The Investor's Briefing #7

Oracle Outshines, OpenAI's $300bn Commitment, Largest Negative Labor Market Revision Since 2009

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the seventh edition of our new weekly newsletter: The Investor’s Briefing.

In Financial News.

U.S. equities climbed to record highs as Oracle shares posted their best day since 1992, soaring over 40% as they revealed a $317 billion increase in contracted revenue. On going increases in data center spend pushed the semiconductor index up ~4%. The S&P 500 was up only +1.4% though, as the BLS (U.S. Bureau of Labor Statistics) slashed nearly 1 million jobs from prior reported employment gains, the deepest cut since 2009. This combined with a cooling labor market and inflation data suggesting price pressures are moderating, will be top of mind during next week’s FOMC meeting.

Oracle’s massive stock price move added over $100 billion to Larry Ellison’s fortune. The majority of Oracle’s new contracts are rumored to have come from OpenAI with the two striking a $300 billion deal for cloud services. As a neutral player who doesn’t have chip or consumer product ambitions— Oracle is well postioned to win contracts with customers that are weary of turning over data or money to the big cloud providers, who are often also competitors.

Other recent high profile customer wins include Nvidia and ByteDance’s TikTok. Oracle’s contracted revenues now sits at $455 billion at the close of its fiscal first quarter

The reaction spilled across the broader market. Semiconductor stocks rallied sharply on expectations of rising AI infrastructure spending, with Broadcom gaining 10%, Nvidia up 3%, and AMD rising 24%. Even utility companies, with exposure to data center power, advanced, as investors began to price in the downstream beneficiaries of the accelerating buildout of AI-driven computing capacity.

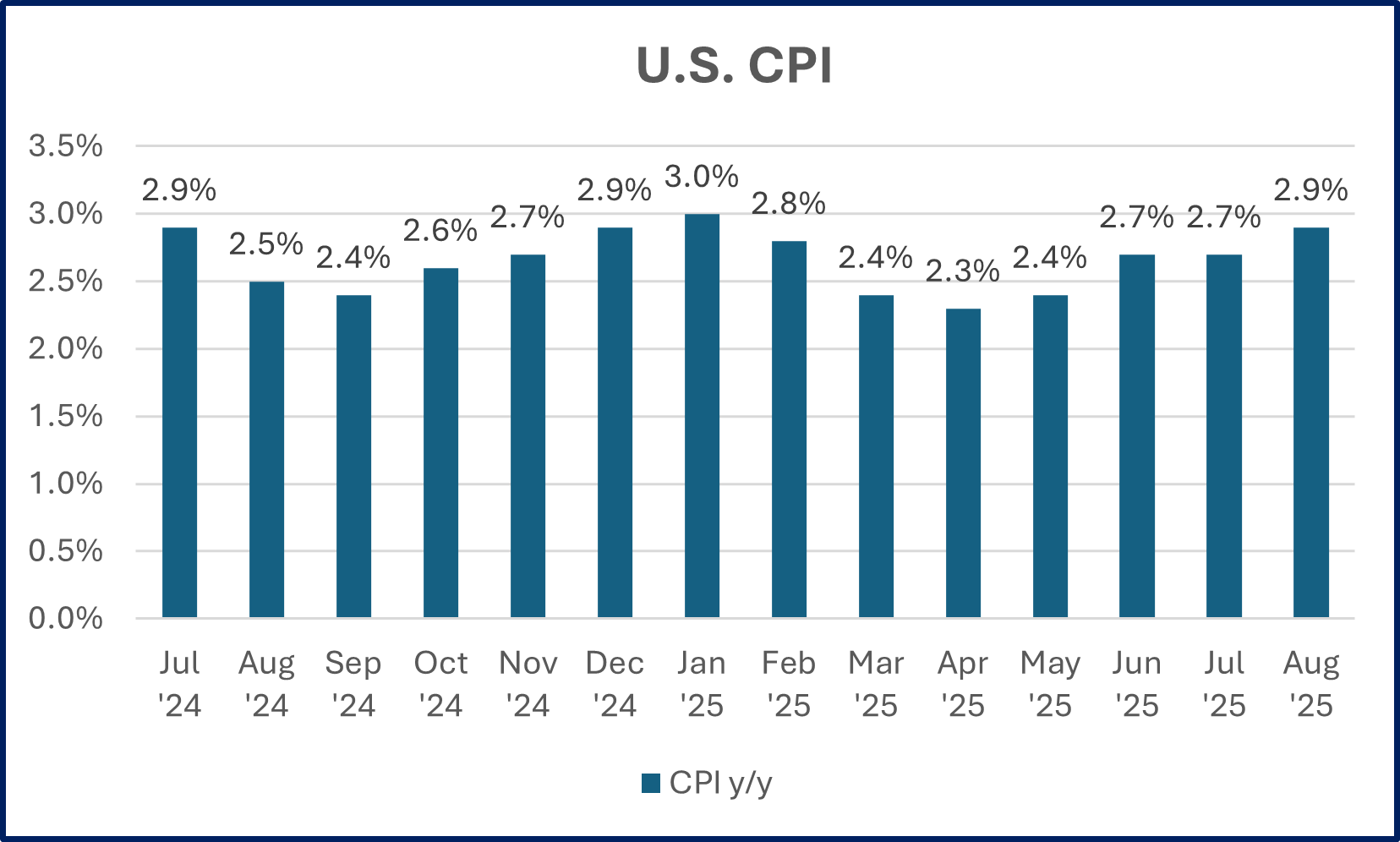

Inflation data presented a mixed picture in August. The Producer Price Index (PPI), which measures wholesale and business-level input costs, cooled to 3.3% y/y, coming in below consensus expectations and signaling some relief in upstream pricing pressures. By contrast, the Consumer Price Index (CPI), the more closely watched gauge of household inflation, surprised to the upside at 2.9% y/y. That marks the hottest CPI print since January and keeps price growth above the Federal Reserve’s long-term 2% target.

Earlier in the week, the BLS said total employment gains for the 12 months ending in March 2025 were overstated by 911,000 jobs. In terms of total jobs lost, the revision marks the largest preliminary downward adjustment since recordkeeping began in 2000. By percentage, it is the deepest cut since 2009 during the financial crisis. That cuts reported growth by more than half, from 1.79 million to just 880,000 jobs.

While Tuesday’s release is preliminary, the final revision won’t be published until February 2026. This is not the first time preliminary revisions overstated job losses. In August 2024, the BLS estimated 818,000 fewer jobs for the year ending March 2024. The final revision proved smaller, at 598,000 fewer jobs. However, even if the revision moderates Tuesday’s estimate, the correction will still rank among the largest in decades.

In addition, applications for U.S. unemployment benefits increased last week to the highest level in nearly four years, signaling that layoff activity may be accelerating as the labor market cools. Initial claims rose by 27,000 to 263,000 for the week ending September 6, the highest reading since October 2021. The sharp increase underscores growing signs of stress in the job market, which has already shown evidence of a pronounced slowdown in hiring over recent months.

Markets seemed to interpret these reports as giving the Fed more room to lean into labor-market weakness rather than doubling down on inflation-fighting measures. Treasury prices rallied alongside equities as investors bet policymakers would tilt their focus toward helping the labor market and avoid overtightening, rather than holding interest rates steady.

With inflation running moderately above the target but a labor market that is weaker than expected, markets expect the Fed to cut rates by 25 basis points at next week’s FOMC meeting, with some economists forecasting up to three rate reductions by year-end.

Company News.

Oracle had its “Nvidia Moment” when it reported earnings earlier this week. The 48-year-old software firm reported an unprecedented surge in its cloud revenue projections. This stunning growth led Oracle to forecast that its cloud server rental revenues will skyrocket from $10 billion in fiscal 2025 to $144 billion by fiscal 2030, rivaling industry leaders like AWS.

However, it is worth noting they potentially have counterparty risk. OpenAI, who is responsible for most this increase is burning through tens of billions of cash. While it is true that they have had little issue raising capital and have many strong partners including Microsoft, they still only generate around ~$12bn in ARR. This single 5-year contract binds them to potentially $60bn a year in spend.

While we don’t know the details of the deal, no doubt OpenAI will need a lot of revenue growth or funding to take them into 2030 in order to avoid missing payments. The Information reported last week that OpenAI is expecting to burn $115bn through 2029. It is not clear if this figure includes the Oracle deal. Even if AI is as huge as the most ardent propents think it will be, it doesn’t mean OpenAI’s revenue model will necessarily be as strong. That’s not to say it can’t be, just that a lot already has to go right for them in order for them to meet their existing obligations.

Apple unveiled its iPhone 17 lineup and the new ultra-thin iPhone Air at its annual September event. This came alongside updated Apple Watches and AirPods Pro 3s. But all of this was expected and shares slipped -3% in response. The iPhone, Apple’s >$200 billion core business, remains a mature segment with low volume growth, so the company is leaning on pricing. The iPhone Air is priced above the Plus models it replaced. A new 2TB iPhone Pro costs $1,999, lifting average selling prices ~12% y/y. With 38% of U.S. users on three-year-old devices. Apple is betting that customer loyalty and delayed upgrade cycles will support near-term demand even as it lags peers in AI and faces policy pressure to reshore manufacturing.

Klarna debuted on the NYSE on Wednesday with shares jumping as much as 30% intraday before closing up 15% at $45.82, giving the Swedish “buy now, pay later” firm a market value of ~$15bn. The IPO priced above range at $40, raising $1.4bn from 34 million shares, and marks another strong showing in a recovering IPO market following Circle and Figma’s high-profile debuts. Founded in 2005, Klarna is expanding beyond installment lending with products like a Visa debit card and a new U.S. partnership as Walmart’s exclusive BNPL provider, while also adding eBay, Nexi, Worldpay, and J.P. Morgan Payments integrations.

Synopsys, the chip-design software maker, suffered its worst single day on record, falling -36% on Wednesday due to U.S. export restrictions impacting its China IP business, which posted a -8% decline in the quarter. This lackluster result is expected to continue into 2026, as Synopsys CEO Sassine Ghazi stated that the push to develop its own IP isn’t achieving the desired results. Management is laying off 10% of its workforce as a result of weakness and a move to refocus its resources on other initiatives. Sysnopys has a $80bn market cap.

Kroger, the third largest supermarket chain in the United States, released positive earnings driven by strong +3.4% same store sales growth (excluding fuel), a +16% surge in e-commerce sales, and improved gross margins. Categories helping sales growth were pharmacy and fresh offerings. Management raised full-year 2025 guidance for sales and operating profit, emphasizing ongoing progress in cost control, digital innovation, and customer experience. Kroger trades at 19x earnings.

Chewy reported continued strength in pet spending, with Autoship sales up 15% y/y and now making up 83% of total revenue. Active customers grew 4.5% to 21 million, while net sales per active customer rose 4.6% to $591, underscoring both loyalty and higher wallet share. The results reinforce a key theme in consumer spending: pet care remains defensive and non-discretionary, even in periods of wallet tightening. Despite good results, the stock fell -15% the next day as results did not meet their optimistic expectations. Chewy trades at 97x earnings.

The design software giant, Adobe, reported earnings on Thursday. Worries about AI risk have put pressure on the shares, which are -20% YTD. However, earnings told a different story. Adobe grew revenues +11% y/y to $6bn, while raising its guidance in the process. Strong growth was driven by AI-powered offerings, with AI-influenced ARR surpassing $5 billion and new AI-first product ARR already exceeding its year-end target. Digital Media segment revenue reached ~$4.5 billion, while Digital Experience segment revenue hit ~$1.5 billion, both posting double-digit increases. Adobe’s remaining performance obligations (RPO) rose to $20.4 billion, up +13% y/y, and the company continued aggressive share repurchases during the quarter by buying back $3.5bn worth of its own shares. Adobe trades at 22x earnings with a $150bn market cap.

At the latest Goldman Sachs conference, Intuit’s CFO gave more color on small business health and Intuit’s plan to move mid-market. Despite flat revenues from small businesses, small business profitability is up as efficiency improves. Key leading indicators such as cash reserves and employee hours have increased y/y, suggesting resilience amid macro challenges like tariffs. Intuit is also trying to move upmarket to serve customers with $2mn to $100mn in revenue. They already have 800k using QuickBooks. While the cost to acquire these mid-market customers is higher, CFO Sandeep Aujla believes they have a higher lifetime value.

Paramount Skydance, fresh off its $8.4bn Paramount Global acquisition, is reportedly preparing an all-cash-backed bid for Warner Bros Discovery with support from the Ellison family, a move that could unite iconic franchises like DC Comics, Star Trek, SpongeBob, and The Matrix alongside HBO, CNN, and Paramount+ under one roof. WBD shares jumped 30% and Paramount 15% on the news, though any deal—valued at $30bn+ with WBD’s debt—would face significant antitrust scrutiny. If successful, the merger would create a formidable streaming rival to Netflix, Disney, and Amazon. Paramount Skydance carries a market value of $11.5bn.

If you enjoyed this summary, please drop a comment or like so we know to keep doing it in the future! Feedback is always welcomed.

Spotlight.

This week, we released a 4Q25 business recap on Copart!

This is in addition to the 12 other 2Q25 business updates. We have released business updates on Meta, APi Group, Floor & Decor, AppFolio, Coupang, Axon, Airbnb, Evolution, CoStar Group, Perimeter Solutions, Constellation Software, and DFH.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

CPRT 2Q25 Business Recap.

CPRT M&A Approach: “We have a two-pronged approach to any M&A activity. One is the investments. On a stand-alone basis, it’s self-compelling, meaning if John, Leah and I — you and Leah and I were sitting here in the room, would we be willing to write our own personal checks in support of a given investment if we were to hold it as a private company? And then the second question is does it enhance fundamentally what Copart is and what we do, right, and/or can we enhance what they do by virtue of Copart’s capabilities.”

Read the full update here: CPRT 2Q25 Business Recap

PRM 2Q25 Business Update.

CEO Haitham Khouri on how IMS can be a model for future acquisitions:

Read the full update here: PRM 2Q25 Business Update

The Synopsis Podcast.

This week, we released a dialogue episode covering Perimeter’s, CSU’s, and Copart’s latest earnings. In addition, we break down Nvidia’s GPU risk and give a brief history of the Fed cutting rates in an inflationary environment. Listen below!

Memo of The Week.

How an Investor Can Evaluate Managers: The Gary Friedman Playbook

RH was weeks away from bankruptcy when Gary Friedman took over in 2001. Two decades later, Friedman grew sales 40x and grew RH into a $4bn company. In this memo, we break down 10 timeless business lessons from Gary Friedman, pulling from our research report on RH.

Read the full memo here: How an Investor Can Evaluate Managers: The Gary Friedman Playbook

Company Report Snippet: Evolution

The Black Box of Asia: “Evolution’s business is different in most of Asia than Europe though, because they use aggregators. An aggregator signs contracts and integrates with dozens of different casino suppliers so they can offer operators a single integration to receive everything. In turn, they help suppliers by signing up the tailend of small operators. This also has the byproduct of giving Evolution distance from what may be unscrupulous business practices of certain operators (many Philippines operations target the China market where gambling is illegal), but it also means by losing the direct customer relationship they become more commoditized, which tends to show up in lower GGR commissions. Asia is a bit of a black box for these reasons.”

*This is an excerpt from our company report on Evolution.

If you are a Speedwell Research Member, read the full report here: Evolution

If you are not already a Speedwell Research member, you can purchase it here: Evolution Individual Report

Upcoming.

Research

Current research report in progress: Exploratory Report on Casey’s, a convenience store and gas station chain that also happens to be the 5th largest pizza retailer in the country.

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Seung-gun Lee, Founder of Viva Republica (Korean fintech app Toss) (link)

Chuck Akre: The Oracle of Middlebury, Virginia (link)

Leandro (Best Anchor Stocks): The Hidden Costs That Hinder Long-Term Returns (link)

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).