The Investor's Briefing #4

Jackson Hole Comments, Canada Relationship Reset, Home Depot Growing, Meta Hiring Freeze

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed.

Welcome to the fourth edition of our new weekly newsletter: The Investor’s Briefing.

In Financial News.

Financial markets ended the week mixed, with the Dow Jones gaining +1.7%, while the Nasdaq slipped -0.5% as investors rotated out of high-valuation tech names and into more defensive sectors. The S&P 500 broke a five-day losing streak on Friday, boosted by a dovish signal from Fed Chair Jerome Powell at Jackson Hole. His remarks shifted sentiment and sparked a late-week rally in equities.

Earlier in the week, the Federal Reserve released its July 29–30 meeting minutes, which struck a notably hawkish tone, dampening market expectations for a rate cut in September. The minutes reflected policymakers’ strong concern about persistent inflation risks, especially due to the impact of tariffs. Most FOMC members saw the risk of inflation as greater than risks to employment, and chose to keep rates steady at 4.25%–4.5% despite calls from President Trump and some committee members to cut.

“Participants assessed that the effects of higher tariffs had become more apparent in the prices of some goods but that their overall effects on economic activity and inflation remained to be seen. They also noted that it would take time to have more clarity on the magnitude and persistence of higher tariffs' effects on inflation.” - July Fed Minutes

But on Friday, attention turned to Jackson Hole for a fresher Fed opinion. Powell signaled a cautious openness to future rate cuts, noting a high level of uncertainty makes policymaking difficult. He stopped short of committing to action but implied the Fed might adjust its policy stance as risks shift between full employment and price stability. With the U.S. labor market remaining strong and the economy resilient, Powell warned that downside risks are increasing. He highlighted concerns that tariffs could reignite inflation, raising the risk of stagflation, a scenario that he wants to avoid.

With rates a full percentage point lower than a year ago and unemployment still low, Powell said the current "restrictive policy” gives the Fed room to "proceed carefully." He acknowledged that the baseline outlook and shifting risks could "warrant adjusting our policy stance," pointing to a possible rate cut at the next Fed meeting in September. Markets reacted immediately to Powell’s remarks with the Dow increasing more than 600 points, while the 2-year Treasury yield fell 11bps to 3.69%.

“With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.” - Fed Chair Jerome Powell

New labor market data supports a less restrictive policy. U.S. labor market concerns are deepening as jobless claims have jumped in the latest jobs report. For the week ending August 16, 2025, initial claims for unemployment benefits rose by 11,000 to 235,000, reaching the highest level since June and exceeding economists’ forecasts of 225,000. The four-week moving average of initial claims also climbed to 226,250, indicating persistent upward pressure. Meanwhile, continuing jobless claims (which reflect ongoing unemployment) rose by 30,000 to 1.97mn, the highest since November 2021, signaling an uptick in the number of people remaining out of work for extended periods.

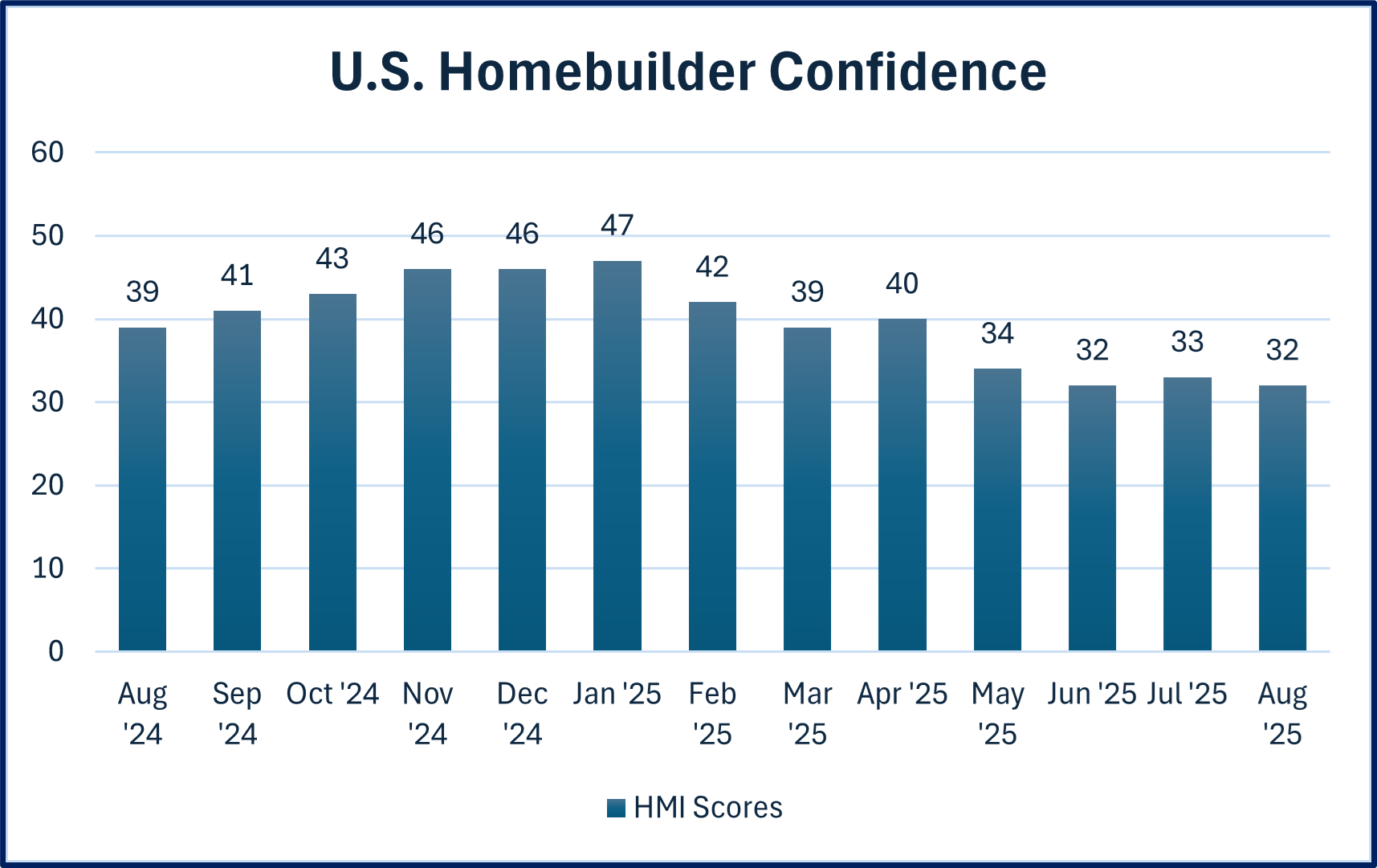

While the labor market shows mounting stress, weakness is also evident in housing, where builder sentiment has deteriorated further. Homebuilder confidence has recently matched its lowest level since December 2022, with the NAHB/Wells Fargo Housing Market Index (HMI) falling to 32 in August 2025. This marks the 16th straight month the index has remained below the optimistic threshold of 50, indicating persistently negative sentiment among builders. In August, 37% of builders reported price cuts averaging 5%, a figure that has stayed consistent in recent months. Meanwhile, 66% of builders offered sales incentives, the highest in the post-COVID era. Regionally, confidence is weakest in the West and South, where affordability pressures are most acute, and higher-cost markets are seeing the deepest buyer hesitancy.

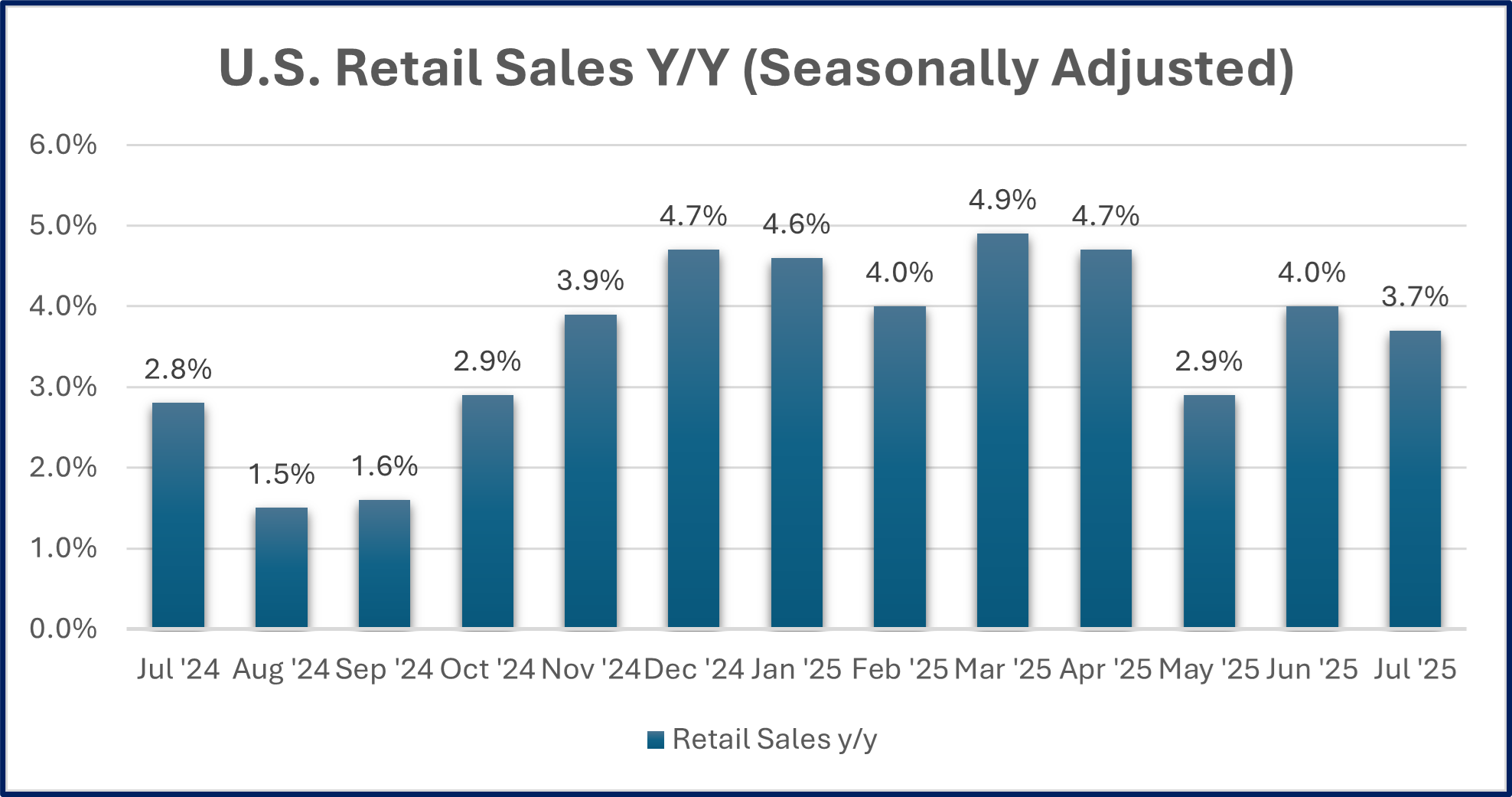

In other news, July retail sales increased +3.7% y/y driven by Amazon Prime Day deals, early back-to-school shopping, and July 4th spending. Year-over-year growth has strengthened compared to the same month last year; July 2024 was +2.8% y/y. Despite the positive growth, volume growth was just +1.4% y/y with $6.2bn attributed to pull-forward spending, signalling that consumers remain cautious and value-driven. Furniture and apparel were the top gainers for the month, with sales rising +6% and +7% respectively. Entertainment, however, lagged behind with theaters and music venues reporting a -6% y/y drop in foot traffic.

Canada announced it will remove about half of its retaliatory 25% tariffs on U.S. goods, effective September 1, marking a significant step forward in bilateral trade relations. The rollback applies to roughly $21 billion of U.S. exports, including consumer goods such as orange juice, appliances, and motorcycles, provided they comply with the USMCA framework. However, tariffs on steel, aluminum, and automobiles will remain in place given their strategic importance and unresolved disputes. The decision followed a call between Prime Minister Mark Carney and President Donald Trump aimed at resetting negotiations after missed trade deadlines. The White House welcomed the move as “long overdue,” and both sides signaled readiness to continue talks. Importantly, this easing of tensions comes ahead of the planned 2026 USMCA review, positioning it as a goodwill gesture and an effort to build momentum toward resolving outstanding trade frictions.

Company News.

Intel shares were up +6% for the week after SoftBank announced a $2 bn investment in the company, and President Trump announced that Intel has agreed to a 10% government stake in the business valued at $10bn.

Home Depot reported earnings, with shares rising more than 3% after it reported a 1% increase in comp sales.

They noted that homeowners are prioritizing smaller, more manageable home improvement tasks over large-scale renovations in areas such as gardening, painting, and lighting.

Big-ticket projects continue to soften, but they noted that consumers are deferring these purchases rather than canceling altogether. Despite weak activity in large discretionary projects, transactions over $1,000 grew by 2.6% y/y, indicating some resilience in the upper segment of home improvement spending. CEO Ted Decker stated that “The No. 1 reason for deferring the large project is general economic uncertainty.”

They reaffirmed their guidance with total sales growing ~2.8% and comp sales growth of ~1%.

Thoma Bravo has agreed to acquire HR software firm Dayforce (formerly Ceridian) in a definitive all-cash transaction valued at $12.3 billion, including debt

Dayforce shareholders will receive $70 per share in cash, representing a 32% premium to its unaffected share price as of August 15, 2025.

The deal is expected to close in early 2026, pending regulatory and shareholder approvals.

Palo Alto Networks shares were up +3% after reporting strong quarterly results, surpassing a $10bn revenue run rate, with 4Q revenue of $2.54 bn (up 16% y/y), product revenue up 19%, and services revenue up 15%; next generation security ARR reached $5.58 billion, up 32% y/y. Palo Alto Networks currently trades at 116x earnings

Toll Brothers reported earnings this week with revenues of $2.9bn. They delivered 2,959 homes at an average price of $974,000. They are guiding to deliver 11,200 homes by year-end.

Toll Brothers CEO on the resilience of the luxury home market: "We are pleased to report another strong quarter...While affordability pressures and uncertain economic conditions persist, we are pleased with the resilience of our luxury business and more affluent customer base.”

Lowes reported earnings with sales reaching $24bn and a +1.1% increase in same-store comp sales.

They also announced the $8.8bn acquisition of Foundation Building Materials (FBM). Along with their recent ADG acquisition, Lowes is trying to create a comprehensive interior solutions platform for large pro customers, offering products and services from drywall to flooring.

Management noted on the call that they will be pausing share repurchases until 2027 to delever following the FBM acquisition.

Estee Lauder shares fell -3.7% following the company’s announcement of a third straight quarter of double-digit declines in revenue and profits. They also announced the approval of 3,200 layoffs, citing ongoing U.S. and China headwinds and a $100mn hit from tariffs.

Target shares fell -6% after they reported weak earnings and reaffirmed a soft outlook

Q2 results showed sequential improvement: Comparable sales declined -2% (better than Q1), with digital comp sales up +4% and same-day delivery via Target Circle 360 up over +25%.

Tariffs and inventory costs pressured margins, but most one-time impacts are behind them now.

They announced that COO Michael Fidelk will become the new Target CEO at the start of 2026.

Analog Devices shares popped +6% on Wednesday after reporting earnings with quarterly revenue up +25% y/y.

Industrial segment (45% of revenue) grew +23% y/y

The automation and robotics business is expected to double by 2030, driven by new sensing modalities, AI, and partnerships with Teradyne and Nvidia

ADI trades at 64x earnings

Meta has recently implemented a hiring freeze for its AI division, following an aggressive recruitment spree earlier this summer. The freeze is part of a restructuring after hiring over 50 leading AI researchers and engineers, many lured from competitors like OpenAI, Anthropic, and Google with lucrative compensation packages.

Meta also made a 6-year cloud deal with Google, valued at over $10bn. Meta plans on using Google Cloud’s servers and storage to expand its AI capabilities.

Nvidia announced they are halting its China-focused H20 AI chips following directives and security concerns raised by Chinese authorities. Just as it appeared that Nvidia was back in China, the halt has deepened uncertainty in Nvidia’s China business.

CEO Jensen Huang expressed his surprise at Beijing’s abrupt security queries, as Nvidia had worked to secure licenses for the H20 chip and cooperate with Chinese regulators. Jensen Huang confirmed that Nvidia is in talks with the U.S. administration about developing a potential new, more powerful AI chip (the B30A) for China.

We are experimenting with new content formats, so if you enjoyed this summary, please drop a comment or like so we know to keep doing it in the future! Feedback welcomed.

Spotlight.

So far this earnings season, we have released 9 2Q25 business updates. We have released business updates on Meta, Api Group, Floor & Decor, AppFolio, Coupang, Axon, Airbnb, CoStar Group, and DFH.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

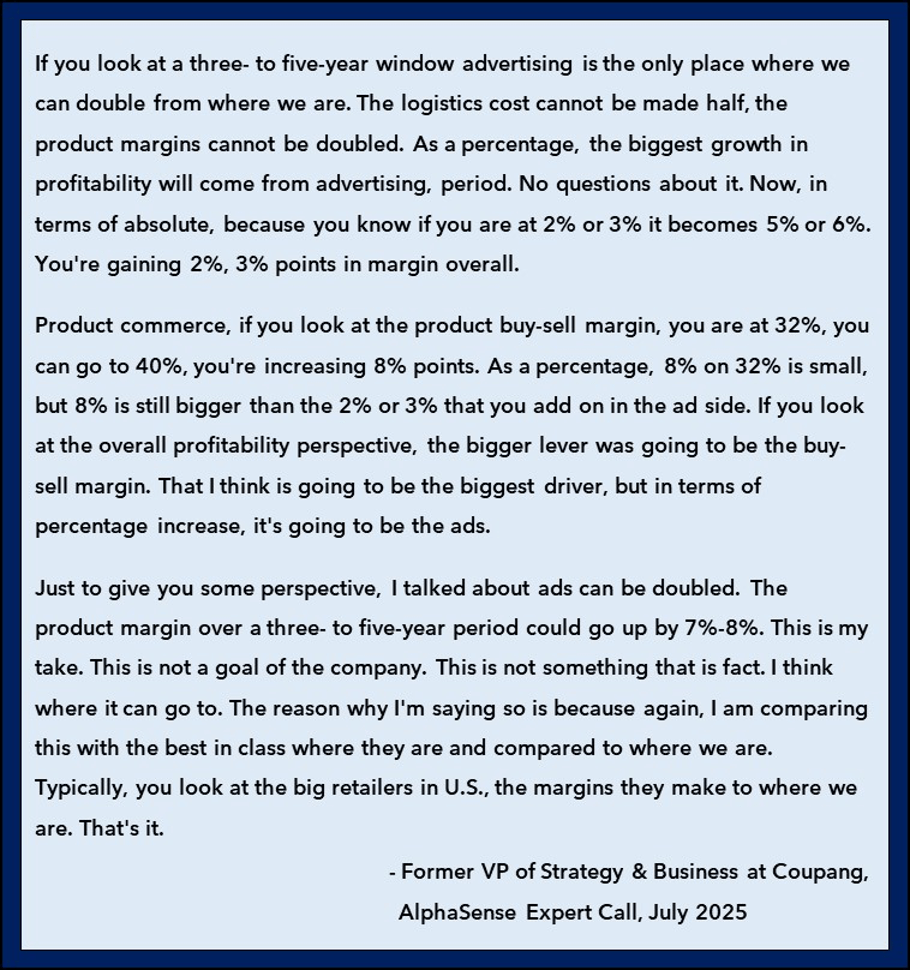

Coupang 2Q25 Business Update.

Former VP at Coupang on Margin Expansion: “In the interview he talked about how he had analyzed many retailers and believes that they should be able to get closer to 40% gross margins as they increase in scale and improve product procurement.”

Read the full update here: Coupang 2Q25 Business Update

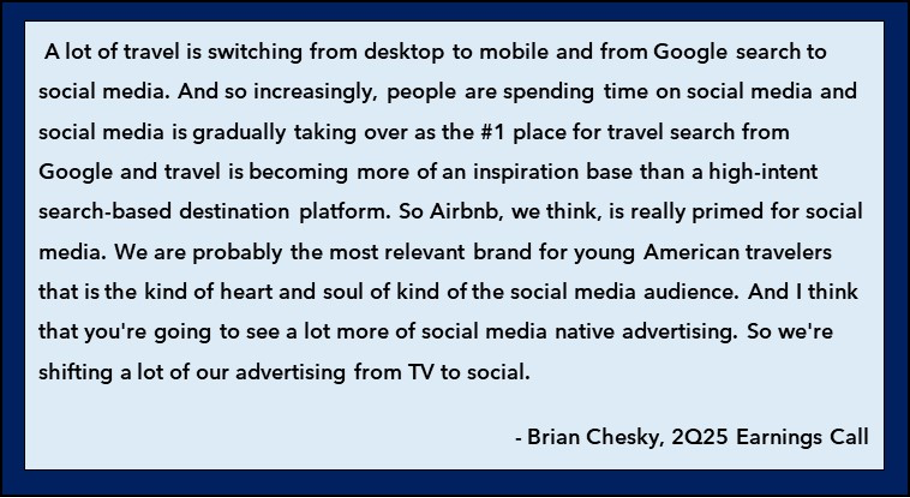

Airbnb 2Q25 Business Update.

ABNB Shifting Ad Spend to Social: “To help increase awareness they are turning to more marketing. They noted that this advertising will help not just services, but their core Airbnb Stays business as well. They also are now leaning more into social media as they observed consumer behavior has changed.”

Read the full update here: ABNB 2Q25 Business Update

The Synopsis Podcast.

This week, we released an interview episode with Ramneek Kundra, who manages over $600mn at DSP Pension Funds. We talk about his investment philosophy, how he constructs his portfolio using the core and explorer framework, and investing in the Indian stock market. Listen below!

Memo of The Week.

Priced to Outperform Perfection: The Home Depot Circa 1999

Buy a Great Company at Any Price?

“The idea that you can buy a great company to hold forever and the price doesn’t matter has seemed to gain some traction. Consider this: the difference between buying Home Depot when it was at 50x earnings at the end of 1999 versus buying it at the end of 2003 at 20x was the difference between a 9% return and a 13% return. While a 9% return before dividends isn’t bad, this line of thinking is missing a key point… Which purchase was less risky?”

Read the full memo here: Priced to Outperform Perfection: Home Depot Circa 1999

Company Report Snippet: Constellation Software

The Moat of Vertical Market Software: “In order for a new entrant to take an existing VMS business, you have to convince their customers that your solution is many-folds better than what they are currently using and that it is worth risking potentially secluding their customer and losing sales, as well as all the headaches that come with removing a foundational building block of a company’s systems that was relied on for decades, which include potentially working to re-integrate other software and retraining your entire employee base.”

*This is an excerpt from our company report on Constellation Software.

If you are a Speedwell Research Member, read the full report here: Constellation Software

If you are not already a Speedwell Research member, you can purchase it here: Constellation Software Individual Report

Upcoming.

Research

Current report in progress: LVMH

Coverage

We will be sharing updates on PRM and CSU for 2Q25 earnings.

For our latest updates on these names, click here → Business Updates

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Founder & Chairman of Mirae Asset Management Hyeon-Joo Park (link)

Nick Sleep’s interview on investing in Costco (2005) (link)

Stanley Druckenmiller Lost Tree Club Interview (2015) (link)

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).