The Investor's Briefing #8

Nvidia Invests in Intel, Factset at 4 Year Lows, Fed Cuts Rates, Meta Neural Band

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the eighth edition of our weekly newsletter: The Investor’s Briefing.

In Financial News.

Financial markets ended the week on a positive note with the S&P 500, Nasdaq 100, and Dow all closing at record levels, driven by tech stocks and a renewed risk appetite following the Fed’s rate cut. The S&P 500 is now up 13.5% YTD. The Russell 2000 advanced 2% this week, achieving its first record close since 2021.

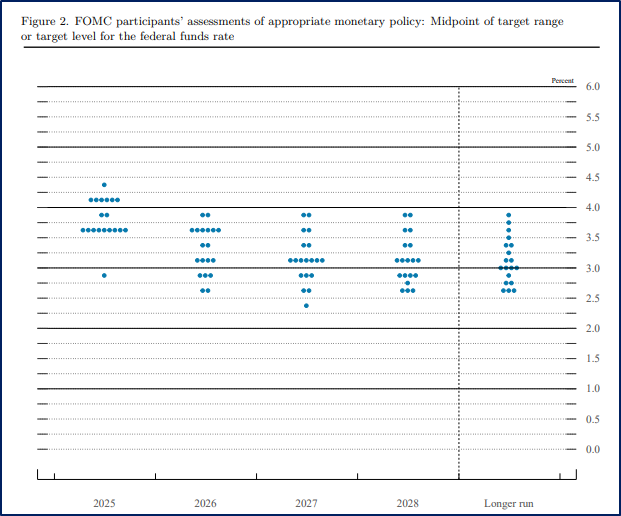

The Federal Reserve cut interest rates for the first time this year, lowering the federal funds rate by 25 bps to 4.00–4.25% with an 11-1 majority. Powell described the move as a “risk management cut,” noting that a “very different picture” of risks has emerged as the labor market has cooled while inflation pressures persist.

“Recent indicators suggest that growth of economic activity moderated in the first half of the year. Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated… Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate and judges that downside risks to employment have risen.” - Fed Statement, September 17th

The rate cut represents a notable shift after the Fed’s extended tightening cycle, yet divisions within the committee underscore how uncertain the path forward remains. Policymakers now expect two more cuts before year-end, up from one in June, though forecasts diverge. One committee member penciled in a year-end rate of 4.4%, above the current range, while another forecasted rates at 2.9%. Looking further ahead, the median projection calls for one additional cut in 2026, yet some officials see room for as many as three. The wide dispersion highlights the lack of consensus on how far easing should go. Powell conceded that with both employment and inflation concerns pressing on the Fed’s dual mandate, “there are no risk-free paths now.”

Complicating matters further, stagflation concerns are bubbling up. U.S. consumer prices rose in August at the fastest pace in seven months, led by housing and food, marking the largest y/y increase since January. Combined with softer labor market data, the uptick in inflation revived fears of stagflation. This mix of weak growth and persistent inflation has not been seen since the 1970s, albeit it is nowhere near as drastic. These risks complicate the Fed’s ability to support the jobs market with aggressive rate cuts.

At the same time, political dynamics also remained in focus. Governor Stephen Miran, who is a Trump-backed governor that was recently sworn in, cast the lone dissenting vote in favor of a larger 50 bps cut. Meanwhile, Governor Lisa Cook—who had been dismissed by Trump—was reinstated by a late court ruling and allowed to participate while the legality of her removal is still being adjudicated. Powell reiterated that decisions are based on economic data, emphasizing the Fed’s independence despite the executive branch expressing vocal policy opinions.

Treasury yields initially fell on expectations of further easing, but longer-dated bonds pared back declines as investors digested the Fed’s divided “dot plot.” For investors, the combination of divided policy signals, lingering stagflation risks, and an active political backdrop suggests volatility across equities and bonds may persist.

In other news, President Trump has asked the Securities & Exchange Commission (SEC) to consider ending the 1970 mandate requiring quarterly earnings reports, shifting to semiannual disclosures. While framed as deregulation, the move faces pushback from institutional investors who argue that frequent reporting underpins transparency and lowers the cost of capital.

History suggests little would change. Europe and the U.K. dropped mandates a decade ago, but many companies continued to release some information—even if just revenue figures—voluntarily under investor pressure. Investor reception to such a move is mixed based off their investing style. In 2018, Warren Buffett and Jamie Dimon urged companies to move away from issuing quarterly EPS guidance, arguing it fostered short-termism.

However, critics warn that less frequent disclosure could increase volatility and obscure material development. One recent example is General Motors’ July disclosure that tariffs had cut $1.1 billion from earnings, which drove shares down -8%. Although, such disruptive events are rare and companies can put out special annoucements in the interim, as many did during early days of Covid.

Ultimately, the discussion reflects a longstanding tension in U.S. capital markets: the believe that more information always equates to better decision making against the idea that tracking short-term figures are likely to lead to short-term decisions.

Company News.

Meta Expands their Push into Smartglasses with New AI-Enabled Models at the Latest Meta Connect Event

Meta unveiled its latest smartglasses at its annual hardware and developer conference on Wednesday, as the company continues to bet on wearable computing.

The new glasses, priced at $799 and available Sept. 30th, feature a small built-in display and can be controlled through subtle hand movements captured by a wristband device known as the Neural Band. The Neural Band is a potential game changer for the device as it lets users discretly navigate the glasses without voice commands, which are too invasive for public use.

Mark Zuckerberg emphasized their commercial readiness, noting in his keynote: “This isn’t a prototype. This is here, it’s ready to go.” He demonstrated the product live on stage; however, an attempted video call with CTO Andrew Bosworth faltered on the first try.

Meta first entered the category in 2021 through a partnership with Ray-Ban owner EssilorLuxottica. At that time, adoption was limited. Early models focused narrowly on photo and video capture. Showing the lack of product market fit, less than one in ten pairs were still in active use two years after purchase. By contrast, a second-generation redesign launched in 2023 proved far more successful. EssilorLuxottica said earlier this year that sales had surpassed two million pairs, and, importantly, it plans to scale production capacity to 10 million units annually by 2026.

In addition to its flagship release, Meta introduced an updated Ray-Ban line and a sports-focused version developed with Oakley, also owned by EssilorLuxottica. These models integrate an AI assistant capable of interpreting the user’s environment, supporting functions such as voice-enhanced conversations called “conversation focus”, audio playback, and photo and video capture.

Meanwhile, competition in the space is intensifying. OpenAI, in collaboration with former Apple designer Jony Ive, is developing an AI “companion” device. Similarly, Google has partnered with Warby Parker and luxury house Kering to release AI-powered glasses after 2025. Snap, for its part, plans to launch augmented-reality eyewear next year, while Amazon already sells glasses with audio and calling features.

While many may have thought this was Apple’s market to take after they essentially invented the smartphone category with the iPhone, the Vision Pro has struggled to gain meaningful adoption or use. Meta seems to be the best postioned currently and seems to have an infinite appetite to spend money to capture the opportunity.

Finally, Meta used the conference to reinforce its broader hardware ecosystem, previewing new content for its Quest virtual-reality headsets. For Zuckerberg, smartglasses are more than another product release; rather, they represent a step toward restoring what he calls “a feeling of presence” that, in his view, has been diminished in the smartphone era.

Nvidia to Invest $5 Billion in Intel

Nvidia agreed to invest $5 billion in Intel and co-develop chips for PCs and data centers, a surprise move that underscores Intel’s efforts to stabilize its business and regain relevance in an industry it once dominated. The deal sent Intel shares up 23% to $30.57, their largest single-day gain since 1987, while Nvidia gained 3.5% to $176.32.

Under the agreement, Nvidia will purchase Intel stock at $23.28 a share, taking a stake of less than 5%. Intel will design custom X86 CPUs that integrate with Nvidia’s GPUs, while also embedding Nvidia graphics technology in upcoming PC processors. The partnership, valued by Nvidia CEO Jensen Huang at a potential $50 billion, allows each company to expand into segments where it has been less competitive. For Intel, the tie-up bolsters its data-center offering against AMD and Arm-based designs. For Nvidia, it extends reach into PCs and edge computing.

Moreover, the investment builds on recent government and corporate support for Intel. In August, the U.S. government converted $9 billion in grants into equity, taking a 10% stake now worth about $14 billion. Last month, SoftBank committed $2 billion, adding to Intel’s cash reserves as it works to finance costly manufacturing upgrades. These moves reflect growing recognition that Intel, once Silicon Valley’s dominant chipmaker, must secure new sources of capital and partnerships to compete in AI and advanced semiconductors.

Still though, challenges remain. While Intel continues to lead in X86 CPUs, its manufacturing unit lags behind TSMC’s. Most chips under the Nvidia deal will still be fabricated by TSMC before being packaged by Intel, underscoring the gap in manufacturing. Intel lost nearly $3 billion last quarter in its foundry division, which is central to its turnaround strategy, and the U.S. government’s plan to onshore more chip production.

At the same time, the partnership also highlights shifting dynamics across the semiconductor industry. As recently as 2022, Intel generated more than twice Nvidia’s revenue. But Nvidia’s early bet on AI accelerators transformed its position: the company is on track to post $200 billion in sales this year, with their quarterly revenue soon expected to exceed Intel’s annual revenue.

For Intel, the agreement offers both financial support and product validation at a critical juncture. For Nvidia, it broadens compatibility and strengthens its ecosystem without compromising its core GPU dominance. Whether the collaboration signals a lasting realignment or a tactical move remains to be seen, but it underscores how strategic alliances and political backing are reshaping the global chip landscape.

FactSet Shares Hit a Four-Year Low as Tech Cost Squeeze Margins

FactSet shares fell 20% to $290 this week, extending their 2025 decline to 39% and marking the lowest level since 2021. The drop came after the company issued earnings guidance that fell short of investor expectations.

Specifically, management projected fiscal 2026 adjusted earnings of $16.90 to $17.60 a share, about 4% below the $18.25 consensus. At the same time, operating margin is expected to narrow to 34%–35.5% from 36.3% last year. According to management, the decline reflects heavier technology spending to expand cloud and analytics offerings.

Investors though are worried this is indicative of a broader landscape shift where competitiveness of AI-native companies weighs on profits as incumbents have to spend heavily to overcome tech debt. FactSet’s investment has widened vs other data analytics peers. While S&P Global and MSCI sustain margins near 50% thanks to their high-margin ratings and index businesses, FactSet has a more susceptible moat, which is requiring a higher spend to keep their products competitive.

Moreover, client pressures compound the challenge. Asset managers and banks are focused on expense reductions, limiting their willingness to absorb price hikes. While a sluggish capital markets backdrop dampens demand for premium analytics. Consequently, the market sees FactSet’s margin step-down as structural, not temporary. FacSet now trades at 19x earnings.

We changed up the format of the company section to extend the story of each company. If you enjoyed this, please drop a comment or like so we know to keep doing it in the future! Feedback is always welcomed.

Spotlight.

This week, we released a 2Q25 business update on RH!

This is in addition to the 13 other 2Q25 business updates. We have released business updates on Meta, Copart, APi Group, Floor & Decor, AppFolio, Coupang, Axon, Airbnb, Evolution, CoStar Group, Perimeter Solutions, Constellation Software, and DFH.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

RH 2Q25 Business Update.

Is RH Luxury?: “We wouldn’t feel compelled to argue that RH is a “true” luxury brand. Rather RH is a high-end brand that uses its elevated branding as a customer acquisition strategy to circumvent the typical designer trade heavy business.”

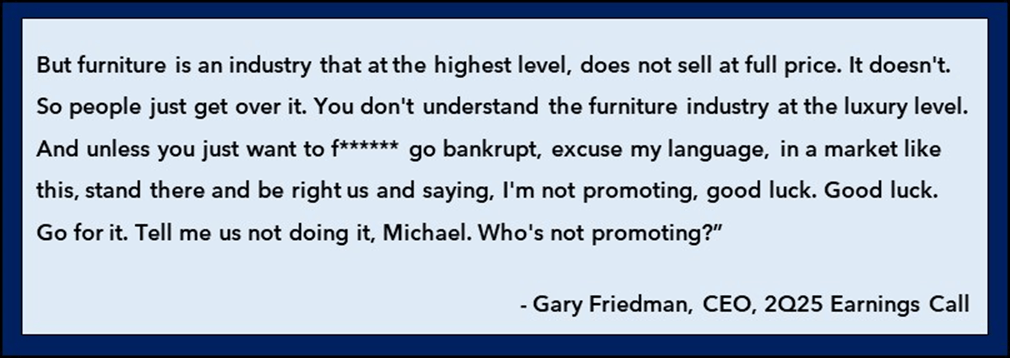

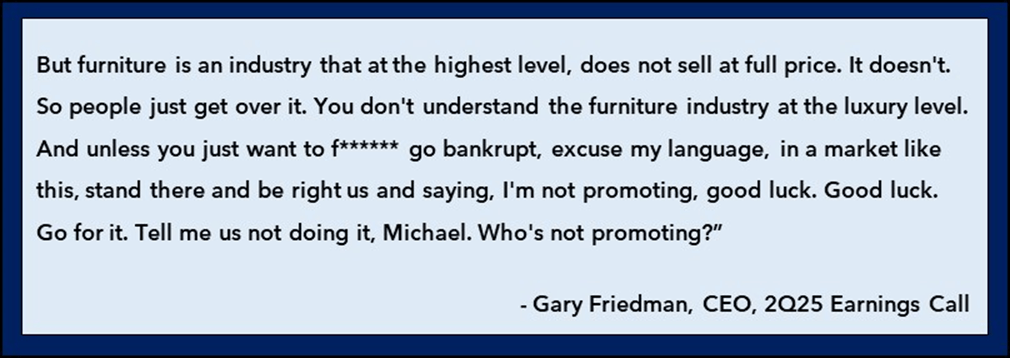

Gary Friedman On Tariffs:

Read the full update here: RH 2Q25 Business Update

LVMH Thread 🧵

Read our deep dive on LVMH here: LVMH Deep Dive

The Synopsis Podcast.

This week, we released a new dialogue episode on RH’s 2Q25 earnings, examining how the company is navigating tariffs, the significance of its Paris opening, and whether furniture is “luxury”. We also explore the implications of OpenAI’s $300 billion deal with Oracle. Listen below!

Memo of The Week.

How Apple, Bloomberg, & Amazon Kept Strategic Coherency

Clay Christensen’s theories on disruption and “Jobs to Be Done” framework shaped how we think about business strategy, but he didn’t always get it right. His prediction that Apple would falter misunderstood the deeper role of consumer preferences and integration. By exploring cases from A&P’s early grocery chains to Bloomberg’s shift away from hardware, to Amazon’s bold in-housing of logistics and the birth of AWS, we see a clearer picture: modularity is not simply about outsourcing, but about aligning with what customers truly value. Sometimes outsourcing creates efficiency; sometimes integration creates differentiation. The challenge and opportunity for business leaders is knowing when to modularize, when to keep control, and when integration becomes a competitive advantage.

Read the full memo here: Understanding Modularity: How Apple, Bloomberg, & Amazon Kept Strategic Coherency

Company Report Snippet: Dream Finders Homes (DFH)

DFH’s “Capital-Light” Strategy: “The “capital-light” strategy means that they do not buy land until they are ready to build a house on it and they do not build a house until they usually know they have a buyer. This is in contrast to most builders who will hold many thousands of acres of land in advance of building on it. They do this because they want to ensure that they will have land in desirable areas far ahead of actually needing it. However, land prices can be much more speculative than real estate prices, and are thus more volatile.”

*This is an excerpt from our company report on DFH.

If you are a Speedwell Research Member, read the full report here: DFH

If you are not already a Speedwell Research member, you can purchase it here: DFH Individual Report

Upcoming.

Research

Current research report in progress: Exploratory Report on Casey’s, a convenience store and gas station chain that also happens to be the 5th largest pizza retailer in the country.

AlphaSummit 2025

AlphaSense is hosting its AlphaSummit October 6-8 in Brooklyn, New York. It is a transformative event for leaders redefining market intelligence. You will hear from industry visionaries and executives, participate in interactive product sessions and expert-led workshops, and connect with research leaders in your field. AlphaSummit is your chance to learn, network, and become part of a community reshaping the future of market intelligence.

Register Your Spot Here and Get 15% Off!

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: Paul Buchheit and Dalton Caldwell (2025) (link)

Mark Leonard- Constellation Software Shareholder Letter (2009) (link)

Terry Smith- Fundsmith’s Inaugural Letter (2011) (link)

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).