The Investor's Briefing #5

Tariffs Struck Down (again), Fed Independence Threatened, Nvidia's Record $60bn Buyback

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the fifth edition of our new weekly newsletter: The Investor’s Briefing.

In Financial News.

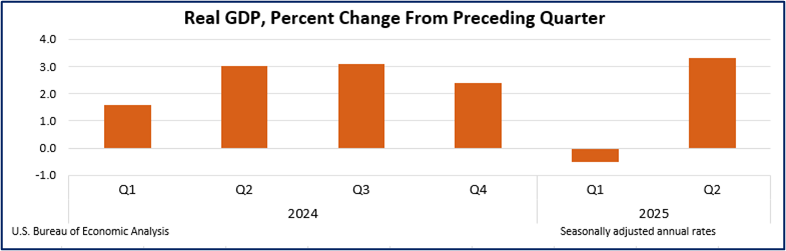

AI enthusiasm and stronger-than-expected GDP revisions drove the S&P 500 to surpass 6,500 for the first time ever. However, Friday’s negative inflation data— core PCE, or personal consumption expenditures, inflation rose +2.9% y/y in July, the highest since February— setting the market back to finish the week essentially unchanged after major indices set fresh record highs on Thursday.

On Thursday, Q2 GDP growth was revised up to +3.3%, an increase from the initial figure of +3.0%. The revision was mainly driven by stronger consumer spending, private investment in AI, and a sharp -30% drop in imports. Currently, the Atlanta Fed now forecasts Q3 GDP to be +3.5%.

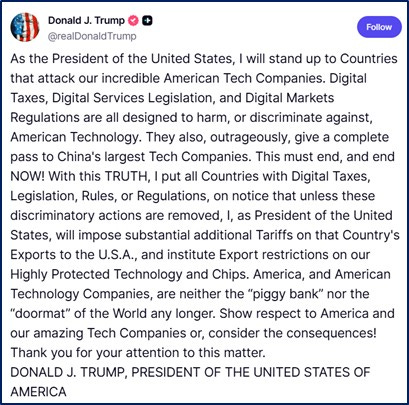

Early this week, President Trump threatened to implement additional tariffs and impose restrictions on technology exports to countries that adopt digital taxes. He stated that these digital tax measures disproportionately affect American technology companies such as Apple, Alphabet, Amazon, and Meta. According to Trump, such policies create an uneven playing field for U.S. firms while providing advantages to some foreign competitors. He indicated that, unless these digital taxes are rescinded, affected countries may face increased tariffs on exports to the United States and limitations on access to U.S. technology and chips.

In other tariff news, the U.S. President has imposed new tariffs that double duties on Indian imports to a total of 50%, primarily as retaliation for India’s continued purchase of Russian oil despite U.S. objections. The new duties target a wide range of Indian exports such as jewelry, textiles, furniture, seafood, and industrial chemicals. The move complicates U.S. companies’ supply chain strategies, as many have recently increased operations in India to reduce dependence on Chinese manufacturing.

The United States ended the “de minimis” exemption on Friday. Imports (including e-commerce products) valued at $800 or less are no longer duty-free and must now pay applicable tariffs and undergo stricter customs checks. This policy change affects all countries and follows an earlier suspension of the exemption for shipments from China and Hong Kong. For the next six months, postal service carriers like FedEx and UPS may pay a flat fee of $80–$200 per package (depending on the country of origin) during a transition phase before all shipments move to standard duty rates. The de minimus exemption was especially important to companies like Temu and Shein who previously relied on the de minimis rule to offer lower prices, which helped them outcompete U.S. retailers who had to pay duties on bulk imports. This move is expected to increase prices, reduce product variety, and create shipping delays as businesses and consumers adapt to the new rules.

Turning to monetary policy, President Trump fired Federal Reserve Governor Lisa Cook on allegations of mortgage fraud, though Cook strongly denies wrongdoing and is suing to challenge her removal. The unprecedented move comes as his administration seeks greater control over the Fed, including the potential to fill multiple board seats with allies, prompting concerns from economists and investors over threats to central bank autonomy. After a hearing Friday there wasn’t a decision yet on whether to temporarily block Cook’s firing while the case is heard.

The importance of the Fed’s independence is best exemplified by President Nixon pressuring then Fed Chairman Arthur Burns to lower interest rates ahead of the 1972 election. This was done in hopes of boosting economic growth in the short-term for political gain. The following year after the Fed lowered interest rates, inflation jumped to 6% y/y and only continued to increase from there. While no historical comparison is perfect, an independent Fed is more likely to inflict short-term economic pain in order to achieve long-term money stability—which is precisely why politicans have sought to influence the institution.

In an interview on Thursday, Federal Reserve Governor Waller publicly advocated for a 25bps rate cut at September’s meeting, citing risks to the labor market. He argues that while the labor market remains resilient on the surface, there are signs of underlying softness that could quickly deteriorate if not addressed preemptively. The probability of a 25bps cut currently stands at 87%.

“While there are signs of a weakening labor market, I worry that conditions could deteriorate further and quite rapidly, and I think it is important that the FOMC not wait until such a deterioration is under way and risk falling behind the curve in setting appropriate monetary policy.” - Federal Reserve Governor Christopher Waller

However, with inflation still above the 2% long-term target, there is still an arguement to be had to keep rates steady. Cutting prior to inflation falling, risks inflation taking a hold again and reaccelerating. On the other hand, cutting too late could mean causing a potential recession. This is a very hard balance to walk—one that only is trickier when political considerations are thrown in the mix.

Lastly, late Friday a federal appeals court struck down the Trump administration’s signature tariff’s in a 7-4 ruling. They found that the President had overstepped his authority in use of emergency powers to reshape U.S. trade policy. However, tariffs will remain in effect through mid-October as the case is set to go to the Supreme Court.

Company News.

Nvidia topped expectations for both earnings and revenue in 2Q and announced a $60 billion buyback, but its shares slipped post-earnings as ongoing uncertainty over China sales overshadowed the results. While the company’s data center revenue surged +56% y/y, Nvidia reported no H20 chip sales to China for the quarter and said its upcoming guidance also excludes any China-related H20 revenue, fueling concerns about future growth despite record results.

Nvidia CEO Jensen Huang on AI Infrastructure: “AI has made remarkable advancements over the past year, emphasizing that the development of AI infrastructure is still in its nascent stages.”

Whether Nvidia should be allowed to sell chips to China has been a sticking point for the Biden and Trump administrations who have tried to find the best strategy of keeping the United State’s lead in AI chips and semiconductor technology, while not encouraging China to develop their own semiconductor ecosystem that is not reliant on U.S. Technology.

MongoDB shares were up over +50% this week after the company reported strong fiscal 2Q results, with revenue rising +24% y/y to $591mn. Atlas, the company’s cloud database platform, grew +29% y/y and now represents ~74% of total revenue. They added 2,800 new customers in the quarter, bringing their total customer count to ~60,000.

CrowdStrike shares slipped about -3% after the company issued fiscal 3Q revenue guidance of ~$1.22bn, coming in slightly below consensus, despite reporting a 21% y/y revenue increase and beating 2Q earnings forecasts. They provided a cautious outlook, impacted by ongoing customer incentives and the lingering effects of last year's IT outage. This prompted investor concerns about the pace of future growth and overshadowed otherwise strong financial results and record net new annual recurring revenue.

Snowflake reported a +32% y/y increase in revenue for its fiscal second quarter, reaching $1.14bn and topping analyst expectations. The company’s product revenue was $1.09bn with strong customer growth and a net revenue retention rate of 125%. Alongside raising its full-year 2026 revenue outlook, Snowflake demonstrated robust adoption of its AI and data offerings. Snowflake shares were up +20% this week.

CoStar has completed its $1.9bn acquisition of Domain Holdings, one of Australia’s largest real estate marketplaces, reaching about 7 million Australians monthly. With this move, CoStar aims to boost competition in the Australian property market by combining its global technology and agent-focused approach with Domain’s well-established local expertise and trusted brands. The company plans to accelerate investment in innovation, digital tools, and customer experience, pledging to deliver a more user-friendly and lower-cost platform for agents, sellers, and homebuyers throughout Australia.

Cracker Barrel sparked controversy this week with a logo redesign as part of its $700mn rebrand that removed the classic “Old Timer” in favor of a barrel-shaped wordmark, aiming to highlight inclusivity, but received strong backlash from customers and investors. The stock fell as much as -14% before rebounding +8% after the company announced it would revert to its old logo, with prominent voices, including President Trump weighing in. The chain continues to face challenges beyond branding, with persistent traffic declines, lackluster same-store sales, and long-term operational issues, even as activist investor Sardar Biglari renews pressure on management and some social media users call for CEO Julie Felss Masino to step down.

Kohl’s reported a mixed quarter with a beat in earnings and a miss on revenues. Sales declined -5% and comp sales fell -4.2%. On the call, management called out that consumer spending remains constrained, particularly among lower to middle-income customers. However, they did see improvement in traffic trends in July.

Kohl’s CFO on consumer confidence: “We know our core customer hasn't left us, they've just given us less of their wallet.”

Dollar General shares were up +6% after lifting its earnings guidance for 2025, supported by rising customer traffic, particularly among more affluent shoppers. Same-store sales were up +2.8% for the quarter. They also increased their same-store sales guidance to 2.1-2.6% for the year. They expanded delivery reach with the new Uber Eats partnership.

Tesla's European sales fell ~40% in July to 8,837 units, marking the seventh consecutive month of steep decline, and its market share in the region has dropped to less than 1% amid rising competition, especially from Chinese automaker BYD, whose registrations surged over 200% in the same period.

While this is the 5th edition, we are still experimenting with this format, so if you enjoyed this summary, please drop a comment or like so we know to keep doing it in the future! Feedback welcomed.

Spotlight.

This week, we released our highly anticipated 121-page, extensive research report on LVMH. LVMH is a global holding company led by Bernard Arnault that specializes in luxury goods. They own and operate over 75 “Maisons”, or brands, in six different industries from leather goods to wines to jewelry. Learn more about LVMH here!

So far this earnings season, we have released 10 2Q25 business updates. We have released business updates on Meta, Api Group, Floor & Decor, AppFolio, Coupang, Axon, Airbnb, Evolution, CoStar Group, and DFH.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

APi Group 2Q25 Business Update.

AI Data Center Opportunity: “On the call they noted that the big spend in data centers is also creating a lot of new opportunities for both of their segments. This is likely one of the larger factors that drove the specialty segment’s organic growth this quarter. Still though, they are broadly diversified across end markets. Although it is an open question if they are willing to increase exposure to data center given it is a fast growing market with a lot of service needs and high quality customers.”

Read the full update here: APi Group 2Q25 Business Update

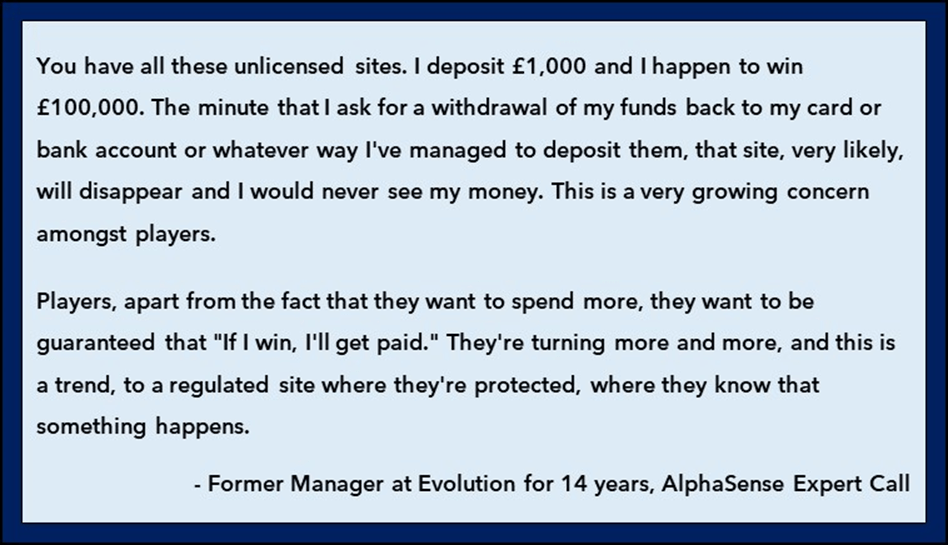

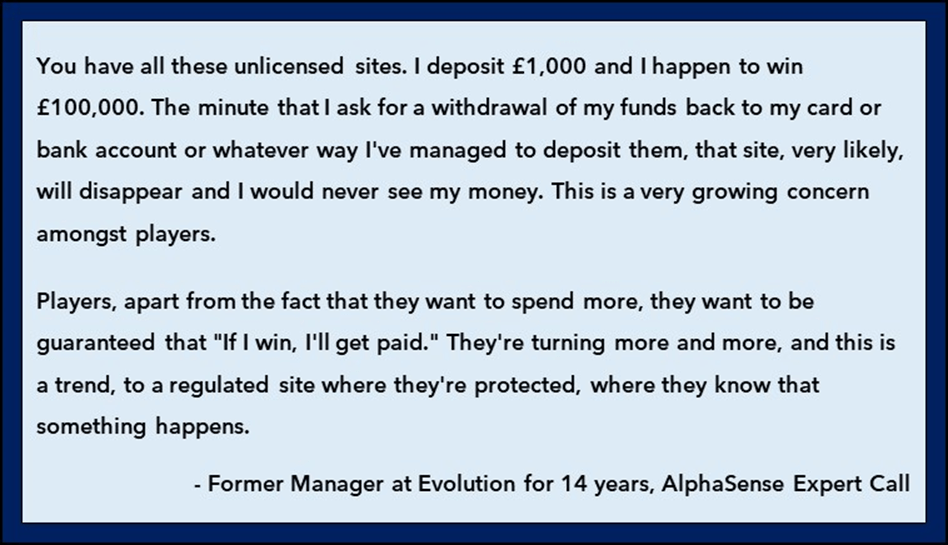

Evolution 2Q25 Business Update.

Preference to Play Legally: “While there may always be an illegal market somewhere, most players prefer to play legally when possible. Players don’t trust websites easily and the unlicensed sites can rip them off with them having no recourse.

Read the full update here: EVO 2Q25 Business Update

The Synopsis Podcast.

This week, we released a dialogue episode covering AppFolio’s latest earnings. In the episode, we break down AppFolio’s 2Q25 business update and share how well AppFolio is competing against its competitors using AlphaSense’s Expert Call interviews. Listen below!

*You can get a free trial of AlphaSense here

Memo of The Week.

The Invisible Competitor

If You Can’t Compete for Customers, Create Them.

“The biggest mistake competitors make is not knowing whether they are competing against a similar service, iterating on a well understood preference, or if they are offering something entirely new, revealing a consumer's latent preference for something that they’ve never seen.”

Read the full memo here: The Invisible Competitor: When Creating Value is Better than Fighting for It

Company Report Snippet: LVMH

Buying a Feeling: “Ultimately, what someone is buying is a feeling. And that is a very hard preference to fill on the Consumer’s Hierarchy of Preferences. Anyone can make a very high quality purse, but getting someone to believe they are more “worthy” for owning your product or building their self-esteem is a very tricky thing to do…”

*This is an excerpt from our new company report on LVMH.

If you are a Speedwell Research Member, read the full report here: LVMH

If you are not already a Speedwell Research member, you can purchase it here: LVMH Individual Report

Upcoming.

Research

We are excited to announce that we are doing an Exploratory Report on Casey’s, a convenience store and gas station chain that also happens to be the 5th largest pizza retailer in the country.

Coverage

We will be sharing updates on PRM and CSU for 2Q25 earnings.

For our latest updates on these names, click here → Business Updates

Copart reports earnings next week

APi Group will be at the Jefferies Mining and Industrials Conference

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Three Definitions of Risk (and Why It Matters) by Altos VC Director of Research Nick Chow (link)

Leandro of Best Anchor Stocks: Never Sell? (link)

Alex Morris of The Science of Hitting (TSOH) Research: The Evolution of a Value Investor (link)

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).