The Investor's Briefing #3

Mixed Inflation Reading Ignored, Sea Limited Shows Growth and Profits, Cava Slows, Apple Scrambles in AI

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed.

Welcome to the third edition of our new weekly newsletter: The Investor’s Briefing.

In Financial News.

Financial markets ended the week higher, with the Dow leading the way, up +1.7% for the week. The Dow Jones hit its first intraday record high since December at 45,169, fueled by UnitedHealth’s 12% jump following news that Berkshire Hathaway bought a $1.6bn stake. The S&P 500 rose +0.9%, bringing YTD gains to 9.9% as strong corporate earnings and a benign inflation reading fed investor’s exuberance.

This week Consumer Price Index (CPI) figures were released for July. The reading showed that inflation remained relatively steady, with headline CPI increasing +2.7% y/y. This report was better than expectations, as economist thought the tariffs would start to impact these numbers. Adding fuel to the rally was Treasury Secretary Scott Bessent’s remarks that “we could go into a series of rate cuts here, starting with a 50 basis-point rate cut in September.” However, the July Producers Price Index (PPI) told a different story. That came in hotter than expected at 3.3% anually vs expecations of 2.5%. Despite this mixed reading, the probability of a 25bps cut in September currently sits at over 90%.

Rate expecations and recent weak jobs numbers put pressure on Treasury yields, which in turn pressured mortgage rates to 4-month lows, spurring a surge in refinancing activity. According to the Mortgage Bankers Association, they reported a +23% jump in refinance applications from the prior week. Refinancing applications rose to 46.5% of total mortgage applications, up 5 points from last week. The average rate for a 30-year fixed loan is now around ~6.6%, the lowest since October 2024.

The fear-index, other known as the VIX, slumped to its lowest level in 2025 at ~14.5. To put this in perspective, the VIX hit a high of 52 in early April, when stock indices fell sharply over fears of new U.S. tariff measures. With continued upward momentum in U.S. equity indices, positive corporate earnings in the second quarter, and hopes of lower rates in the Fall, investors are pricing in less volatility—or arguably getting complacent.

U.S. consumer sentiment fell for the first time in four months, with the University of Michigan’s preliminary index falling to 58.6 from 61.7 in July. The drop is largely attributed to heightened concerns about inflation, with consumer’s expecting year-ahead inflation of 4.9% versus 4.5% prior. Long-term inflation expecations also increased by a similar amount to 3.9%.

This is problematic because as Paul Volcker would argue, inflation can become a self-fulfilling prophecy. As people expect prices to rise, they start to demand larger pay increases and businesses start to price goods expecting larger labor costs. A weak labor market hurts workers’ negotiating power, which can help take the pressure off of inflation. But then that becomes it’s own issue because then there are calls for the Fed to lower rates, which will increase economic activity and thus improve the labor market.

The survey also found that buying conditions for durable goods fell 14% to their lowest reading in a year, reflecting anxiety about high prices. Consumers continue to expect both inflation and unemployment to worsen moving forward. This could land us with the worst of both worlds with stagflation. That makes the Fed pick between keeping interest rates high to stave off inflation, but causing a recession—or keeping the economy humming, but risking inflation taking off. When Paul Volcker was faced with this decision, he chose a recession, knowing that if inflation ever got bad enough it could wreck an entire country. (In the 70s, inflation exceeded 12% annually).

Crude oil fell 1.4% to $63 as the U.S. Energy Information Administration (EIA) raised its forecast for the 2025 global oil surplus to 1.7mn barrels per day from 1.1mn barrels per day. In addition, with the possibility of progress at the Trump-Putin summit in Alaska, oil markets are anticipating that the talks could lead to a relaxation in Russian oil sanctions, which could lead to an increase in global oil supply.

On the policy front, President Trump extended the China tariff pause for another 90 days, pushing trade negotiations out to November. The pause keeps U.S. tariffs on Chinese goods at 30%, while Chinese tariffs on U.S. goods remain at 10%.

In addition, Nvidia and AMD reached an agreement with the U.S. government under which they will pay 15% of their revenues from chip sales to China in exchange for export licenses. Originally, sales of advanced AI chips to China were banned to prevent potential military and artificial intelligence advancements that could threaten U.S. interests. However, some proponents point out that it is better for America to have China reliant on U.S. made chips than have them develop their own, even if it does take them many years. While the legality of this deal is a little murky as it has a private business paying a fee to the U.S. governement, it looks like it will reopen the Chinese markets to Nvidia and AMD. Treasury Secretary Scott Bessent said that this deal could serve as a model for future negotiations.

Company News.

Amazon rose +4% on news that they were expanding same-day grocery delivery to 1,000 cities, with plans to reach more than 2,300 locations by the end of the year. This move is a bid to compete with rivals like Instacart and Walmart+, who have been making strides in same-day grocery delivery. The service is free for Prime Members. After a trial, Amazon says the services has increased purchase frequency and Prime loyalty.

Webvan was a dot com era start-up that tried to do just this, but went bankrupt. While many people ridiculed the idea at the time as being unfeasible, Amazon is now able to do this at scale today.

Apple is reportedly making a push into robotics as part of its new AI strategy.

They are actively working on a smart home tablet with a robotic arm that utilizes advanced AI, expressive movement, and next-gen Siri integration. A potential 2027 date for release was leaked. It is also reported that they are working on another AI home tablet as well as a Ring-like security system. This is in addition to an updated Siri LLM and new animations for how to engage with Siri.

Gildan has agreed to acquire HanesBrands for $2.2bn.

This deal will create a global leader in basic apparel, combining Gildan’s position in activewear, underwear, and socks with HanesBrands' lines. The deal is structured with 87% paid in Gildan stock and 13% in cash. Gildan has a $8bn market cap and currently trades at 17x.

Cava dropped -20% on an earnings miss and guidance cut. Cava reported 2Q25 revenue up +20% with same-store sales up +2%. This +2% same-store sales growth was much less the mid to high single digit growth investors were expecting. They ended the quarter with 398 restaurants in total, leaving this Mediterranean Chipotle copycat only about 10% on their way to mirroring Chipotle’s footprint.

Cava, like many fast-casual chains (Starbucks, Shake Shack, and Chipotle), is having a challenging 2025 so far. There are 2 main reasons why: 1) Lower-middle income diners are tightening budgets with inflation and layoff fears top of mind, 2) Rising costs in labor, food, and overhead have climbed steadily in the year, pushing many restaurants to increase prices despite knowing they could lose out on price-sensitive customers.

Target and Ulta Beauty have announced they will end their shop-in-shop partnership in August 2026, concluding a retail experiment that began in 2021 and eventually grew to more than 600 Ulta mini-beauty shops within Target stores.

Target will continue to curate its beauty assortment, launching new brands and exclusive collaborations, while Ulta plans to bolster its omnichannel presence with the upcoming Ulta Beauty Marketplace. The breakup comes amid merchandising changes and leadership transitions at both retailers, including a new CEO at Ulta

Perplexity AI has bid $34.5bn to acquire Alphabet’s Google Chrome browser. The offer comes amid antitrust litigation, where a judge is weighing a proposal that could require Google to divest Chrome. Alphabet has not responded to the bid.

AAON reported 2Q25 results that missed expectations due to ERP implementation and supply chain disruptions. Total revenues were down -0.6% y/y and net income was 70% lower than last year. Their BASX segment drove growth, especially in the data center markets.

Sea Limited shares soared over 21% after reporting strong 2Q25 with revenue jumping +38% y/y. Operating margins reach 9%, a step-function improvement y/y from when they were barely profitable. GMV was +28% y/y, putting them at $112bn in GMV LTM.

SEA started as a video game distributor that leveraged an early Tencent partnership into eventually a fintech and ecommerce arm. Shopee, their ecommece site, was founded in 2015 and despite entering into a market that was riddled with better funded competition, they have taken a clear lead. More impressive though is their ability to do continue to do so while showing strong profit growth. The stock dropped 90% from Covid peaks, to a market cap of just $20bn. Today they sport a market cap of $105bn and trade at about 5x sales or 88x earnings.

Applied Materials shares fell 14% after reporting 3Q25 results. Despite beating expectations, they issued weaker-than-expected Q4 guidance due to weak demand from China. China accounts for 35% of AMAT’s sales, so when AMAT cited a pause in demand from Chinese customers with high inventory levels, investors started to price in a slow down.

United Healthcare rose +10% on Friday after Warren Buffett’s Berkshire Hathaway disclosed a $1.6bn stake in the health giant in their 13F filing. This, however, is a small percentage of the Berkshire portfolio at just 0.6%.

Intel shares saw a 7% bump after reports that the Trump administration is considering a stake in the company. Reports suggest the government may use funds from the CHIPS Act to partially finance the investment. This law, originally signed in 2022, was designed to support domestic semiconductor production and alleviate chip shortages.

Beyond Meat is currently facing severe financial challenges, including a 20% year-over-year decline in quarterly revenue, mounting debt of about $1.2bn, and weakening demand in the U.S. plant-based meat market. These struggles have led to layoffs (about 6% of its global workforce), suspension of operations in China, and efforts to restructure costs and management. They were rumored to be entering Chapter 11 bankruptcy this week before they denied that. Today they are valued at just $200mn, down from over $18bn at peak.

Monday.com, the cloud-based work operating system, shares dropped -20% after reporting 2Q25 earnings. Monday.com issued conservative guidance for the remainder of the year, indicating slowing growth and operating margin pressure.

AI adoption accelerated, with 46mn AI-driven actions since launch and new products (Monday Magic, Vibe, Sidekick) introduced; initial monetization of AI features began in Q1, with expectations for increased AI-related revenue in 2026.

Paramount acquired UFC rights for $7.7bn for 7 years, sending Paramount shares up +37%. Beginning next year, every UFC numbered event and Fight Night—previously available primarily through pay-per-view—will be available at no additional charge to Paramount+ subscribers. Shares in TKO Group (UFC’s parent company) rose +16% as a result.

We are experimenting with new content formats, so if you enjoyed this summary, please drop a comment or like so we know to keep doing it in the future! Feedback welcomed.

Spotlight.

This week, we released 2 business updates on Axon and Airbnb.

This is in addition to the 7 other 2Q25 business updates we shared so far this earnings season. We have released business updates on Meta, Api Group, Floor & Decor, AppFolio, Coupang, CoStar Group, and DFH.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

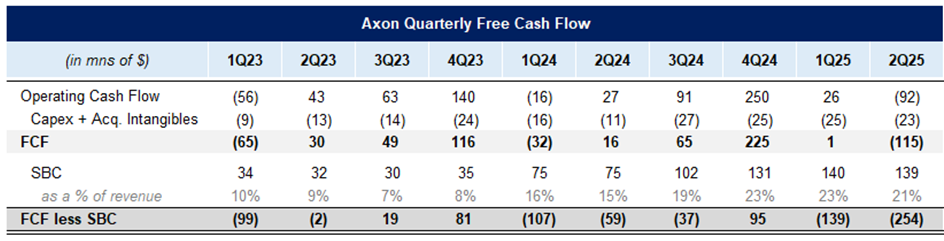

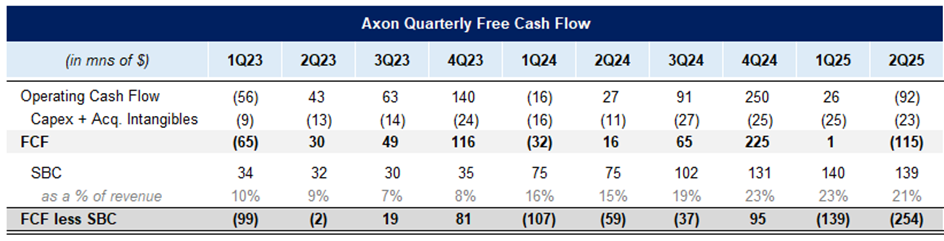

AXON 2Q25 Business Update.

Axon Free Cash Flow Conversion: “However, revenues have not been translating into cash flows. The nature of recording most revenues from a contract upfront and receiving cash for it over the term, plus ample stock comp has meant tepid free cash flow. After backing out SBC, they burned $250mn this quarter. Investors aren’t complaining though given the growth figures they are putting up.”

Read the full update here: Axon 2Q25 Business Update

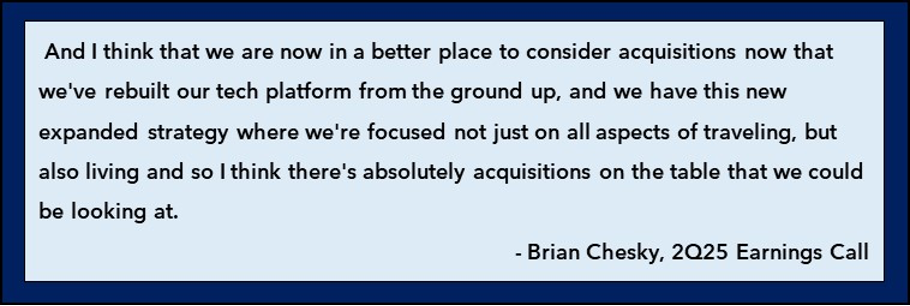

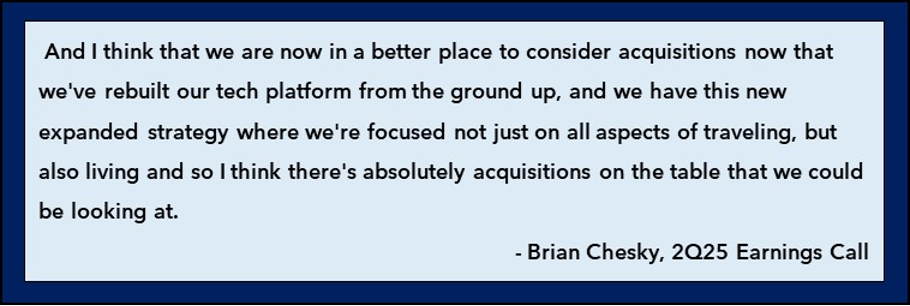

ABNB 2Q25 Business Update.

ABNB M&A?: “We could see more free cash flow directed to acquisitions in the future though. After their tech platform rebuild, it makes it easier for them to launch new businesses and potentially acquire business as well. They indicated that M&A could be used to accelerate growth in complementary areas that fit their expanded vision for Airbnb.”

Read the full update here: ABNB 2Q25 Business Recap

The Synopsis Podcast.

In case you missed it, we released a dialogue episode discussing our new business updates on Floor & Decor and Meta. We expand on calculating the ROIC for AI spend for Meta as well as FND’s new mature store unit economics. Listen below!

Memo of The Week.

Balancing Risk and Return: The Simple Statistics of Investing

Higher risk doesn’t guarantee higher returns; it widens the range of possible outcomes, both good and bad. Skilled investors, like Buffett, seek situations with strong probabilities of acceptable returns and minimal chances of loss. A Reverse DCF helps quantify this by linking different operating scenarios to expected returns, revealing whether even pessimistic cases clear the risk-free rate. The goal is to find investments where the downside is remote and the upside remains compelling.

Read the full memo here: Balancing Risk and Return: The Simple Statistics of Investing

Company Report Snippet: Axon

The Essential Need for Safety Technology: “Public spending on safety has tended to only go up over time, with a few occasional setbacks whether from recessions or political movements. However, even if there was a focus to cut back on police budgets, it would be rational to rely more on technology to replace some personnel.”

*This is an excerpt from our company report on Axon.

If you are a Speedwell Research Member, read the full report here: Axon

If you are not already a Speedwell Research member, you can purchase it here: Axon Individual Report

Upcoming.

Research

Current report in progress: LVMH

Coverage

We will be sharing updates on PRM and CSU for 2Q25 earnings.

For our latest updates on these names, click here → Business Updates

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Norges Bank Investment Management Portfolio Manager Stephanie Vardheim on the Life of a Portfolio Manager (link)

LiLu on “Global Value Investing in Our Era” (link)

Howard Marks’s new memo: The Calculus of Value (link)

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).