The Investor's Briefing #9

Investor Doubt Creeps into Constellation Software and Copart, with both down 30% from Peak

Welcome to Speedwell Research’s Newsletter. We write about business and investing. Our paid research product can be found at SpeedwellResearch.com. You can learn more about us here.

This is a weekly briefing, where we summarize key financial news in the week and recent content you may have missed. You can listen to this Investor’s Briefing on Spotify or Apple Podcasts too.

Welcome to the ninth edition of our weekly newsletter: The Investor’s Briefing.

In Financial News.

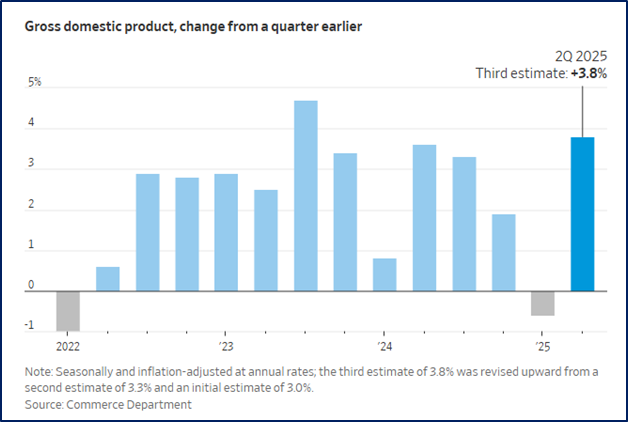

The U.S. economy expanded at a faster pace this spring than initially reported, reflecting resilient consumer spending and robust business investment. However, the housing market continues to struggle under the weight of high prices and elevated mortgage rates, underscoring the uneven conditions across sectors.

Revised Commerce Department data underscored the economy’s resilience. 2Q GDP expanded at a 3.8% annualized pace, up from an earlier estimate of 3%, marking the fastest growth in nearly two years. Consumer spending rose 2.5%, led by service spending. At the same time, business investment provided a further boost, with intellectual property spending, such as R&D and software, advancing 15%, the strongest gain since 1999. In addition, AI-related infrastructure contributed meaningfully, as companies invested in data centers at a annualized rate of $40 billion, more than quadruple the level recorded in early 2020, mirroring the late-1990s wave of telecom buildouts.

However, this robust second-quarter performance contrasted sharply with last quarter, which was revised downard to show a 0.6% contraction as companies accelerated imports ahead of new tariffs. Historically, tariff cycles have often distorted trade flows; a similar pattern occurred in 2018 when businesses front-loaded shipments before the Trump administration’s first round of duties on Chinese goods.

Since then, more recent indicators have been mixed. On one hand, July and August retail sales point to resilient consumer demand, echoing the strength seen during the early post-pandemic reopening in 2021. On the other hand, hiring has slowed and inflation pressures remain persistent. As Fed Chair Jerome Powell emphasized last week, there is “no risk-free path” to balancing price stability with labor market health, language reminiscent of Alan Greenspan’s caution during the late 1990s, when growth and asset markets ran ahead of inflation control.

Meanwhile, housing data illustrate the limits of consumer strength. Existing home sales edged down 0.2% in August to a 4 million unit annualized rate, according to the National Association of Realtors. Although the decline was smaller than expected, sales remain stuck at historically low levels for the third consecutive year. For perspective, annual sales averaged nearly 5.5 million units during the decade before the pandemic. Meanwhile, the median home price increased 2% from a year earlier to $422,600, the highest on record for August. Prices have now climbed 52% since 2019, keeping affordability strained.

Moreover, mortgage rates have offered little relief. After briefly dipping to an 11-month low earlier this month, the 30-year fixed rate has climbed back to 6.3%. While analysts expect additional Fed rate cuts later this year, much of the benefit may already be reflected in mortgage pricing. Historically, mortgage markets tend to react quickly to Fed signals, as in 2019, when rates fell ahead of the central bank’s “insurance cuts”.

On the supply side, inventories have grown modestly, giving some buyers leverage to negotiate concessions. Yet listing growth is slowing, and weakness remains concentrated in markets such as Florida and Texas. In some cases, owners are delisting properties altogether as homes linger too long on the market. By contrast, new-home sales increased 21% in August, the largest monthly gain in three years, as builders relied on incentives, like mortgage buy downs, which temporarily reduce the mortgage’s interest rate to stimulate demand. It seems that the housing market is holding out for lower rates and is still digesting the elevated covid activity when some mortgage rates dropped below 3%.

Against this backdrop, markets ended the week about flat. However, this was only after the S&P 500 rebounded 0.6% on Friday after the August core PCE reading, which rose 2.9% y/y in line with expectations and reinforced confidence in an October Fed rate cut.

Company News.

Constellation Software Says AI Brings Promise and Risks, But No Existential Threat Yet

Constellation Software devoted its latest investor call to AI, striking a balance between optimism and caution. Founder Mark Leonard and senior executives acknowledged AI’s potential to reshape vertical market software (VMS) but emphasized that the technology poses no immediate threat to the company’s business model.

Leonard opened with a parable on forecasting. He recalled Geoffrey Hinton’s 2016 prediction that AI would quickly displace radiologists. Nine years later, U.S. board-certified radiologists had risen 17% to 30,500. “Geoff wasn’t wrong about the applicability of AI to radiology,” Leonard noted. “Where he was wrong was that the technology would replace people. Instead, it’s augmented people.” For Leonard, the lesson is clear: even experts misjudge how technology will alter professional structures. He suggested the same uncertainty applies to programming today, which may be entering either a “renaissance or a recession.”

The discussion then turned to software customization. VMS has long operated between low-cost, general-purpose applications and bespoke systems tailored to client needs. Leonard argued AI could accelerate customization, but it also shifts power toward clients who may increasingly adapt products themselves. “Whenever we go see a large client’s IT director, we’re in a negotiation regarding what we’ll do and what they’ll do,” he said. “It’s not going to be an easy answer. It’s going to be somewhere in between.”

On productivity, Leonard pushed back against inflated claims. While AI tools may promise “10x improvements” in coding output, he warned that poorly designed applications risk generating costly bugs and rigid systems. “You may give up on the roundabouts what you made on the swings,” he said.

Executives also stressed that Constellation’s competitive advantage lies less in data than in decades of accumulated process knowledge. “Our businesses have incredible knowledge of the end users’ processes and workflows, often better than the end users themselves,” one said. Leonard added that VMS represents the “distillation of a conversation between the vendor and the customer that has gone on frequently for a couple of decades,” and AI offers new ways to reexamine and improve those exchanges.

Far from shrinking budgets, management argued that AI could expand them by deepening the scope of software deployment. “It could be that software budget will become much bigger because of the broadening and deepened scope,” one executive said, positioning AI as central to competitive differentiation.

On capital allocation, Leonard said AI has not changed the firm’s approach to acquisitions. “We are opportunity constrained,” he said. “Narrowing the aperture is a bad idea. We end up sitting on a whole pile of cash… AI isn’t reducing what we’re looking at. It may influence pricing on certain things, but it isn’t changing much in the M&A world.”

He closed by urging investors to apply skepticism amid the AI narrative. “Predicting the future [is] really, really hard, particularly at times like these,” Leonard said. “But monitoring what’s happening in real time, a whole lot easier; just approach it with a healthy skepticism.”

Shares are now down almost 30% from peak as investors fear that AI will lower the cost to produce software, making it viable for even small businesses to cheaply create custom software. Said differently, this is essentially a cost reduction for these businesses. However, it is important to note that most businesses are not particularly price sensitive to their software currently, as it is a small portion of their overall costs and mission critical.

The reason why VMS software is so sticky in the first place is because of a fear of disruption and the lopsided risk/ benefit of replacing an existing solution. Saving a little bit of money by switching to a competitor’s offering versus the headache of replatforming a system and risking an outage, which could result in unrecoverable sales, is what has kept businesses on their existing solution for decades. AI allowing for a lower cost product doesn’t address this aspect that has traditionally prevented customers from switching.

Further adding to investor trepeidation though was the announced resignation of Founder and CEO Mark Leonard on Thursday due to health reasons. This was unexpected and the timing of it alongside this AI call made some wonder whether the two could be related with the subtext being that Leonard was not fit to lead in an AI era.

On the other hand, Constellation Software has worked on decentralization for decades, grooming executives to take on greater responsibilities as the company acquired more businesses and siloed operations as they scaled. This all means that Mark Leonard has been making little to no actual operational decisions for decades, but rather sets the investment tone and strategy, something that is already well enmeshed in Constellation’s culture. COO Mark Miller was announced to fill his role as President.

VP at Openlane Sees Copart Losing Market Share

In a recent AlphaSense Expert Call, a veteran auto-industry executive at Openlane described how structural tailwinds and shifting competitive dynamics are reshaping the salvage auction market. OpenLane was formerly called KAR Global, which owned a few auto related services, including IAA, which they spun off in 2019.

Corroborating what Copart has long said, this executive sees rising total-loss volumes as a structural phenomenon. He noted that high repair costs, driven by increasingly complex technology, make it more economical for insurers to declare vehicles a total loss. “Insurance companies are totaling them out because of the expense of the computers and the digital,” he said, adding that tariffs are likely to push prices higher still. “I definitely think total loss is going to continue to climb.” Copart has mentioned this many times in the past several years.

This executive believes that electric vehicles could further extend this trend. Battery replacement remains a significant unknown, both in cost and longevity. “We’re a little too young on the life cycle to really understand what the battery is, how long they’re going to last, how much they cost,” he observed. “A dealer told me it was like $70,000 for a battery in a truck he had to fix. At some point, the batteries wear out. What does that look like for a consumer? We’re just a little bit too early stages to really know that yet.”

On competition, the executive argued that the merger of Ritchie Bros. and IAA has created a larger rival with scale, brand reach, and M&A capacity. “With IAA and Ritchie Bros. combining their strategies and their assets and their technology, they’re the bigger giant in the room right now,” he said, estimating they could capture an additional 10–15% market share. He believes Copart retains advantages in digital execution and user experience, but expects the combined Ritchie Bros. / IAA to edge ahead, perhaps leaving the industry split 60/40.

He added that while Copart’s real estate ownership remains strategically useful, it is less decisive in a digital-first environment. Over time, both companies could repurpose land for service bays and reconditioning. Looking forward, technology will be the next battleground. “If they can leverage AI somehow to build out their pricing [and] repair costs, certainly, they should be investing in that,” he said. He also flagged the potential for consumer-driven platforms where cars are listed directly to buyers in auction-style formats.

Copart’s stock is down almost 30% from peak, as investors fear that Copart is losing market share for the first time ever. In the past 2 quarters Copart noted that they had negative insurance volumes, while Ritchie Bros reports gaining share. Copart attributes this to fewer insured drivers which means the insurance companies they contract with have fewer damaged vehicles to send to Copart. While seeing negative volumes is never comforting, their reasoning makes sense. It is key to note that (as far as we know), Copart hasn’t actually lost any customers.

This executive seems to capture well the worst fears investors have about Copart today. However, they are poorly reasoned and lack context. IAA has been a business that has been traded around several times in the past couple decades. What this has meant is a lot of short-term decisions that make it hard for them to operate as well as Copart. The executive seems to dismiss Copart’s ownership of land as a key differentiator, making a comment about a “digital first world” which doesn’t seem to have much susbtance behind it. The land is also particularly important during CAT events where that excess land allows for quicker service during what is typically a churn event for insurers (taking a month to get a customer cash after their vehicle is totaled and sits outside their home is the surest way to get them looking for new insurance providers).

The executive also notes that Ritchie Bros and IAA can combine their assets, but as readers of our orginal Copart report know, only land with special approvals for salvage vehicles can carry the damaged cars. It is unlikely any of Ritchie Bros. existing footprint has this approval, or will be able to get it because people heavily protest salvage yards as the potentially toxic liquid can drip onto the ground and seep into water.

What is lacking from the experts commentary is any reasoning why someone would prefer IAA over Copart. IAA may be improving their systems and technology, but that is only relatively to the very inept job they were doing prior. The real test anyway will be what happens the next time there is a large CAT event and all of their systems are stressed. Copart prepares and trains for this with 10x surge capacity in certain areas to accomodate excess volume.

It is also probably true though that IAA was so poorly managed prior that improving operations is helping boost their business. But there is no evidence this is hurting Copart and Copart’s growth markets are internationally anyway, where IAA has near no presence.

This is from an AlphaSense Expert Call Interview.

You can get a free trial of AlphaSense here

CarMax Earnings Show Auto Industry Strain

CarMax, the largest used-car retailer, posted steep declines in sales and profit last quarter, sending shares down 20%. Management noted that some buyers accelerated purchases earlier in the year to avoid tariff-related uncertainty, leaving weaker demand in recent months. Loan performance at its finance arm also deteriorated, forcing higher loss provisions. “The consumer has been distressed for a little while,” CEO Bill Nash said, adding that “even creditworthy buyers are hesitant.”

Elsewhere, automakers are adjusting to account for this softness and change in consumer preferences. Ford is offering cheaper financing to clear unsold F-150 pickups, while Honda is scrapping its electric Acura SUV after one year. Other brands are discounting EVs ahead of the expiration of federal tax credits. Meanwhile, Tricolor, a Dallas-based subprime lender and dealer, collapsed into bankruptcy, and First Brands, a major parts supplier, is preparing to seek protection with more than $6 billion in debt. Bosch, the world’s largest supplier, said it will cut 13,000 jobs globally.

For now, overall sales remain supported by a rush into EVs ahead of credits expiring, with September volumes projected to rise 28% y/y. Yet sales of gasoline and hybrid models, the bulk of the market, are expected to fall 2.5%. Vehicle prices remain elevated, up 2.9% over the past year to nearly $45,800, while incentives have stayed flat.

Tariffs on steel, aluminum, and parts continue to raise costs, though trade deals with the U.K., EU, and Japan capped some duties at 15% instead of 25%. Still, the combination of higher prices, tighter credit, and cautious consumers underscores the fragility of the industry at a time of major transition.

We changed up the format of the company section to extend the story of each company. If you enjoyed this, please drop a comment or like so we know to keep doing it in the future! Feedback is always welcomed.

Spotlight.

Check out all of our 2Q25 business updates we have released on Meta, Copart, APi Group, Floor & Decor, AppFolio, Coupang, Axon, Airbnb, Evolution, CoStar Group, Perimeter Solutions, Constellation Software, RH, and DFH.

Become a Speedwell Research Member to gain access to all extended versions of all of our updates, as well as our library of in-depth research reports! Click here to learn more.

Below are select quotes from our most recent business updates & recaps

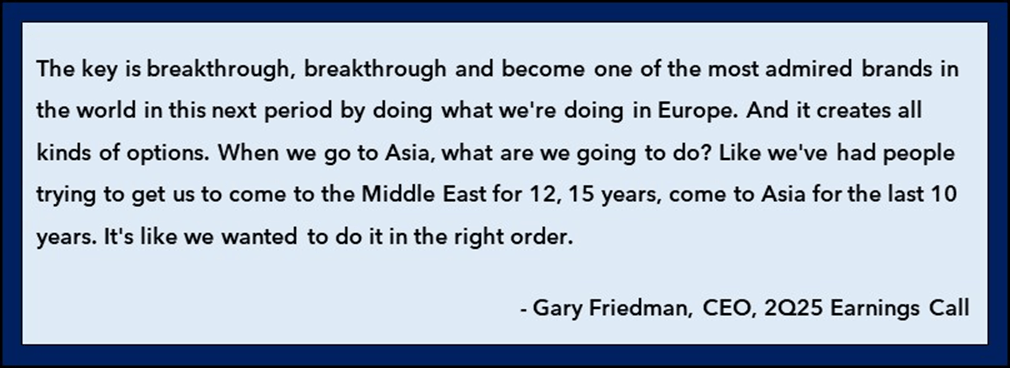

RH 2Q25 Business Update.

Gary Friedman On Expanding Internationally in the Right Order:

Read the full update here: RH 2Q25 Business Update

The Synopsis Podcast.

This week, we released a new interview episode! In this interview, we sat down with a head of M&A from Constellation Software to talk about copycats, style drift, organic growth, and much more.

*This episode was originally recorded during an AlphaSense webinar we hosted in late July. Many thanks to AlphaSense for making this conversation possible. Listen below!

Memo of The Week.

If the Model Doesn’t Work, Don’t Fix It: A look at Traditional Apparel Retailers, Zara, and Shein

The apparel industry is a game of uncertainty, where styles change overnight, weather can wreck sales, and a single misstep can spiral into discounting, brand damage, or even bankruptcy. Traditional retailers gamble months in advance, placing bulk orders without knowing what customers will actually want. Zara disrupted this model by creating “fast fashion,” shortening lead times and betting on small batches that could be quickly scaled if popular. Shein took the model further, flooding the market with micro-batches and relying on consumer feedback, influencer marketing, and data-driven reorders to outpace competitors. Both companies solved the same problem, how to manage demand when you can’t predict it, by restructuring their businesses around entirely different approaches.

Learn more about the story of Zara and Shein in this memo here 👇

If the Model Doesn’t Work, Don’t Fix It. A look at Traditional Apparel Retailers, Zara, and Shein.

Company Report Snippet: Perimeter Solutions (PRM)

PRM’s Decentralized Structure: “While they only operate two segments, they note that they structure their operations into 7 business units, in a structure somewhat reminiscent of Constellation Software. This allows for more decentralized decision making and accountability. Each business unit has a business unit manager that is incentivized on operational and financial results of the individual business unit.”

*This is an excerpt from our company report on PRM.

If you are a Speedwell Research Member, read the full report here: PRM

If you are not already a Speedwell Research member, you can purchase it here: PRM Individual Report

Upcoming.

Research

Current research report in progress: Exploratory Report on Casey’s, a convenience store and gas station chain that also happens to be the 5th largest pizza retailer in the country.

AlphaSummit 2025

AlphaSense is hosting its AlphaSummit October 6-8 in Brooklyn, New York. It is a transformative event for leaders redefining market intelligence. You will hear from industry visionaries and executives, participate in interactive product sessions and expert-led workshops, and connect with research leaders in your field. AlphaSummit is your chance to learn, network, and become part of a community reshaping the future of market intelligence.

Register Your Spot Here and Get 15% Off!

If you enjoyed this investor’s brief, subscribe so that you don’t miss a single update!

Sharing Links.

Check out Speedwell Research’s Drew Cohen’s YouTube Channel. It is focused on general investing and business content.

Other Links.

A Letter a Day: David Tepper (2025) (link)

Mark Leonard- Constellation Software President Letter (2017) (link)

Howard Marks Reflects on Long-Term Capital Management (1998) (link)

And a special thank you to Matthew Harbaugh for helping put this weekly recap together!

The Synopsis Podcast.

Follow our Podcast below. We have four episode formats: “company” episodes that breakdown in-depth each business we write a report on, “dialogue” episodes that cover various business and investing topics, “article” episodes where we read our weekly memos, and “interviews”.

Speedwell Research Reports.

Become a Speedwell Research Member to receive all of our in-depth research reports, shorter exploratory reports, updates, and Members Plus also receive Excels.

(Many members have gotten their memberships expensed. If you need us to talk with your compliance department to become an approved vendor, please reach out at info@speedwellresearch.com).