SuperApp effectively acts as a low-cost funnel of future customer acquisition for different offerings by keeping customers captive to a slew of everyday services. The high frequency nature of these “everyday services” keeps consumer churn de minimus. Since the consumer already uses the app regularly, getting consumer adoption for a new service is as simple as promoting it on the home page.

At its best, an app rolls out a new service and can easily get a large portion of their users to sign-up for it. Since it is all in the same app, there is little friction to signing up with preloaded payment and user info. The new service may not only be profitable in and of itself, but increases usage of the app, making it stickier. The increased clicks on the app opens the door for more cross-sell opportunities and perhaps even increases usage of the original service by remaining more top of mind. It is a flywheel at its best.”

Learn more about the SuperApps in this memo here 👇

WeChat, Meituan, and Grab: What is a SuperApp and Why You Will Fail Building One

Company Report Snippet: Coupang (CPNG)

Pulling the IPO to Mimic Amazon: “Six months into their IPO process, and just a mere week before the prospectus was supposed to be printed, Bom Kim had a moment of clarity and pivoted the business. Bom Kim thought, “if we really wanted to provide something that really mattered to customers—100 times better, exponentially better—we had to go through an enormous amount of change”. They pulled the IPO, knowing they would have to remain private for the immense business shift and heavy investment period they were about to undertake.

The third party marketplace they operated offered an inconsistent experience with a variety of different sellers and limited logistics coverage nationally. The mixed merchant experience combined with unreliable shipping—half of all complaints were about shipping—helped clarify what Coupang would need to build in order to achieve a “100x better experience”. Coupang would mimic Amazon by building out a large first party offering and their own logistics network.”

*This is an excerpt from our company report on Coupang.

If you are a Speedwell Research Member, read the full report here: Coupang

If you are not already a Speedwell Research member, you can purchase it here: Coupang Individual Report

Upcoming.

Research

Current research report in progress: Shift4, the payment provider. Shift4 caught our attention because it is in a generally sticky industry (payments + software), still has founder involvement, is growing topline over >20%, and is down -46% from peak. Stay tuned for more!

Business updates on Copart, Dream Finders Homes, and RH

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Howard Schultz 1992 Shareholder Letter (link)

Best Anchor Stocks: The PE ratio: Not All Growth is Created Equal (link)

Warren Buffett’s Thanksgiving Letter (link)

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).